CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN)

EVALUATING DECENTRALIZED OPERATIONS

DISCUSSION QUESTIONS

1. In a centralized operation, all major planning and operating decisions are made by top management.

In a decentralized operation, managers of separate divisions or units are delegated operating

responsibility. The division (unit) managers are responsible for planning and controlling the

operations of their divisions. Divisions are often structured around products, customers, or regions.

5. A division of a decentralized company could be considered the least profitable, even though it

earned the largest amount of operating income, when its return on investment is the lowest. In

this situation, the division would be considered the least profitable per dollar invested in the

division because it generated less profit out of each dollar of assets invested.

6. By dividing operating income by the amount of invested assets, each division is placed on

a comparable basis of operating income per dollar invested.

7. (a) Although a new investment’s rate of return exceeds the minimum acceptable for the company as

a whole, a divisional manager might reject the investment if it would decrease the manager’s current

rate of return. (b) The use of residual income as a performance measure can overcome this

disadvantage of the return on investment.

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

BASIC EXERCISES

BE 24–1 (FIN MAN); BE 10–1 (MAN)

$81,000 under budget ($36,000 + $45,000)

BE 24–2 (FIN MAN); BE 10–2 (MAN)

Retail Division Service Charge for Computer Technology Department:

$220,000 = 2,750 billed hours × ($320,000 ÷ 4,000 hours billed)

BE 24–3 (FIN MAN); BE 10–3 (MAN)

Retail

Commercial

Division

Division

Sales …………………………………………………………….

$ 2,150,000

$1,200,000

Cost of goods sold ………………………………………..

(1,300,000)

(800,000)

Gross profit …………………………………………………..

$ 850,000

$ 400,000

Selling expenses ……………………………………………

Operating income before support

Service department allocations ………………………

BE 24–4 (FIN MAN); BE 10–4 (MAN)

a. Profit Margin = $36,000 ÷ $720,000 = 5.0%

BE 24–5 (FIN MAN); BE 10–5 (MAN)

Operating income …………………………………………………………………….

$12,680,000

Minimum acceptable operating income as a

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

BE 24–6 (FIN MAN); BE 10–6 (MAN)

Increase in Pembroke (Supplying)

Division’s Operating Income

=

(Transfer Price – Variable Cost per Unit)

× Units Transferred

=

($82 – $75) × 15,000 units = $105,000

Division’s Operating Income

=

× Units Transferred

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

EXERCISES

Ex. 24–1 (FIN MAN); Ex. 10–1 (MAN)

a.

(a)

$4,300,000

(g)

$8,515,000

(b)

$4,000,000

(h)

$8,200,000

(c)

$300,000

(i)

$315,000

(d)

$8,515,000

(j)

$18,890,000

(f)

$375,000

(l)

$315,000

Schedules of supporting calculations (answers in italics; the solution requires working

from the department level, up to the plant level, then to the vice president of production

level):

