Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 11 - Flexible Budgeting and Analysis of Overhead Costs

CHAPTER 11

Flexible Budgeting and Analysis of Overhead

Costs

ANSWERS TO REVIEW QUESTIONS

11-2 The advantage of a flexible budget is that it is responsive to changes in the activity

11-3 Flexible overhead budgets are based on an input activity measure, such as process

time, in order to provide a meaningful measure of production activity. An output

11-4 A columnar flexible budget has several columns listing the budgeted levels of cost at

different levels of activity. Each column is based on a different activity level. A

11-5 Production overhead is added to Work-in-Process Inventory under standard costing

as shown in the following T-accounts:

Work-in-Process Inventory

Production Overhead

X *

X *

*The amount of X is the following:

allowed standard

nedpredetermi

Chapter 11 - Flexible Budgeting and Analysis of Overhead Costs

11-6 Advances in manufacturing technology have resulted in a shift from variable toward

fixed costs. In addition, as automation increases, more and more firms are switching

11-7 The interpretation of the variable-overhead spending variance is that a different total

amount was spent on variable overhead than should have been spent in accordance

11-8 An unfavorable variable-overhead spending variance does not necessarily imply that

the company paid more than the anticipated rate per kilowatt-hour for electricity. An

11-9 The interpretation of the variable-overhead efficiency variance is related to the

efficiency in using the activity upon which variable overhead is budgeted. For

example, if the basis for the variable-overhead budget is direct-labor hours, an

11-10 The interpretations of the direct-labor and variable-overhead efficiency variances are

very different. The direct-labor efficiency variance does convey information about

Chapter 11 - Flexible Budgeting and Analysis of Overhead Costs

11-12 The fixed-overhead volume variance is the difference between budgeted fixed

overhead and applied fixed overhead. The best interpretation for this variance is a

means of reconciling two disparate purposes of the standard-costing system: the

11-13 A common but misleading interpretation of the fixed-overhead volume variance is

that it is a measure of the cost of underutilizing or overutilizing production capacity.

For example, when budgeted fixed overhead exceeds applied fixed overhead, the

11-14 The following graph depicts budgeted and applied fixed overhead and displays an

unfavorable (positive) volume variance.

Fixed overhead

Applied fixed

overhead

11-15 All kinds of organizations use flexible budgets, including manufacturing firms, retail

11-16 The conceptual problem in applying fixed production overhead as a product cost is

that this procedure treats fixed overhead as though it were a variable cost. Fixed

overhead is applied as a product cost by multiplying the fixed overhead rate by the

11-17 The control purpose of a standard-costing system is to provide benchmarks against

which to compare actual costs. Then management by exception is used to follow up

11-18 Fixed-overhead costs sometimes are called capacity-producing costs because they

are the costs incurred in order to generate a place and environment in which

Chapter 11 - Flexible Budgeting and Analysis of Overhead Costs

11-19 The following graph depicts budgeted and applied variable overhead. Budgeted and

applied variable overhead are represented by the same line because variable

overhead is a variable cost. Both budgeted and applied variable overhead increase

11-20 Plausible activity bases for a variety of organizations to use in flexible budgeting are

as follows:

11-21 Conventional flexible budgets typically are based on a single cost driver, such as

direct-labor hours or machine hours. Costs are categorized as variable or fixed. The

Chapter 11 - Flexible Budgeting and Analysis of Overhead Costs

SOLUTIONS TO EXERCISES

EXERCISE 11-22 (20 MINUTES)

1.

Calculation of overhead variances:

a.

Variable-overhead spending variance

=

actual variable overhead – (AQ

SVR)

=

$607,500 – (60,750 machine hrs $9.00)

c.

Fixed-overhead budget variance

=

actual fixed overhead – budgeted fixed overhead

d.

Fixed-overhead volume variance

=

budgeted fixed overhead – applied fixed overhead

†Applied fixed overhead

=

(MH) hours machine

allowed standard

rate overhead

fixed nedpredetermi

EXERCISE 11-23 (15 MINUTES)

Variable-overhead spending variance

=

*SQ = 56,000 units 5 direct-labor hours per unit

Fixed-overhead budget variance

=

actual fixed overhead – budgeted fixed overhead

Fixed-overhead volume variance

=

budgeted fixed overhead – applied fixed overhead

Chapter 11 - Flexible Budgeting and Analysis of Overhead Costs

EXERCISE 11-24 (10 MINUTES)

1.

