CHAPTER 11

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 11-1C

(a) Jan. 10 Cash (40,000 X $3.60) …………………… 144,000

Common Stock (40,000 X $2) ….. 80,000

Paid-in Capital in Excess of

Stated Value-Common

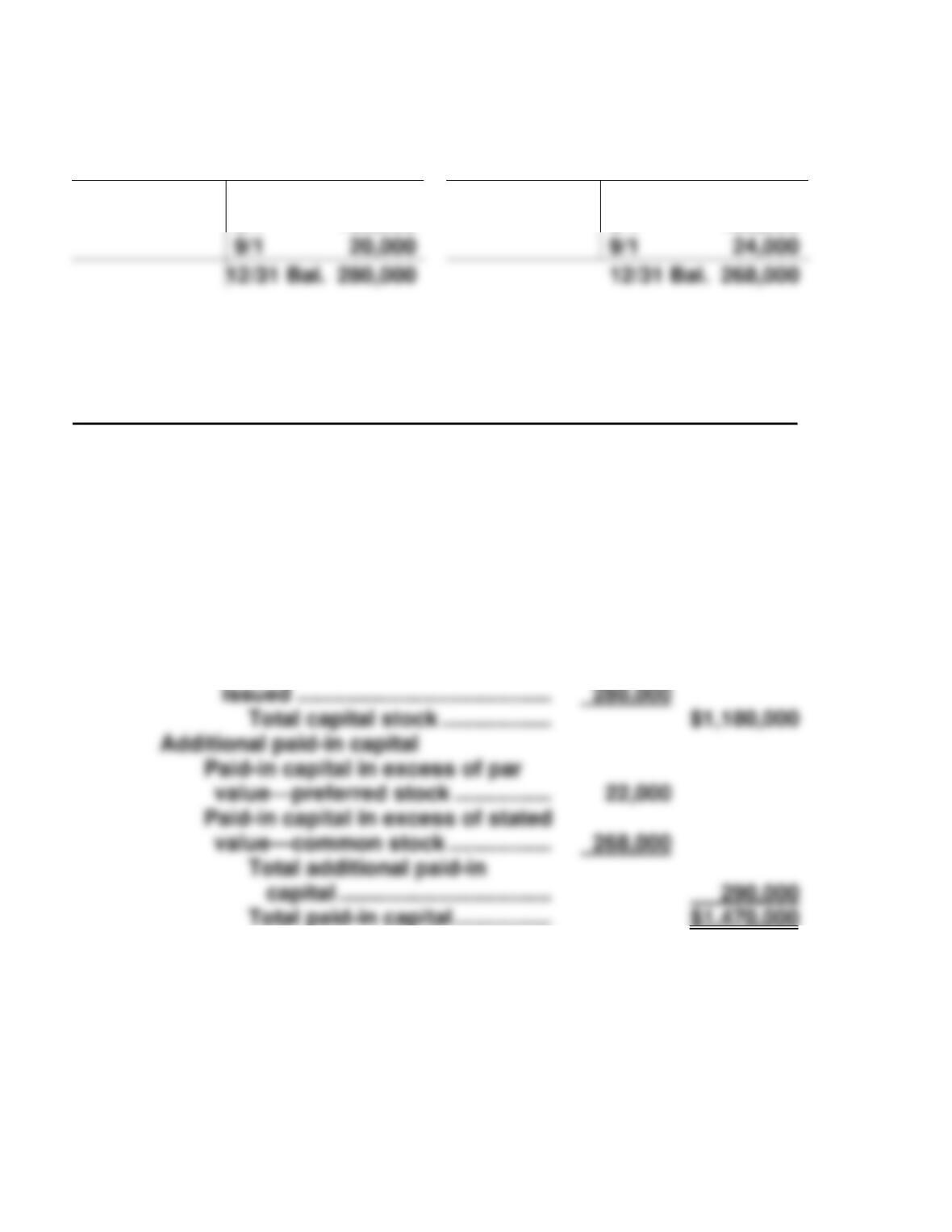

Common Stock (90,000 X $2) ….. 180,000

Sept. 1 Cash (10,000 X $4.40) …………………… 44,000

Paid-in Capital in Excess of

Stated Value—Common

(b)