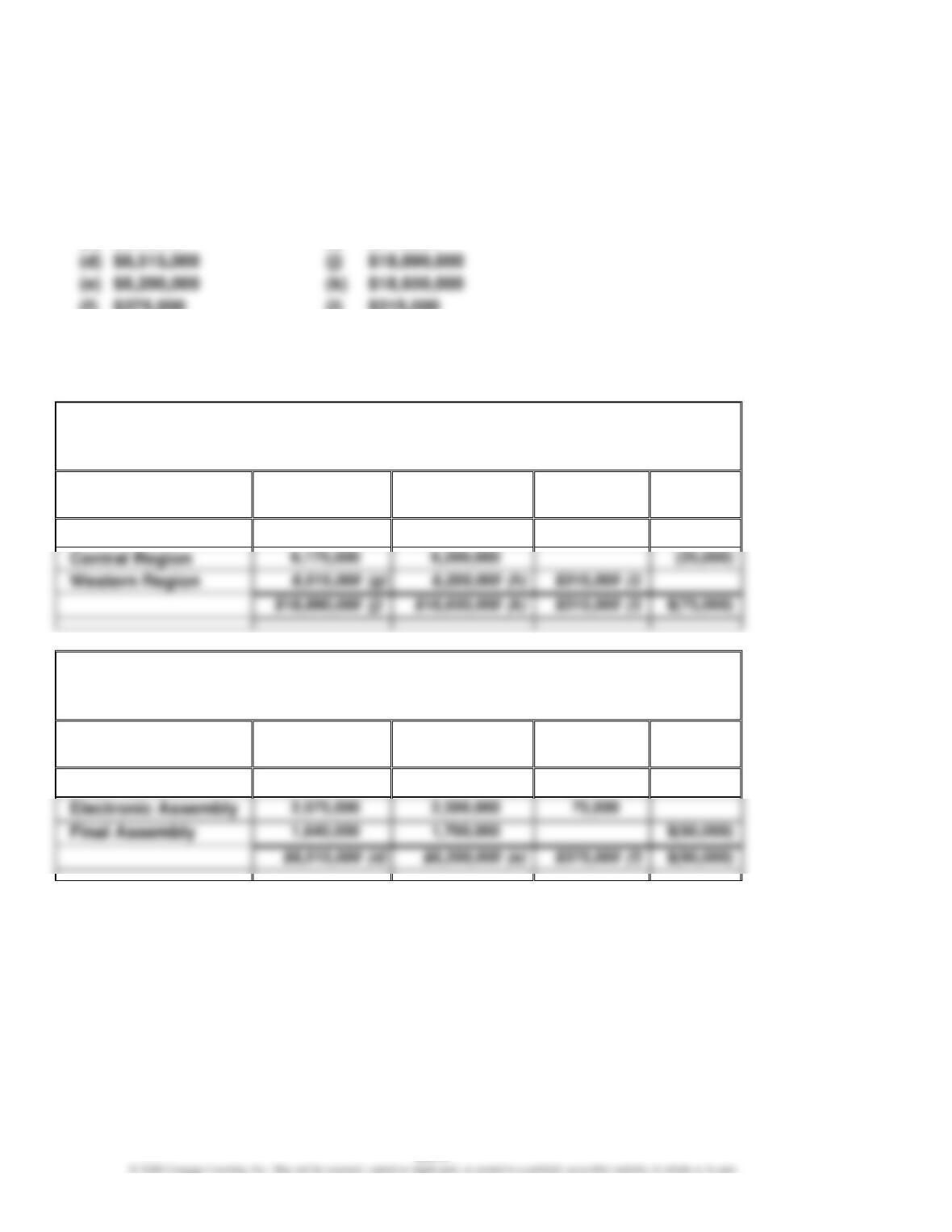

Delmar Company

Budget Performance Report—Vice President, Production

For the Month Ended June 30

Plant

Actual

Budget

Over

Budget

(Under)

Budget

Eastern Region

$ 4,200,000

$ 4,250,000

$(50,000)

Delmar Company

Budget Performance Report—Manager, Western Region Plant

For the Month Ended June 30

Department

Actual

Budget

Over

Budget

(Under)

Budget

Chip Fabrication

$4,300,000

(a)

$4,000,000

(b)

$300,000

(c)

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

Ex. 24–1 (FIN MAN); Ex. 10–1 (MAN) (Concluded)

Delmar Company

Budget Performance Report—Supervisor, Chip Fabrication

For the Month Ended June 30

Cost

Actual

Budget

Over

Budget

(Under)

