Investing Activities 323

New building = $229,600 per year

For the new building, the total cost must be determined. It is the

sum of the costs given in the problem plus interest on the one-

C. If the firm purchases the existing building and land, there would be

an outflow in the investing section for the cost of the building and

D. The difference that the controller wishes to recognize as a Gain on

P11-5 A.

Straight-Line Depreciation

Year

Beginning

Book Value

Depreciation

Expense

Accumulated

Depreciation

Ending

Book Value

1

$124,000

$ 24,000*

$ 24,000

$100,000

2

76,000

3

52,000

4

28,000

5

324 Chapter 11

Double-Declining-Balance Depreciation

Year

Beginning

Book Value

(BBV)

Depreciation

Expense

(BBV × 0.4)

Accumulated

Depreciation

Ending

Book Value

1

$124,000

$ 49,600

$ 49,600

$74,400

B.

Units-of-Production Depreciation

Year

Beginning

Book Value

Depreciation

Expense*

Accumulated

Depreciation

Ending

Book Value

1

$124,000

$ 24,000

$ 24,000

$100,000

2

76,000

3

52,000

4

28,000

5

Total

$120,000

C. Using the answers from parts A and B, the book value at the time of

the sale must be calculated for each depreciation method. For the

straight-line and double-declining-balance methods, one-half of the

2

44,640

3

26,784

4

16,070

5

Total

$120,000

Investing Activities 325

Straight-

Line

Double-

Declining-