Preferred Stock

Paid-in Capital in Excess of

Par Value—Preferred Stock

3/1 500,000

3/1 10,000

11/1 400,000

11/1 12,000

12/31 Bal. 900,000

12/31 Bal. 22,000

PROBLEM 11-1C (Continued)

Common Stock

Paid-in Capital in Excess of

Stated Value—Common Stock

1/10 80,000

1/10 64,000

5/1 180,000

5/1 180,000

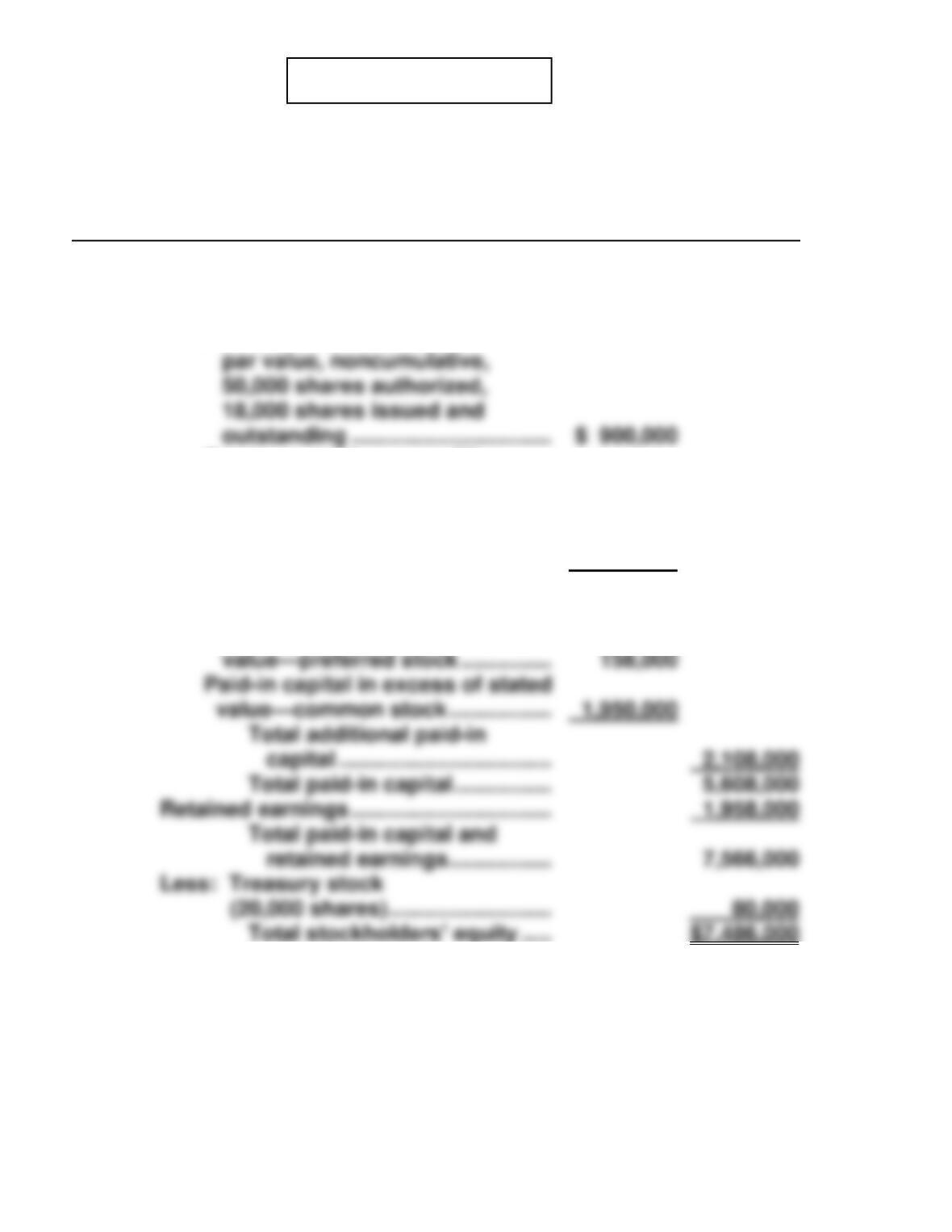

(c) HENNES CORPORATION

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

8% Preferred stock, $100 par

value, 10,000 shares

authorized, 9,000 shares

issued …………………………………… $900,000

Common stock, no-par, $2

stated value, 500,000 shares

authorized, 140,000 shares

