Analysis of Financing Activities 285

P10-5 A. and B Pro Forma Income Statements

Equity Debt

Financing Financing

Sales revenue $ 429,600 $429,600

C.

Net income

Stockholders’

equity

Return on

equity

Actual 2007 results

$33,600

$102,000

32.94%

Pro-forma 2008

(equity financing)

$49,320

14.04%

Pro-forma 2008

(debt financing)

$42,120

29.23%

Financing the acquisition of new equipment with equity has the ef-

fect of cutting 2008’s return on equity by more than one-half (from

32.94% to 14.04%). Even financing with debt, however, will dilute the

return on equity somewhat (from 32.94% to 29.23%). Of the two op-

tions, debt financing is clearly the better choice if management

286 Chapter 10

P10-6 A. The following ratio values might be helpful in identifying the firm’s

capital structure.

Ratio

Computation

2004

2003

Long-term debt to total assets

a ÷ c

0.17

0.17

B.

Current Ratio

2004

2003

P10-7 A. Return on equity = net income ÷ stockholders’ equity

2004 = 52.2% ($4,504 ÷ $8,633)

b ÷ c

0.40

0.49

a ÷ d

0.29

0.34

0.67

0.94

Analysis of Financing Activities 287

P10-8 Primary alternatives for raising additional capital include long-term debt,

preferred stock, and common stock. Risk issues that should be consid-

ered include the risk of default and bankruptcy and the risk of loss of

control. Return issues include the cost of debt, payment of preferred div-

idends, and dilution of earnings available for common stockholders.

