Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 10

SOLUTIONS TO EXERCISES—SET B

EXERCISE 10-1B

(a) Under the historical cost principle, the acquisition cost for a plant

asset includes all expenditures necessary to acquire the asset and

make it ready for its intended use. For example, the cost of factory

(b) 1. Equipment

2. Equipment

3. Land

EXERCISE 10-2B

1. Equipment

2. Equipment

3. Equipment

EXERCISE 10-3B

(a) Cost of land

Cash paid .......................................................................... $75,000

Net cost of removing warehouse

($6,400 – $1,200) ........................................................... 5,200

(b) The architect’s fee ($5,800) should be debited to the Buildings account.

EXERCISE 10-4B

1. True.

2. False. Depreciation enables companies to properly match the expense

of using buildings and equipment to the revenues they help earn.

3. True.

4. False. Depreciation applies to three classes of plant assets: land improve-

ments, buildings, and equipment.

EXERCISE 10-5B

(a) Depreciation cost per unit is $1.80 per mile

[($188,000 – $8,000) ÷ 100,000].

(b)

Computation

End of Year

Year

Units of

Activity

X

Depreciation

Cost /Unit

=

Annual

Depreciation

Expense

Accumulated

Depreciation

Book

Value

2017

27,000

$1.80

$48,600

$ 48,600

$139,400

EXERCISE 10-6B

(a) Straight-line method:

$145,000 –$25,000

5

= $24,000 per year.

(b) Units-of-activity method:

$145,000 –$25,000

20,000

= $6.00 per hour.

(c) Declining-balance method:

EXERCISE 10-7B

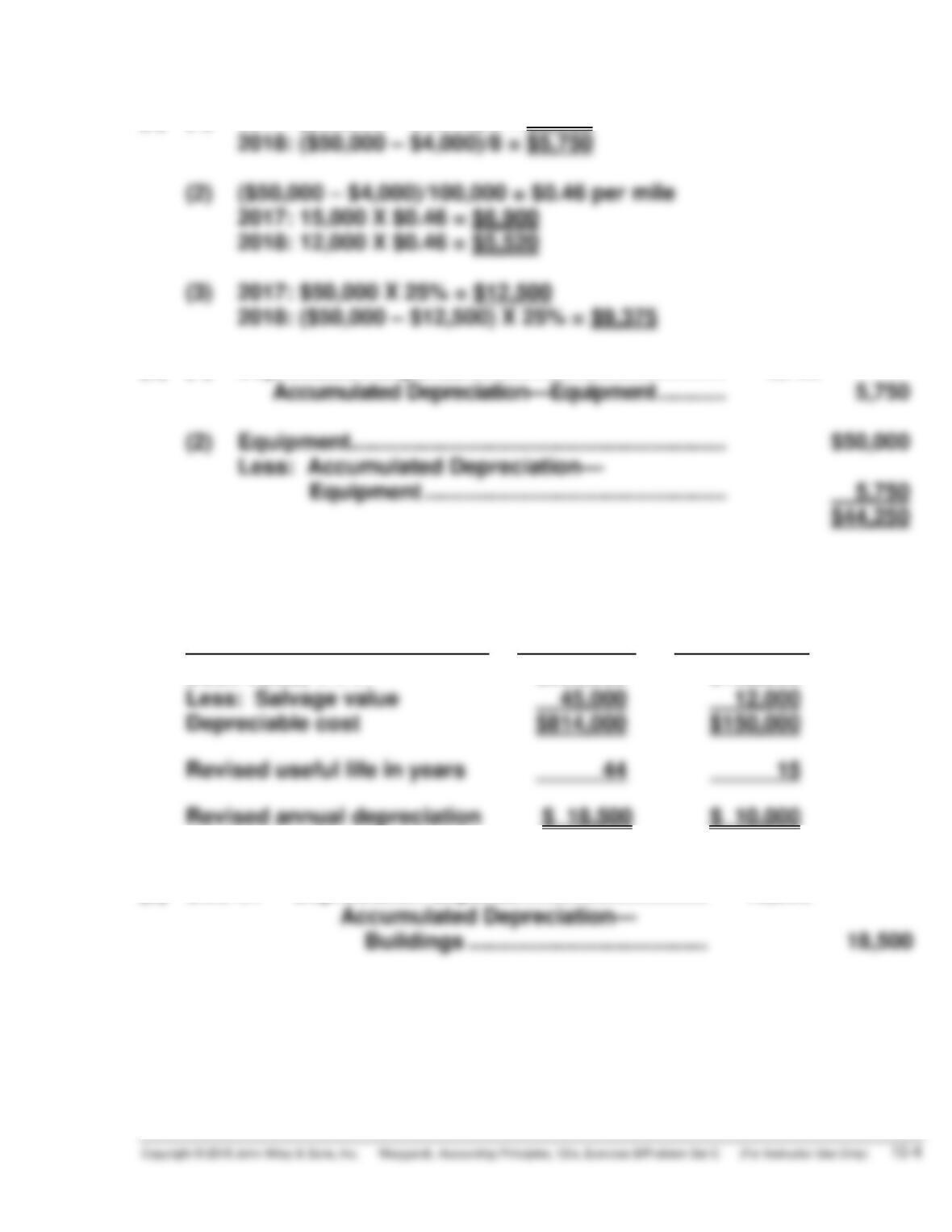

(a) (1) 2017: ($50,000 – $4,000)/8 = $5,750

2018: ($50,000 – $4,000)/8 = $5,750

(2) ($50,000 – $4,000)/100,000 = $0.46 per mile

(b) (1) Depreciation Expense .......................................... 5,750

Accumulated Depreciation—Equipment ........... 5,750

EXERCISE 10-8B

(a)

Type of Asset

Building

Warehouse

Book value, 1/1/17

Less: Salvage value

$859,000

45,000

$162,000

12,000

(b) Dec. 31 Depreciation Expense .............................. 18,500

EXERCISE 10-9B

Jan. 1 Accumulated Depreciation—Equipment .......... 75,000

Machinery ................................................... 75,000

June 30 Depreciation Expense ....................................... 3,500

Accumulated Depreciation—

Equipment ($35,000 X 1/5 X 6/12) .......... 3,500

EXERCISE 10-10B

(a) Cash ............................................................................. 38,000

Accumulated Depreciation—Equipment

(b) Depreciation Expense

[($70,000 – $10,000) X 1/5 X 4/12]............................ 4,000

Accumulated Depreciation—Equipment .......... 4,000

EXERCISE 10-10B (Continued)

(c) Cash ........................................................................... 23,000

Accumulated Depreciation—Equipment .................. 36,000

Loss on Disposal of Plant Assets ............................ 11,000

Equipment ........................................................... 70,000

EXERCISE 10-11B

(a) Dec. 31 Inventory ................................................... 75,000

Accumulated Depletion

(100,000 X $.75) ............................. 75,000

EXERCISE 10-12B

Dec. 31 Amortization Expense .................................. 16,000

Patents ($120,000 X 1/5 X 8/12) ............ 16,000

EXERCISE 10-13B

1/2/17 Patents .......................................................... 840,000

Cash ...................................................... 840,000

4/1/17 Goodwill ....................................................... 450,000

Cash ...................................................... 450,000

(Part of the entry to record

purchase of another company)

Ending balances, 12/31/17:

Patents = $720,000 ($840,000 – $120,000).

EXERCISE 10-14B

*EXERCISE 10-15B

(a) Equipment (new) ........................................................ 54,000

Accumulated Depreciation—Equipment (old) ......... 42,000

Loss on Disposal of Plant Assets ............................ 7,000

Equipment (old) .................................................. 74,000

Cash .................................................................... 29,000

Cost of old trucks $74,000

Less: Accumulated depreciation 42,000

(b) Equipment (new) ........................................................ 25,000

Accumulated Depreciation—Equipment (old) ......... 14,000

Gain on Disposal ................................................ 2,000

Equipment (old) .................................................. 20,000

Cash .................................................................... 17,000

*EXERCISE 10-16B

(a) Equipment (new) ........................................................ 8,000

Loss on Disposal of Plant Assets ............................ 2,000

Accumulated Depreciation—Equipment (old) ......... 25,000

Equipment (old) .................................................. 35,000

(b) Equipment (new) ........................................................ 8,000

Accumulated Depreciation—Equipment (old) ......... 16,000

Equipment (old) .................................................. 21,000

Gain on Disposal of Plant Assets ..................... 3,000

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 10-1C

Item

Land

Buildings

Other Accounts

1

2

3

4

($ 2,000)

$600,000

22,000

$ 3,000 Property Taxes Expense

PROBLEM 10-2C

(a)

Year

Computation

Cumulative

12/31

MACHINE 1

2013

2014

2015

2016

$ 80,000 X 10% = $8,000

$ 80,000 X 10% = $8,000

$ 80,000 X 10% = $8,000

$ 80,000 X 10% = $8,000

$ 8,000

16,000

24,000

32,000

(b)

Year

Depreciation Computation

Expense

MACHINE 2

(1)

2015

$120,000 X 25% X 9/12 = $22,500

$22,500