9/1 20,000

9/1 24,000

12/31 Bal. 268,000

PROBLEM 11-2C

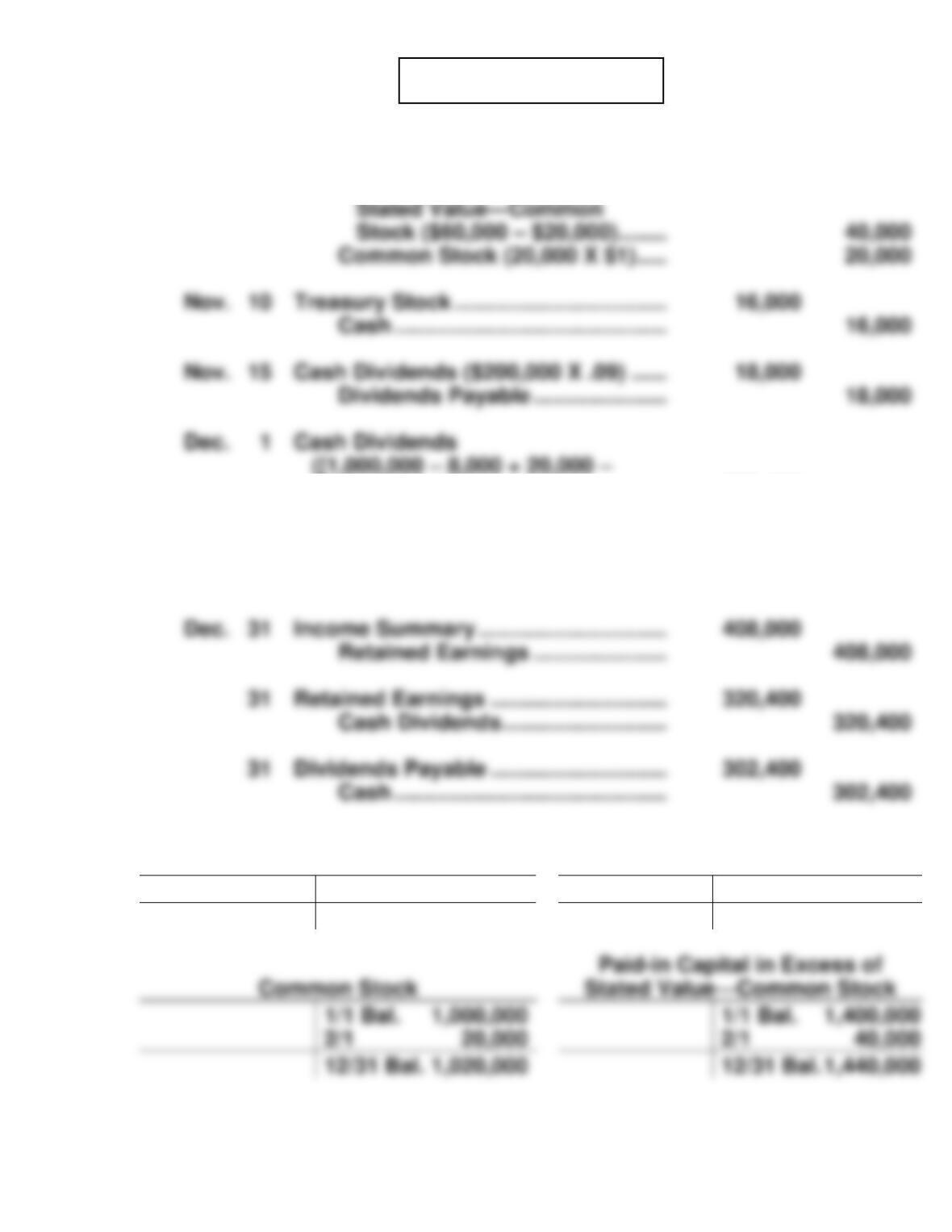

(a) Feb. 1 Cash …………………………..……………….. 60,000

Paid-in Capital in Excess of

4,000) X $0.30] …………………………... 302,400

Dividends Payable …………………. 302,400

Dec. 15 Dividends Payable ……………………….. 18,000

Cash ……………………………………… 18,000

(b) Preferred Stock

Paid-in Capital in Excess of

Par Value—Preferred Stock

1/1 Bal. 200,000

1/1 Bal. 16,000

12/31 Bal. 200,000

12/31 Bal. 16,000

Paid-in Capital in Excess of

2/1 20,000

2/1 40,000

12/31 Bal. 1,020,000

12/31 Bal. 1,440,000

PROBLEM 11-2C (Continued)

Retained Earnings

Treasury Stock

12/31 320,400

1/1 Bal. 1,716,000

1/1 Bal. 20,000

12/31 408,000

11/10 16,000

(c) NARDIN CORPORATION

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

9% Preferred stock, $50

par value, cumulative,

10,000 shares authorized,

4,000 shares issued and

outstanding …………………………... $ 200,000

value—common stock ……………. 1,440,000

Total additional paid-in

capital …………………………….. 1,456,000

Total paid-in capital ……………. 2,676,000

Retained earnings …………………………………. 1,803,600

12/31 Bal.1,803,600

12/31 Bal. 36,000

11/15 18,000

12/1 302,400

12/31 320,400

12/31 Bal. –0–

PROBLEM 11-2C (Continued)

(d)

