11

Service Department and Joint Cost Allocation

Solutions to Review Questions

11–1.

Companies allocate costs to estimate or assess the costs of their activities (products,

processes, etc.). It is an estimate and subject to the problem that cost allocation

contains an arbitrary element. Not allocating costs, however, is also an estimate—an

estimate of zero. This may be appropriate for some decisions, but not for others.

Some of the disadvantages (costs) include:

(1) Additional bookkeeping;

11–2.

The three methods of allocating service department costs are the (1) direct method, (2)

step method, and (3) reciprocal method.

11–3.

The essential difference is the allocation of costs among service departments. The

11–4.

Allocations usually begin from the service department that has provided the greatest

proportion of its services to other service departments, or that services the greatest

11–5.

11–6.

11–7.

Joint cost allocations are usually made to assign a cost to a product after the split-off

11–8.

Because net realizable values of the output provide a measure of the economic benefit

11–9.

It could be preferable to use a physical quantities measure if it reflects the economic

benefit ultimately obtainable from the production process, particularly if there is no

11–10.

For joint products, costs of the inputs up to the split-off point are allocated to each of the

11–11.

Solutions to Critical Analysis and Discussion Questions

11–12.

Management might believe there are benefits to the use of allocated costs. An

awareness of total costs may influence managerial behavior and decision making. For

11–13.

Allocating zero costs is another allocation method. It, too, is an arbitrary method.

11–14.

As with all cost allocation methods, there is a cost-benefit trade-off to be made. If the

11–15.

The concepts of direct and indirect are related to a specific cost object within the

organization. Costs that can be attributed to a cost object and can, in both a physical

11–16.

The reciprocal method takes into account all of the services rendered among the

11–17.

11–18.

The addition of an employee in one department will increase the allocation base and,

therefore, reduce the allocation to the department that does not add the employee. The

manager of the department that does not add the employee benefits from the actions of

11–19.

Answers will vary. Before deciding to outsource a service department, a company would

want to consider some of the following. (1) Will the quality of service be the same?

11–20.

Answers will vary. First, it is useful to consider whether there are any reciprocal

services. Both the Library and Career Development make use of Computer Support, but

Computer Support probably uses little or no service from the other two. This suggests a

11–21.

Some managers use fully allocated cost numbers for long-run pricing and other long-run

11–22.

The two situations are similar in that the conceptual treatment of the allocation problem

11–23.

11–24.

The allocation of joint cost is similar to that of fixed costs in the sense that if I sell less of

Solutions to Exercises

11–25. (15 min.) Why Costs Are Allocated—Ethical Issues: Giga-Corp.

a. The president of Stable Division would probably prefer to allocate Personnel costs

11–26. (20 min.) Cost Allocation—Direct Method: Caro Manufacturing.

Direct Method:

To

From

Machining

Assembly

Maintenance ………………………………

$25,000a

$15,000

Cafeteria ……………………………………

costs by Maintenance are ignored.)

11–27. (30 min.) Allocating Service Department Costs First to Production

Departments and Then to Jobs: Caro Manufacturing.

Machining

Assembly

Total

Costs allocated to each department

(from Exercise 11.26) ………………………………….

$41,000

$31,000

$72,000

Allocation bases:

Total ………………………………………………………

270

330

Department rates:

11–28. (15 min.) Cost Allocation–Direct Method: University Printers

Maintenance

Personnel

Printing

Developing

Service department

costs ………………………………………………………….

$5,000

$12,000

–0–

–0–

$1,250

11–29. (25 min.) Cost Allocation—Step Method: Caro Manufacturing.

a. Step Method—Maintenance First:

To

From

Maintenance

Cafeteria

Machining

Assembly

Service department costs ……………………………..

$40,000

$32,000

b. Step Method—Cafeteria First:

To

From

Cafeteria

Maintenance

Machining

Assembly

Service department costs ……………………………..

$32,000

$40,000

11–30. (20 min.) Cost Allocation—Step Method: University Printers

Maintenance

Personnel

Printing

Developing

Service department costs ……………………………..

$ 5,000

$12,000

NA

NA

(13,000)

1,000

(1,000 + 1,000 + 3,000)

3,000

(500 + 2,000)

11–31. (30 min.) Cost Allocation—Reciprocal Method: Caro Manufacturing.

Set up the equations:

S2 (Cafeteria)

=

+

Substituting, the first equation into the second yields,

S2

=

$32,000 + 0.20 ($40,000 + 0.80 S2)

S2

=

$32,000 + $8,000 + 0.16 S2

S2

=

$47,619

S1

=

$40,000 + 0.80 ($47,619)

S1

=

$78,095

Allocations

Cost Allocation To:

From:

Maintenance

Cafeteria

Machining

Assembly

4,762

4,762

Service dept.

11–32. (30 min.) Cost Allocation—Reciprocal Method, Two Service Departments:

Kim & Co.