Also, preferred stock normally does not have voting rights. Therefore,

current owners could retain control of the company. Dividends paid on

preferred stock reduce the earnings and cash flows available for common

stockholders. But preferred stockholders do not necessarily participate in

earnings to the same extent as common stockholders. Therefore, the fam-

288 Chapter 10

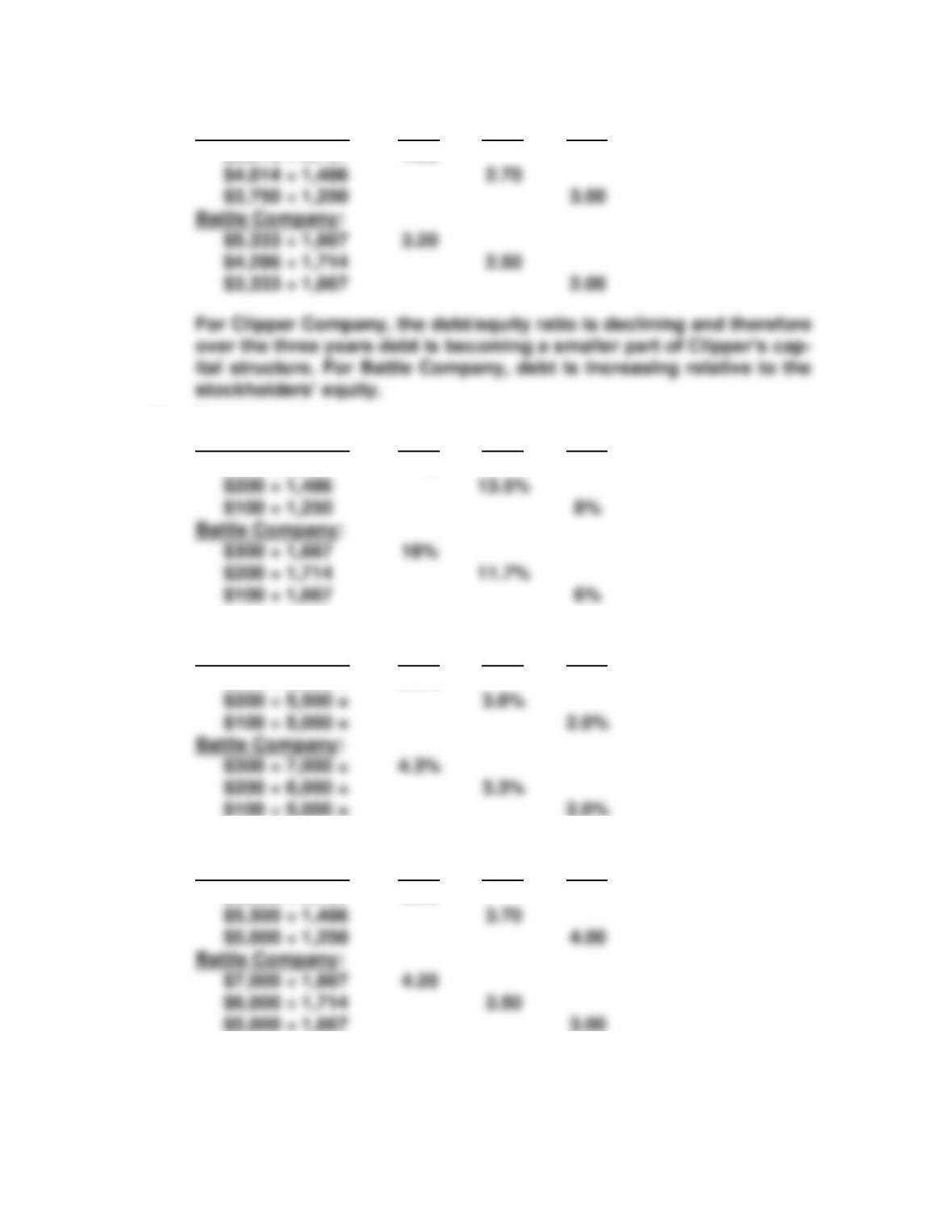

P10-9 A. Debt to Equity

Clipper Company: 2008 2007 2006

$3,273 ÷ 2,727 1.20

B. Return on Equity:

Clipper Company: 2008 2007 2006

$300 ÷ 2,727 11%

Return on Assets:

Clipper Company: 2008 2007 2006

$300 ÷ 6,000 = 5.0%

Financial Leverage:

Clipper Company: 2008 2007 2006

$6,000 ÷ 2,727 2.20

Clipper Company had a greater increase in ROA over the three years

than did Battle Company. However, Battle Company has had an

increase in financial leverage over the years, while Clipper Company

Analysis of Financing Activities 289

C. Dividend Payout Ratio:

Clipper Company: 2008 2007 2006

$75 ÷ 300 25%

D. Students may point out that each company has had the same income

each year so that the investment decision might be based solely on

the dividends paid out. Some investors may prefer a higher dividend

distribution, while others may prefer investing in companies that re-

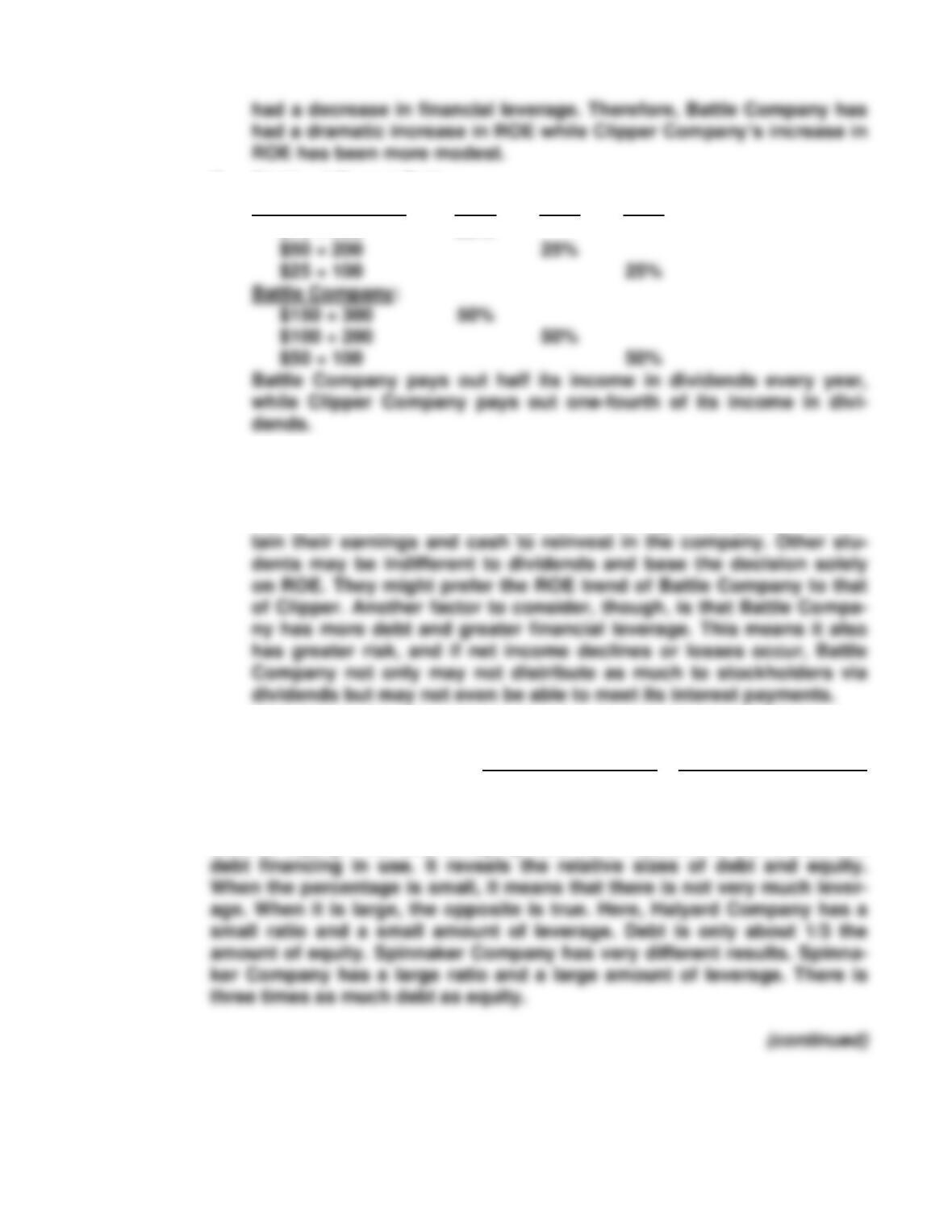

P10-10 A.

Halyard Company

Spinnaker Company

i. Debt-to-equity ratio

33.3%

300.0%

ii. Debt-to–assets ratio

25.0%

75.0%

Debt to equity: The debt-to-equity ratio is a measure of the amount of

290 Chapter 10

Debt to assets: The debt-to-assets ratio also measures the amount of

debt financing in use. It reveals the portion of assets that are financed by

B.

Halyard Company

Spinnaker Company

Bad

Year

Normal

Year

Good

Year

Bad

Year

Normal

Year

Good

Year

i. Return on assets

(3.13)

9.38

21.88

(3.13)

9.38

21.88

ii. Financial leverage

1.33

1.33

4.00

4.00

4.00

iii. Return on equity

(4.17)