Payout ratio= $302,400

$408,000=74.1%

Earnings per share= $408,000–$18,000

PROBLEM 11-3C

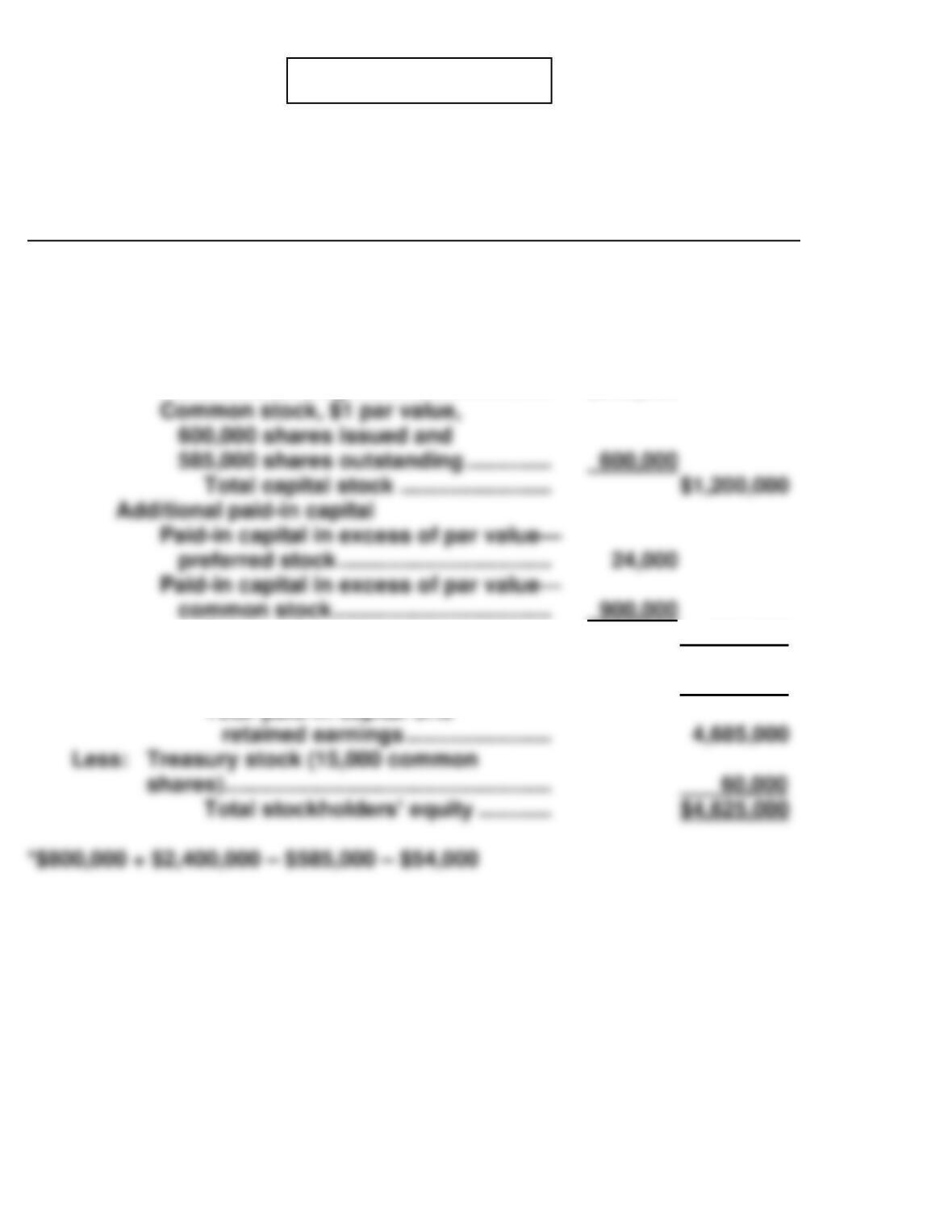

BRYANT COMPANY

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

9% Preferred stock, $50 par value,

cumulative, 12,000 shares issued

and outstanding …………………………... $600,000

Total additional paid-in capital ….. 924,000

Total paid-in capital ………………….. 2,124,000

Retained earnings ……………………………………….. 2,561,000*

Total paid-in capital and

PROBLEM 11-4C

(a)

Retained Earnings

Dec. 31 380,000

Jan. 1 Balance 660,000

(b) FLICKA CORPORATION

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

10% Preferred stock, $50 par

500,000 shares authorized,

350,000 shares issued and

outstanding ………………………………….. 3,500,000

Total capital stock ………………. $3,800,000

Additional paid-in capital

Paid-in capital in excess of par

Dec. 31 Net Income 525,000

PROBLEM 11-5C

CHARLOTTE CORPORATION

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

8% Preferred stock, $50

Common stock, no-par, $2

stated value, 1,800,000 shares

authorized, 1,300,000 shares

issued, and 1,280,000 shares

outstanding …………………………... 2,600,000

Total capital stock ……………… $3,500,000

Additional paid-in capital

Paid-in capital in excess of par

PROBLEM 11-6C

GABRIEL INC.