Budget

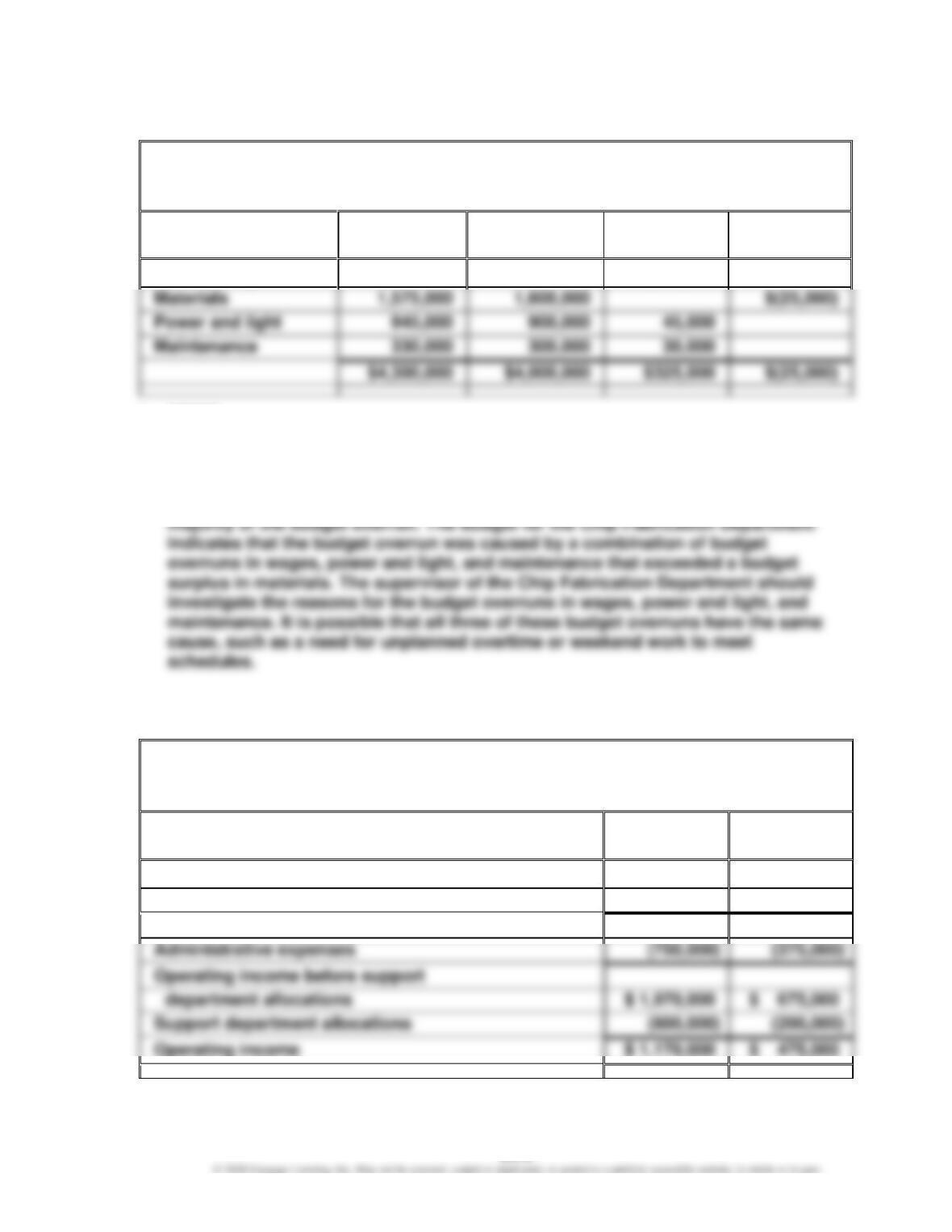

Factory wages

$1,450,000

$1,200,000

$250,000

Power and light

b. MEMO

To: Randi Wilkes, Vice President of Production

The Western Region plant has experienced a budget overrun, while the Eastern

and Central region plants have experienced a budget surplus. The budget of the

Western Region plant reveals that the Chip Fabrication Department caused the

Ex. 24–2 (FIN MAN); Ex. 10–2 (MAN)

Ruiz Industries Inc.

Divisional Income Statements

For the Year Ended November 30, 20Y8

Commercial

Division

Residential

Division

Sales

$ 6,120,000

$ 2,850,000

Cost of goods sold

(3,400,000)

(1,800,000)

Gross profit

$ 2,720,000

$ 1,050,000

Administrative expenses

Operating income before support

Support department allocations

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

Ex. 24–3 (FIN MAN); Ex. 10–3 (MAN)

Support Department Costs

Cost Driver

a.

Legal

Number of hours of legal service

b.

Duplication services

Number of pages copied

c.

Electronic data processing

Central processing unit (CPU) time, number of

Central purchasing

Number of requisitions, number of purchase

e.

Number of phones, number of minutes used

Ex. 24–4 (FIN MAN); Ex. 10–4 (MAN)

a.

6

e.

8

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

Ex. 24–5 (FIN MAN); Ex. 10–5 (MAN)

a.

Government

Residential

Commercial

Contract

Total

Number of payroll checks:

Monthly payroll × 12 ………………..

Weekly payroll × 52………………….

b.

Service

Cost

Allocation

Dept. Cost

÷

Driver

=

Rate

Support department

÷

÷

allocation rates:

Government

Residential

Commercial

Contract

Total

Support department

1 21,760 checks × $1.50 per distribution

2 13,360 checks × $1.50 per distribution

3 7,920 checks × $1.50 per distribution

The support department allocations are determined by multiplying the support

department allocation rate by the cost driver for each division.

c. Residential’s support department allocations are higher than the other two

divisions because Residential is a heavy user of support department services.

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

Ex. 24–6 (FIN MAN); Ex. 10–6 (MAN)

a.

$90,000

Help desk : = $25 per call

3,600calls

$120,000

Network center : = $80 per device monitored

1,500devices

$160,000

Electronic mail: =

5,000accounts $32 per user or email account

$72,000

Smartphone support : = $18 per smartphone issued

4,000smartphones

b. August allocations to the COMM:

Help desk allocation:

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

Ex. 24–7 (FIN MAN); Ex. 10–7 (MAN)

Horton Technology

Divisional Income Statements

For the Year Ended December 31, 20Y7

Consumer

Division

Commercial

Division

Revenues

$ 15,500,000

$ 33,250,000

Cost of goods sold

(10,000,000)

(15,800,000)

Gross profit

$ 5,500,000

$ 17,450,000

Operating expenses

(3,000,000)

(1,750,000)

Operating income before

$ 15,700,000

Support department allocations:

Supporting calculations for controllable support department allocations:

Note 1:

Consumer Division ($1,170,000 ÷ 1,800 computers) × 1,100 computers = $715,000

Commercial Division ($1,170,000 ÷ 1,800 computers) × 700 computers = $455,000

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

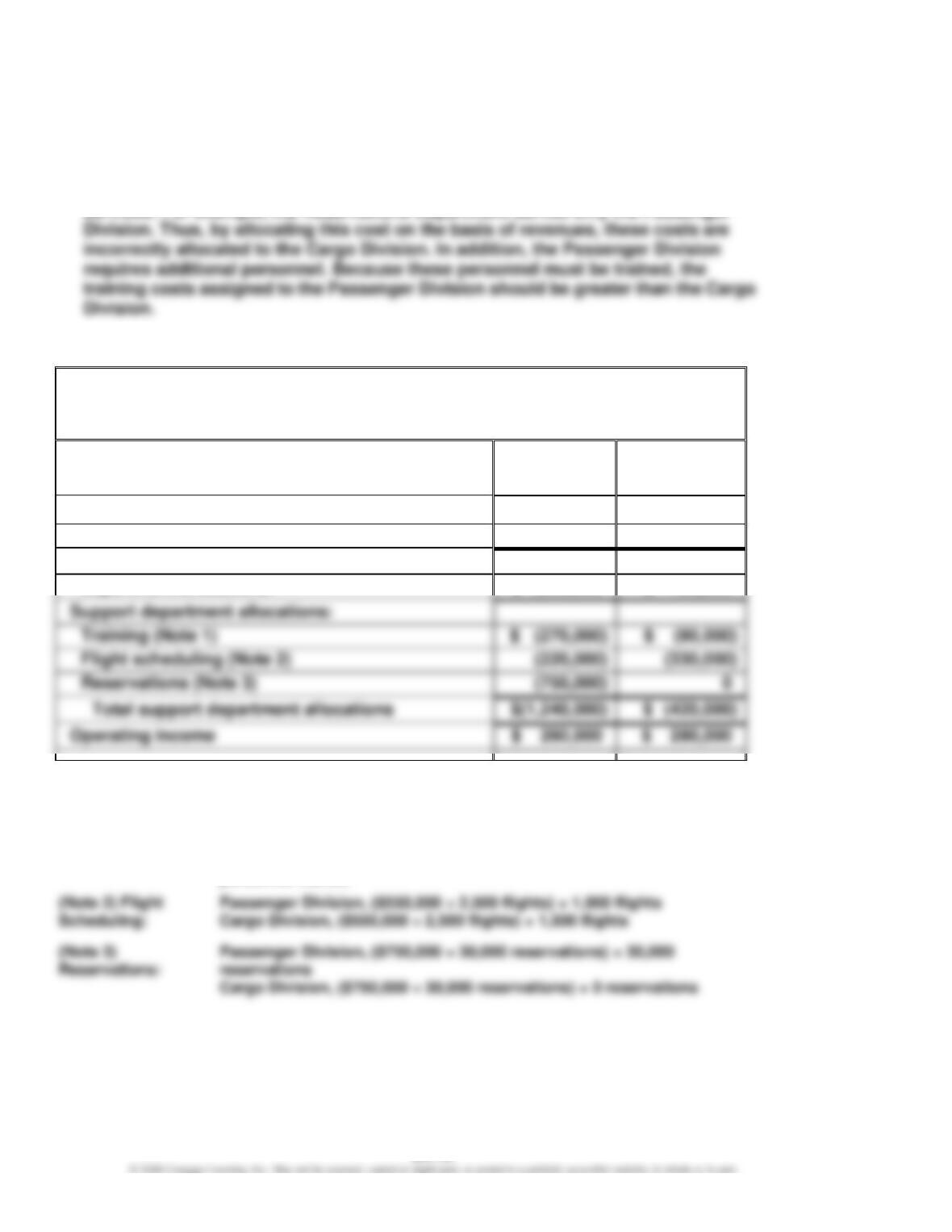

Ex. 24–8 (FIN MAN); Ex. 10–8 (MAN)

a. The reported operating income does not accurately measure performance because

the support department allocations are based on revenues. Revenues are not

associated with the profit center manager’s use of the support department

b.

Rocky Mountain Airlines Inc.

Divisional Income Statements

For the Year Ended December 31, 20Y9

Passenger

Division

Cargo

Division

Revenues

$ 4,200,000

$ 4,200,000

Operating expenses

(2,700,000)

(3,500,000)

Operating income before support

department allocations:

$ 1,500,000

$ 700,000

Support department allocations:

Flight scheduling (Note 2)

Reservations (Note 3)

Supporting calculations for controllable support department allocations:

(Note 1) Training:

Passenger Division, ($360,000 ÷ 800 personnel trained) × 600

personnel trained

Cargo Division, ($360,000 ÷ 800 personnel trained) × 200

(Note 2) Flight

Passenger Division, ($550,000 ÷ 2,500 flights) × 1,000 flights

(Note 3)