12.50

29.17

37.50

87.50

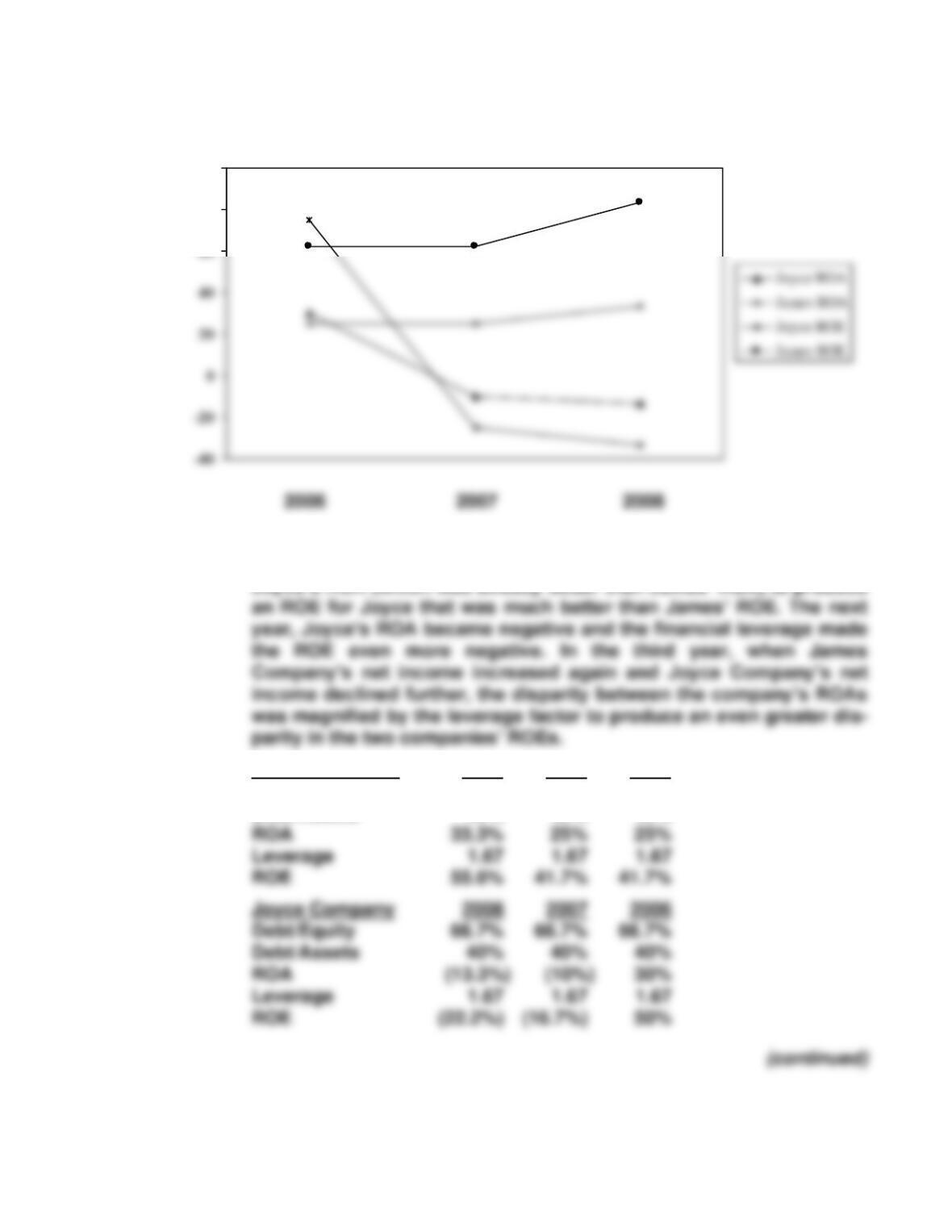

P10-11 A. James Company 2008 2007 2006

Debt/Equity 150% 150% 150%

Debt/Assets 60% 60% 60%

Analysis of Financing Activities 291

B.