Balance

Units-of–

Production

Original cost

$124,000

$124,000

$124,000

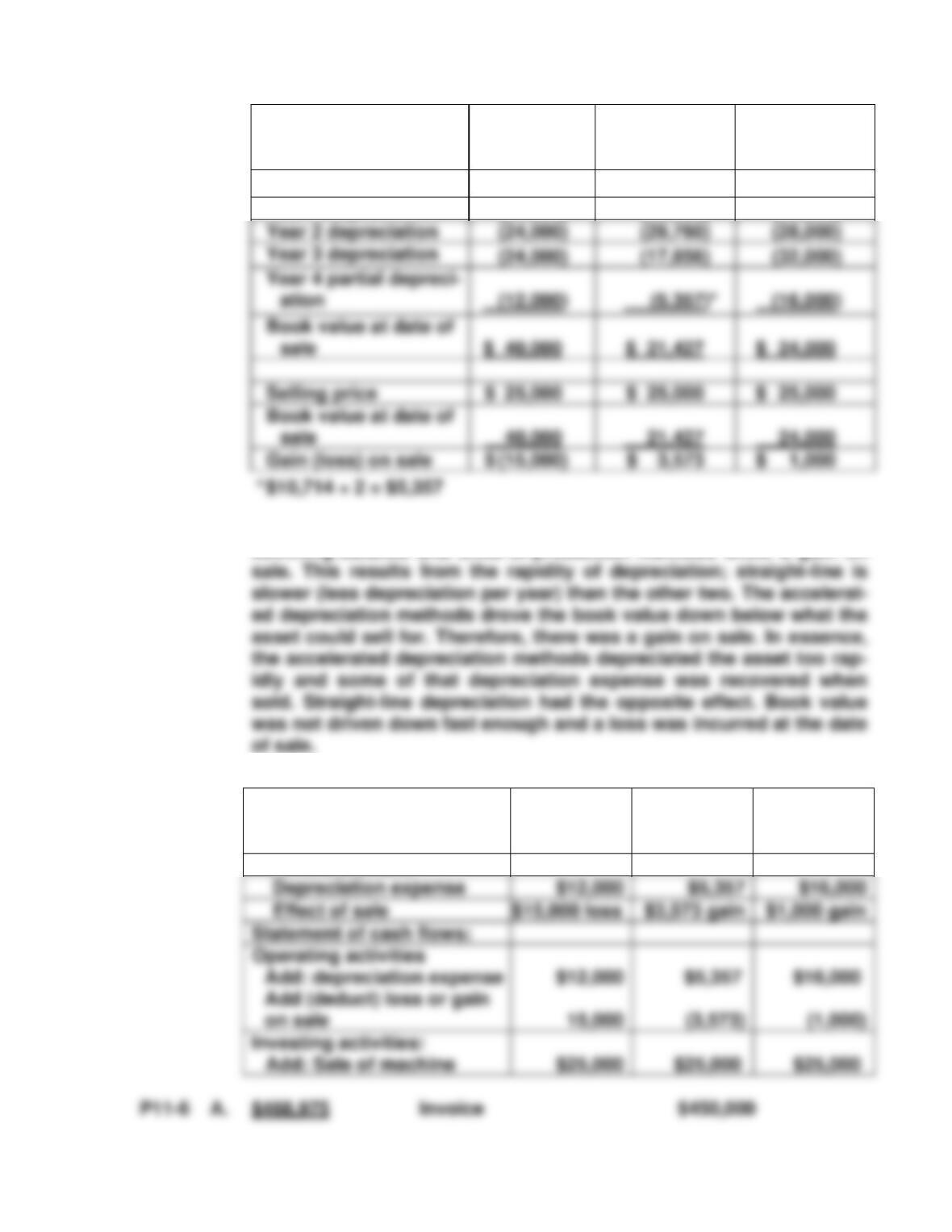

Year 1 depreciation

(24,000)

(49,600)

(24,000)

The straight-line method yields a loss on sale, while the double-

declining-balance and units-of-production methods show a gain on

D.

Straight-

line

Double-

Declining-

Balance

Units-of–

Production

Income statement:

Statement of cash flows:

Year 2 depreciation

(24,000)

(29,760)

(28,000)

(24,000)

(17,856)

(32,000)

$ 40,000

$ 21,427

$ 24,000

Selling price

$ 25,000

$ 25,000

$ 25,000

40,000

21,427

24,000

Gain (loss) on sale

$ (15,000)

$ 3,573

$ 1,000

326 Chapter 11

B.

Straight-Line Method

Double-Declining-Balance

Method

Year

Depreciation

Expense

End-of-Year

Book Value

Depreciation

Expense

End-of-Year

Book Value

0

468,975

468,975

1

397,479

156,325

312,650

2

325,983

104,217

208,433

3

138,955

4

182,991

5

111,495

6

C.

Income statements:

Straight-line depreciation

All years are

the same

Income before depreciation and taxes

Depreciation

Income before taxes

Income taxes (35%)

Net income

D.

Income statements:

Double-declining-

balance

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Income before

depreciation and taxes

$160,000

$160,000

$160,000

$160,000

$160,000

$160,000

Depreciation

Income before taxes

3,675

Income taxes (35%)

