CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Ex. 11–25

a. OfficeMax:

=Earnings per Share

Net Income – Preferred Dividends

Avg. Number of Common Shares Outstanding

11-21

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–1A

1.

Total Per Per

Dividends Total Share Total Share

2009………… $ 18,000 $18,000 $0.45 $ 0 $0.00

2. Average annual dividend for preferred: $0.75 per share ($4.50 ÷ 6)

PROBLEMS

Year

Preferred Dividends Common Dividends

11-22

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–2A

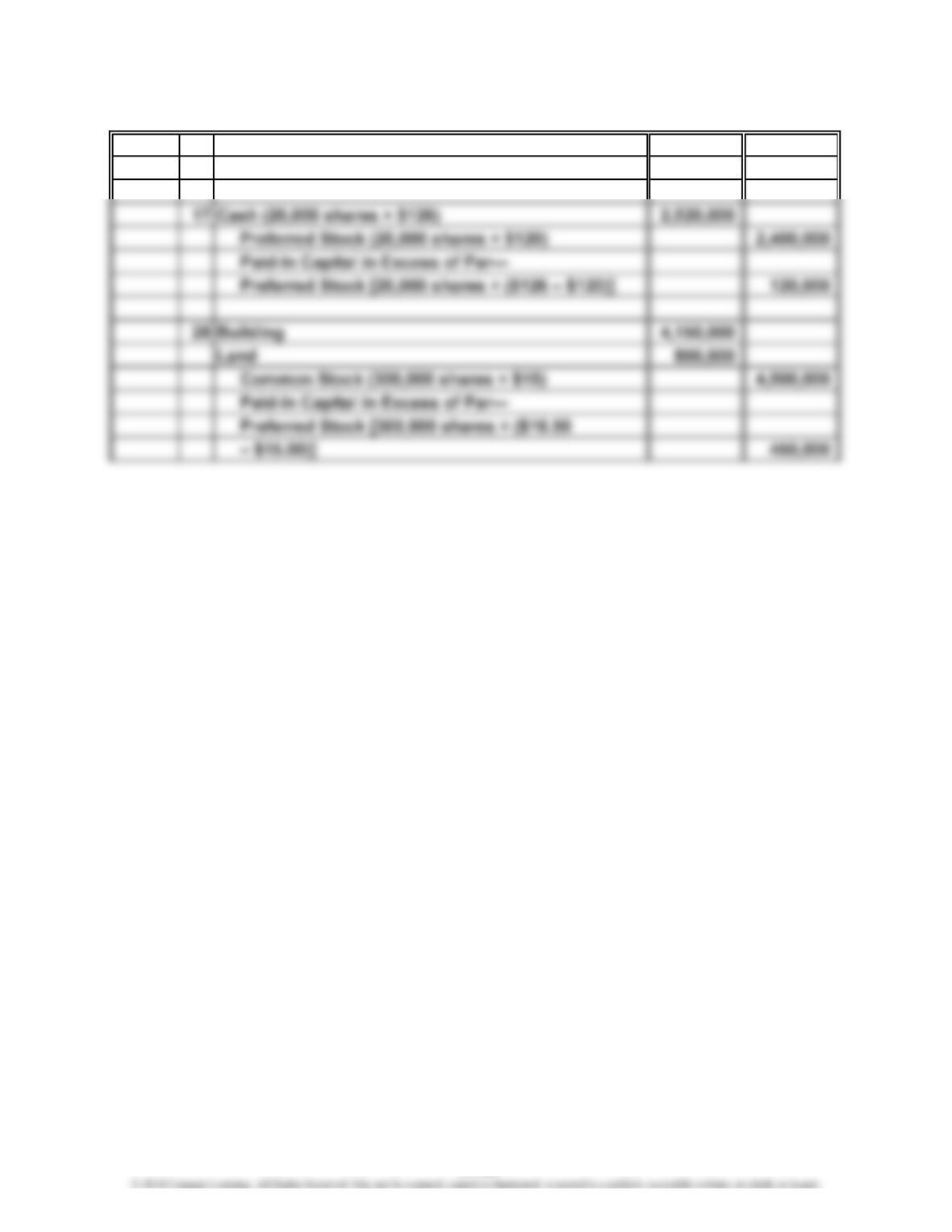

11 Building 3,375,000

Land 1,500,000

May

11-23

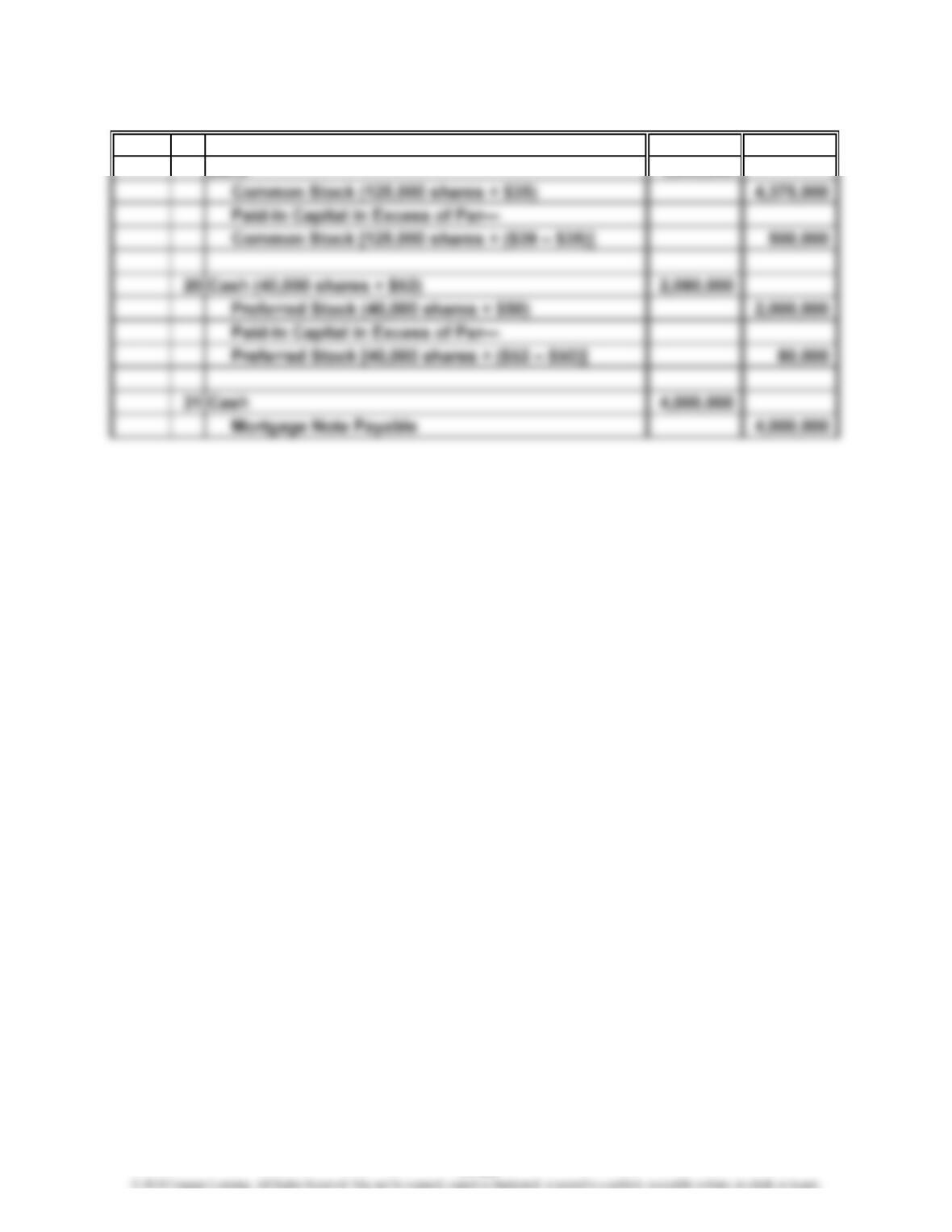

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–3A

a. Cash (360,000 shares × $22) 7,920,000

Common Stock (360,000 shares × $12) 4,320,000