In the year 2006, when Joyce Company had a higher net income than

James Company, the existence of financial leverage magnified

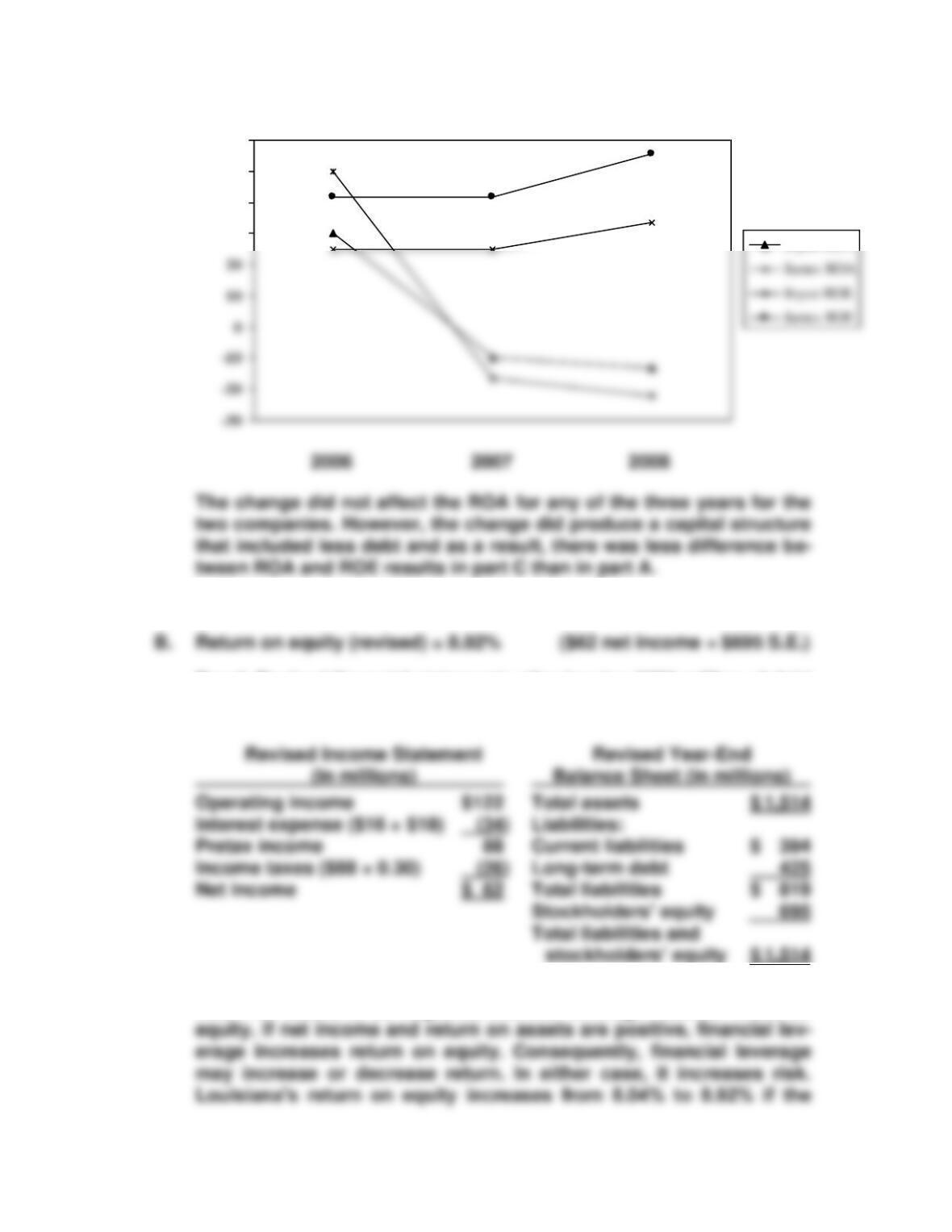

C. James Company 2008 2007 2006

Debt/Equity 66.7% 66.7% 66.7%

Debt/Assets 40% 40% 40%

80

100

292 Chapter 10

P10-12 A. Return on equity (as reported) = 8.04% ($74 net income ÷ $920 S.E.)

Proof: Revised financial statements after issuing $225 million of debt

and repurchasing $225 million of stock would be as follows.

C. Higher financial leverage increases risk. If a net loss occurs, causing

return on assets to be negative, financial leverage reduces return on

30

40

50

60

Joyce ROA

Analysis of Financing Activities 293

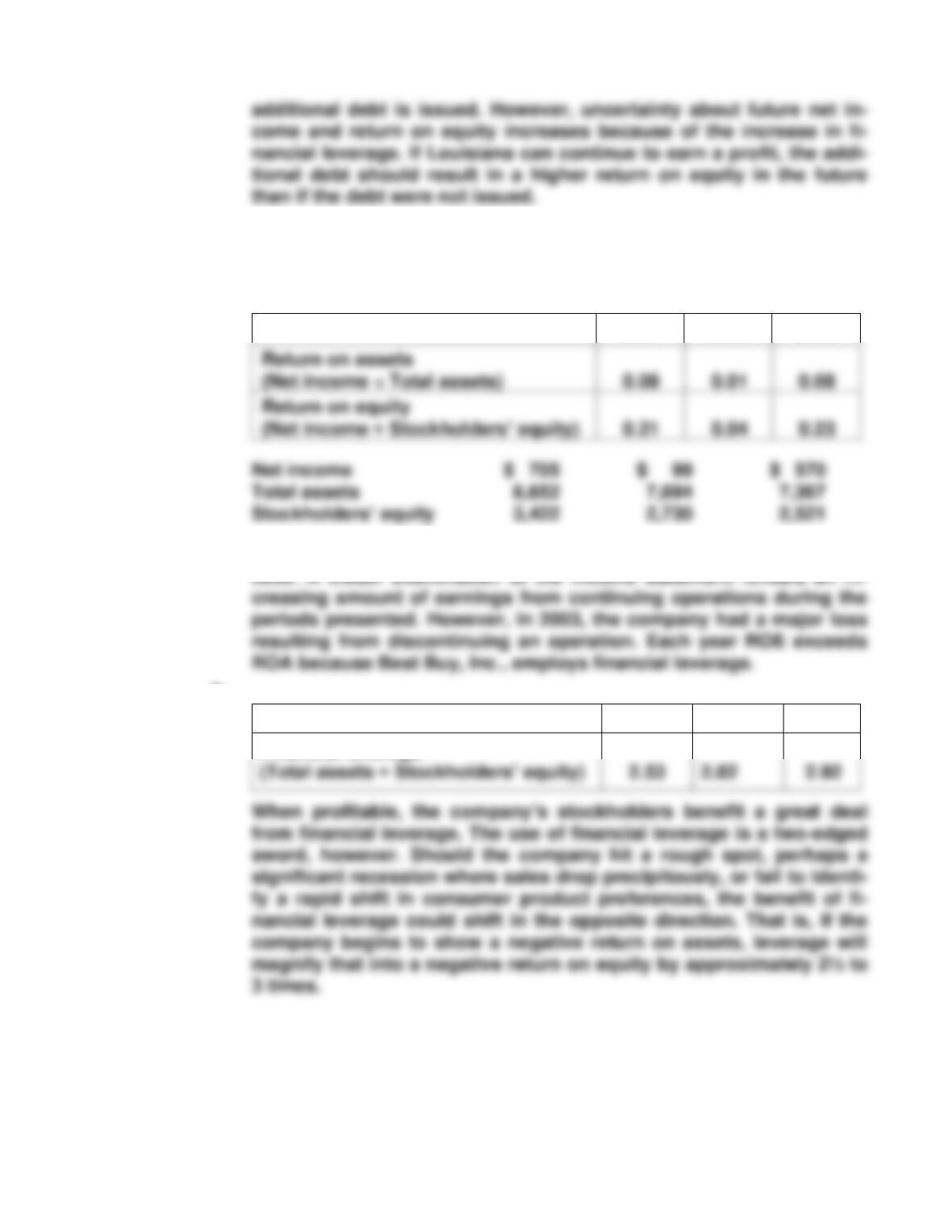

P10-13 A. An analysis of profit performance would include computation of the

return on assets and return on equity for the periods under consid-

eration.

