303

CHAPTER 11

Investing Activities

THINKING BEYOND THE QUESTION

How do we account for investing activities?

Investing is necessary for a company to grow. Good investments provide

resources that a company can use to produce and sell additional prod-

QUESTIONS

Q11-1 The primary types of assets Archer would include in its accounting sys-

tem are:

a. Current assets: those assets management expects to convert to

cash or consume during the next fiscal year.

i. Cash and short-term marketable securities: highly liquid re-

b. Long-term assets: those assets that management does not expect to

convert to cash or consume during the next fiscal year.

i. Property, plant, and equipment: physical assets used by the

304 Chapter 11

Q11-2 The gross amount of property, plant, and equipment is the original cost

paid to acquire those assets. The net amount of property, plant, and

Q11-3 Student responses will vary. Some students will note that interest is the

cost of renting money. It is a period cost that is traceable to a given peri-

od and should be expensed on the income statement during that period.

Q11-4 This statement is not true. Sometimes the units–of-production method will

lead to faster depreciation than straight-line and sometimes it will lead to

Q11-5 A capital expenditure is one in which new plant assets are acquired or in

which the expected useful life or value of a plant asset is enhanced. Capi-

Q11-6 In a way the friend is correct. The terms depletion and depreciation both

describe the process of allocating a portion of an asset’s cost to expense

each period of the asset’s useful life. In this way, both terms describe the

Investing Activities 305

Q11-7 Depletion arises when a natural resource is consumed or used up. In

most cases, it arises when the natural resource is harvested. For exam-

ple, ore is taken from a mine, oil is pumped from a well, or gravel is taken

Q11-8 The problem with using market value (for most classes of assets) is ob-

taining a reasonable estimate of market value at each balance sheet date.

For example, what is the market value on a given balance sheet date for

the Empire State Building? Or for a patent, or machinery in the factory?

Q11-9 Investments in the securities of other firms (e.g., stocks, bonds, certifi-

cates of deposit, notes) are classified on a balance sheet according to

management’s intention for holding the item. If the investment was made

Q11-10 When marketable securities are held as trading securities it means that

the company routinely sells securities as part of its primary business. In

fact, they are more like inventory than investments. The securities are a

current asset and expected to be sold soon. Therefore, it is appropriate

306 Chapter 11

Q11-11 Marketable securities and intangible assets have very different character-

istics. It is these differences that cause them to be reported using differ-

ent valuation methods. First, marketable securities are homogeneous in

Q11-12 Goodwill arises when one company buys another at a price in excess of

the market value of the second company’s identifiable net assets. The

amount of goodwill recorded is equal to the difference between the price

paid and fair value of identifiable net assets acquired. Goodwill repre-

Investing Activities 307

Q11-13 The effects of this transaction will show up in two places on the next

statement of cash flows. First, the gain on sale ($25,800) will be reported

in the operating activities section as a deduction from net income. The

Q11-14 Accounting information identifies the amounts of assets that a company

has recorded. These amounts and other records about a company’s as-

sets provide a benchmark against which actual assets can be compared.

For example, if accounting records indicate a cash balance of $30,000, an

308 Chapter 11

EXERCISES

E11-2 Deep Drillers, Inc.

Long-Term Assets Section of Balance Sheet

At Year-End

Investments:

Investment in Susanna Company $ 195,600

Property, Plant, and Equipment:

E11-3 a. Intangible assets: A long-term asset category including items such

as patents, copyrights, trademarks, and goodwill

b. Inventories: A current asset composed of items that are being held

for sale to customers

c. Investment in marketable securities: a current or long-term asset,

depending on the holding period intended by management

Investing Activities 309

d. Property, plant, and equipment: A long-term asset including such

items as trucks, buildings, machinery, and equipment

E11-4 Long-term investments: (h) Common stock of Flower Corporation

(l) Investment in bonds of Beech Brothers, Inc.

