*PROBLEM 10-7A

2014

(a) Jan. 1 Interest Payable …………………………… 96,000

Cash …………………………………….. 96,000

(b) Dec. 31 Interest Expense ………………………….. 98,400

Interest Payable

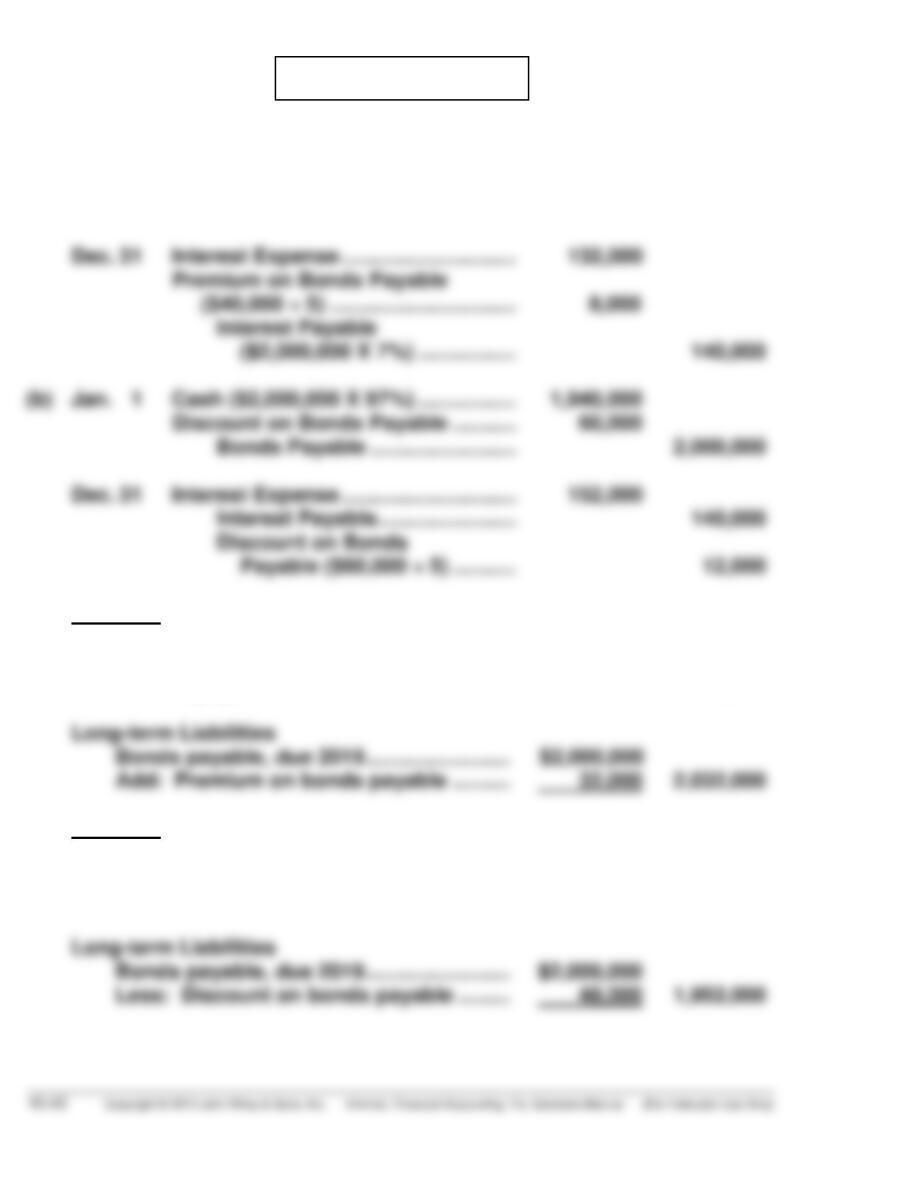

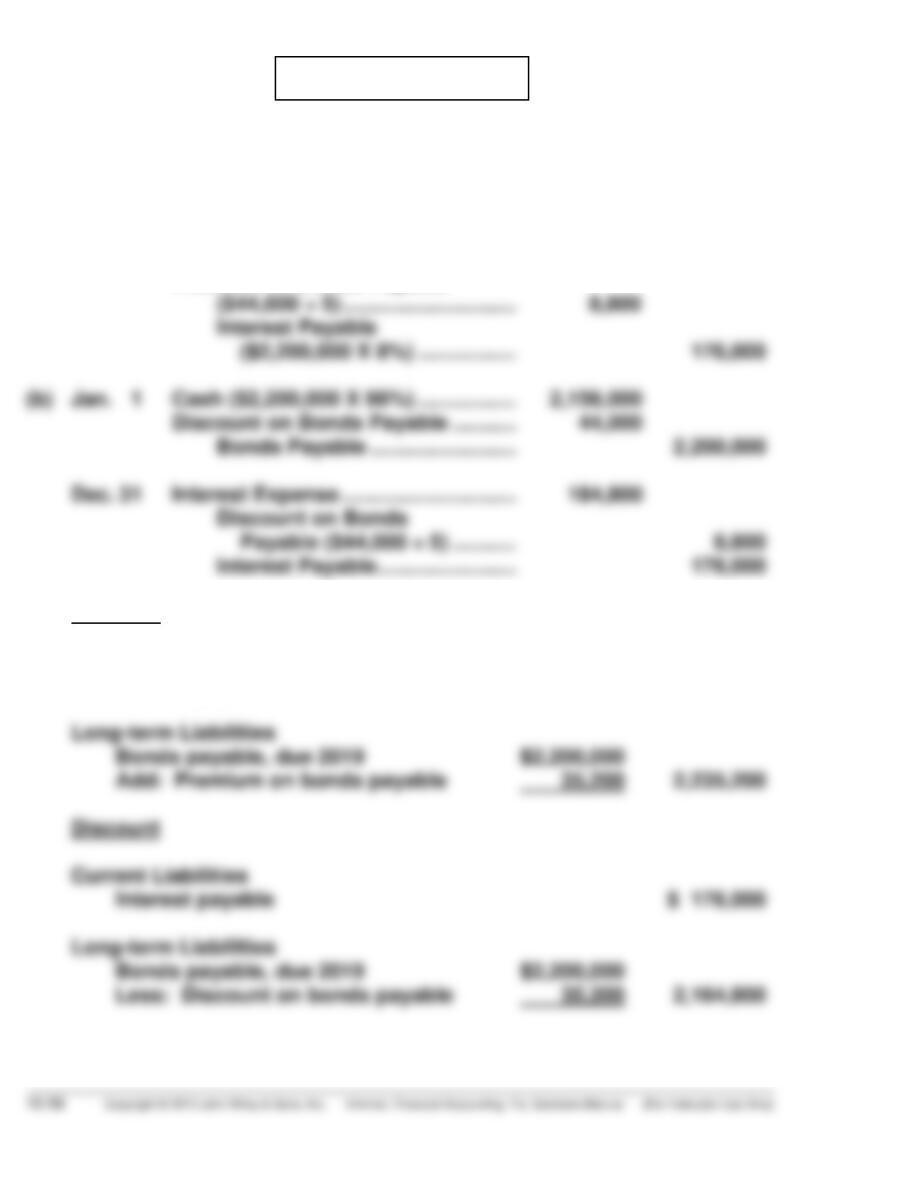

(d) Dec. 31 Interest Expense ………………………….. 82,000

Interest Payable ……………………. 80,000**

Discount on Bonds Payable ….. 2,000**

*PROBLEM 10-8A

(a) Jan. 1 Cash ($2,000,000 X 102%) …………… 2,040,000

Bonds Payable ……………………. 2,000,000

Premium on Bonds Payable …. 40,000

(c) Premium

Current Liabilities

Interest payable …………………………………. $ 140,000

Discount

Current Liabilities

Interest payable …………………………………. $ 140,000

*PROBLEM 10-9A

(a) 1. 1/1/14 Cash ($3,000,000 X 103%) ……. 3,090,000

Bonds Payable ……………… 3,000,000

Premium on Bonds

(b) See amortization tables on following page.

(c) 1. 12/31/14 Interest Expense …………………. 231,000

Premium on Bonds

(d) 1. Long-term Liabilities:

Bonds Payable ………………………………. $3,000,000

10-44 Copyright © 2013 John Wiley & Sons, Inc. Kimmel, Financial Accounting, 7/e, Solutions Manual (For Instructor Use Only)