1,286

Net income

2,389

E. A very different pattern of net income is reported over the six years

depending on which depreciation method is used. Because double–

Investing Activities 327

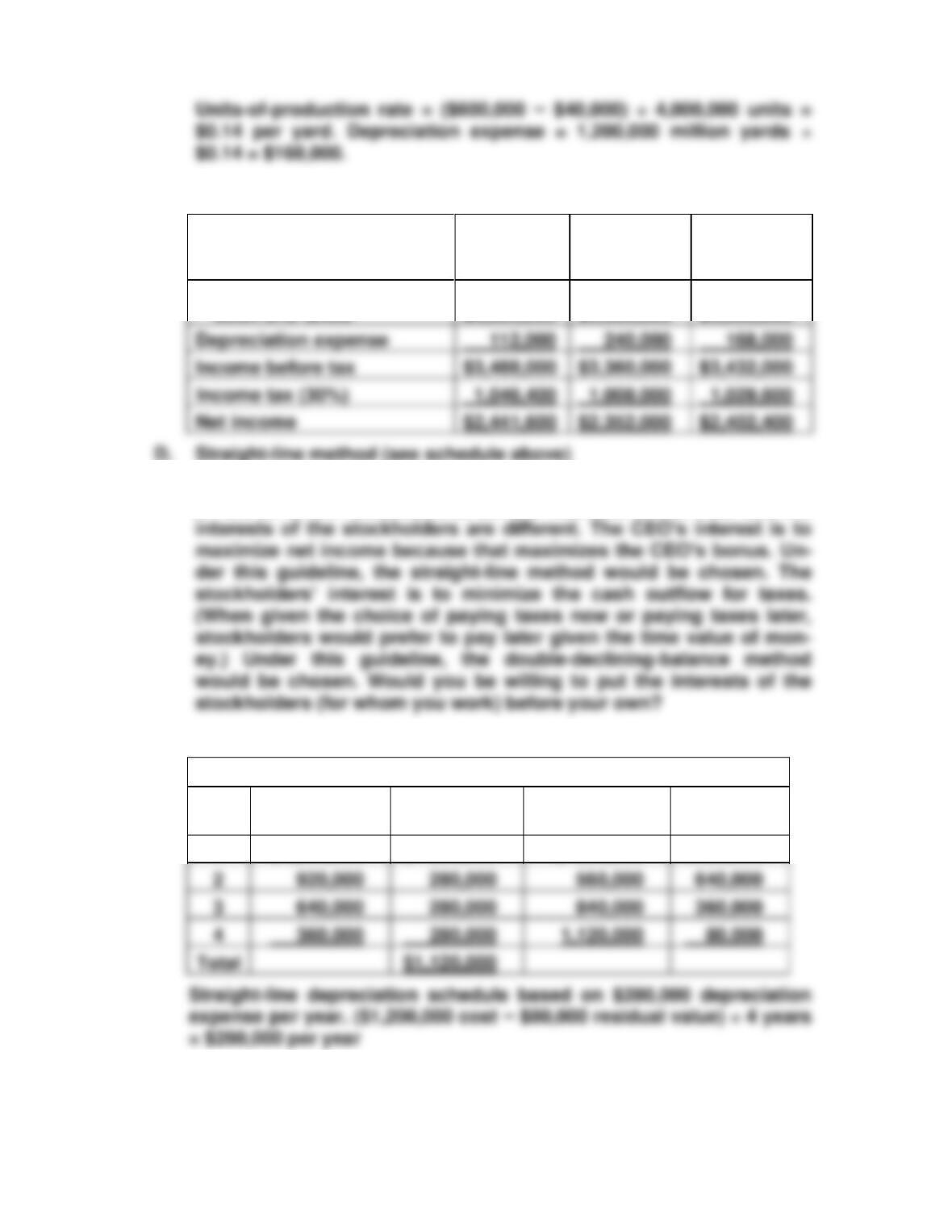

P11-7 A.

Straight-Line Depreciation

Year

Beginning

Book Value

Depreciation

Expense

Accumulated

Depreciation

Ending

Book Value

1

$600,000

$112,000

$112,000

488,000

2

376,000

3

264,000

4

152,000

5

Total

$560,000

Double-Declining-Balance Depreciation

Year

Beginning

Book Value

Depreciation

Expense

Accumulated

Depreciation

Ending

Book Value

1

$600,000

$240,000

$240,000

$360,000

2

3

4

77,760

5

Total

$560,000

The double-declining-balance depreciation schedule is based on

these computations:

($600,000 × 2/5 = $240,000)

328 Chapter 11

C. Double-declining-balance method

Straight-

Line

Double-

Declining-

Balance

Units-of–

Production

Net income before depreci-

ation and taxes

$3,600,000

$3,600,000

$3,600,000

Depreciation expense

Income before tax

$3,488,000

$3,360,000

$3,432,000

Income tax (30%)

Net income

$2,441,600

$2,352,000

$2,402,400

D. Straight-line method (see schedule above)

E. This is an example of moral hazard. The CEO must make a decision

on behalf of the stockholders, but the interests of the CEO and the

P11-8 A.