Property, plant, and

equipment: (a) Machinery, net

E11-5

Depreciation

Method

Depreciation

Expense

Computations

Straight-line

$42,857

($300,000 ÷ 7 years = $42,857)

($300,000 × 2/7 = $85,714)

production

= $96,000)

(continued)

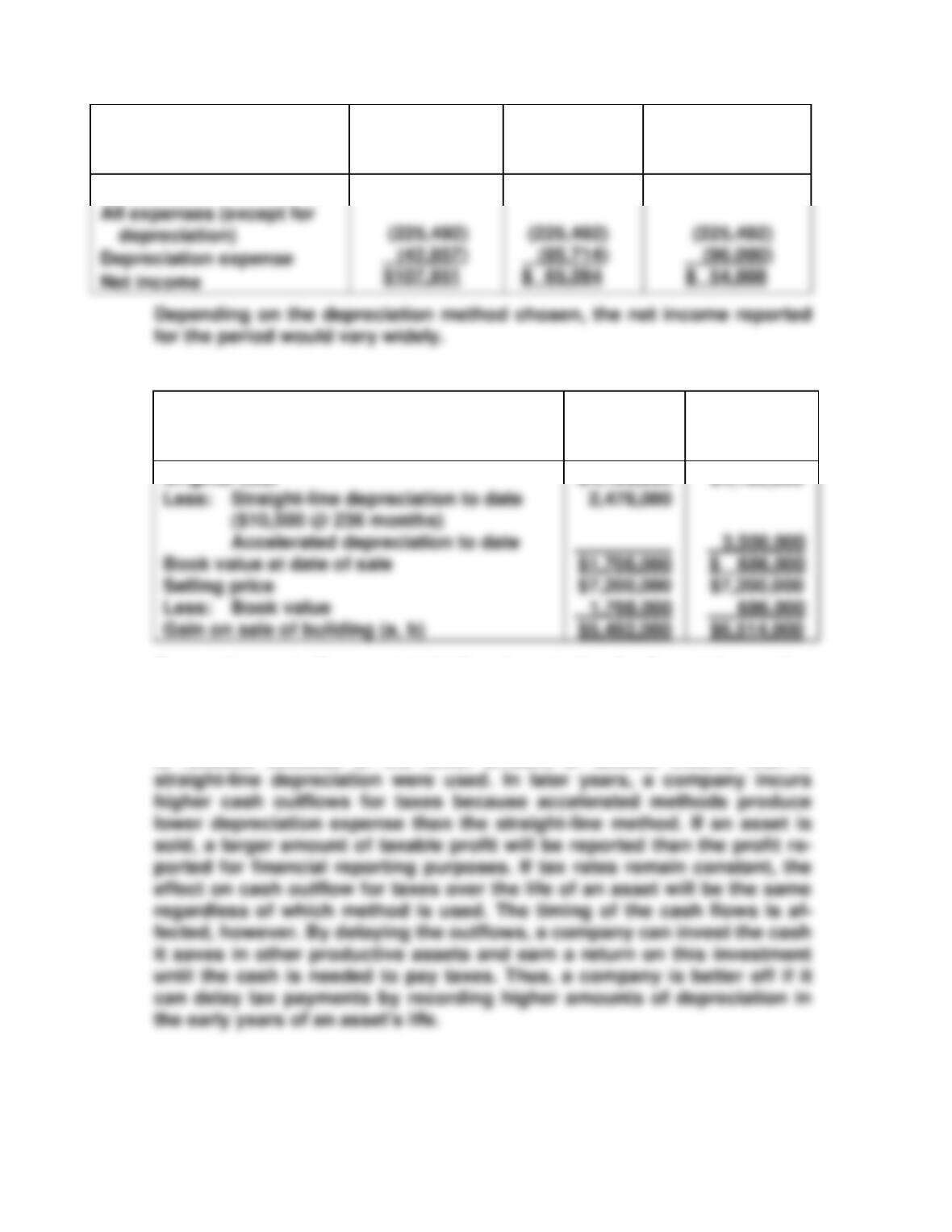

310 Chapter 11

Income Statements

Straight-

Line Method

DDB

Method

Units-of–

Production

Method

Revenues

$376,300

$376,300

$ 376,300

E11-6

Calculation of Gain on Sale

Financial

Reporting

Purposes

Tax

Purposes

Original cost

$4,186,000

$4,186,000

Companies typically use straight-line depreciation for financial reporting

purposes to minimize the effect of depreciation on net income. Accelerat-

ed methods result in larger amounts of depreciation expense for tax pur-

poses in the early years of asset lives. Therefore, cash outflow for taxes

is reduced because of the lower amount of taxable income than if

Investing Activities 311

E11-7 a. Cost of equipment $ 480,000

Less: Depreciation per year

[($480,000 − $30,000) ÷ 8 years = $56,250]

Accumulated depreciation total over 5 years 281,250

E11-8 a. The total construction costs, $1,228,000, would be recorded as an

asset, construction work–in-process. Special tools and equipment

necessary for the construction and interest for financing the con-

struction would be included as part of the asset. The cost would be

E11-9 a. 2004 = $9,000 ($48,000 − $3,000) ÷ 5 years = $9,000

2005 = $9,000

312 Chapter 11

c. 2004 2005 2006 2007

Operating activities:

Depreciation expense $ 9,000 $ 9,000 $ 9,000 $ 5,250

E11-10 Depletion expense: $16.8 million ($140 million × 6 ÷ 50)

Book value of reserves: $39.2 million ($140 million − $100.8 million*)

E11-11 a. $1,650,000 The cost of the land ($4,500,000) should be recorded in

an account separate from the cost of the trees growing

on the land. The cost to be depleted includes the cost of

planting the trees and the cost of thinning and monitor-

Investing Activities 313

E11-12

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

a.

Cash

−30,000

Long-Term Investment

30,000

E11-13

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

a.