2004

2003

2002

The company experienced a significant dip in ROA and ROE during

B.

2004

2003

2002

Financial leverage

294 Chapter 10

P10-14 Johnson & Johnson does not appear to be facing financial problems. It

has used cash to pay dividends, repurchase stock, and pay off both long–

Increased Decreased

Financial Financial

Financing activity Leverage Leverage

Payment of dividend ($2,746 + $3,251) $ 5,997

P10-15 M E M O R A N D U M

DATE: (today’s date)

TO: Wellington Smythe

FROM: (student’s name)

SUBJECT: Credit worthiness of Sunny Meadow Enterprises

I am responding to your concerns about the recent net loss of Sunny

Meadow Enterprises and the implications of the loss for the company’s

ability to make its principal and interest payments. While not favorable,

Analysis of Financing Activities 295

Also worrisome is the current portion of long-term debt that comes

due in this next year. While last year’s cash flow from operations of

$144.2 million was more than sufficient to meet last year’s then-current

portion of long-term debt of $31.6 million, this is not the case now. If next

year’s cash flow from operations is about the same as this year (i.e., $6.8

P10-16 A. A leveraged buyout involves the massive issuance of debt and use

of the proceeds to buy back the outstanding common stock of the

owns.

B. Whenever bonds are issued with a nominal rate less than the market

C. When a company increases its debt and decreases its equity, it be-

D. The reversal of net income to net loss is not encouraging. Still, the

immediate issue is whether the company can make the interest pay-

296 Chapter 10

P10-17 A. Financing Cash Flows:

During the three-year period, the company issued debt, paid off debt,

B. Dividend Policy:

Inspection of the cash flow statement (financing activities section)

C. Company value:

Year 2004 2003

Highpoints:*

P10-18 There are at least two unethical activities in this case. First, the company

is intentionally hiding debt from interested parties. The only reason the

partnerships are established is to make Endrun’s financial statements

Analysis of Financing Activities 297

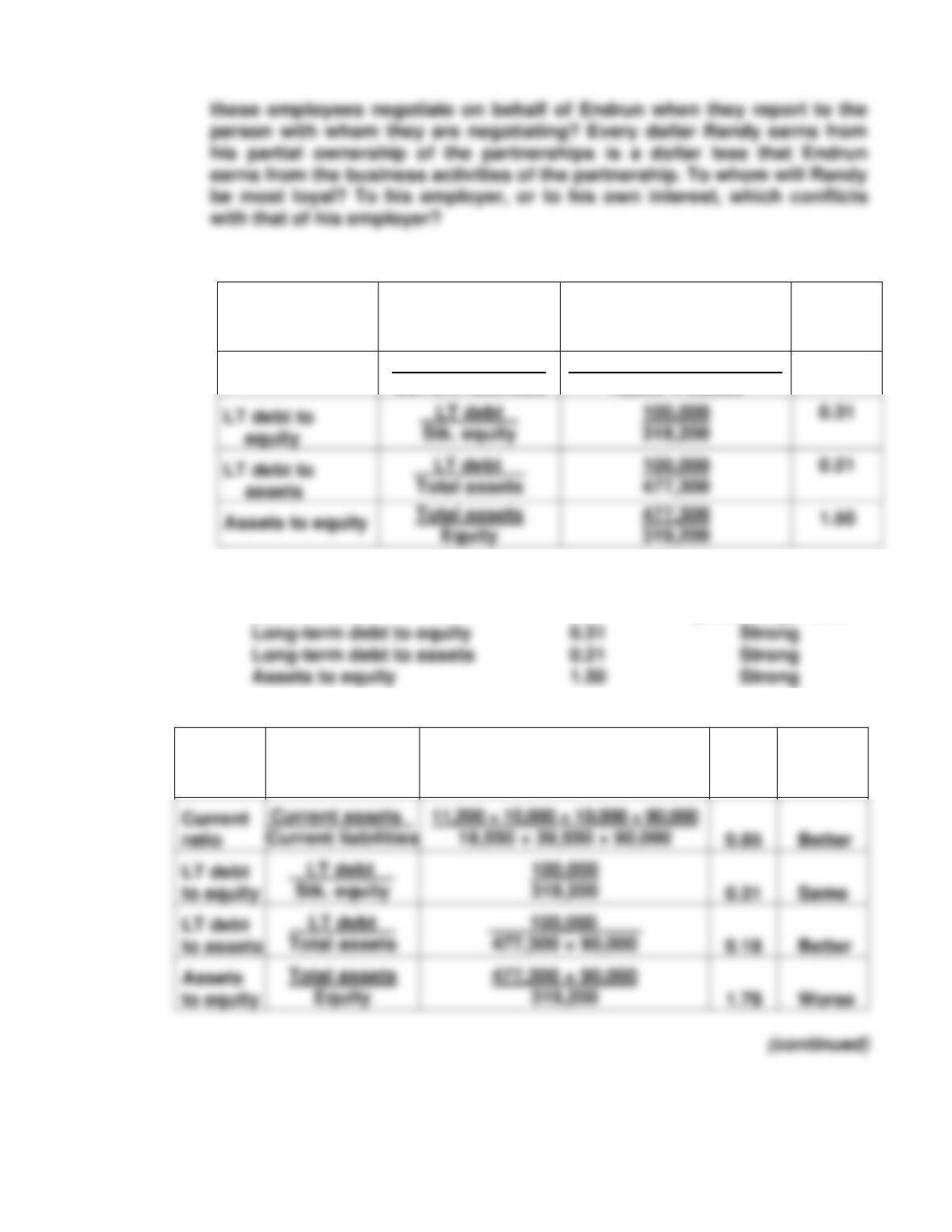

P10-19 A.