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Common stock, $1 par value,

1,000,000 shares authorized,

610,000* shares issued, and

592,000 outstanding ……………………………….. $ 610,000

PROBLEM 11-7C

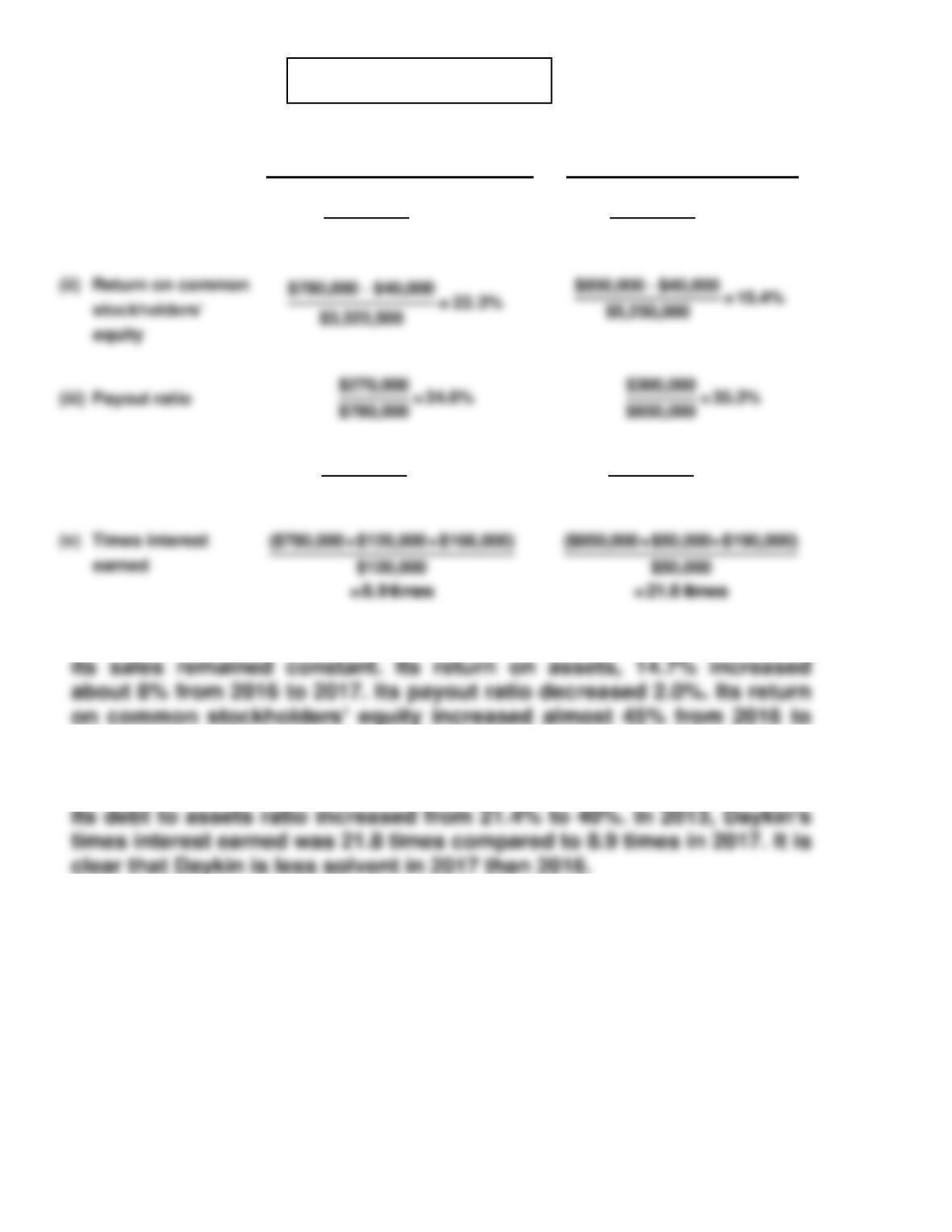

2017 2016

(a)

(i) Return on assets

ratio

$780,000

$5,312,500 = 14.7%

$850,000

$6,230,000 =13.6%

(iv) Debt to assets ratio

$2,000,000

$5,000,000 =40%

$1,200,000

$5,610,000 =21.4%

(b) Daykin Company’s net income decreased $70,000 in 2017 even though

2017. An increase of this size indicates improved profitability.

(c) Daykin Company acquired more debt in 2017 and became less solvent.

PROBLEM 11-7C (Continued)

(d) It appears that the decision to issue bonds and purchase treasury stock

was a wise choice. The bonds require payment of 8% interest which is

less than Daykin’s 14.7% return on assets. This positive difference

resulted in the significant improvement in return on common stock–

*PROBLEM 11-8C

(a) Feb. 1 Cash Dividends (80,000 X $0.50) …… 40,000

Dividends Payable ………………… 40,000

July 1 Stock Dividends (12,000* X $25) …… 300,000

Common Stock Dividends

Distributable (12,000 X $20)…. 240,000

Paid-in Capital in Excess of

Par Value (12,000 X $5) ……….. 60,000

Dec. 1 Cash Dividends (92,000 X $1) ……….. 92,000

Dividends Payable ………………… 92,000

*PROBLEM 11-8C (Continued)