d. Cash (51,000 shares × $21) 1,071,000

Treasury Stock (51,000 shares × $18) 918,000

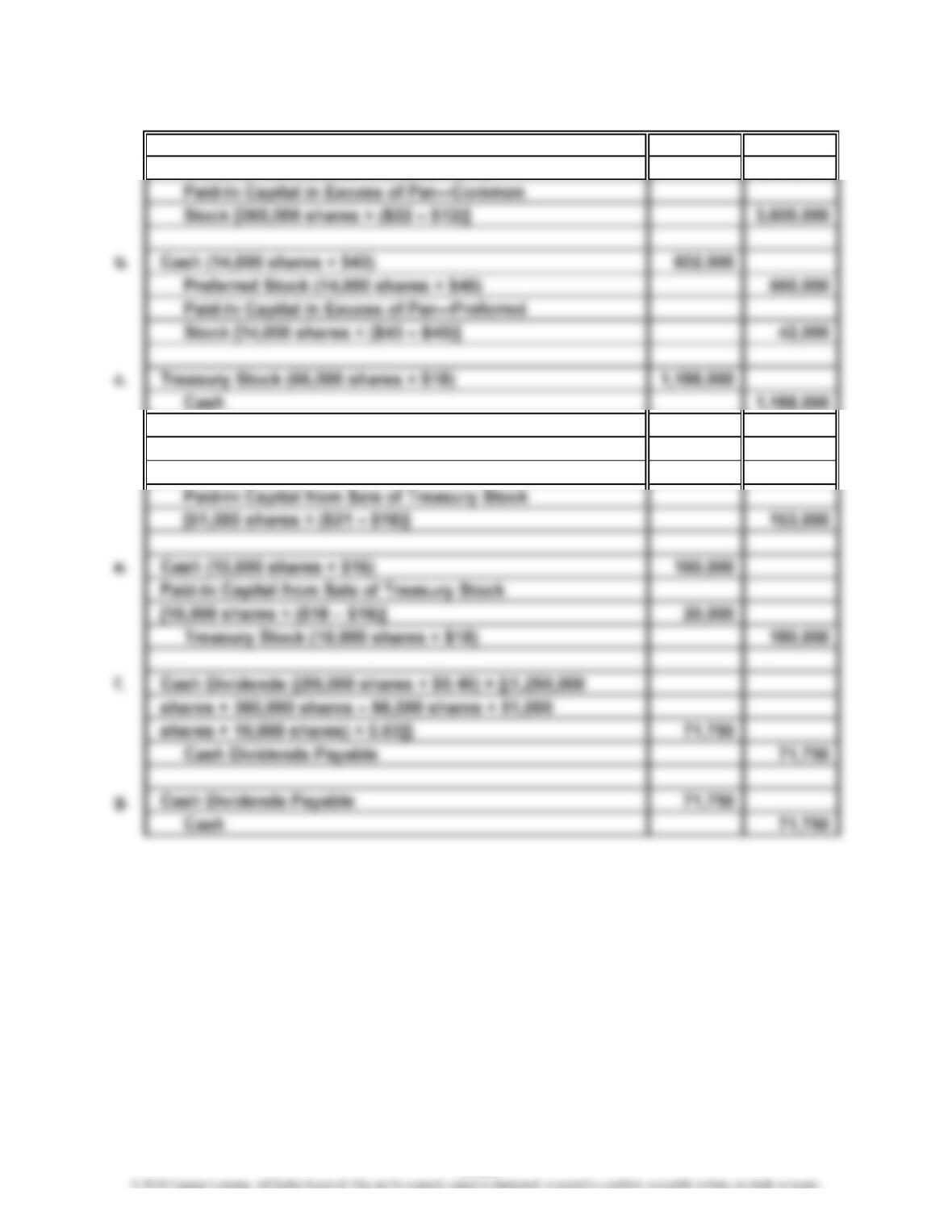

11-24

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–4A

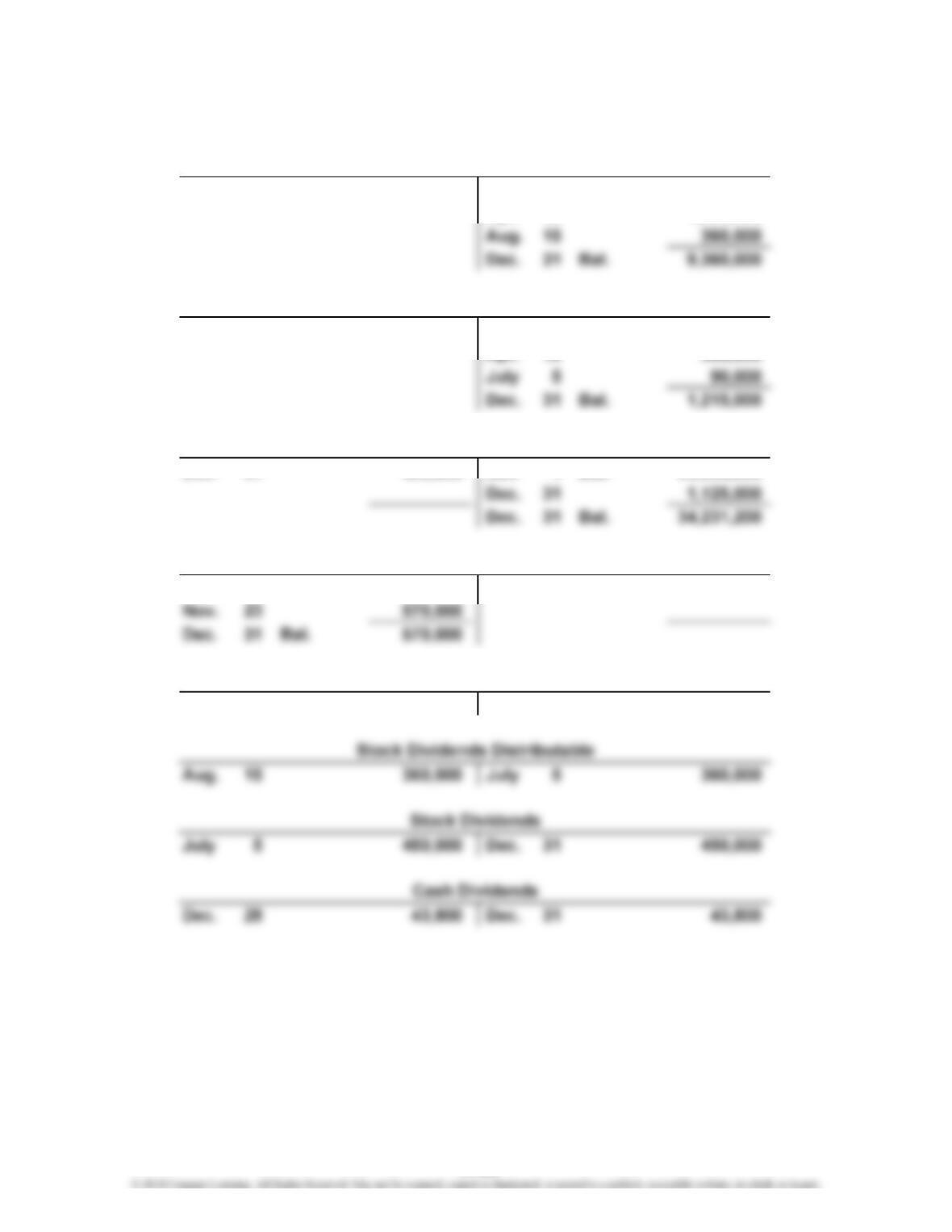

1. and 2.