Product

Std Direct

Labor Hrs/Unit

Number

of Units

Total Std Direct

Labor Hours

Field ..................................................

4

300

1,200

2.

Basing the flexible budget on the number of binoculars produced would not be

meaningful. Production of 700 binoculars could mean 100 field models and 600

Chapter 11 - Flexible Budgeting and Analysis of Overhead Costs

EXERCISE 11-25 (20 MINUTES)

1.

Variable-overhead spending variance

=

actual variable overhead – (AQ

SVR)

2.

Variable-overhead efficiency variance

=

SVR(AQ – SQ)

3.

Fixed-overhead budget variance

=

actual fixed overhead – budgeted fixed overhead

4.

Fixed-overhead volume variance

=

budgeted fixed overhead – applied fixed overhead

†Applied fixed overhead

=

hours labordirect

allowed standard

rate overhead

fixed nedpredetermi

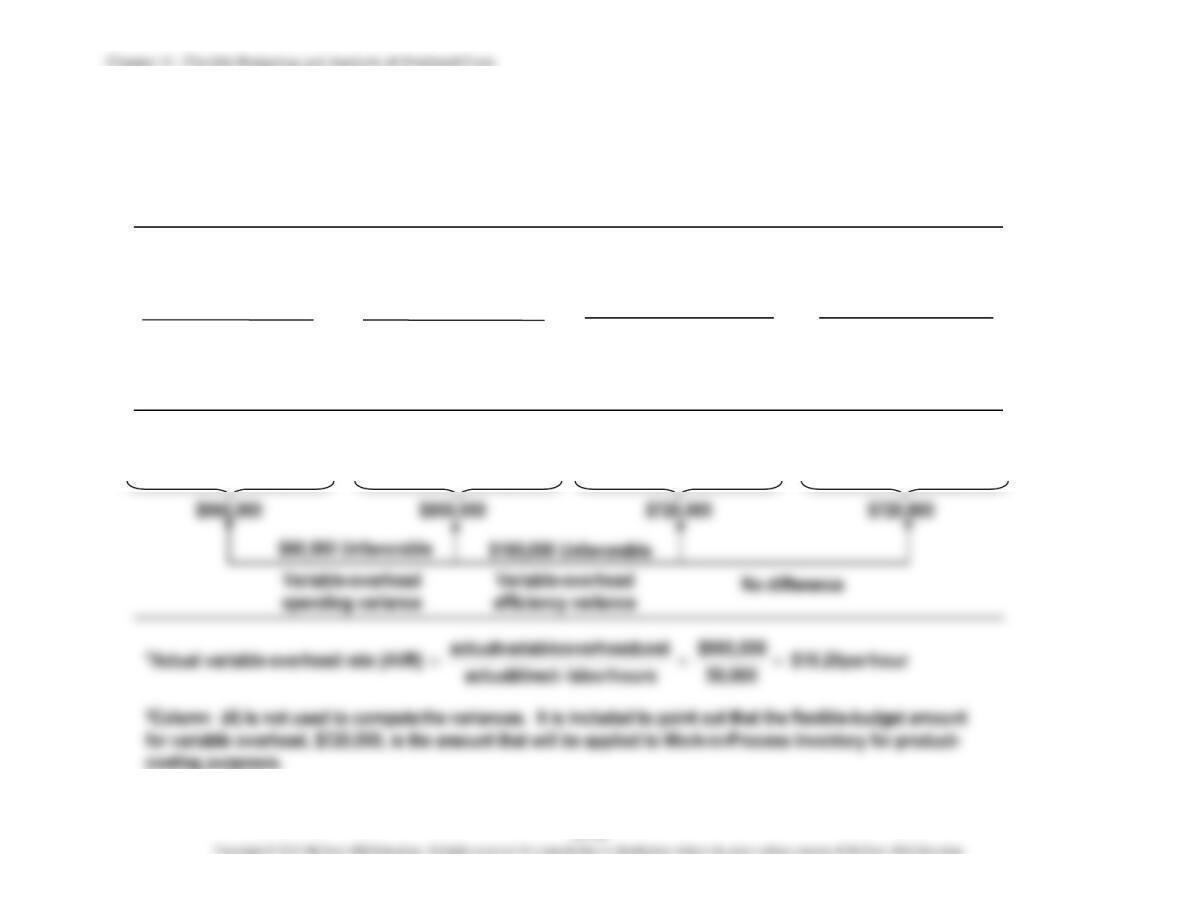

EXERCISE 11-26 (40 MINUTES)

1.