Set up the equations:

Total service

department costs

=

Direct costs of

the service

department

+

Cost allocated

to the service

department

11–32 (continued)

Allocations

Cost Allocation To:

From:

Administration

Factory Support

Fabrication

Assembly

Finishing

Service department costs ..

$480,000

$1,250,000

—

—

—

Administrationa ………………

(630,208)

$252,084

$ 189,064

$ 126,040

$ 63,020

Direct costs …………………..

11–33. (35 min.) Cost Allocation—Reciprocal Method: University Printers

Set up the equations:

Total service

department costs

=

Direct costs of

the service

department

+

Cost allocated

to the service

department

=

+

=

Substituting the value of S2 back into the first equation gives,

Allocations

Cost Allocation To:

From:

Maintenance

Personnel

Printing

Developin

g

11–34. (15 min.) Evaluate Cost Allocation Methods: University Printers

a. The answer to this question depends on the cost and benefits of each method. The

b. The value of any particular method depends on how the numbers will be used. If the

11–35. (15 min.) Reciprocal Cost Allocation – Outsourcing a Service Department:

Caro Manufacturing

To determine the avoidable cost, first determine the variable cost (including the

variable cost of reciprocal services for the maintenance department). This can be

done by setting up the equations for the reciprocal method using only variable costs.

Set up the equations:

11–36. (15 min.) Reciprocal Cost Allocation – Outsourcing a Service

Department: University Printers.

To determine the avoidable cost, first determine the variable cost (including the

variable cost of reciprocal services for the maintenance department). This can be

done by setting up the equations for the reciprocal method using only variable costs.

11–37. (15 min.) Net Realizable Value Method: Euclid Corporation.

Total joint costs are $432,000 (based on the $144,000 materials plus $288,000

conversion). These costs are allocated as follows:

To Output P-11:

11–38. (20 min.) Estimated Net Realizable Value Method: Blasto, Inc.

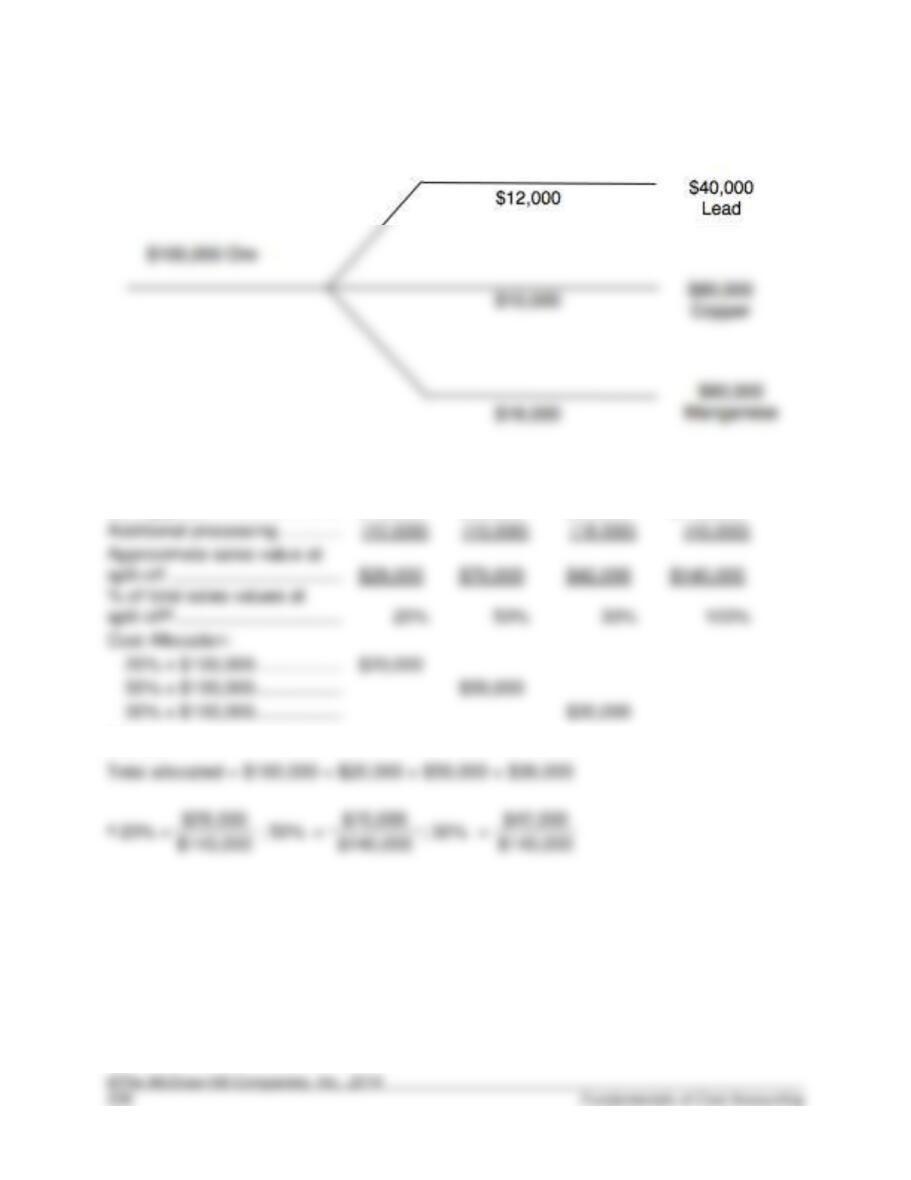

Although not required, the process may be diagrammed as follows:

The diagram can be used to help organize the solution, which follows:

Lead

Copper

Manganese

Total

Selling price ……………………………………………….