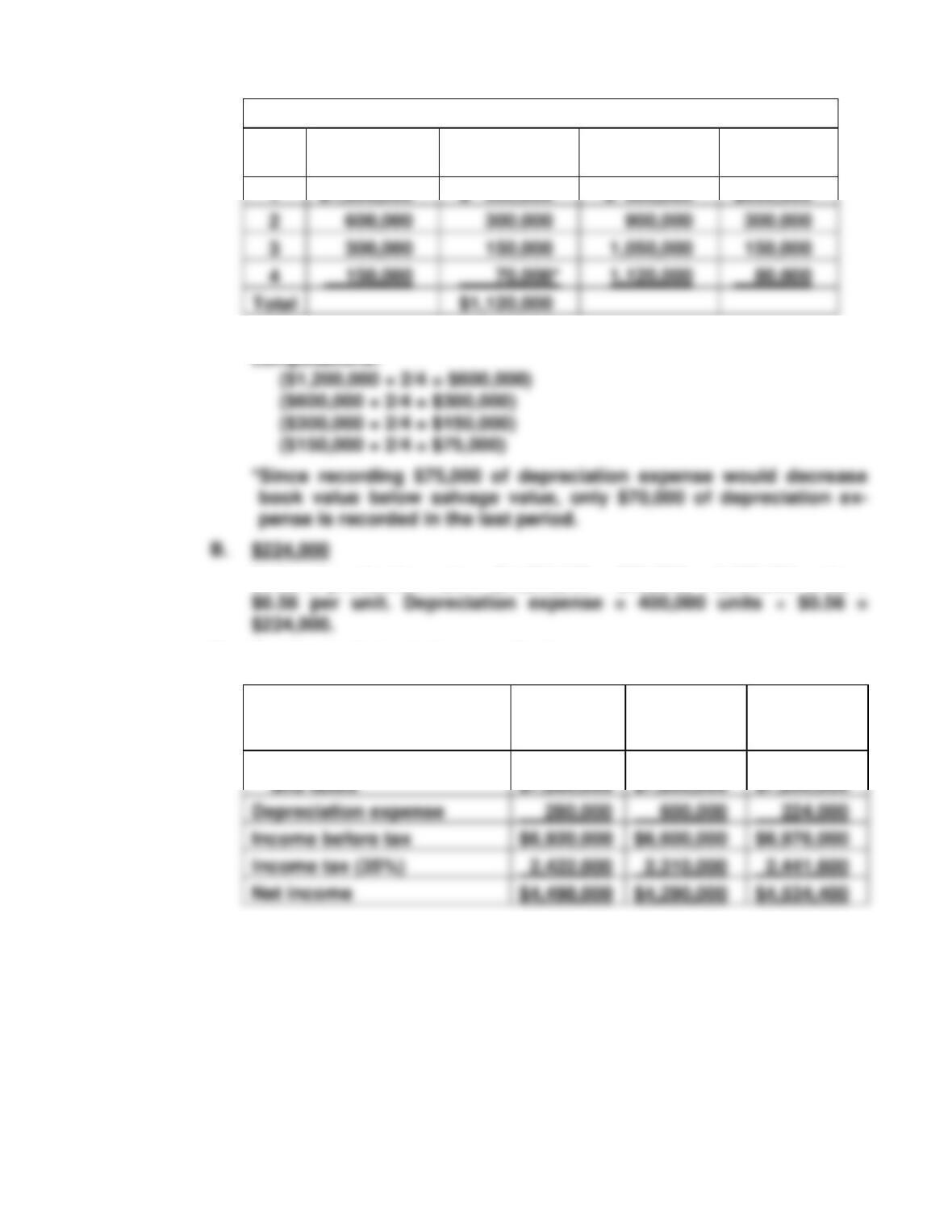

Straight-Line Depreciation

Year

Beginning

Book Value

Depreciation

Expense

Accumulated

Depreciation

Ending

Book Value

1

$1,200,000

$ 280,000

$ 280,000

$920,000

2

3

4

Total

Investing Activities 329

Double-Declining-Balance Depreciation

Year

Beginning

Book Value

Depreciation

Expense

Accumulated

Depreciation

Ending

Book Value

$1,200,000

$ 600,000

$ 600,000

$600,000

Double-declining-balance depreciation schedule is based on these

Units-of-production rate = ($1,200,000 – $80,000) ÷ 2,000,000 units =

C. Double-declining-balance method

Straight-

Line

Double-

Declining-

Balance

Units-of–

Production

$7,200,000

Depreciation expense

Income before tax

$6,920,000

$6,600,000

$6,976,000

Income tax (35%)