Jan. 1 Bal. 7,500,000

Apr. 10 1,500,000

Jan. 1 Bal. 825,000

Apr. 10 300,000

Dec. 31 493,800 Jan. 1 Bal. 33,600,000

Jan. 1 Bal. 450,000 June 6 450,000

June 6 200,000

Common Stock

Paid-In Capital in Excess of Stated Value—Common Stock

Retained Earnings

Treasury Stock

Paid-In Capital from Sale of Treasury Stock

11-25

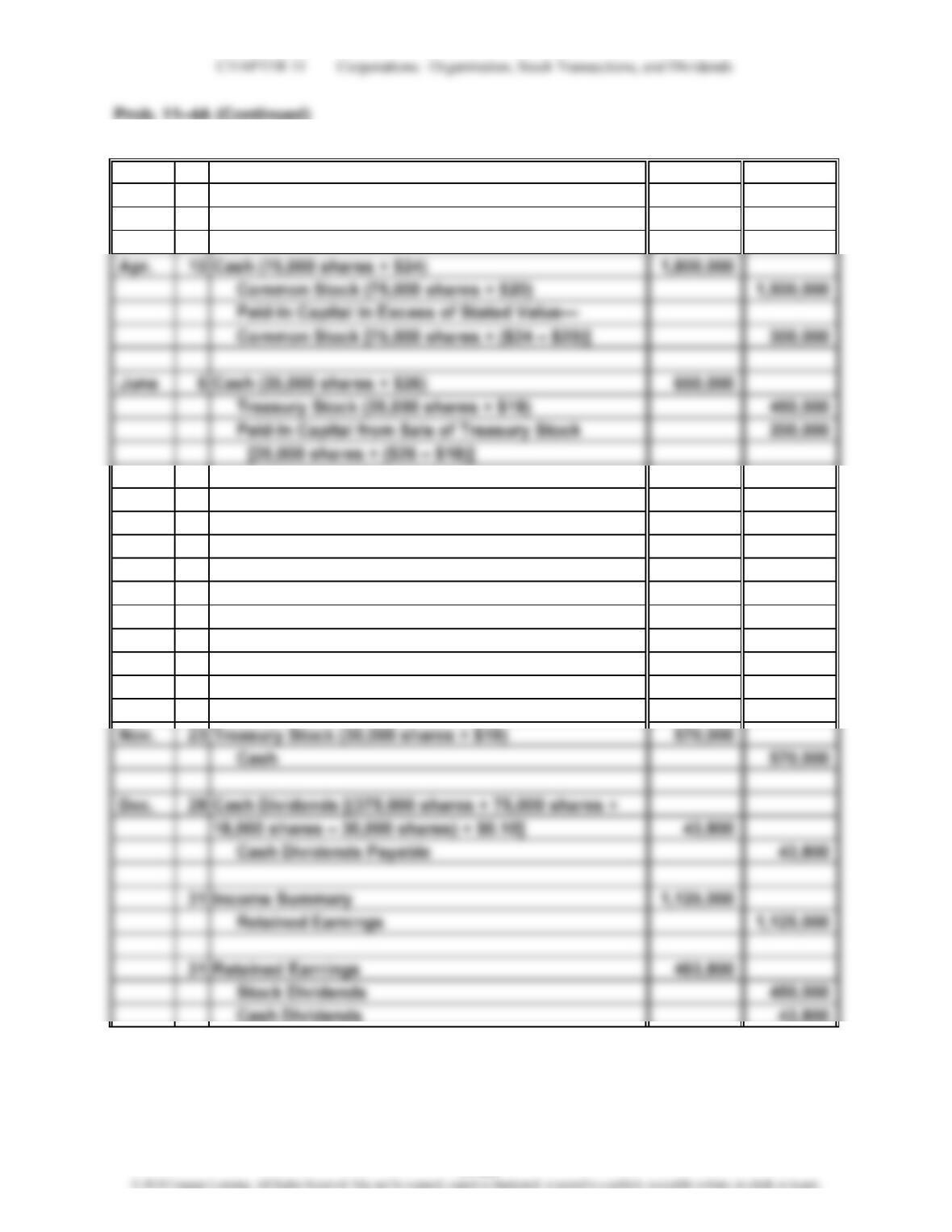

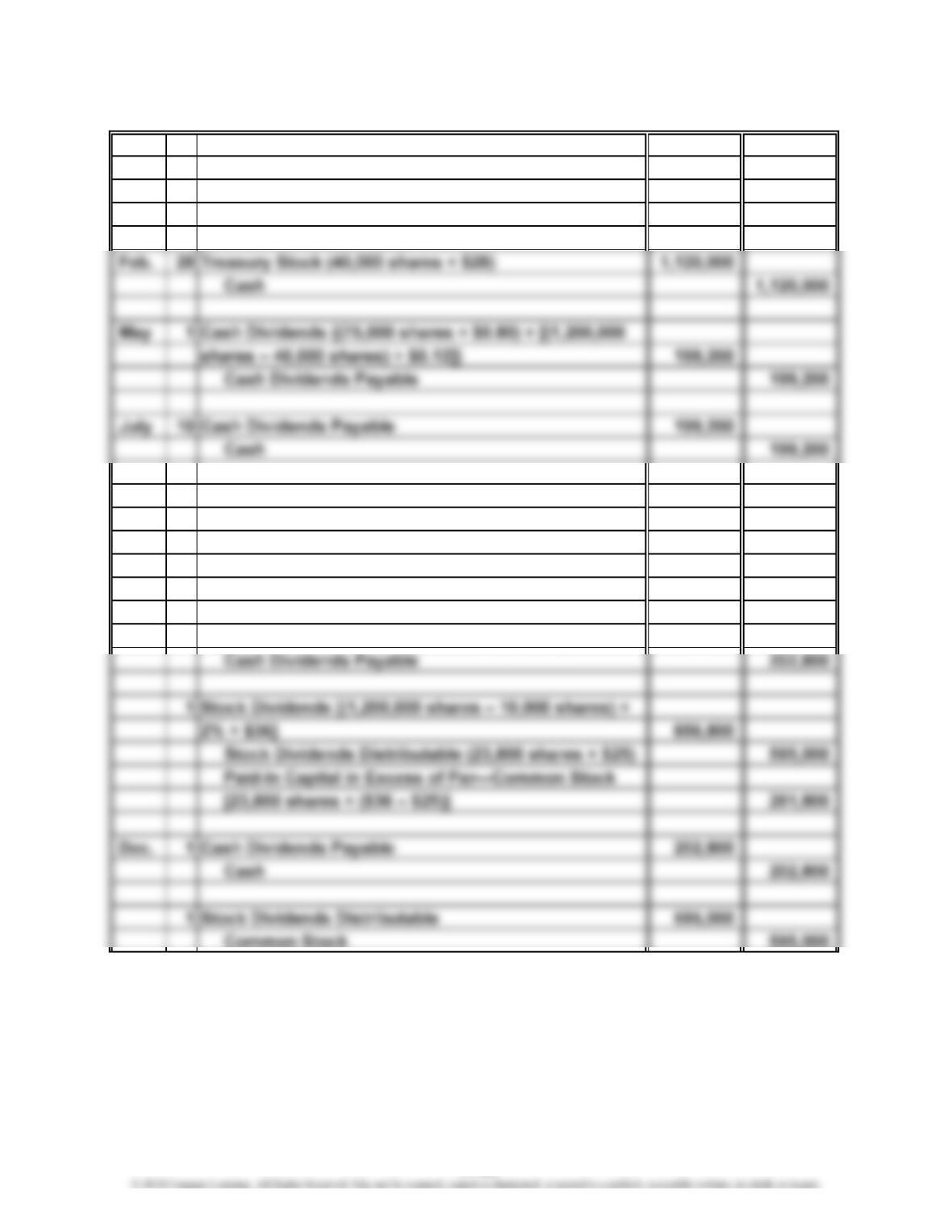

2.

Jan. 22 Cash Dividends Payable [(375,000 shares – 25,000

shares) × $0.08] 28,000

Cash 28,000

July 5 Stock Dividends [(375,000 shares + 75,000 shares)

× 4% × $25] 450,000

Stock Dividends Distributable (18,000 shares

× $20) 360,000

Paid-In Capital in Excess of Stated Value—

Common Stock [18,000 shares × ($25 – $20)] 90,000

Aug. 15 Stock Dividends Distributable 360,000

Common Stock 360,000

11-26

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–4A (Concluded)

3.

Retained earnings, January 1, 2014 $33,600,000

4.

Paid-in capital:

Common stock, $20 stated value (500,000 shares

authorized, 468,000 shares issued) $9,360,000

Stockholders’ Equity

MORROW ENTERPRISES INC.

Retained Earnings Statement

For the Year Ended December 31, 2014

11-27

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–5A

Jan. 9 No entry required. The stockholders’ ledger

would be revised to record the increased

number of shares held by each stockholder and

new par value.