Cash

−330,000

330,000

Cash

−440,000

Short-Term Investment in

440,000

20,000

Unrealized Holding Gain*

−80,000

Unrealized Holding Loss*

Short-Term Investment in

At year-end, the two investments should be combined and reported in the

asset section as short-term investments, $710,000 ($330,000 + $440,000 +

Unrealized Holding Gain*

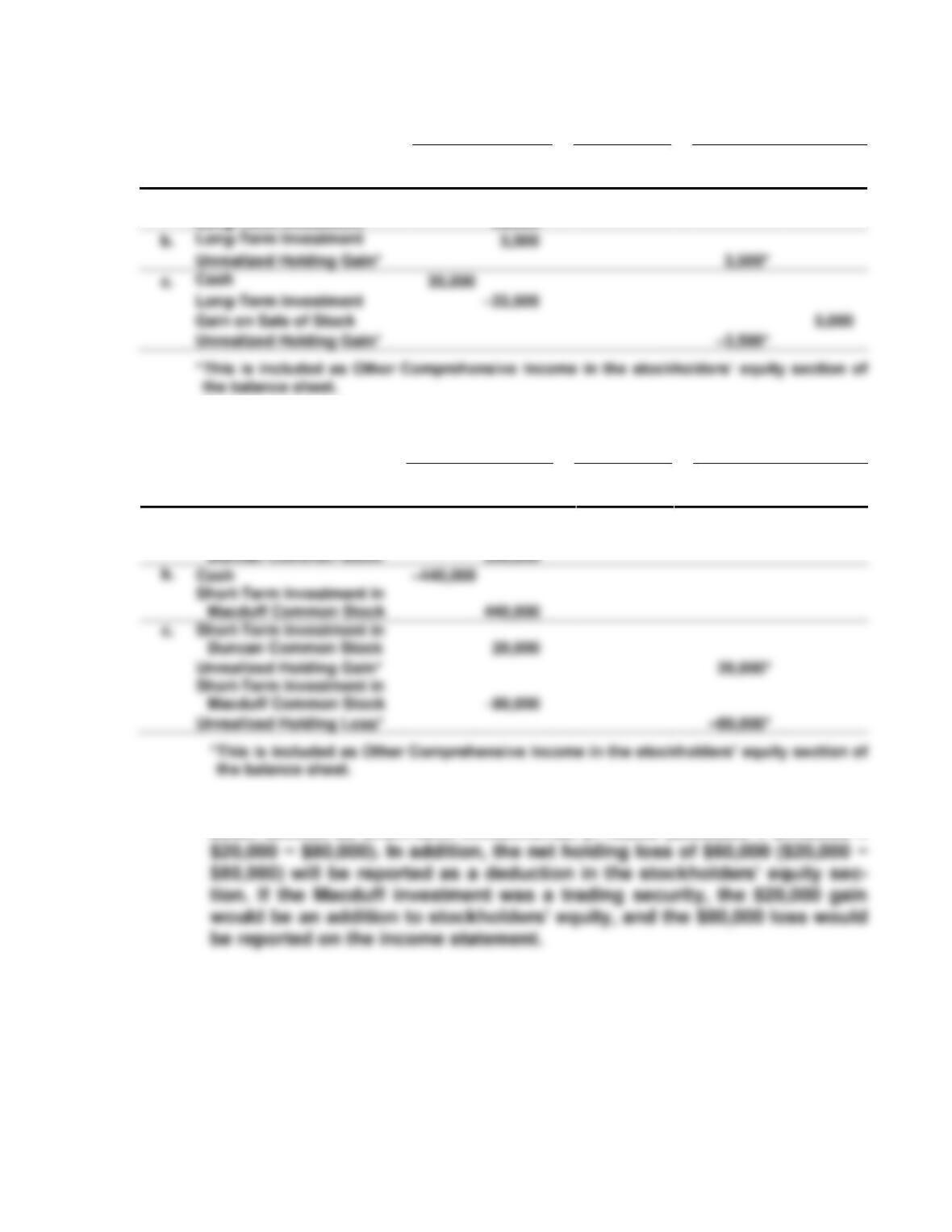

c.

Long-Term Investment

−33,500

Gain on Sale of Stock

Unrealized Holding Gain*

E11-14

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

a.