Income before depreciation

D. Units-of-production method (see part C solution)

Total

330 Chapter 11

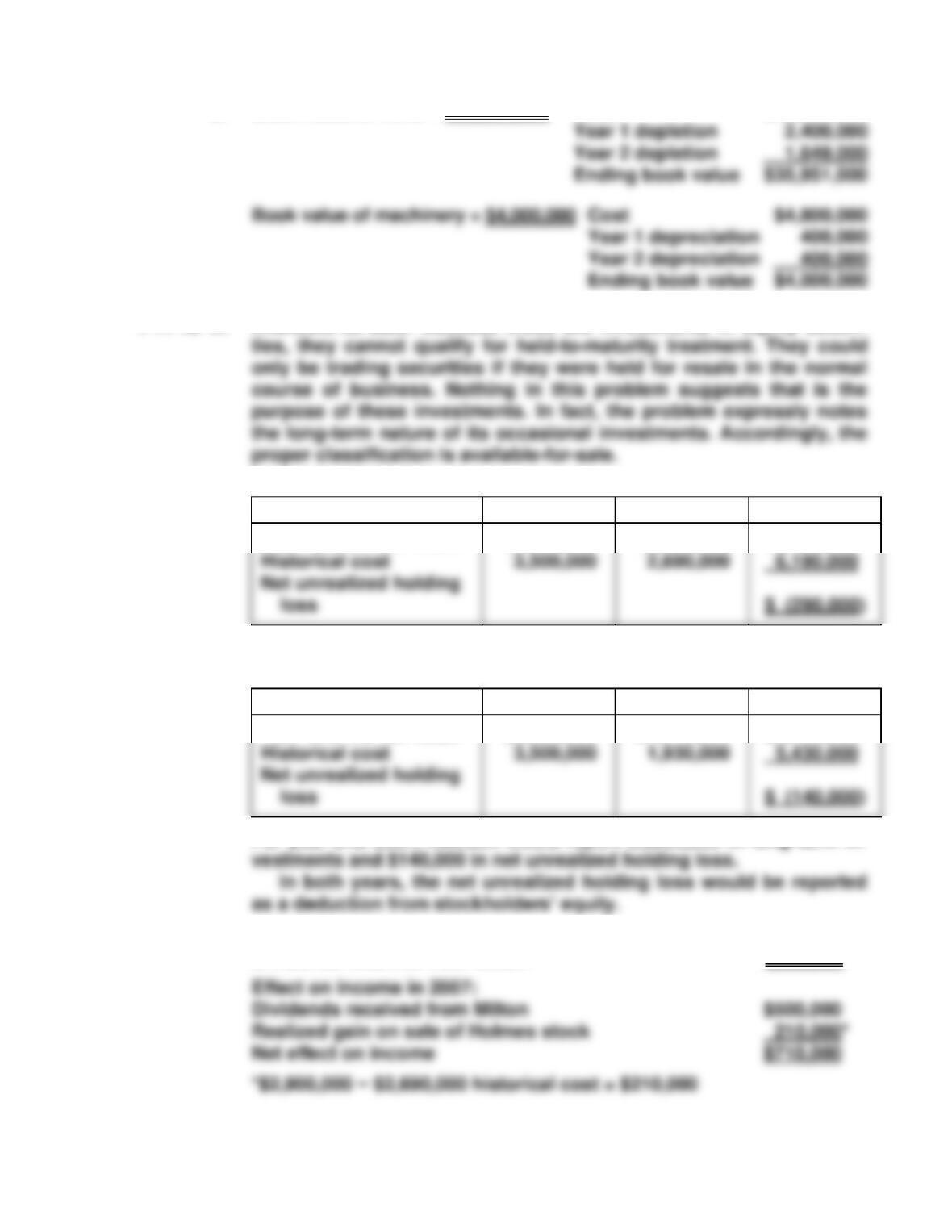

P11-9 A. First year depletion = $2,400,000 Cost of mine $40,000,000

*Student responses will vary. One reasonable approach is as

follows. If the machinery can be used only for this mine, it is

reasonable to base depreciation on the output of the mine;

that is, use units-of-production depreciation, rather than

Part A Part B

Revenue ($120 × 30,000 tons) $3,600,000 $3,600,000

D. Second year depletion = $1,649,000

Cost of mine $ 40,000,000

First year depletion 2,400,000

Investing Activities 331

E. Book value of mine = $35,951,000 Cost $40,000,000

P11-10 A. Available-for-sale: Because these are investments in equity securi-

B.