Ratio

Formula

Computation

Today’s

Ratio

Value

Current ratio

Current assets

Current liabilities

11,200 + 15,000 + 10,000

18,550 + 39,550

0.62

B. Comparison to

Ratio Today’s Value Industry Benchmarks

Current ratio 0.62 (incredibly) Weak

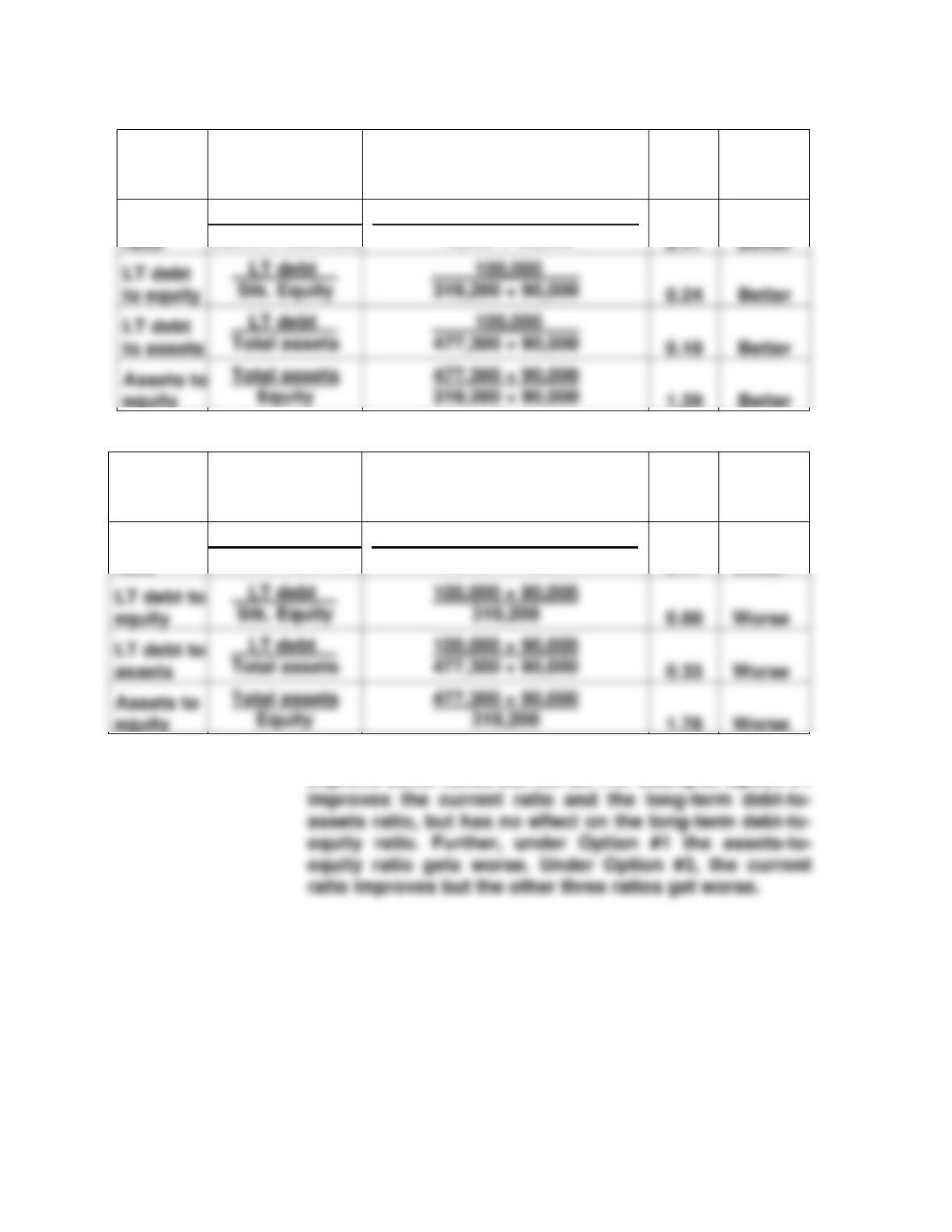

C. Option #1: Obtain short-term bank loan

Ratio

Formula

Computation

New

Ratio

Change

From

Today

298 Chapter 10

Option #2: Sell new shares of common stock

Ratio

Formula

Computation

New

Ratio

Change

From

Today

Current

Current assets

Current liabilities

11,200 + 15,000 + 10,000 + 90,000

18,550 + 39,550

Option #3: Issue long-term bonds payable

Ratio

Formula

Computation

New

Ratio

Change

From

Today

Current

ratio

Current assets

Current liabilities

11,200 + 15,000 + 10,000 + 90,000

18,550 + 39,550

2.17

Better

LT debt to

0.60

Worse

LT debt to

0.33

Worse

Assets to

1.78

Worse

D. Option #2 Only Option #2 improves all four ratios. The other ratios

improve some ratios but not all. For example, Option #1

ratio

2.17

LT debt

0.24

LT debt

0.18

Assets to

1.39

Analysis of Financing Activities 299

P10-20

High Income

Low Income

Current

Less Debt

More Debt

Current

Less Debt

More Debt

Operating income

$ 647,585

$ 647,585

$ 647,585

$ 200,000

$ 200,000

$ 200,000

Interest expense

Pretax income

Income taxes

Net income

Return on assets

5.30%

6.34%

4.26%

0.13%

1.17%

−0.91%

Financial leverage

Return on equity

8.85%

8.16%

1.51%

−2.16%

Note: Students may observe slight rounding errors between their solutions and the solutions

presented here. Rounding errors typically occur because of the number of significant digits

Excel uses in its calculations.

P10-21

1

2

3

4

5

6

7

8

9

10

Effect of Financial Leverage on Return

0.08

0.10

0.12

Total assets

5,623,107

5,623,107

5,623,107

5,623,107

3,097,416

2,097,416

1,097,416

3,097,416

4,370,241

300 Chapter 10

CASES

C10–1 At the end of 2007, Terabyte Technology’s capital structure consisted of

48.7% equity ($4,257 ÷ $8,742) and 51.3% debt. Long-term debt accounted

for 9.1% ($792 ÷ $8,742) of the capital structure. At the end of 2008, the

capital structure consisted of 49.4% ($4,630 ÷ $9,375) equity and 50.6%

nancial problems.

C10-2 Summary of actual results and projected results of the events noted in

the case (dollar amounts in millions)

Actual

Results

Event A

Event B

Event C

Net

income

$3

$3.45

$2

$3.8

equity*

*Assumes preferred stock is part of equity

A. The substitution of common stock for existing bonds would have

Analysis of Financing Activities 301

Current liabilities $ 2,400,000 no change

Long-term debt (9% bonds) 0 all bonds repurchased

B. The reduction of net income by $1 million would leave it at $2 million.

Capital structure would be changed only by the amount of net in-

come. At year-end 2007, therefore, the capital structure of the firm

would be as follows:

Current liabilities $ 2,400,000 no change

C. The purchase of $8 million of new assets would increase net income

by $1.6 million before allowing for $800,000 of additional interest ($8

302 Chapter 10

At year-end 2007, total assets would also equal $34,800,000. There-

fore, the return on assets decreases from 11.5% to 10.9% because

fault.

C10-3 Students will have their own ideas and their own way of weighing the var-

ious considerations. Here is a brief outline of factors that students may

consider:

I. Factors in the decision to lend money to Sporty Footware, Inc.

a. Debt is a small part of the company’s capital structure and there-

II. Factors in the decision to invest in the stock of Sporty Footware, Inc.

a. According to the cash flow statement, cash from operations has

increased each of the three years presented here, indicating suc-

cess.