Variable overhead variances:

VARIABLE-OVERHEAD SPENDING AND EFFICIENCY VARIANCES

(Hours = Direct-Labor Hours)

Actual

Hours

(AQ)

Actual

Rate

(AVR)

Actual

Hours

(AQ)

Standard

Rate

(SVR)

Standard

Rate

(SVR)

Standard

Rate

(SVR)

Standard

Allowed

Hours

(SQ)

Standard

Allowed

Hours

(SQ)

50,000

hours

50,000

hours

40,000

hours

40,000

hours

$19.20

per

hour*

$18.00

per

hour

$18.00

per

hour

$18.00

per

hour

x

x

x

x

x

x

x

x

FLEXIBLE BUDGET:

VARIABLE OVERHEAD

ACTUAL VARIABLE

OVERHEAD

VARIABLE OVERHEAD

APPLIED TO

WORK-IN-PROCESS

(1)

(2)

(3)

(4)†

PROJECTED VARIABLE

OVERHEAD

EXERCISE 11-26 (CONTINUED)

2.

Fixed-overhead variances:

FIXED-OVERHEAD BUDGET AND VOLUME VARIANCES

(Hours = Direct-Labor Hours)

(1)

ACTUAL

FIXED

OVERHEAD

(2)

BUDGETED

FIXED

OVERHEAD

(3)

FIXED OVERHEAD

APPLIED TO

WORK IN PROCESS

Standard

Standard

Fixed-

Allowed

Overhead

Hours

Rate

EXERCISE 11-27 (35 MINUTES)