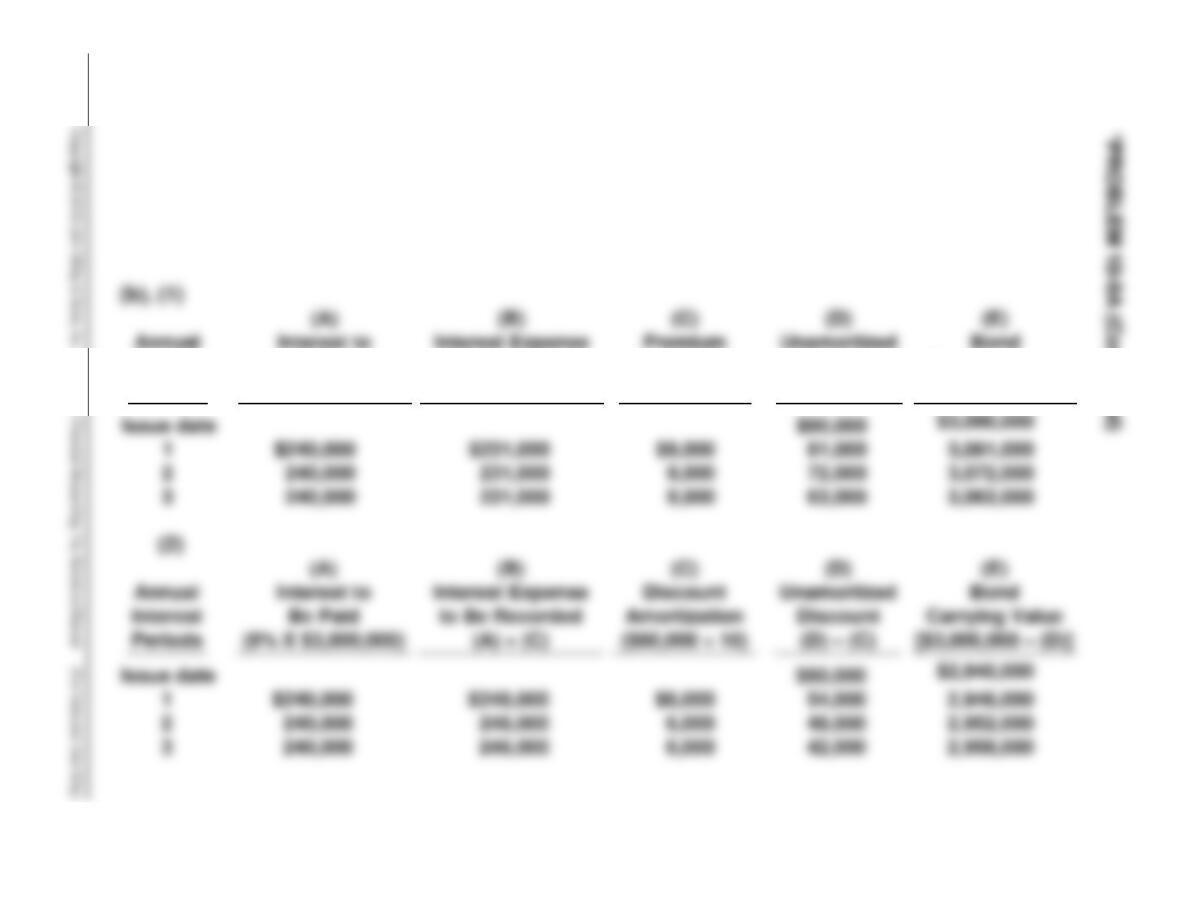

Annual

Interest

Periods

Interest to

Be Paid

(8% X $3,000,000)

Interest Expense

to Be Recorded

(A) – (C)

Premium

Amortization

($90,000 ÷ 10)

Unamortized

Premium

(D) – (C)

Bond

Carrying Value

[$3,000,000 + (D)]

*PROBLEM 10-10A

2014

(a) Jan. 1 Cash ………………………………………….. 1,667,518

(b) LOCK CORP.

Bond Discount Amortization

Effective-Interest Method—Annual Interest Payments

5% Bonds Issued at 6%

Annual

Interest

Periods

(A)

Interest

to Be

Paid

(B)

Interest

Expense

to Be

Recorded

(C)

Discount

Amor-

tization

(B) – (A)

(D)

Unamor-

tized

Discount

(D) – (C)

(E)

Bond

Carrying

Value

($1,800,000 – D)