$40,000

$80,000

$60,000

$180,000

Additional processing …………………………………..

(40,000)

split-off ………………………………………………………

Cost Allocation:

$30,000

Check:

11–39. (20 min.) Net Realizable Value Method To Solve For Unknowns: GG

Products, Inc.

Since the sales value of each product at the split-off point is available, the appropriate

11–40. (10 min.) Net Realizable Value Method: Bixel Components.

11–41. (10 min.) Net Realizable Value Method with By-Products: Butterfly

Company.

11–42. (15 min.) Net Realizable Value Method: Deming & Sons.

The net realizable value method is a cost allocation method that allocates joint costs in

proportion to the net realizable value of the individual products. The calculation is:

Net Realizable

Value at

Split-Off

($000)

Allocation

Joint Costs

Allocated

W-10 ………….

$ 336

(336 ÷ 960)

x

$384,000

$134,400

W-40 ………….

(144 ÷ 960)

x

Note: The costs incurred after split-off are not joint costs and are therefore not

included.

11–43. (15 min.) Physical Quantities Method: Deming & Sons.

The physical units method is a cost allocation method that allocates joint costs in

proportion to the units produced of the individual products. The calculation is:

Production

(units)

Allocation

Joint Costs

Allocated

W-10 ………….

x

$384,000

$134,400

W-40 ………….

x

11–44. (15 min.) Sell or Process Further: Deming & Sons.

Product W-10. The sales value at split-off is $336,000. If processed further, the sales

value is $30,000 more, but you incur an additional $36,000 in processing costs. The

11–45. (20 min.) Physical Quantities Method: Kyle Company.

a.

Total units of KA ………………

=

84,000

units

Total units produced …………

=

units

Joint product costs ……………

=

$189,000

b.

Net realizable value of KB at split-off ……..

=

$210,000

Total net realizable value at split-off ………

=

600,000

Joint product costs ………………………………

=

Additional processing costs ………………………….

11–46. (20 min.) Physical Quantities Method; Sell or Process Further: Kyle

Company.

a.

When KC can no longer be sold and must be disposed of, the disposal costs become

part of the joint cost of production for KA and KB. Using the physical units method,

the allocated costs are:

11–47. (20 min.) Physical Quantities Method With By-Product: Trans-Pacific

Lumber

The allocation computations are:

To Grade-A Lumber:

Solutions to Problems

11–48. (50 min.) Step Method With Three Service Departments: Model, Inc.

a. To facilitate the solution, reduce the different allocation bases to proportions used by

departments other than the same department.

Proportion Used By

Administration

Accounting

Maintenance

Molding

Painting

Building Area ………………………………………………

—a

.06b

.04b

.72

.18

Employees …………………………………………………

.35

.50

11-48. (continued)

Model, Inc.

Step Method

To

Maintenance

Accounting

Administration

Molding

Painting

Direct Costs ……………………………………………….

$200,000

$400,000

$250,000

$687,500

$485,000

FROM

Maintenancea ……………………………………………..

(200,000)

40,000

2,000

104,000

54,000

_________

_______

(.01 + .20 + .52 + .27)

(.01 + .20 + .52 + .27)

(.72 + .18)

11-48. (continued)

b.

Molding

Painting

Direct materials …………………………………………..

$237,500

$210,000

Direct labor ………………………………………………..

337,500

200,000

Overhead (direct) ………………………………………..

112,500

Overhead (allocated) …………………………………..

Molding:

$1,190,632 ÷ 100,000 units …………………………..

=

Painting:

=

c. Unit cost of allocated service department costs:

11–49. (40 min.) Comparison of Allocation Methods: BluStar Company.

a. Direct Method:

Administration

Accounting

Domestic

International

Department costs …………………………..……………

$360,000

$144,000

$936,000

$3,600,000

a

$288,000

(45 + 180)

b

(20,000 + 80,000)

x $144,000

45

b. Step Method—Administration First:

To

From

Admin

Accounting

Domestic

International

Department costs ………………………………………..

$936,000

$3,600,000

a

$ 36,000

=

25

x $360,000

(25 + 45 + 180)

=

x $360,000

(25 + 45 + 180)

=

x $360,000

(25 + 45 + 180)

=

x $180,000

=

x $180,000

(20,000 + 80,000)

11-49. (continued)

c. Reciprocal Method:

Set up the equations:

Total service

department costs

=

Direct costs of

the service

department

+

Cost Allocated

to the Service

Department

S1 (Administration)

=

$360,000

+

0.20 S2

=

Allocations:

Administration

Accounting

Domestic

International

d.