Cash

−314,000

Long-Term Investment in

Othello Common Stock

314,000

Cash

−418,000

418,000

Long-Term Investment in

Unrealized Holding Gain*

Ferdinand Common Stock

Unrealized Holding Loss*

At year-end, the two investments should be combined and reported in the

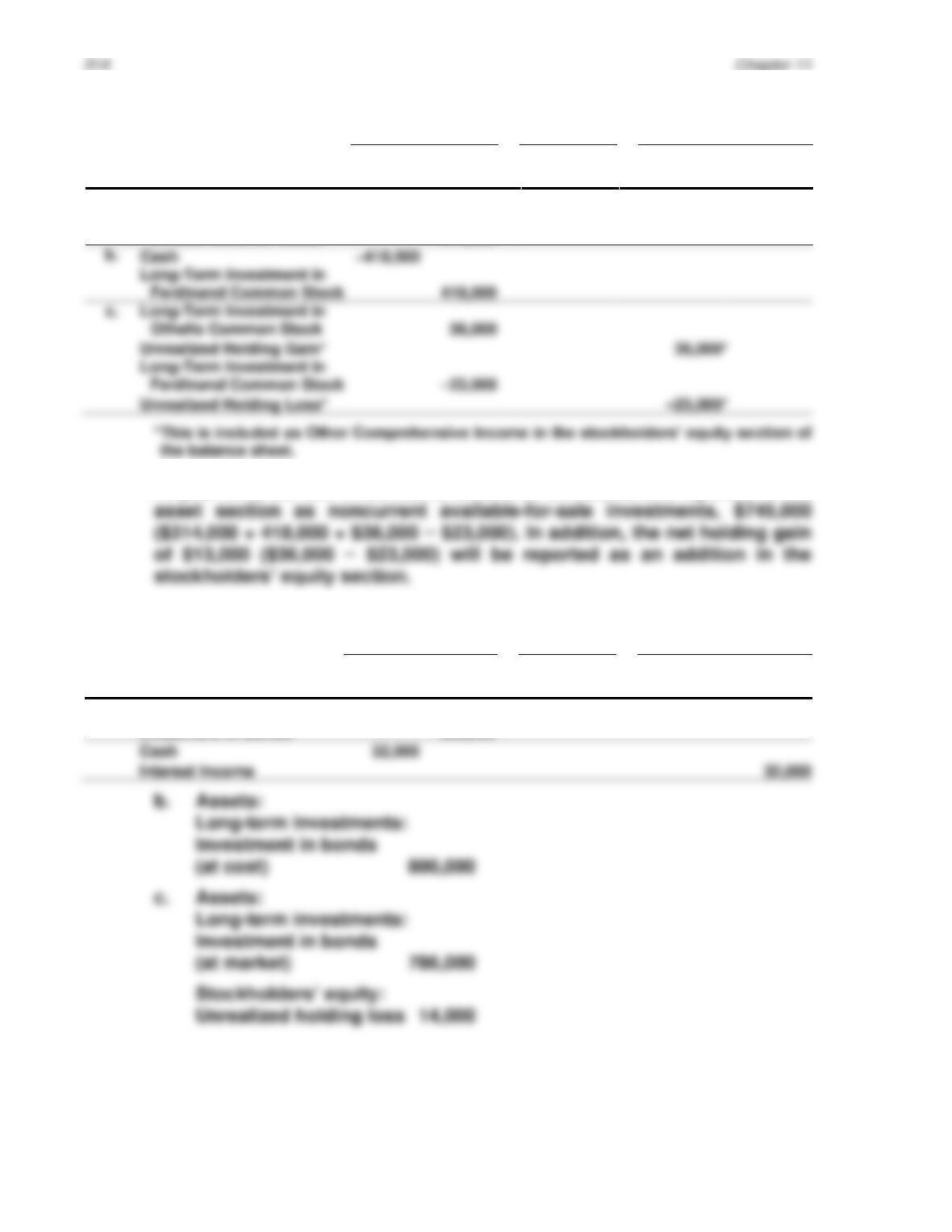

E11-15 a.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Cash

−800,000

Investment in Bonds

800,000

Cash

Interest Income

Investing Activities 315

E11-16 1.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

May 15,

Cash

−380,000

2005

Long-Term Investment

380,000

Apr. 6,

Cash

400,000

2007

Long-Term Investment

–440,000

Realized Gain on Sale

20,000

Loss*

Ending Balances

46,400

46,400

Explanations:

May 15, 2005: Investment recorded at cost.

September 12, 2005: Dividends reported as realized income; reported in

the income statement in computing net income for the year.

2. 2005 2006

Cost of investment $380,000 $ 380,000

Sep. 12,

Cash

12,000

2005

Investment Income

12,000

Dec. 31,

Long-Term Investment

100,000

Gain*

Sep. 12,

Cash

14,400

2006

Investment Income

14,400

Dec. 31,

Long-Term Investment

Loss*

316 Chapter 11

E11-17 a. Goodwill arises when one firm buys another. It is the difference be-

b. The key to understanding goodwill is that certain valuable aspects of

c. Goodwill is reported as an intangible asset on the balance sheet of a

d. $30 million. The fair market value of the acquired company’s net as-

e. Sometimes, management of the acquiring firm simply makes a mis-

take by offering more for a company than it is worth. The estimated

E11-18 a. Amount paid to acquire 100% of Metrodome’s net assets $845,000

Fair market value of Metrodome’s net assets 783,000

Goodwill $ 62,000

b. In general, goodwill becomes impaired when the activities that creat-

Investing Activities 317

E11-19 a. 1. $23,017 1st year depreciation: SLN(314221,15000,13)

b. 1. $47,387 1st year depreciation: DDB(118468,5000,5,1)

E11-20 Investing activities are those that involve acquisition, use, and disposal

of long-term assets. Short-term investments in marketable securities are

also part of investing activities.