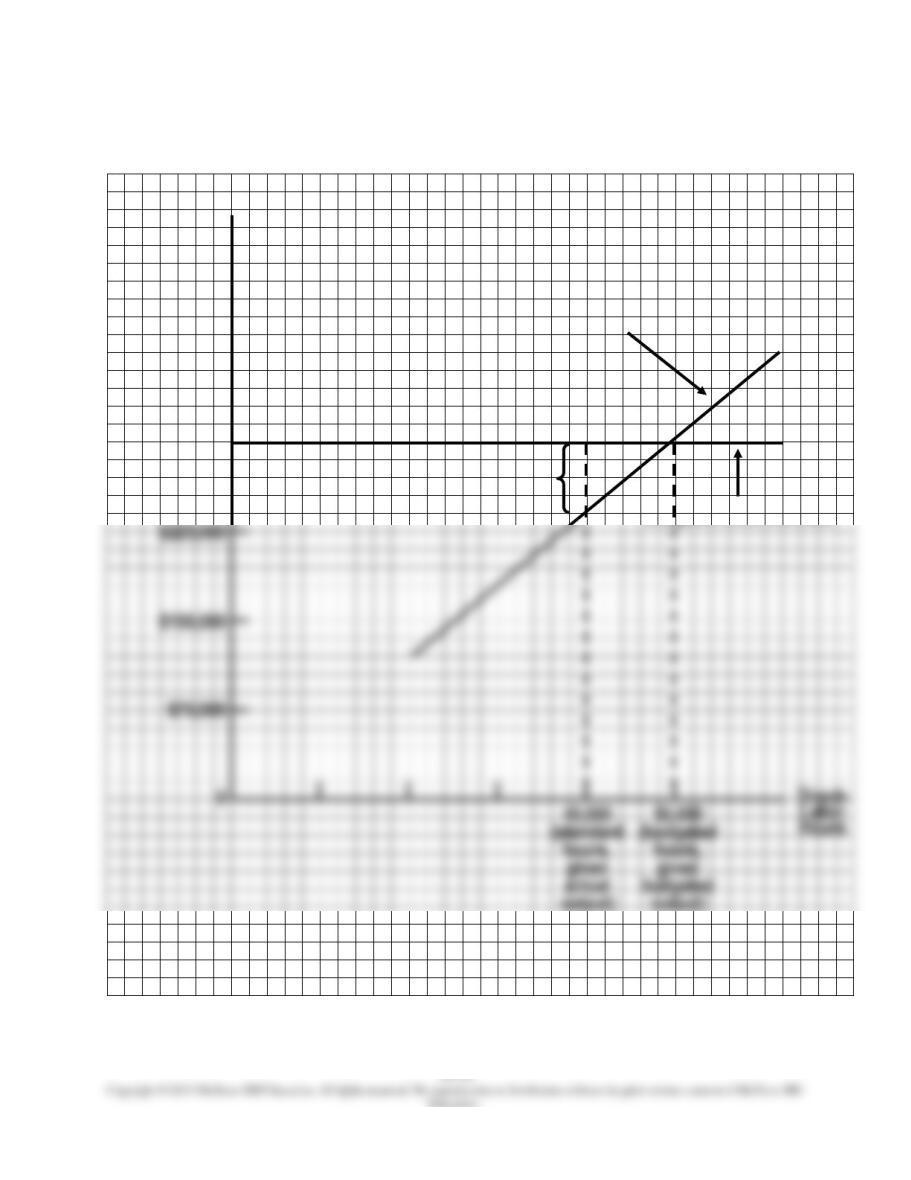

(a) Graphical analysis of variable-overhead variances*:

Rate

$19.20

$18.00

(standard)