Regardless of the allocation method used, the final allocations are the same. The

11–50. (40 min.) Solve For Unknowns: Frank’s Foods.

a. Since the direct method is used, Operations Support’s (S2’s) costs are allocated

only to P1 and P2, not to S1.

To find the cost of S2’s services:

b.

Amount allocated from S2 to P1

=

$45,000

= (

.5

x

$72,000

)

.5 + .3

11–51. (40 min.) Solve For Unknowns: RT Renovations.

11–52. (60 min.) Cost Allocation—Step Method With Analysis And Decision

Making: Steamco Corporation.

11–52. (continued)

b.

Let:

S1

=

Steam generation

S2

=

Electric generating—fixed

S3

=

Electric generating—variable

P1

=

Alpha

P2

=

Beta

Allocation:

To Department:

(Direct Costs Shown Below Department)

S4

S2

S3

P1

P2

$144

$90

$240

$1,800.00

$1,320.00

Amount to

From department:

be allocated

Steam generation

(S1)a …………………………………………………………

$ 210

84

21.00

105.00

18

90.00

27.00

40.50

67.50

variable (S3)d ……………………………………………..

215.47

117.53

c. If the company could realize $174,000 from the sale of the steam, then the relevant

costs would be:

11–53. (30 min.) (Appendix) Cost Allocations—Reciprocal Method (Computer

Required): Steamco.

The total costs of the two producing departments include their direct costs. The

allocated costs, therefore, are:

11–54. (30 min.) Cost Allocation— Step Method, Reciprocal Method: Great

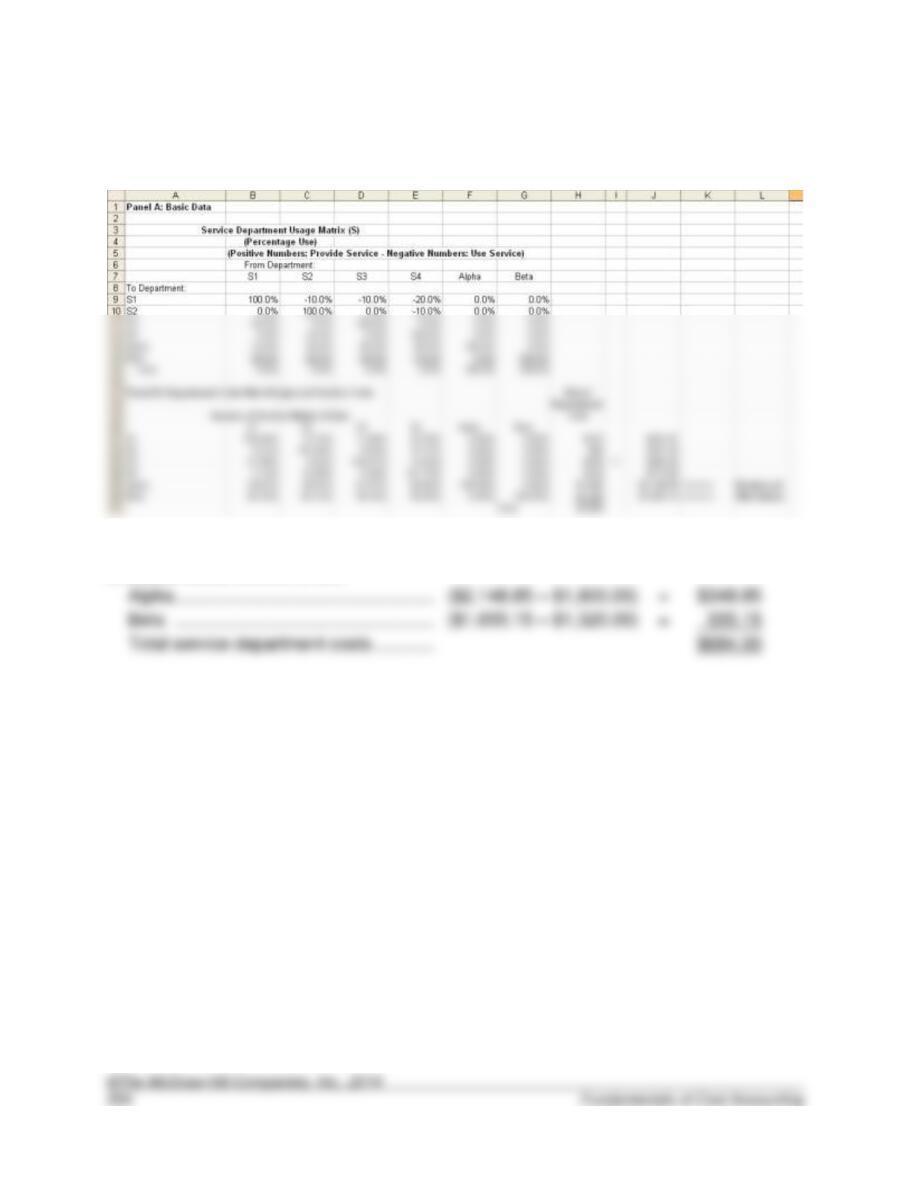

Eastern Credit Union.

