25 Minutes, Medium

a.

Stockholders’ equity

shares authorized, issued, and outstanding 500,000$

Retained earnings at Dec. 31, 2016 170,000$

Add: Net income for 2017 and 2018 890,000

Net income for four-year period 1,060,000$

Less: Dividends paid on 8% preferred stock:

2018 (8% x $100 x 5,000 shares = $40,000) 40,000 (120,000)

Dividends on $9 preferred stock:

2018 ($9 x 5,000 shares) 45,000 (90,000)

Dividends on common stock:

b.

1.

2.

PROBLEM 11.3A

MANHATTAN TRANSPORT COMPANY

December 31, 2018

Partial Balance Sheet

MANHATTAN TRANSPORT COMPANY

A corporation might decide to use cumulative preferred stock rather than debt to finance

operations for any of the following reasons (only 2 required):

Although cumulative dividends must eventually be paid if the corporation is profitable, they

8% cumulative preferred stock, $100 par, 5,000

*Computation of retained earnings at December 31, 2018:

$9 cumulative preferred stock, no-par value, 10,000 shares

authorized, 5,000 shares issued and outstanding 512,000

shares issued and outstanding 200,000

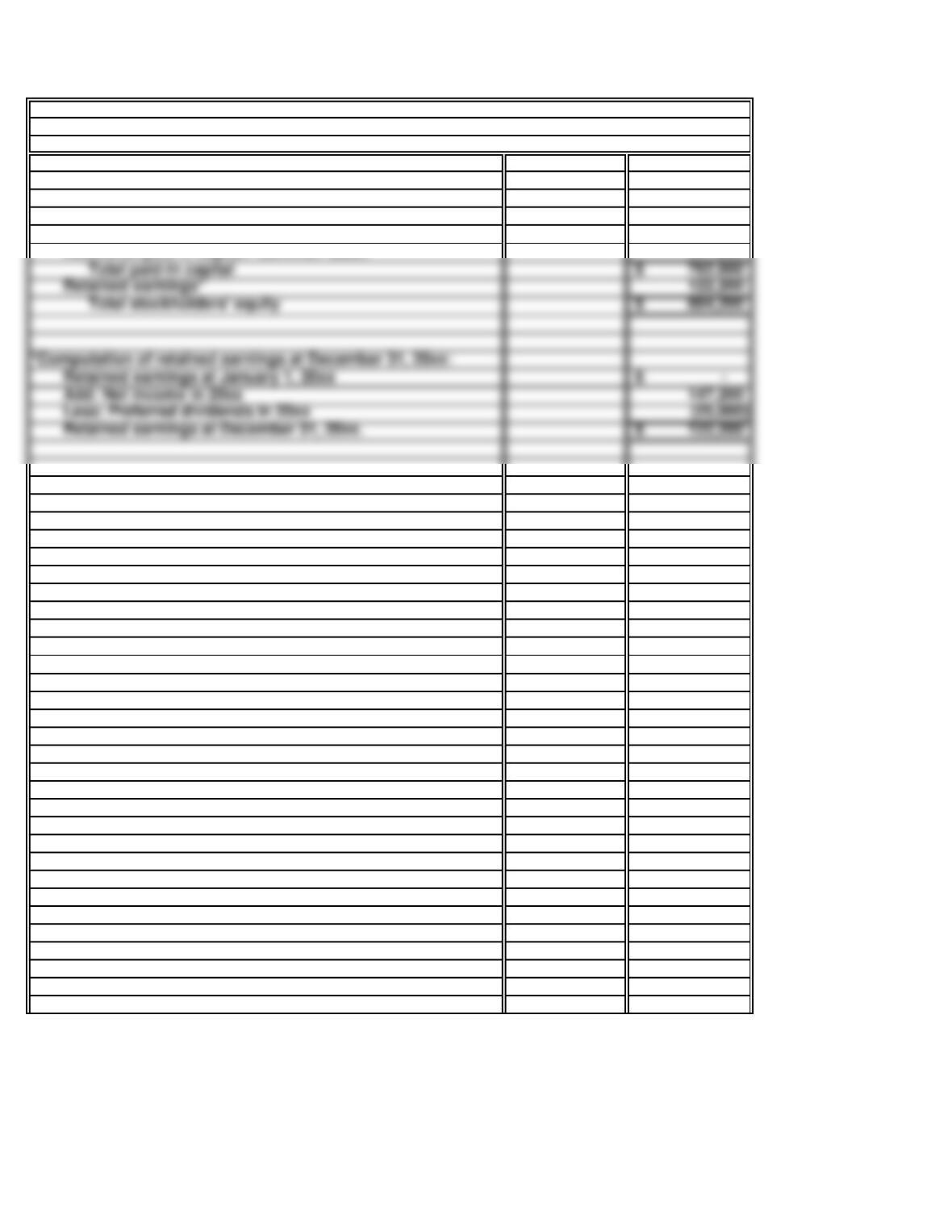

Total paid-in capital 1,812,000$

Common stock, $2 par, 200,000 shares authorized, 100,000

35 Minutes, Medium

Jan 6 Cash 280,000

Common Stock 40,000

240,000

12 250,000

250,000

Common Stock 30,000

195,000

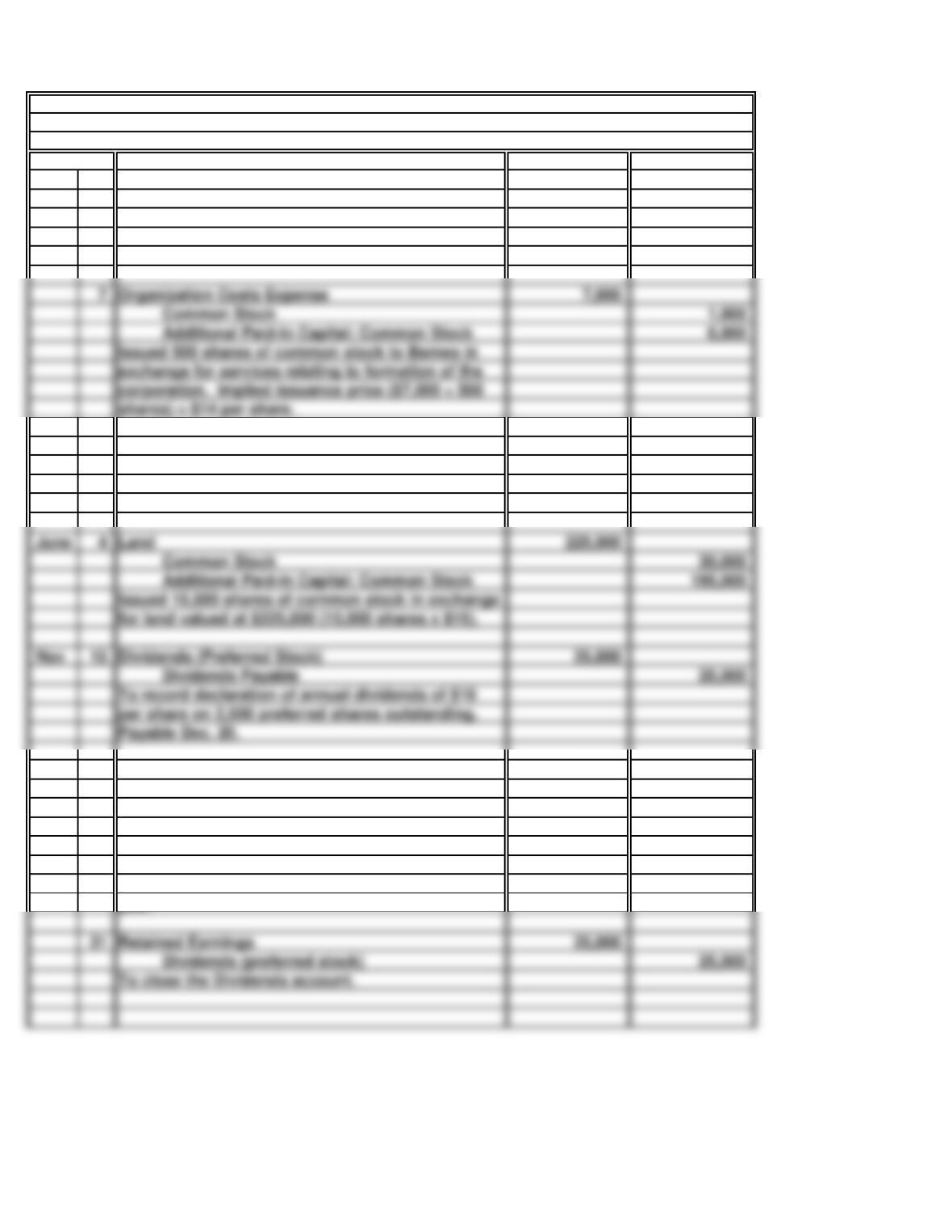

for land valued at $225,000 (15,000 shares x $15).