Efficiency

Chapter 11 - Flexible Budgeting and Analysis of Overhead Costs

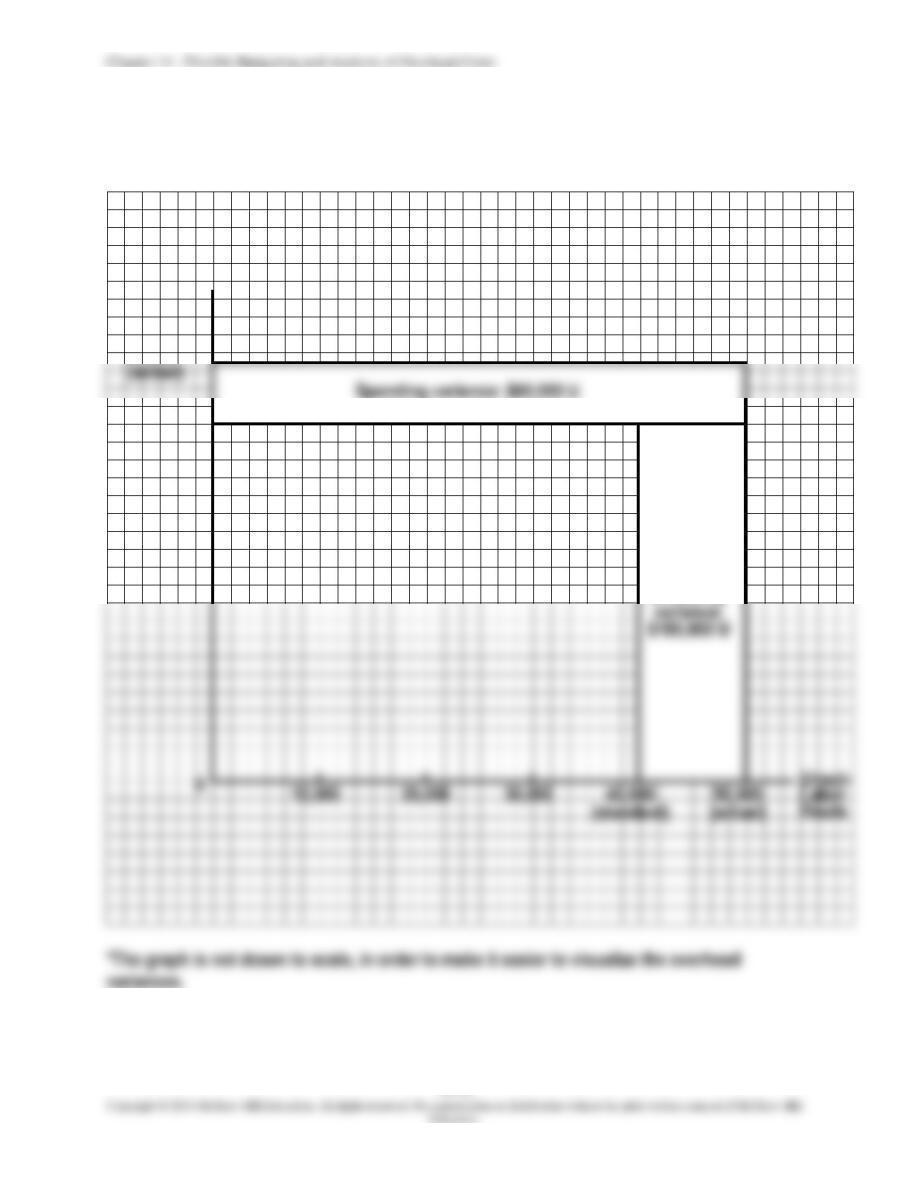

EXERCISE 11-27 (CONTINUED)

(b) Graphical analysis of budgeted versus applied fixed overhead:

Fixed overhead

Applied fixed overhead:

$6.00 per hour

Volume variance: $60,000

Budgeted fixed overhead

$300,000

EXERCISE 11-28 (15 MINUTES)

Memorandum

Date:

Today

To:

I. Makit, Production Supervisor

From:

I. M. Student, Controller

Subject:

Variable-overhead efficiency variance

The variable-overhead efficiency variance has a misleading name. This variance does not

convey any information about the efficiency with which variable overhead items are used,

EXERCISE 11-29 (30 MINUTES)

1. Answers will vary widely, depending on the governmental unit selected and the

budget items selected by the student. For example, fire fighting costs might be

Chapter 11 - Flexible Budgeting and Analysis of Overhead Costs

EXERCISE 11-30 (10 MINUTES)

1.

Flexible budgeted amounts, using activity-based flexible budget:

a.

Indirect material: $33,000 ($18,000 + $3,000 + $3,000 + $9,000)

2.

Variance for setup cost:

a.

Using the activity-based flexible budget: $1,000 F (actual cost minus flexible

EXERCISE 11-31 (45 MINUTES)

Budgeted fixed overhead .........................................................................................

$ 25,000

Actual fixed overhead ..............................................................................................

$ 32,500a

Budgeted production in units ................................................................

12,500

Actual production in units ................................................................

12,000c

Chapter 11 - Flexible Budgeting and Analysis of Overhead Costs

*Some accountants would designate a positive fixed-overhead volume variance as unfavorable.

EXERCISE 11-31 (CONTINUED)

Explanatory Notes:

a.

Fixed-overhead budget variance

=

actual fixed overhead – budgeted fixed overhead

b.

Total actual overhead

=

actual variable overhead + actual fixed overhead

$356,500

=

X + $32,500

Chapter 11 - Flexible Budgeting and Analysis of Overhead Costs

EXERCISE 11-31 (CONTINUED)

c.

Fixed-overhead rate

=

hours machine budgeted

overhead fixed budgeted

Total applied

overhead

=

total std machine hours total std overhead rate

d.

Actual machine hrs. per

unit of output

=

production actual

hrs. machine actual total

EXERCISE 11-31 (CONTINUED)

f.

Total budgeted overhead (static budget)

=

unit per

hrs. machine standard

production

budgeted

rate overhead

standard total

g.

Fixed overhead volume variance

=

budgeted fixed overhead – applied fixed overhead

EXERCISE 11-32 (15 MINUTES)

1.

Formula flexible budget:

2.

Columnar flexible budget:

Patient Days

30,000

40,000

50,000

Variable electricity cost ............

€ 97,500

€ 130,000

€ 162,500

EXERCISE 11-33 (15 MINUTES)

Production Overhead ....................................................................

1,251,000*

Various Accounts .................................................................

1,251,000

To record actual overhead costs.

Chapter 11 - Flexible Budgeting and Analysis of Overhead Costs

EXERCISE 11-34 (10 MINUTES)

budgeted

actual

($11.50* – $12.00†) 13,500 = $6,750 Unfavorable

−

=

sales

budgeted

sales

actual

variancevolume-Sales

budgeted sales