Passenger Division, ($750,000 ÷ 30,000 reservations) × 30,000

personnel trained

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

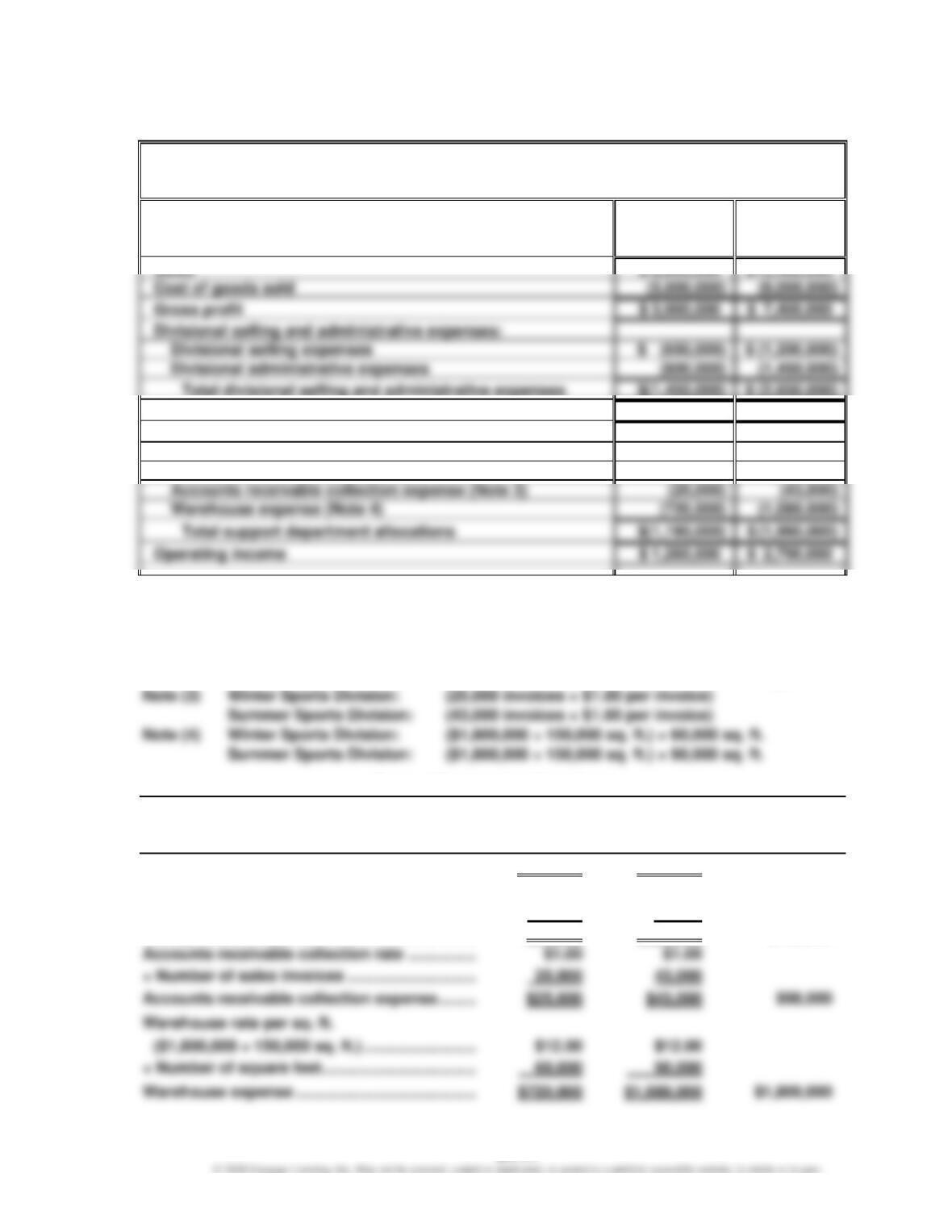

Ex. 24–9 (FIN MAN); Ex. 10–9 (MAN)

Championship Sports Inc.

Divisional Income Statements

For the Year Ended December 31, 20Y9

Winter

Summer

Sports

Sports

Division

Division

$ 8,900,000

Cost of goods sold

Gross profit

$ 3,900,000

$ 7,400,000

Divisional selling and administrative expenses:

Divisional selling expenses

$ (1,200,000)

Divisional administrative expenses

Total divisional selling and administrative expenses

$(1,450,000)

$ (2,650,000)

Operating income before support department allocations

$ 2,450,000

$ 4,750,000

Support department allocations:

Advertising expense (Note 1)

$ (375,000)

$ (715,000)

Transportation expense (Note 2)

(70,000)

(122,000)

Accounts receivable collection expense (Note 3)

(25,000)

Warehouse expense (Note 4)

Operating income

$ 1,260,000

$ 2,790,000

Supporting calculations:

Note (1)

Winter Sports Division:

$375,000

Summer Sports Division:

$715,000

Note (2)

Winter Sports Division:

(17,500 bills of lading × $4.00 per bill of lading)

Summer Sports Division:

(30,500 bills of lading × $4.00 per bill of lading)

Note (3)

Winter Sports Division:

(25,000 invoices × $1.00 per invoice)

Summer Sports Division:

(43,000 invoices × $1.00 per invoice)

Note (4)

Winter Sports Division:

($1,800,000 ÷ 150,000 sq. ft.) × 60,000 sq. ft.

Summer Sports Division:

($1,800,000 ÷ 150,000 sq. ft.) × 90,000 sq. ft.

Support Department Allocations

Winter

Summer

Sports

Sports

Division

Division

Total

Advertising expense ……………………………………

$375,000

$715,000

$1,090,000

Transportation rate per bill of lading ……………

$4.00

$4.00

× Number of bills of lading …………………………..

17,500

30,500

Transportation expense ………………………………

$70,000

$122,000

$192,000

× Number of sales invoices …………………………

25,000

43,000

$12.00

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

Ex. 24–10 (FIN MAN); Ex. 10–10 (MAN)

a.

Retail Division:

24% ($9,600,000 ÷ $40,000,000)

b.