Balance sheet:

1. Most noncurrent asset accounts involve investing activities. Increases

Income statement:

1. Depreciation, amortization, and depletion are reported as part of oper-

318 Chapter 11

Statement of cash flows:

1. Depreciation, amortization, and depletion expense are added to net in-

come (under the indirect method) in the operating activities section.

E11-21 Zirconium Graphics Company

Partial Statement of Cash Flows

For the Year Ended December 31

Cash Flow from Operating Activities

Net income $ 60,000

Adjustments for noncash items:

Depreciation and amortization expense $ 7,500

E11-22 a. Equity method. This investment was large enough to acquire sig-

Investing Activities 319

b.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Jan. 1

Cash

–43,200

Long-Term Investment

43,200

PROBLEMS

P11-1 A. Depreciation Schedule

Straight-Line

Method

Declining-Balance

Method

Units-of-Production Meth–

od

Year

Depreciation

Expense

Book

Value

Depreciation

Expense

Book

Value

Depreciation

Expense

Book

Value

0

1

$ 30,000

$125,000

95,000

$ 62,500

$125,000

62,500

$ 31,200

$125,000

93,800

Double-declining-balance:

Year 1 = $125,000 × (2/4) = $62,500

Units-of-production (unit depreciation rate is $120,000 ÷ 1,000 hours =

$120 per hour):

Year 1 = $120 per hour × 260 hours = $31,200

Investment Income

Long-Term Investment

320 Chapter 11

B. The straight-line method generally has the advantage of creating the

smallest amount of depreciation expense in the early years of the

asset’s life. Therefore, it would usually result in higher reported net

C. Depreciation expense reduces the book value of an asset but does

not require cash outflow. Cash flow is affected indirectly by depreci-

P11-2 A. B.

Year

Book Value

at

Beginning

of Year

Usual

Double-

Declining-

Balance Method

(2/6 × Book Val-

ue)

Book Value

at Beginning

of Year

Modified

Double-

Declining-

Balance Meth-

od

2007

$2,100,000

$ 700,000

$2,100,000

$ 700,000

Under the modified approach, depreciation for tax purposes in 2007,

2008, and 2009 uses the standard double-declining-balance method (2/6 ×

Investing Activities 321

$311,111 = $622,222). This results in the same amount of depreciation

($207,407) for each of the last three years. In 2011 and 2012, the straight-

pense.

C.

Year

1

Modified Double-

Declining-

Balance Method

2

Straight-Line

Depreciation

(Cost ÷ 6 years)

3

Difference

in Income

(Column 1 −

Column 2)

4

Difference

in Taxes

(Column 3

× 35%)