a. The key to this problem is to recognize that Administration provides no service to

either of the other two service departments and that Processing only provides

Allocated to:

Costs

Processing

Adminstration

Branches

Electronic

Maintenance

$220,000

$22,000

(10%)

$44,000

(20%)

$44,000

(20%)

$110,000

(50%)

Total

11–55. (30 min.) Cost Allocation— Step Method and Reciprocal Method: Midland

Resources.

The key to this problem is to write out the equations expressing the usage:

Substituting the equations for Engineering and Maintenance into the equation for

Administration yields:

Allocated to:

Costs

Fabrication

Assembly

Engineering

$81,000

Maintenance

Total

$8,100

$32,400

11–56. (35 min.) Allocate Service Department Costs: State Financial Corp.

11–57. (45 min.) Allocate Service Department Costs—Ethical Issues: FSP.

a. Direct Method:

Member

Department

Commercial

Department

Total

Accounting …………….

$8,000a

$8,000a

$16,000

Computer Services ….

12,320b

.40

.10

.40

d. Step Method:

Computer

Services

Accounting

Member

Department

Commercial

Department

Before allocation …………

$61,600

$16,000

$ –0–

$ –0–

Accounting …………………

(.50 + .10 + .40)

(.50 + .10 + .40)

11-57. (continued)

e. Reciprocal Method:

Set up the equations:

Total service

department costs

=

Direct costs of

the service

department

+

Cost Allocated

to the Service

Department

S1 (Accounting)

=

+

S2 (Computer Services)

=

+

Substituting, the first equation into the second yields,

S2

=

61,600 + 0.20 ($16,000 + 0.50 S2)

=

61,600 + 3,200 + 0.10 S2

=

S2

=

S1

=

=

Allocations

From:

Accounting

Computer

Service

Member

Commercial

Costs …………………………..…………………………….

department costs

=

department

+

Department

11–58. (45 min.) Reciprocal Cost Allocation – Outsourcing a Service Department:

BluStar Company.

a. To determine the avoidable cost, first determine the variable cost (including the

b. Using the same approach, the avoidable cost from outsourcing Accounting is

$69,000 (= $36,000 + $15,000 + $18,000 avoidable fixed costs).

Total service

department costs

=

Direct costs of

the service

department

+

Cost Allocated

to the Service

Department

11–59. (45 min.) Reciprocal Cost Allocation – Outsourcing a Service Department:

Great Eastern Credit Union.

To determine the avoidable cost, first determine the variable cost (including the

variable cost of reciprocal services for the Processing department). This is done by

11–60. (15 min.) Reciprocal Cost Allocation – Outsourcing a Service Department:

Great Eastern Credit Union.

11–61. (45 min.) Net Realizable Value of Joint Products: Davenport Company.

a. $375,000

Since there is no further processing for Beta-1 after split-off, the net realizable value

is simply the sales value of all units produced.

11–61. (continued)

Net realizable value of Beta-1 ……………………….

$375,000a

Net realizable value of Beta-2 ……………………….

225,000b

Net realizable value of Beta-3 ……………………….

Additional processing costs:

Direct labor ………………………………………………..

Overhead …………………………………………………..

Total cost of Beta-2 ………………………………….

$1,125,000

Cost per unit

=

=

$1.1667/unit

11–62. (40 min.) Estimated Net Realizable Value and Effects Of Processing

Further: Fletcher Fabrication, Inc.

a.