Issue date

$132,482

$1,667,518

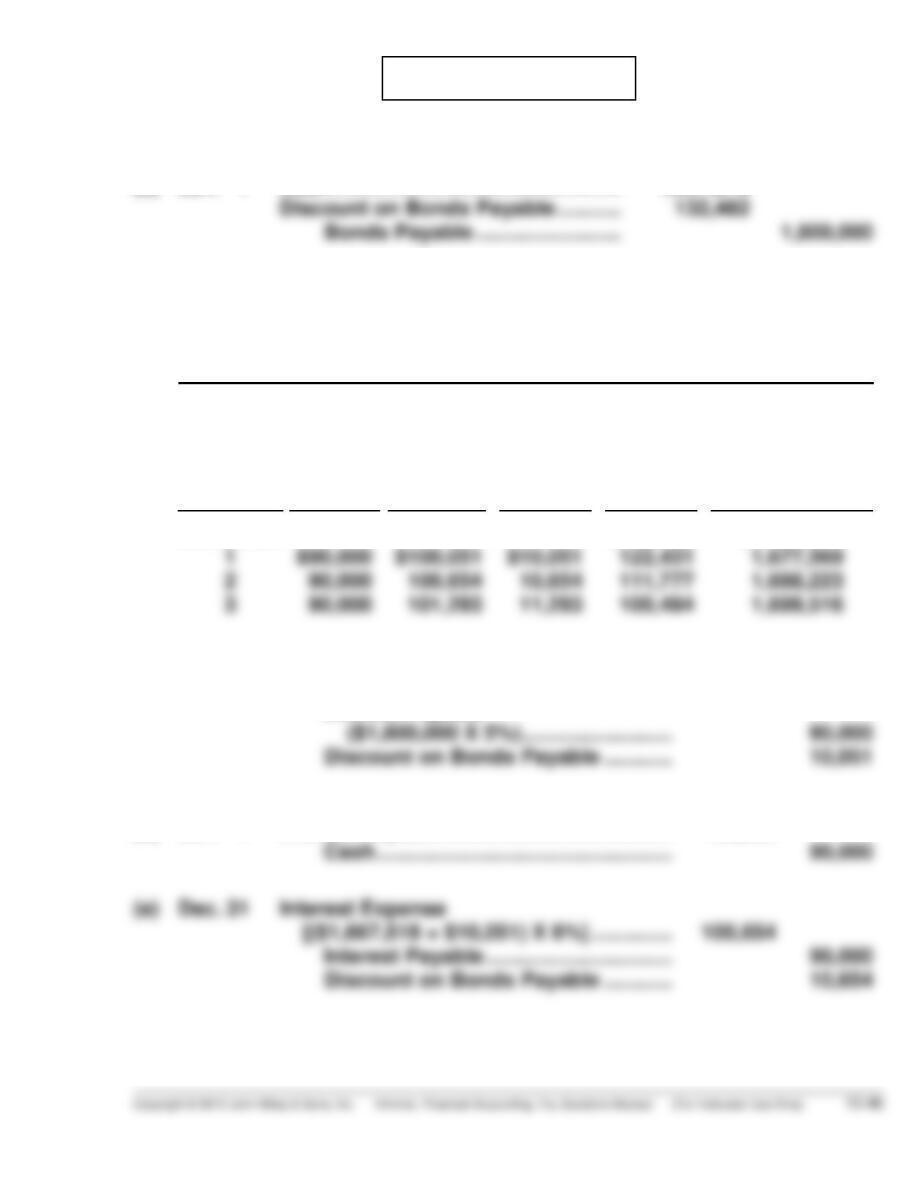

(c) Dec. 31 Interest Expense

($1,667,518 X 6%) …………………………… 100,051

Interest Payable

2015

(d) Jan. 1 Interest Payable …………………………………. 90,000

*PROBLEM 10-11A

2014

(a) 1. Jan. 1 Cash …………………………………….. 2,147,202

Bonds Payable ………………. 2,000,000

2. Dec. 31 Interest Expense

($2,147,202 X 6%) ………………. 128,832

2015

3. Jan. 1 Interest Payable ……………………. 140,000

Cash ……………………………… 140,000

(b) Bonds payable …………………………………………….. 2,000,000

(c) 1. Total bond interest expense—2015, $128,162.