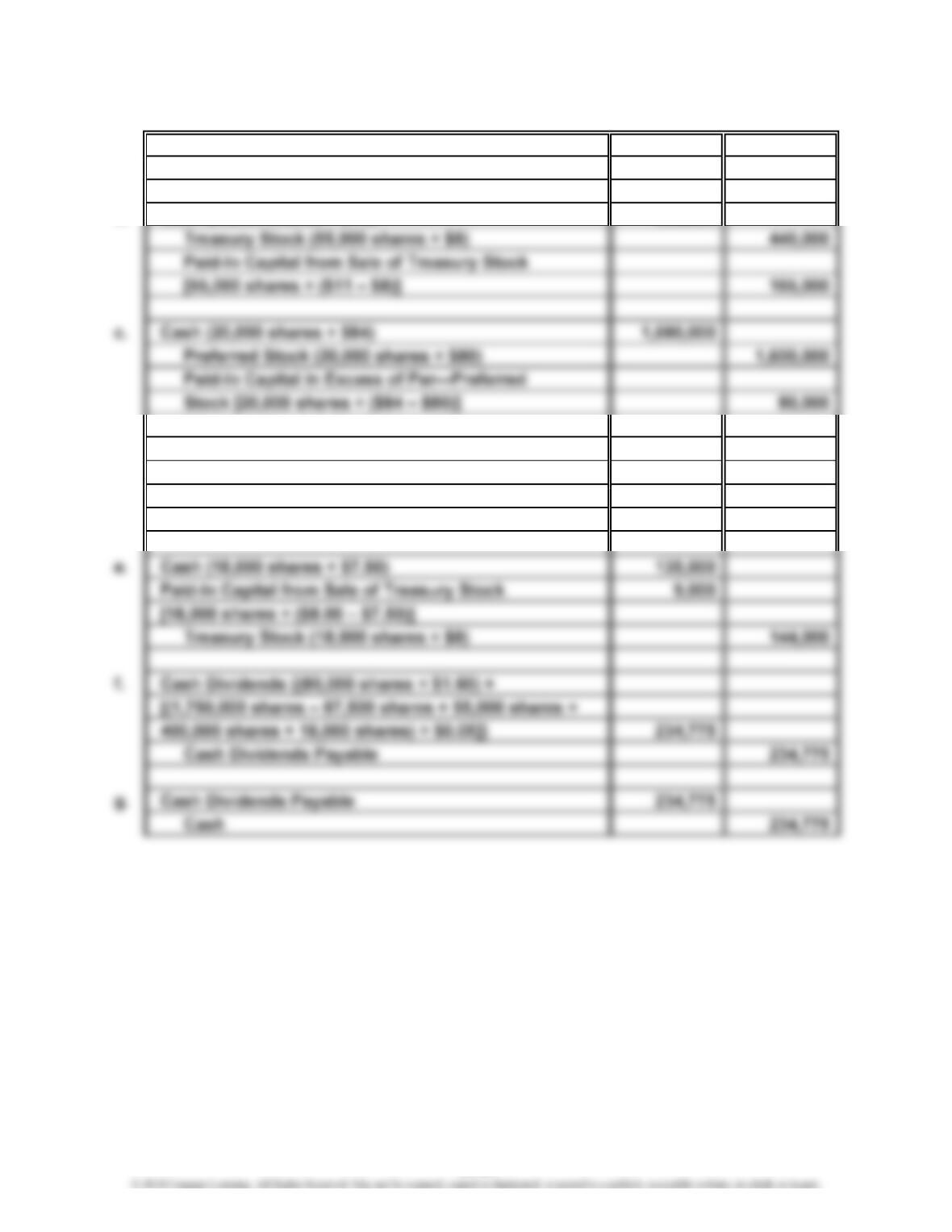

Sept. 7 Cash (30,000 shares × $34) 1,020,000

Treasury Stock (30,000 shares × $28) 840,000

Paid-In Capital from Sale of Treasury Stock

[30,000 shares × ($34 – $28)] 180,000

Oct. 1 Cash Dividends {(75,000 shares × $0.80)

+ [(1,200,000 shares – 10,000 shares) × $0.12]} 202,800

11-28

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–1B

1.

Total Per Per

Dividends Total Share Total Share

2009………

…

$ 24,000 $ 24,000 $ 0.96 $0 $0.00

Year

Preferred Dividends Common Dividends

11-29

…

…

…

…

…

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–2B

9 Cash 1,500,000

Mortgage Note Payable 1,500,000

Oct.

11-30

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–3B

a. Treasury Stock (87,500 shares × $8) 700,000

Cash 700,000

b. Cash (55,000 shares × $11) 605,000

d. Cash (400,000 shares × $13) 5,200,000

Common Stock (400,000 shares × $9) 3,600,000

Paid-In Capital in Excess of Par—Common

Stock [400,000 shares × ($13 – $9)] 1,600,000

11-31