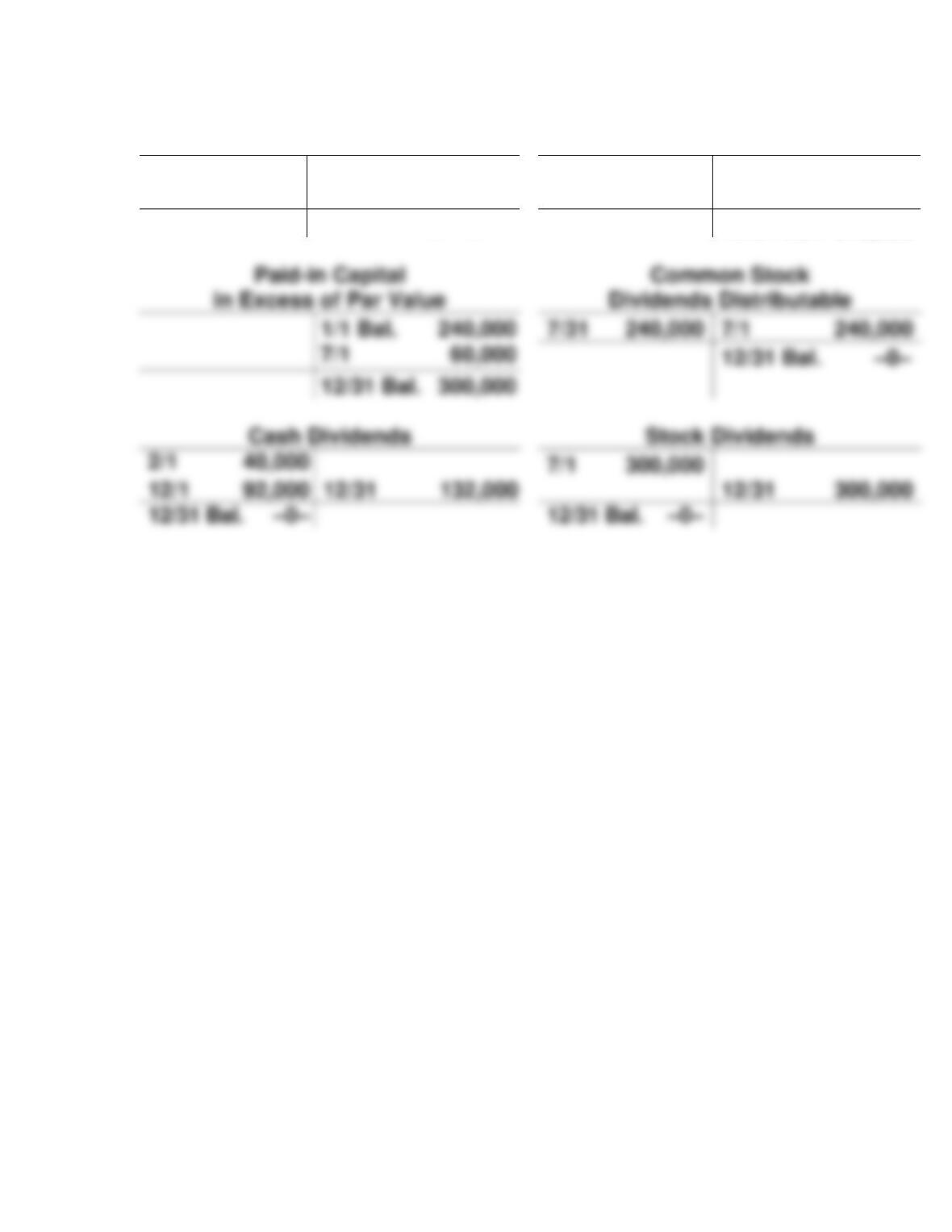

(b)

Common Stock

Retained Earnings

1/1 Bal. 1,600,000

12/31 300,000

1/1 Bal. 750,000

7/31 240,000

12/31 132,000

12/31 500,000

12/31 Bal. 1,840,000

12/31 Bal. 818,000

7/31 240,000

7/1 240,000

12/31 Bal. –0–

7/1 300,000

12/1 92,000

12/31 132,000

12/31 300,000

12/31 Bal. –0–

12/31 Bal. –0–

*PROBLEM 11-8C (Continued)

(c) JASON CORPORATION

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

Common stock, $20 par value,

(d)

Payout ratio = $132,000a

$500,000 = 26.4%

a($40,000 + $92,000)