2. The effective-interest method will result in more interest expense

*PROBLEM 10-12A

(a)

Quarterly

Interest Period

(A)

Cash

Payment

(B)

Interest

Expense

(D) X 2%

(C)

Reduction

of Principal

(A) – (B)

(D)

Principal

Balance

(D) – (C)

Issue Date

1

$30,259

$6,400

$23,859

$320,000

296,141

(b) Dec. 31 Mortgage Payable …………………………… 23,859

Long-term liabilities

*PROBLEM 10-13A

(a)

Period

Cash

Payment

(A)

Interest

Expense

(B) = (D) X 7%

Principal

Reduction

(C) = (A) – (B)

Balance

(D) = (D) – (C)

July 1, 2013 $150,000

June 30, 2014 $ 36,584 $10,500 $ 26,084 123,916

June 30, 2015 36,584 8,674 27,910 96,006

(b) July 1/13 Cash …………………………………………… 150,000

Notes Payable ………………………… 150,000

(c) 2015

Current liabilities

PROBLEM 10-1B

(a) Jan. 1 Cash ………………………………………………….. 18,000

Notes Payable …………………………….. 18,000

(b) Jan. 31 Interest Expense ………………………………… 120

Interest Payable

($18,000 X 8% X 1/12 = $120) ……. 120

PROBLEM 10-1B (Continued)

(c) Current liabilities

Notes payable ……………………………………………………….. $ 18,000

Accounts payable ………………………………………………….. 52,000

PROBLEM 10-2B

(a) Aug. 1 Inventory or Purchases …………………….. 6,000

Notes Payable ……………………………. 6,000

Oct. 1 Buildings ………………………………………….. 50,000

Notes Payable ……………………………. 40,000

Cash ………………………………………….. 10,000

PROBLEM 10-2B (Continued)

(b)

Notes Payable Interest Payable

11/1 6,000 8/1 6,000 11/1 135 8/31 45

9/1 15,000 9/30 145

Interest Expense

8/31 45

9/30 145

(c) Current liabilities

Notes payable ……………………………………………………….. 55,000

PROBLEM 10-3B

(a) Jan. 1 Interest Payable ……………………………….. 96,000

Cash ………………………………………….. 96,000

PROBLEM 10-4B

(a) 2013 Cash …………………………………………………. 600,000

April 1 Bonds Payable …………………………… 600,000

(d) 2014 Interest Payable ………………………………… 22,500

April 1 Interest Expense

($600,000 X 5% X 3/12) ……………………. 7,500

PROBLEM 10-5B

(a) 2014

Jan. 1 Cash ($5,000,000 X 103%) …………….. 5,150,000

Bonds Payable ……………………… 5,000,000

(b) Long-term Liabilities

(c) 2015

Jan. 1 Bonds Payable …………………………….. 5,000,000

Premium on Bonds Payable …………. 120,000*

PROBLEM 10-6B

(a)

2014 2013

1. Current ratio $2,717 ÷ $4,044

= .67:1

$2,427 ÷ $4,020

= .60:1

(b) The company’s liquidity position as measured through the current

ratio and free cash flow has improved. The debt to assets ratio

(c) Kellogg’s use of operating leases (vs. capital leases) would reduce its

solvency. If the leases were capital rather than operating, the balance

*PROBLEM 10-7B

2014

(a) Jan. 1 Interest Payable ………………………… 144,000

Cash ………………………………….. 144,000

2015

(c) Jan. 1 Bonds Payable ………………………….. 1,800,000

Premium on Bonds Payable ………. 126,000*

(d) Dec. 31 Interest Expense ……………………….. 58,000

Premium on Bonds Payable ………. 14,000**

*PROBLEM 10-8B

(a) Jan. 1 Cash ($2,200,000 X 102%) …………… 2,244,000

Premium on Bonds Payable …. 44,000

Bonds Payable ……………………. 2,200,000

Dec. 31 Interest Expense ………………………… 167,200

Premium on Bonds Payable

(c) Premium

Current Liabilities

Interest payable $ 176,000

*PROBLEM 10-9B

(a) (1) 1/1/14 Cash ($3,000,000 X 103%) ….. 3,090,000

Bonds Payable ……………. 3,000,000

(2) 1/1/14 Cash ($3,000,000 X 99%) ……. 2,970,000

Discount on Bonds

(b) See amortization tables on following page.

(c) (1) 12/31/14 Interest Expense ……………….. 198,750

Premium on Bonds

(2) 12/31/14 Interest Expense ……………….. 213,750

Discount on Bonds

(d) (1) Long-term Liabilities:

(2) Long-term Liabilities:

Interest

Be Paid

to Be Recorded

Amortization

Premium

Carrying Value

10-60 Copyright © 2013 John Wiley & Sons, Inc. Kimmel, Financial Accounting, 7/e, Solutions Manual (For Instructor Use Only)