2007

$ 700,000

$ 350,000

$ 350,000

$122,500

D. The higher the depreciation, the lower is taxable income and the

lower is the amount of cash paid out for taxes. Choosing an acceler-

ated depreciation method raises depreciation in the earlier years of

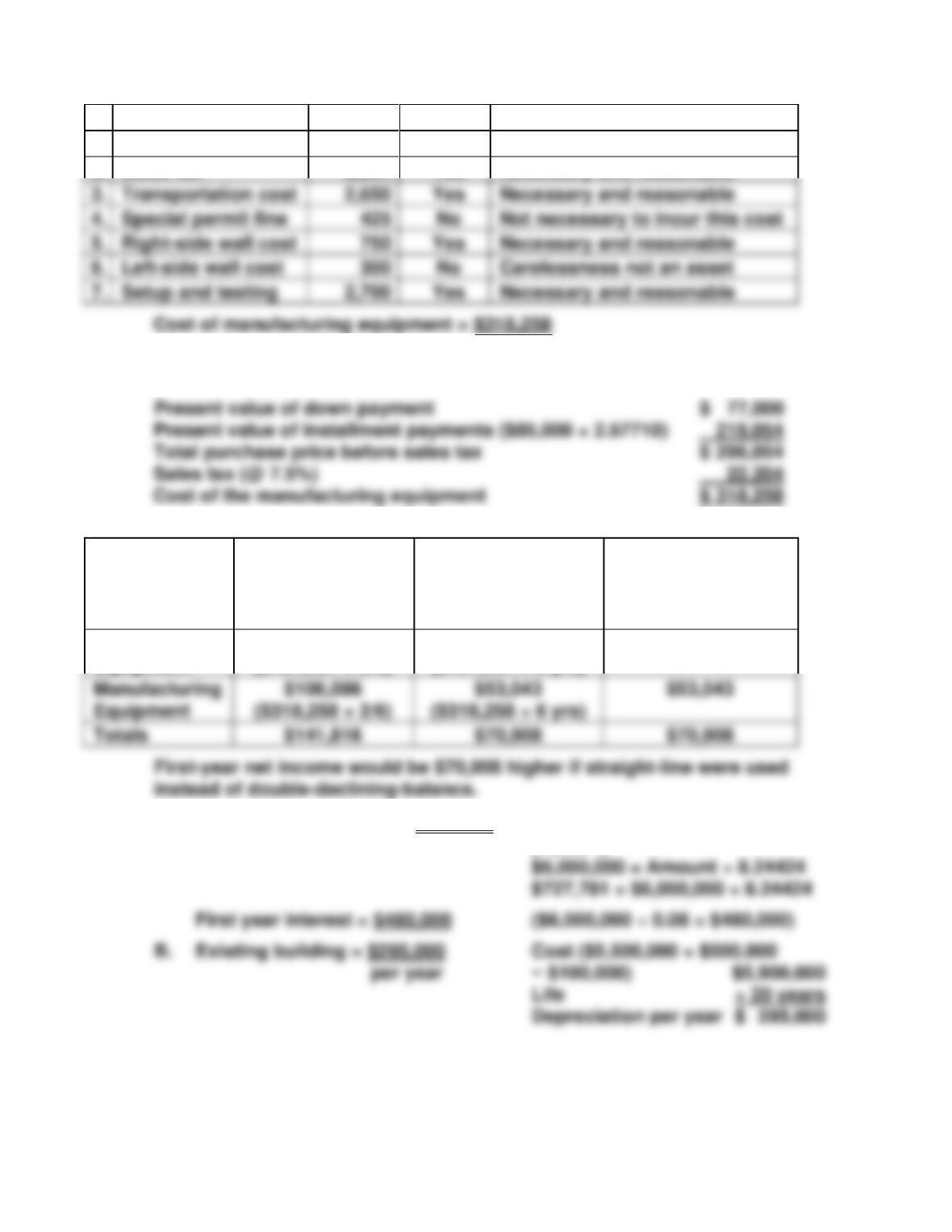

P11-3 A. Cost of diagnostic equipment = $107,191

322 Chapter 11

Item

Amount

Include?

Reason

1.

Invoice cost

$93,000

Yes

Necessary and reasonable

2.

Sales tax

8,091

Yes

Necessary and reasonable

The cost of the equipment is the present value of the cash flows neces-

sary to acquire it.

B.

Asset

DDB Depreciation

for the

First Year

SL Depreciation

for the

First Year

Difference in First-

Year Depreciation

Expense and Net

Income

Diagnostic

Equipment

$35,730

($107,191 × 2/6)

$17,865

($107,191 ÷ 6 yrs)

$17,865

Manufacturing

$53,043

$53,043

Totals

P11-4 A. Equal annual payment = $727,781 PV of an annuity = Amount × IF

(Table 4)

3.

Transportation cost

2,650

Yes

Necessary and reasonable

4.

Special permit fine

Not necessary to incur this cost

5.

Right-side wall cost

Yes

Necessary and reasonable

6.

Left-side wall cost

Carelessness not an asset

7.

Setup and testing

2,700

Yes

Necessary and reasonable