2006

Milton

Holmes

Total

Year-end market value

$3,100,000

$2,800,000

$5,900,000

For year-end 2006, Keelson would report $5,900,000 in long-term in-

vestments and $290,000 in net unrealized holding loss.

2007

Milton

Balthasar

Total

Year-end market value

$3,350,000

$1,940,000

$5,290,000

For year-end 2007, Keelson would report $5,290,000 in long-term in-

C. Effect on income in 2006:

Dividends received from Milton $500,000

332 Chapter 11

P11-11 A. 1. Short-term investments (at market value):

2. Long-term investments (at market value):

3. Stockholders’ equity:

Net unrealized holding gain $2,210

Proof:

Market

Cost

Gain (Loss)

Harbor

$41,000

$37,500

$ 3,500

Regency

Hilton

Paxton

(1,210)

Net unrealized holding gain

C. Companies hold assets because of the future economic benefits that

can be derived from them. In the case of buildings and equipment,

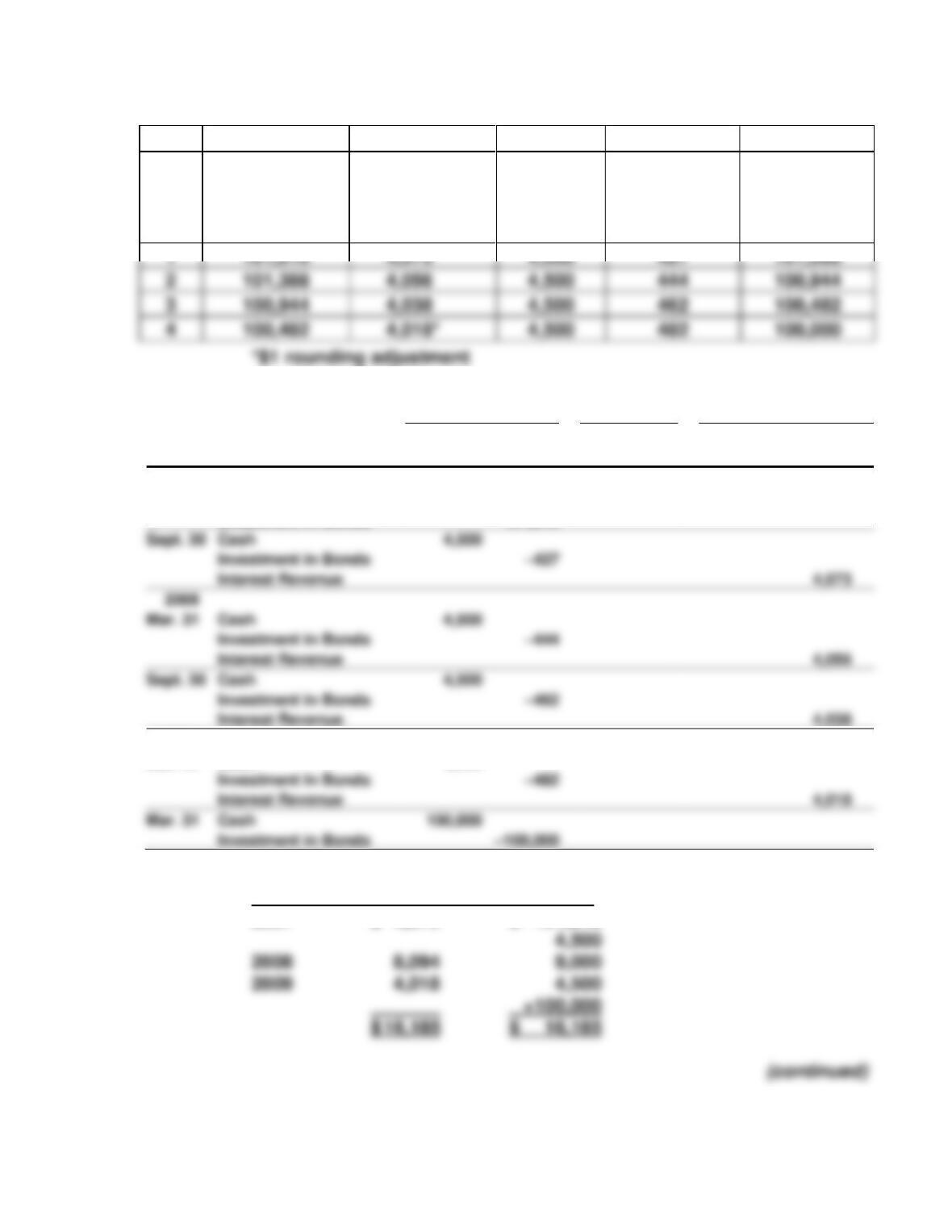

P11-12 A. $101,815. The price of the bonds would be computed as the present

Investing Activities 333

B.

1

2

3

4

5

6

Period

Present Value

at Beginning

of Period

Interest

Revenue

(Column 2 ×

4%)

Cash

Interest

Received

Amort. of

Premium

(Column 4 −

Column 3)

Value at End

of Period

C.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

2007

Apr. 1

Cash

−101,815

Investment in Bonds

101,815

Sept. 30

Cash

4,500

Investment in Bonds

Interest Revenue

2008

Mar. 31

Cash

4,500

Investment in Bonds

Interest Revenue

Sept. 30

Cash

4,500

Investment in Bonds

Interest Revenue

2009

Mar. 31

Cash

4,500

Investment in Bonds

Interest Revenue

Mar. 31

Cash

100,000

Investment in Bonds

D. Interest Cash

Year Revenue Flows

2007 $ 4,073 $ −101,815

1

2

3

4

334 Chapter 11

E. When considering a completed transformation cycle, accrual basis

P11-13

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Part

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

A

Cash

–10,000

Long-Term Investments

10,000

B

Cash

500

Interest Revenue

C

No entry necessary

D

Long-Term Investments

E

Cash

–10,445

Long-Term Investments

10,445

Cash

500

Interest Revenue

G

No entry necessary

H

Long-Term Investments

37

Unrealized Holding Gain2*

37*

1 A portion of the premium must be amortized. Cash interest received equals $500

Investing Activities 335

I. The carrying values to be reported on the balance sheet at the end of

year one in parts C, D, G, and H would be:

Part

Original

Cost

Amortization

of Premium

Market Value

Adjustment

Carrying Value

(Book Value) at

End of Year 1

H

10,445

− $82

+ $37

10,400

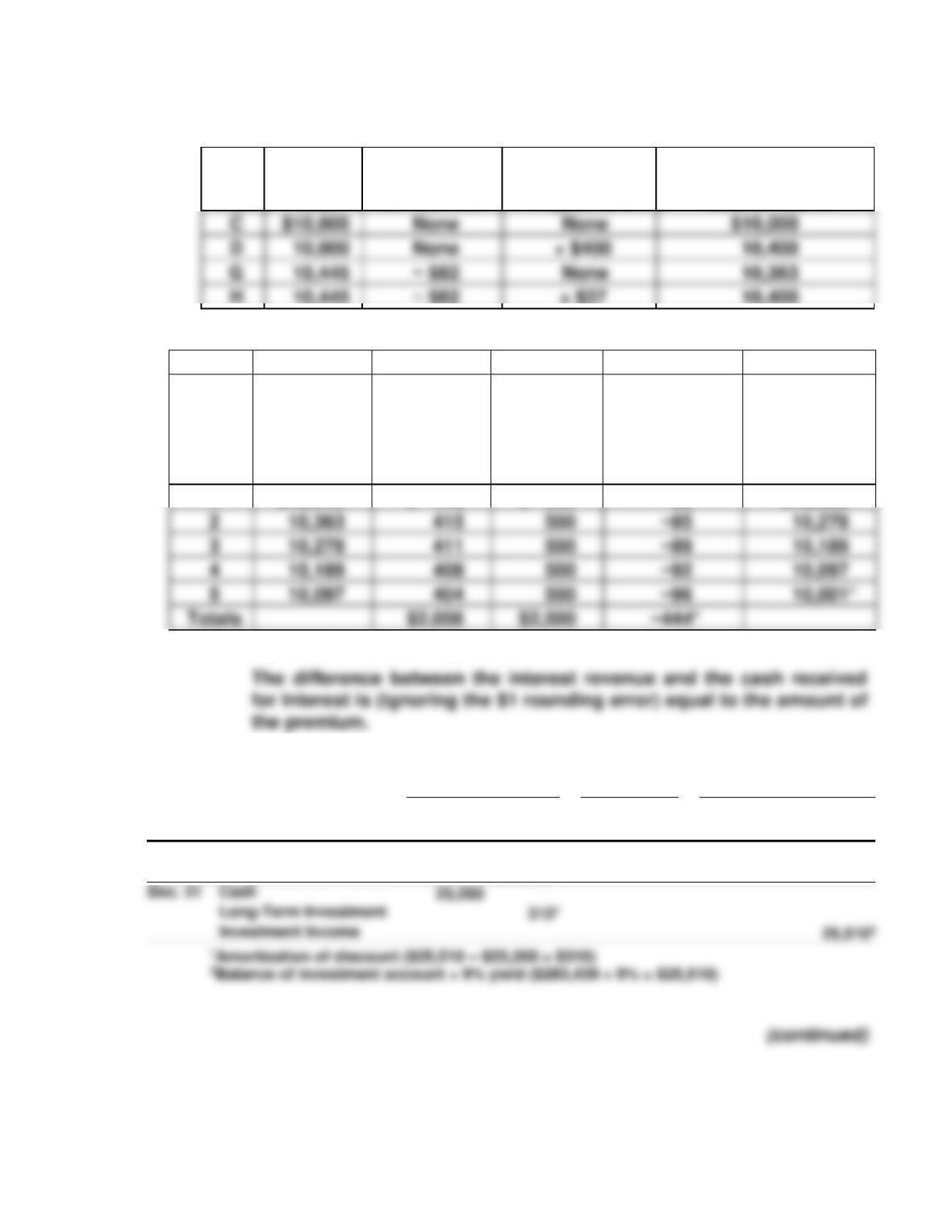

J. Amortization table

1

2

3

4

5

6

Year

Present

Value at

Beginning

of Year

Interest

Revenue

(Column 2

× Interest

Rate)

Cash

Received

Amortization

of Premium

(Column 3 −

Column 4)

Value at

End of Year

(Column 2 −

Column 5)

1

$10,445

$ 418

$ 500

−82

$10,363

2

10,363

−85

4

10,189

−92

$2,056

$2,500

*Ignore the $1 rounding error.

P11-14 A.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Jan. 1

Cash

–283,439

Long-Term Investment

283,439

Long-Term Investment

Investment Income

C

D

10,000

G

10,445

− $82

10,363

336 Chapter 11

B.

If the bonds are?

Held-to–

Maturity

Securities

Trading

Securities

Available-

for-Sale

Securities

Accounting method to be used

Amortized

cost

Mark to

market

Mark to

market

Amount of unrealized holding gain (loss) to

be reported on income statement

none

$(1,749)3

none

P11-15 A.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Aug. 22

Cash

–160,800

160,800*

Amount of unrealized holding gain (loss) to

be reported on balance sheet

none

none

Balance of investment account on balance

sheet at end of first year

Investing Activities 337

B.

If the total number of Radius common

shares outstanding totals

1 million1

80,0002

30,0003

Accounting method to be used

Mark to

market

Equity method

Consolidation

method

Amount of unrealized holding gain

1 A small investment (2% of outstanding shares) that does not create sig-

nificant influence or control.

C.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Jan. 23

Cash

171,400

Realized Holding Gain

P11-16 A.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

1.

Mining Site

−660,000

Cost of Goods Sold

statement

Amount of unrealized holding gain

sheet

balance sheet

determinable