Retail Division

Ex. 24–11 (FIN MAN); Ex. 10–11 (MAN)

a.

Retail

Commercial

Internet

Division

Division

Division

Operating income …………………………….

$ 9,600,000

$12,100,000

$ 6,480,000

Minimum amount of

operating income:

b. Commercial Division

Ex. 24–12 (FIN MAN); Ex. 10–12 (MAN)

a. 2.20 = 13.2% ÷ 6%

b. 18% = 10% × 1.80

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

Ex. 24–13 (FIN MAN); Ex. 10–13 (MAN)

a.

Return

on Investment

=

Profit Margin × Investment Turnover

b. The profit margin would increase from 17% to 18.5%, the investment turnover

would remain unchanged, and the return on investment would increase from

27.2% to 29.6%, as shown below.

Return

on

Investment

=

Profit Margin × Investment Turnover

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

Ex. 24–14 (FIN MAN); Ex. 10–14 (MAN)

a.

Return on O perating Incom e R e v e n u e s

=×

Revenues Invested Assets

Investm ent

( )

Parks and Resorts : $3,298 $16,974

×

$16,974 $28,275

= 19.4% × 0.60

=11.6% rounded

Studio Entertainment : $2,703 $9,441

×

$9,441 $15,359

= 28.6% × 0.61

=17.4% rounded

b. The four segments are different from each other. Media Networks combines a good

profit margin of 32.7% with an investment turnover of 0.72. Media Networks is

sensitive to advertising revenue, while the Studio Entertainment segment is

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

Ex. 24–15 (FIN MAN); Ex. 10–15 (MAN)

a.

16.5% ($198,000 ÷ $1,200,000)

g.

$105,000 ($750,000 × 14%)

b.

$144,000 ($1,200,000 × 12%)

h.

12.0% ($90,000 ÷ $750,000)

c.

$54,000 ($198,000 – $144,000)

i.

$15,000 ($105,000 – $90,000)

$160,000 ($120,000 + $40,000)

24.5% ($441,000 ÷ $1,800,000)

e.

20.0% ($160,000 ÷ $800,000)

k.

$270,000 ($1,800,000 × 15%)

Ex. 24–16 (FIN MAN); Ex. 10–16 (MAN)

a.

(a)

$60,200 ($860,000 × 7.0%)

(b)

$344,000 ($60,200 ÷ 17.5%)

(c)

2.5 (17.5% ÷ 7.0%) or $860,000 ÷ $344,000

(d)

$1,140,000 ($51,300 ÷ 4.5%)

(e)

$300,000 ($1,140,000 ÷ 3.8)

$102,000 ($680,000 × 15.0%)

10.0% ($102,000 ÷ $1,020,000)

1.5 ($1,020,000 ÷ $680,000)

(k)

8.0% ($89,600 ÷ $1,120,000)

2.0 ($1,120,000 ÷ $560,000)

b.

North Division:

$18,920 [$60,200 – ($344,000 × 12%)]

South Division:

$15,300 [$51,300 – ($300,000 × 12%)]

East Division:

$20,400 [$102,000 – ($680,000 × 12%)]

West Division:

$22,400 [$89,600 – ($560,000 × 12%)]

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

Ex. 24–17 (FIN MAN); Ex. 10–17 (MAN)

a.

Increase in Ziegler Inc.’s

Market

Variable Cost

Units

Operating Income

=

Price

–

per Unit

×

Transferred

$33,750,000

=

($1,350

–

$900)

×

75,000

=

×

Variable Cost

Units

Operating Income

Price

–

per Unit

Transferred

Ex. 24–18 (FIN MAN); Ex. 10–18 (MAN)

a.

Increase in Ziegler Inc.’s

Market

Variable Cost

Units

Operating Income

=

Price

–

per Unit

×

Transferred

$33,750,000

=

($1,350

–

$900)

×

75,000

This amount is the same amount by which Ziegler Inc.’s operating income increased

in Ex. 24–17, when a transfer price of $1,000 was used.

b.

Increase in the Instrument Division’s

Market

Transfer

Units

Operating Income

=

Price

–

Price

×

Transferred

$11,250,000

=

($1,350

–

$1,200)

×

75,000

×

This is the amount the Components Division earns by using available excess capacity

to produce and sell products above variable cost to the Instrument Division.

d. Any transfer price will cause the total income of the company to increase, as long

as the supplier division capacity is used toward making materials for products that

are ultimately sold to the outside. However, transfer prices should be set between

variable cost and the market price in order to give the division managers proper

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

PROBLEMS

Prob. 24–1A (FIN MAN); Prob. 10–1A (MAN)

1.

GHT Tech Inc.