Dividends (Preferred Stock)

Dividends Payable

To record declaration of annual dividends of $10

Payable Dec. 20.

per share on 2,500 preferred shares outstanding.

Issued 15,000 shares of common stock in exchange

Additional Paid-in Capital: Common Stock

Dec 20 25,000

Cash 25,000

31

Retained Earnings 147,200

147,200

year.

31 25,000

25,000

Dividends (preferred stock)

To close the Dividends account.

Retained Earnings

10% Cumulative Preferred Stock

Income Summary

To record payment of dividend declared Nov. 15.

Dividends Payable

To close the Income Summary account for the

20__

Issued 20,000 shares of $2 par value common stock

Additional Paid-in Capital: Common Stock

at $14 per share.

PROBLEM 11.4A

a.

General Journal

SHARNES COMMUNICATIONS, INC.

Issued 2,500 shares of $100 par value, 10%,

cumulative preferred stock at par value.

Cash

7 7,000

Common Stock 1,000

Organization Costs Expense

Issued 500 shares of common stock to Barnes in

Additional Paid-in Capital: Common Stock

corporation. Implied issuance price ($7,000 ÷ 500

shares) = $14 per share.

exchange for services relating to formation of the

b.

Stockholders’ equity

50,000 shares, issued and outstanding 2,500 shares 250,000$

issued and outstanding 35,500 shares 71,000

441,000

10% cumulative preferred stock, $100 par, authorized

PROBLEM 11.4A

SHARNES COMMUNICATIONS, INC.

December 31, 20xx

Partial Balance Sheet

SHARNES COMMUNICATIONS, INC. (concluded)

Common stock, $2 par, authorized 400,000 shares,

Additional paid-in capital: Common stock

122,200

*Computation of retained earnings at December 31, 20xx:

Retained earnings*

Retained earnings at December 31, 20xx.

Retained earnings at January 1, 20xx

Add: Net income in 20xx

Less: Preferred dividends in 20xx

35 Minutes, Strong

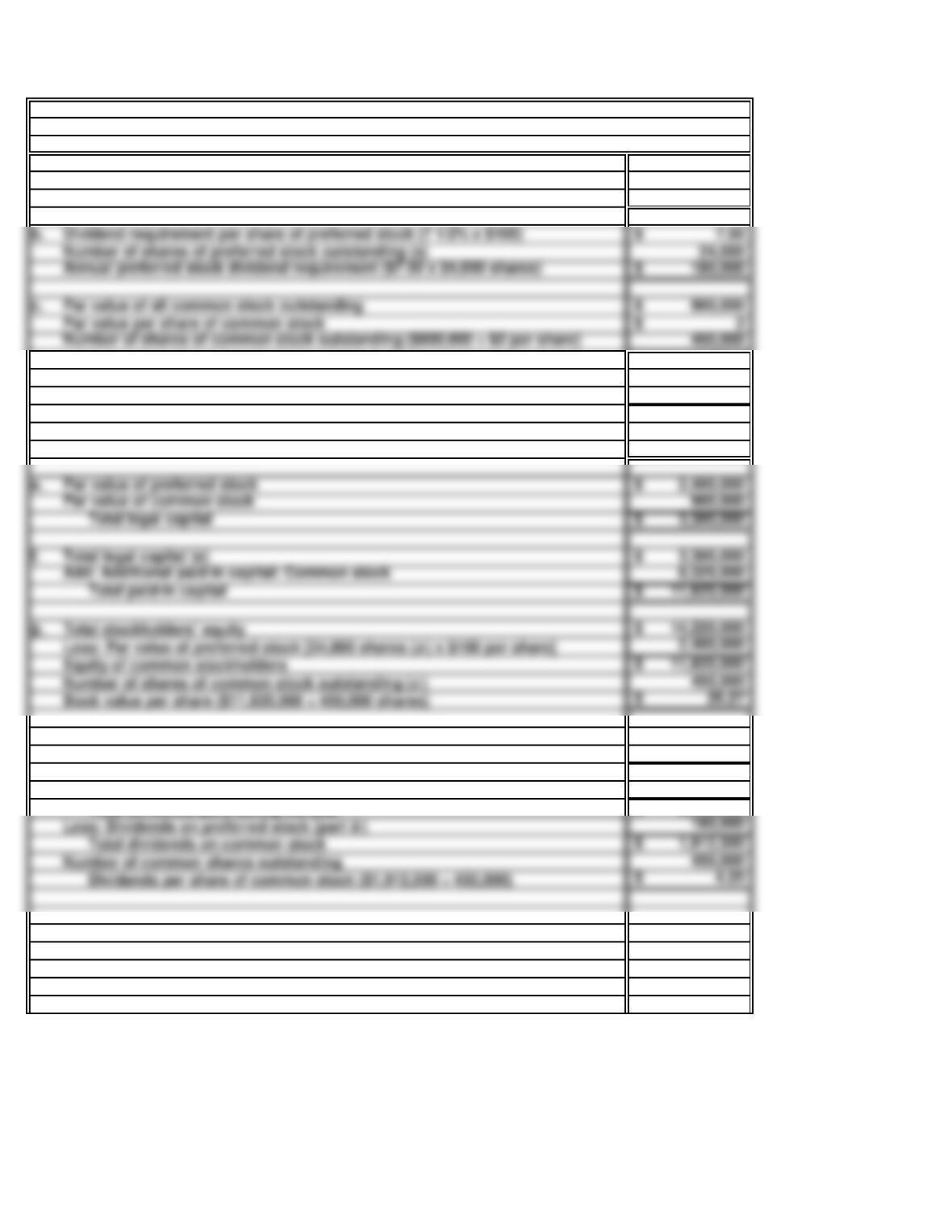

a. Par value of all preferred stock outstanding 2,400,000$

100$

24,000

d. 900,000$

Paid-in capital in excess of par: Common 8,325,000

Total issuance price of all common stock 9,225,000$

Number of shares of common stock issued (c) 450,000

20.50$

g. Total stockholders’ equity 14,220,000$

Book value per share ($11,820,000 ÷ 450,000 shares) 26.27$

Total paid-in capital

Par value of preferred stock

Par value of common stock

Total legal capital

Total legal capital (e)

Add: Additional paid-in capital: Common stock

h. Retained earnings, beginning of the year 717,500$

Add: Net income for the year 3,970,000

Subtotal 4,687,500$

Less: Retained earnings, end of the year 2,595,000

Total dividends paid during the year 2,092,500$

Total dividends on common stock 1,912,500$

Average issuance price per share of common ($9,225,000 ÷ 450,000 shares)

Par value of all common stock issued

PROBLEM 11.5A

FT. SMITH PRODUCTS

Par value per share of preferred stock

Number of shares of preferred stock outstanding ($2,400,000 ÷ $100)

b. Dividend requirement per share of preferred stock (7 1/2% x $100) 7.50$

Par value of all common stock outstanding

Number of shares of preferred stock outstanding (a)

Par value per share of common stock

35 Minutes, Medium

In Thousands

(Except for Per

Share Amounts)

a. Par value of all common stock outstanding 6,819$

Par value per share 0.50

Number of shares outstanding ($6,819/$0.50) 13,638

PROBLEM 11.6A

PARSONS, INC. CORPORATION

b. Dividend requirement per share of preferred stock 17.20$

Numbers of shares of preferred stock outstanding 345

Annual dividends paid to preferred stockholders ($17.20 x 345) 5,934$

Additional paid-in capital 87,260

Total paid-in capital 180,329$

Less: Preferred stock par value = ($250 x 345 shares) 86,250

Number of shares of common stock outstanding 13,638

Book value per share ($151,342/13,638 shares) 11.10$

e.

f.

g.

PROBLEM 11.6A

PARSONS, INC. (concluded)

The basic advantage of being publicly owned is that the corporation has the opportunity to

raise large amounts of equity capital from many investors. Some publicly owned

The term convertible means that at the option of the preferred stockholder, each preferred

At $248 per share, Parson’s preferred has a dividend yield of 6.9% ($17.20 ÷ $248). In

15 Minutes, Easy

a.

b.

The company’s par value—one-tenth of a cent per share—is quite low. However, the

corporation can set par value at any level that it chooses; the amount of par value has

PROBLEM 11.7A

TECHNO CORPORATION

Par value is the legal capital per share—the amount by which stockholders’ equity cannot

be reduced except by losses. Thus, par value may be viewed as a minimum cushion of

equity capital existing for the protection of creditors.

15 Minutes, Medium

Stockholders’ equity:

Common stock, $1 par, 50,000 shares authorized, issued, and 50,000$

outstanding

Additional paid-in capital: Common stock 350,000

c.

The treasury stock purchase of $35,000 in 2017 was reported as a financing cash outflow

PROBLEM 11.8A

a. Feller Corporation

31-Dec-18

Partial Balance Sheet

FELLER CORPORATION

Net income in 2016 95,000$

Net income in 2017 27,500

30 Minutes, Strong

Stockholders’ equity:

10% preferred stock, $100 par, cumulative, authorized,

issued, and outstanding 30,000 shares 3,000,000$

Total stockholders’ equity at Dec. 31, 2018 6,695,000$

*Computation of additional paid-in capital on treasury stock:

Purchase price per share: $400,000 ÷ 20,000 shares = $20

per share

per share

($5 per share x 10,000 shares reissued)

Preferred dividend (for years 2014-2018)

c.

Had the company decided to split its common stock 3-for-1 on December 31, 2018, the market value

PROBLEM 11.9A

a.

HERNDON INDUSTRIES

treasury 1,200,000

Additional paid-in capital: Common stock 720,000

20 Minutes, Easy

a.

Stockholders’ equity

authorized 2,000 shares, issued and out- 50,000$

standing 500 shares

Issued and outstanding 80,000 shares 80,000

b.

c.

10% cumulative preferred stock, $100 par value,

SOLUTIONS TO PROBLEMS SET B

PROBLEM 11.1B

SEARFOSS, INC.

December 31, 2018

Partial Balance Sheet

SEARFOSS, INC.

The market price of preferred stock usually decreases as interest rates increase. At

Common stock, $1 par value, authorized 300,000 shares

There are no dividends in arrears at December 31, 2018. We know this because common

Total paid-in capital 1,250,000$

*Computation of retained earnings at December 31, 2018:

Net income for the four-year period 2015-2018

Less: Preferred dividends ($5,000 per year for four years)

20 Minutes, Easy

a.

Stockholders’ equity

authorized, issued, and outstanding 10,000 shares 1,000,000$

b.

Note to financial statements:

Common stock, $1 par value, authorized 1 million shares,

PROBLEM 11.2B

BANNER PUBLICATIONS

December 31, 2018

Partial Balance Sheet

BANNER PUBLICATIONS

10% cumulative preferred stock, $100 par value,

issued and outstanding 400,000 shares 400,000

Retained earnings, December 2017

Net income for the five-year period 2013-2017

Less: Preferred dividends ($100,000 x 5 years)

*Computation of retained earnings at December 31, 2018:

25 Minutes, Medium

a.

Stockholders’ equity

Retained earnings at Dec. 31, 2016 530,000$

Add: Net income for 2017 and 2018 1,400,000

Less: Dividends paid on 10% preferred stock:

2018 (10% x $100 x 10,000 shares = $100,000) 100,000 (300,000)

Dividends on $6 preferred stock:

2018 ($6 x 5,000 shares) 30,000 (60,000)

b.

1.

2.

A corporation might decide to use cumulative preferred stock rather than debt to finance

operations for any of the following reasons (only 2 required):

Although cumulative dividends must eventually be paid if the corporation is profitable, they

10% cumulative preferred stock, $100 par value, 10,000

*Computation of retained earnings at December 31, 2018:

PROBLEM 11.3B

RAY BEAM, INC.

December 31, 2018

Partial Balance Sheet

RAY BEAM, INC.

shares authorized, issued, and outstanding 1,000,000$

$6 cumulative preferred stock, no-par value, 8,000 shares

shares issued and outstanding 130,000

Common stock, $1 par, 260,000 shares authorized, 130,000

35 Minutes, Medium

Jan 7 Cash 300,000

18 400,000

400,000

July 5 Land 120,000

for land valued at $120,000 (10,000 shares x $12).

Additional Paid-in Capital: Common Stock

Issued 10,000 shares of common stock in exchange

Nov 25 20,000

20,000

Dec 11 20,000

Cash 20,000

Retained Earnings 810,000

31 20,000

20,000

To close the Income Summary account for the

Income Summary

To close the Dividends account.

Retained Earnings

Dividends (Preferred Stock)

20__

per share on 4,000 preferred shares outstanding.

Cash

To record payment of dividend declared Nov. 25.

Dividends Payable

5% Cumulative Preferred Stock

Payable Dec. 11.

To record declaration of annual dividends of $5

Dividends (Preferred Stock)

Dividends Payable

Issued 4,000 shares of $100 par value, 5%,

cumulative preferred stock at par value.

PROBLEM 11.4B

a.

General Journal

MARKUP, INC.

Common Stock 30,000

12 12,000

11,000

Issued 1,000 shares of common stock to Deal in

corporation. Implied issuance price ($12,000 ÷ 1,000

shares) = $12 per share.

Issued 30,000 shares of $1 par value common stock

Additional Paid-in Capital: Common Stock

Organization Costs Expense

at $10 per share.

Additional Paid-in Capital: Common Stock

exchange for services relating to formation of the