Departments

Production Costs

X

Y

Z

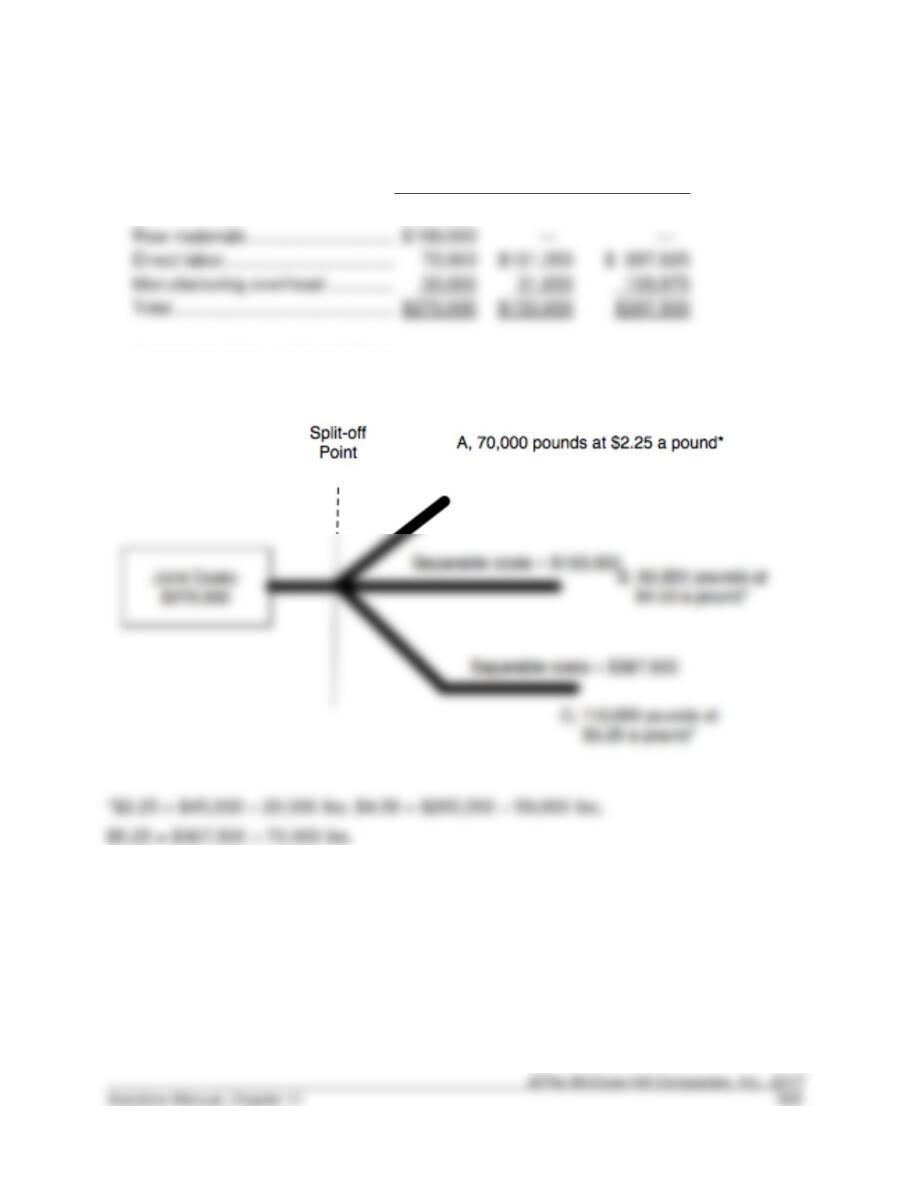

A diagram of the problem follows:

11–62. (continued)

Product A

Product B

Product C

Total

1.

Selling price per pound:

A: $45,000 20,000 …………………………………

$2.25

C: $367,500 70,000 ……………………………….

$5.25

Multiply by pounds produced:

A: 20,000 + 50,000 …………………………………..

C: 70,000 + 40,000…………………………………..

_______

Gross sales values ……………………………………..

Less costs of separate processing:

A: — ………………………………………………………

B: $121,350 + $31,650 ……………………………..

C: $287,625 + $109,875 …………………………...

Percentage of total ………………………………………

Allocation:

A: 35% x $270,000

=

$94,500

B: 25% x $270,000

=

C: 40% x $270,000

=

108,000

11–62. (continued)

3. and 4.

Total Costs

Cost of

Goods Sold

Ending

Inventory

Product A:

Joint costs allocated …………………………………

$ 94,500

Sold: (20,000 70,000) x $94,500 ……………..

$ 27,000

Inventory …………………………..……………………

$ 67,500

Product B:

Joint costs allocated …………………………………

Separate processing costs ………………………..

Total, all sold ………………………………………………

Product C:

Joint costs allocated …………………………………

Separate processing costs ………………………..

Total costs of Z ………………………………………..

$505,500

$505,500 …………………………………..

Inventory …………………………..……………………

________

Totals ………………………………………………………..

$820,500

$569,182

$251,318

Proof of total:

Raw material cost Dept. X …………………………

$168,000

Direct labor cost—X …………………………………

72,000

Direct labor cost—Y …………………………………

Direct labor cost—Z …………………………………

Manufacturing overhead—X …………………………

Manufacturing overhead—Y …………………………

Manufacturing overhead—Z …………………………

Total costs accounted for ……………………………..

$820,500

b.

Incremental revenue of further processing

A: ($12.90 – $2.25 forgone) x 70,000 ………….

Incremental costs of further processing

B: $6.00 x 70,000 …………………………………….

11–63.

(35 min.) Find Missing Data—Net Realizable Value: Spartan Chemicals.

Spartan must be using the net realizable value method because the ratio of G-1’s joint

costs to the total does not equal the ratio of G-1’s physical units to the total.

a. Allocate joint costs to G-3:

c and d. The ratio of sales value at split-off for each product to total sales value at split–

off equals the joint cost ratio:

11–64.