Budget Performance Report—Director, Consumer Products Division

For the Month Ended January 31

Actual

Budget

Over

Budget

(Under)

Budget

Customer service salaries

$ 602,350

$ 546,840

$ 55,510

Insurance and property taxes

110,240

114,660

$ (4,420)

Distribution salaries

861,200

872,340

(11,140)

Marketing salaries

56,860

Engineer salaries

820,008

836,850

(16,842)

Warehouse wages

562,632

586,110

(23,478)

Equipment depreciation

183,610

183,792

Total

$4,225,270

$4,168,962

$112,370

$(56,062)

2. The customer service and marketing salaries are significantly over budget. The

director should investigate the cause of these results. One possibility is that the

company is having an increase in sales, requiring greater marketing effort and

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

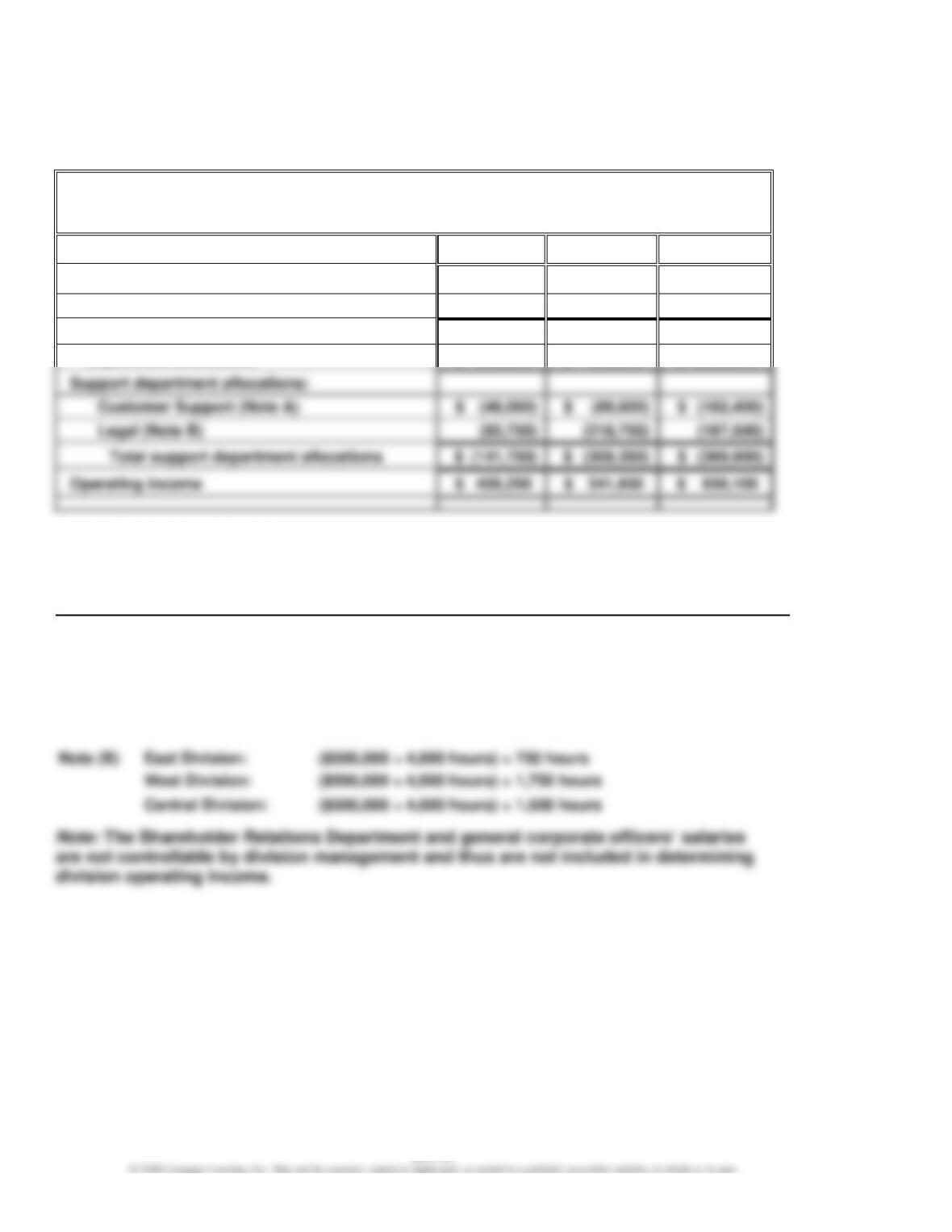

Prob. 24–2A (FIN MAN); Prob. 10–2A (MAN)

1.

Red Line Railroad Inc.

Divisional Income Statements

For the Quarter Ended December 31

East

West

Central

Revenues

$1,400,000

$ 2,000,000

$ 3,200,000

Operating expenses

(800,000)

(1,350,000)

(1,900,000)

Operating income before support

department allocations

$ 600,000

$ 650,000

$ 1,300,000

Support department allocations:

Supporting computations:

Support department allocation rates for Customer Support and Legal are determined as

follows:

East

West

Central

Total

Number of customer contacts …..

1,500

2,800

5,700

10,000

Number of hours billed ……………..