(35 min.) Find Missing Data—Net Realizable Value: Blaine, Inc.

Blaine must be using the net realizable value method because the ratio of Argon’s joint

costs to the total does not equal the ratio of Argon’s physical units to the total.

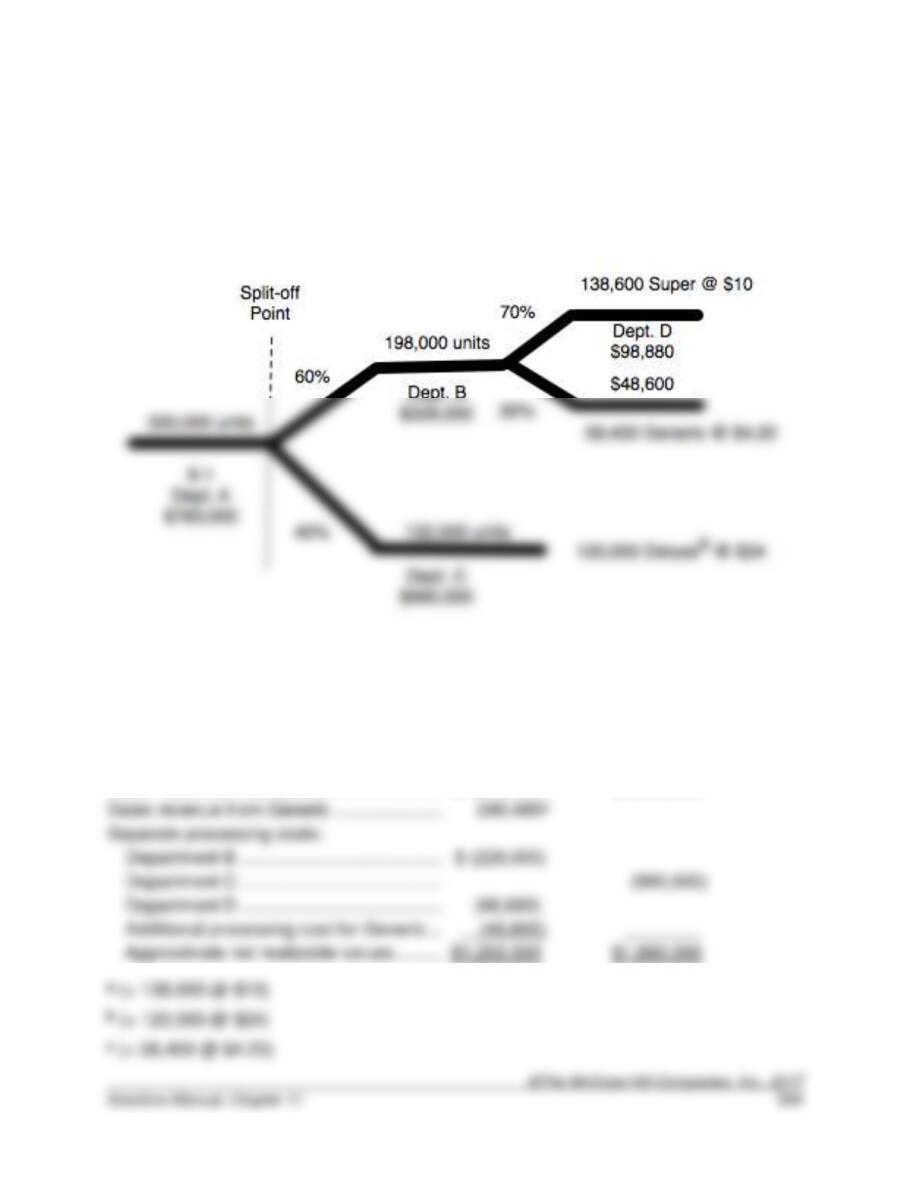

11–65. (50 min.) Joint Costing In A Process Costing Context—Estimated Net

Realizable Value Method: West Coast Designs.

It is helpful to diagram the flow of units before attempting to solve the problem.

a120,000 good output = 132,000 ÷ 110%

The next step is to determine the net realizable values of Super and Deluxe at the first

split-off.

Super

Deluxe

Sales value after completion …………………………

$1,386,000a

$2,880,000b

Separate processing costs:

11-65. (continued)

Cost allocation:

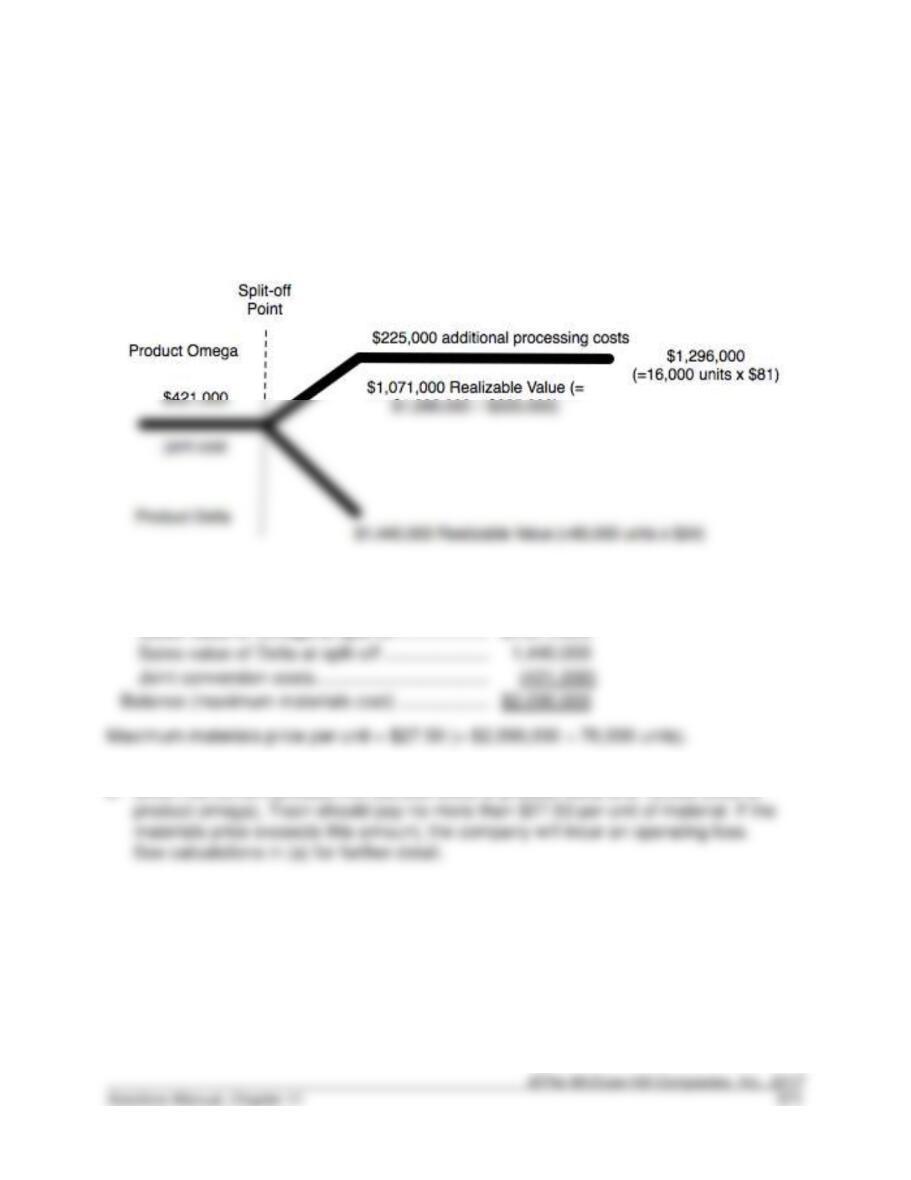

11–66. (35 min.) Find Maximum Input Price—Estimated Net Realizable Value

Method: Ticon Corporation.

a. A diagram of the operation appears as follows:

The total allowable materials costs would then be:

11–67. (30 min.) Effect Of By-Product versus Joint Cost Accounting: Fisher

Chemicals.

a. (1) Accounted for as a joint product.

(2) Allocated for as a by-product.

Allocation:

11–68. (30 min.) Joint Cost Allocation and Product Profitability: Prescott Lumber

a. Allocation on the basis of units of output

Grade A:

b. Allocation on the basis of market value

Grade A:

Grade B:

Allocated cost of logs ………………….

c. It is not possible to determine which product is more profitable. One cannot be

produced without the other—hence only the profitability of the total output is

relevant. Use of the physical quantities measured in Part (a) would suggest that

Solution to Integrative Case

11–69. (60 min.) Effect of Cost Allocation on Pricing and Make versus Buy

Decisions: Ag-Coop

a. Output:

Output Mix

Kwh per lb.

Kwh per 100 lbs. Input

Greenup …………………………………………………….

50

%

32

1,600

Maintane ……………………………………………………

30

20

Maximum processing:

750,000 kwh ÷ 3,000 kwh per 100 lbs.

25,000 lbs. of input

Fixed cost allocation ……………………………………

25,000

=

per lb.

11-69. (continued)

b. Total joint cost incurred in processing 25,000 lbs. of input =

Quantities of each product produced:

Greenup …………………………………………………….

25,000

x

.5

=

12,500

Maintane ……………………………………………………

25,000

x

.3

=

25,000

Greenup …………………………………………………….

12,500

$105,000

$118,750

x

($105,000 ÷ $200,600)

12,500 lbs.

11-69. (continued)

c. The profit under current production schedule A is:

Total net realizable value

=

$200,600

(from b above)

Outputs under alternative production schedule B:

Product

Output Mix

Unit kwh Usage

Usage per 100 Lbs. of Input

Maintane

Amount of Maintane produced

=

22,590

x

=