750

1,750

1,500

4,000

Note (A)

East Division:

($320,000 + 10,000 contacts) × 1,500 contacts

West Division:

($320,000 ÷ 10,000 contacts) × 2,800 contacts

Central Division:

($320,000 ÷ 10,000 contacts) × 5,700 contacts

West Division:

($500,000 ÷ 4,000 hours) × 1,750 hours

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

Prob. 24–2A (FIN MAN); Prob. 10–2A (MAN) (Concluded)

2. The CEO evaluates the three divisions using operating income as a percent of

revenues (profit margin). This measure is computed for the three divisions as follows:

3. To: CEO

The method used to evaluate the performance of the divisions should be

reevaluated. The present method identifies the amount of operating income per

dollar of earned revenue. However, this company requires a significant investment

in fixed assets for production and distribution facilities. The amount of assets may

CHAPTER 24 (FIN MAN); CHAPTER 10 (MAN) Evaluating Decentralized Operations

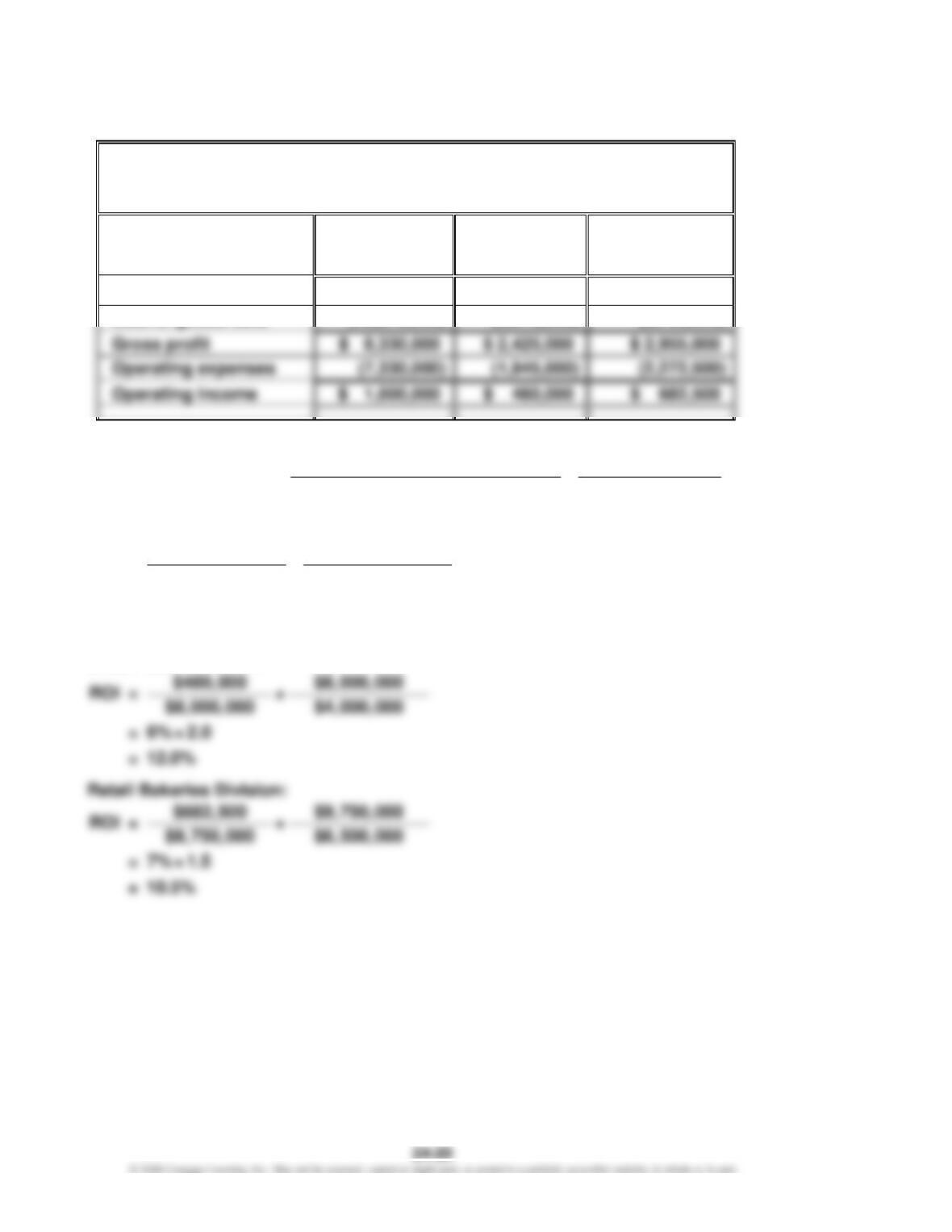

Prob. 24–3A (FIN MAN); Prob. 10–3A (MAN)

1.

The Crunchy Granola Company

Divisional Income Statements

For the Year Ended June 30, 20Y7

Cereal

Division

Snack Cake

Division

Retail

Bakeries

Division

Sales

$ 25,000,000

$ 8,000,000

$ 9,750,000

2.

Return on Investment = Profit Margin × Investment Turnover

Operating Income Sales

Return on Investment = ×

Sales Invested Assets

Cereal Division:

$1,000,000 $25,000,000

ROI = ×

$25,000,000 $10,000,000

= 4% × 2.5

= 10.0%

Snack Cake Division: