EXERCISE 10-10

(a) Jan. 1 Cash ($600,000

× 1.03) ………………………. 618,000

Bonds Payable …………………………… 600,000

EXERCISE 10-11

(a) Jan. 1 Cash ($500,000

× .96) ……………………… 480,000

EXERCISE 10-12

(a) The General Electric bonds were issued at a premium and the Boeing

bonds were issued at a discount.

(b) The prices of the two bonds differed because bond price is based on the

EXERCISE 10-13

2014

(a) Jan. 1 Cash ……………………………………………….. 350,000

Bonds Payable …………………………. 350,000

EXERCISE 10-14

(a) April 30 Bonds Payable ……………………………….. 140,000

Loss on Bond Redemption ……………… 14,900*

Cash ($140,000 X 101%) …………… 141,400

EXERCISE 10-15

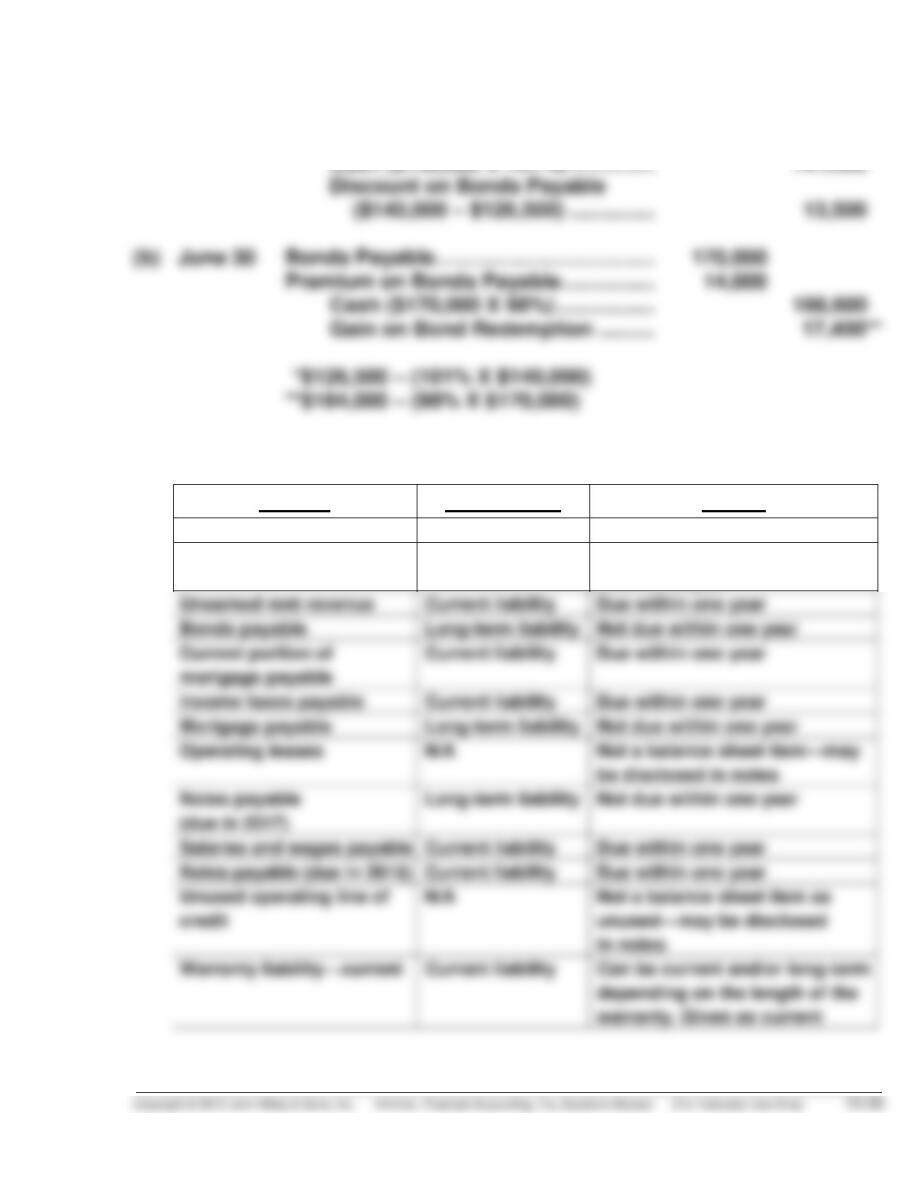

(a) Account Classification Reason

Accounts payable Current liability Due within one year

Accrued pension liability Long-term liability Relates to pensions. Not due

within one year

EXERCISE 10-15 (Continued)

(b) SANTANA INC.

Balance Sheet (Partial)

January 31, 2014

(in thousands)

Current liabilities

Notes payable ……………………………………… $2,563.6

Accounts payable ……………………………….. 4,263.9

EXERCISE 10-16

(a) 1. Working capital = $3,416.3 – $2,988.7 = $427.6

2. Current ratio = $3,416.3 ÷ $2,988.7 = 1.14:1

EXERCISE 10-16 (Continued)

(b) Debt to assets ratio, adjusted for off-balance-sheet lease obligations.

EXERCISE 10-17

(a) Current ratio

2014 $10,795 ÷ $4,897 = 2.20:1

EXERCISE 10-18

(a) Current ratio

(b) Current ratio

(c) The liquidity ratios would not change but having access to a line of

EXERCISE 10-19

(a) The company does not have to record these contingent liabilities

because they have determined that they are not likely to occur and the

impact would be immaterial in any event.

*EXERCISE 10-20

2014

(a) Jan. 1 Cash ($500,000 X 103%) ………………….. 515,000

Bonds Payable ………………………… 500,000

Premium on Bonds Payable ……… 15,000

*EXERCISE 10-21

2013

(a) Dec. 31 Cash ……………………………………………… 288,000

Discount on Bonds Payable ……………. 12,000

Bonds Payable ………………………… 300,000

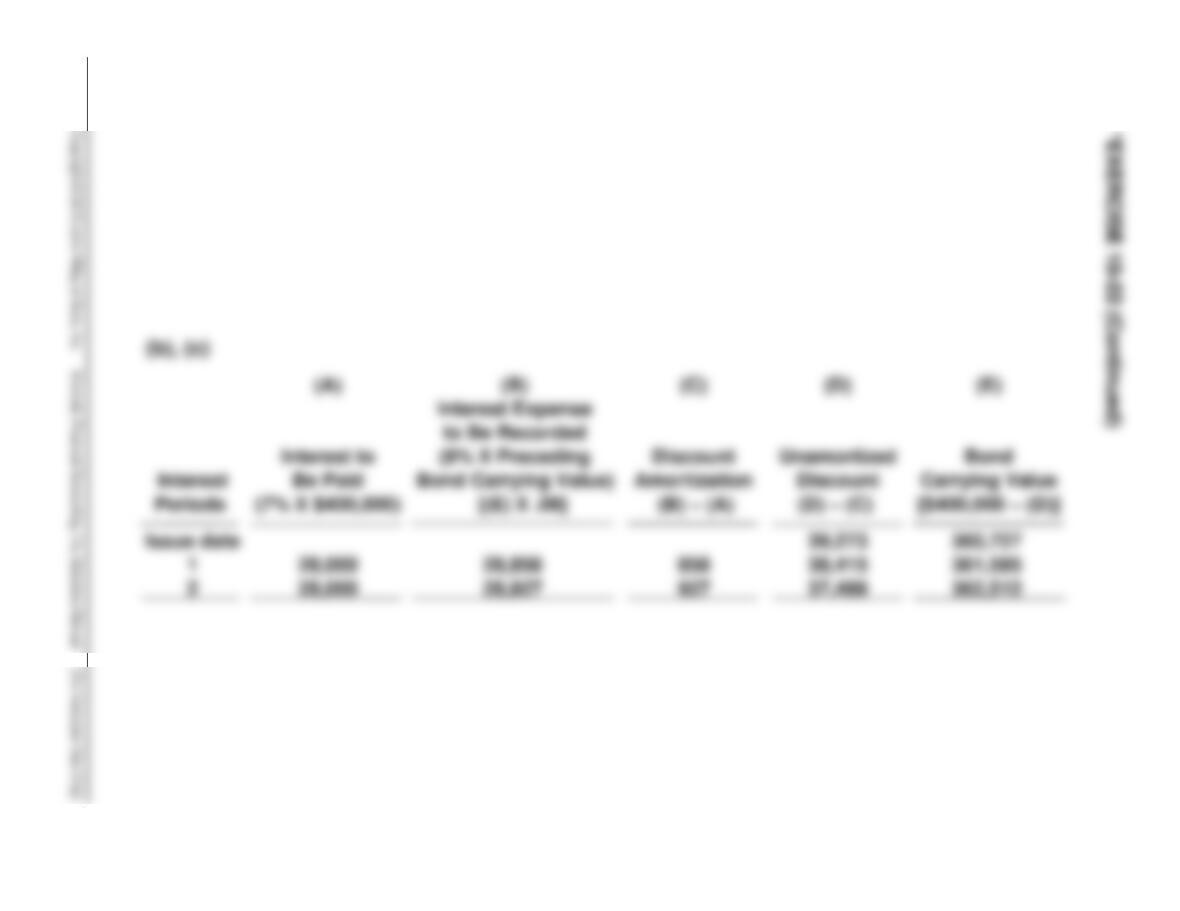

*EXERCISE 10-22

2014

(a) Jan. 1 Cash ……………………………………………….. 360,727

Discount on Bonds Payable …………….. 39,273

Bonds Payable …………………………. 400,000

10-28

10-28 Copyright © 2013 John Wiley & Sons, Inc. Kimmel, Financial Accounting, 7/e, Solutions Manual (For Instructor Use Only)

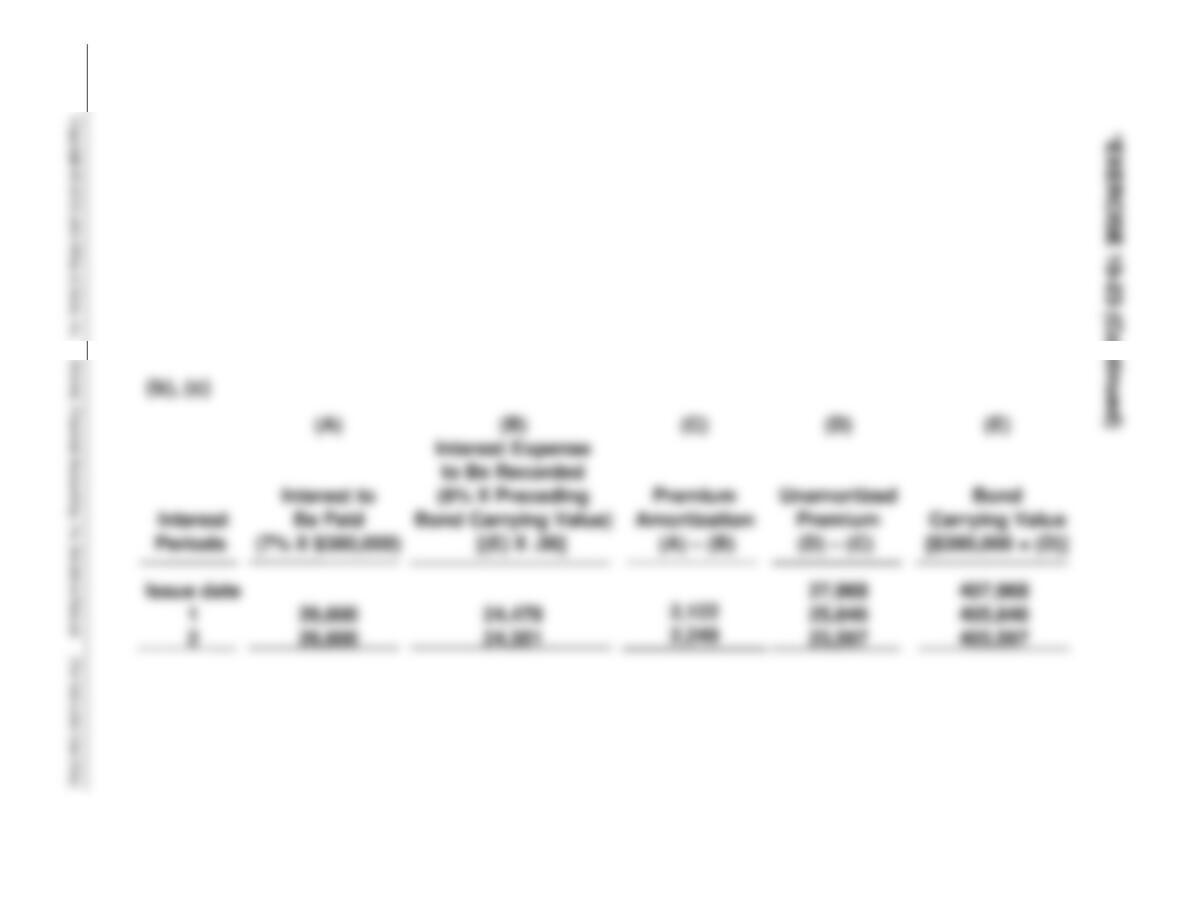

*EXERCISE 10-23

2014

(a) Jan. 1 Cash ……………………………………………….. 407,968

Bonds Payable …………………………. 380,000

Premium on Bonds Payable ……… 27,968

10-30 Copyright © 2013 John Wiley & Sons, Inc. Kimmel, Financial Accounting, 7/e, Solutions Manual (For Instructor Use Only)

*EXERCISE 10-24

Issuance of Note

2014 Dec. 31 Cash …………………………………………. 280,000

Mortgage Payable ………………. 280,000

(A) (B) (C) (D)

Semiannual Interest Reduction Principal

Interest Cash Expense of Principal Balance

*EXERCISE 10-25

Annual

Interest

Period

(A)

Cash

Payment

(B)

Interest

Expense

(D) X 10%

(C)

Reduction

of Principal

(A) – (B)

(D)

Principal

Balance

(D) – (C)

GOINS CORPORATION

Balance Sheet (Partial)

December 31, 2014

SOLUTIONS TO PROBLEMS

PROBLEM 10-1A

(a) Jan. 1 Cash ………………………………………………….. 18,000

Notes Payable …………………………….. 18,000

5 Cash ………………………………………………….. 6,254

Sales Revenue ($6,254 ÷ 1.06) ……… 5,900

Sales Taxes Payable

(b) Jan. 31 Interest Expense ………………………………… 75

Interest Payable

($18,000 X 5% X 1/12) ……………….. 75

PROBLEM 10-1A (Continued)

(c) Current liabilities

Notes payable ……………………………………………………….. $ 18,000*

Accounts payable ………………………………………………….. 42,500*

PROBLEM 10-2A

(a) Sept. 1 Inventory ……………………………………………. 12,000

Notes Payable ……………………………… 12,000

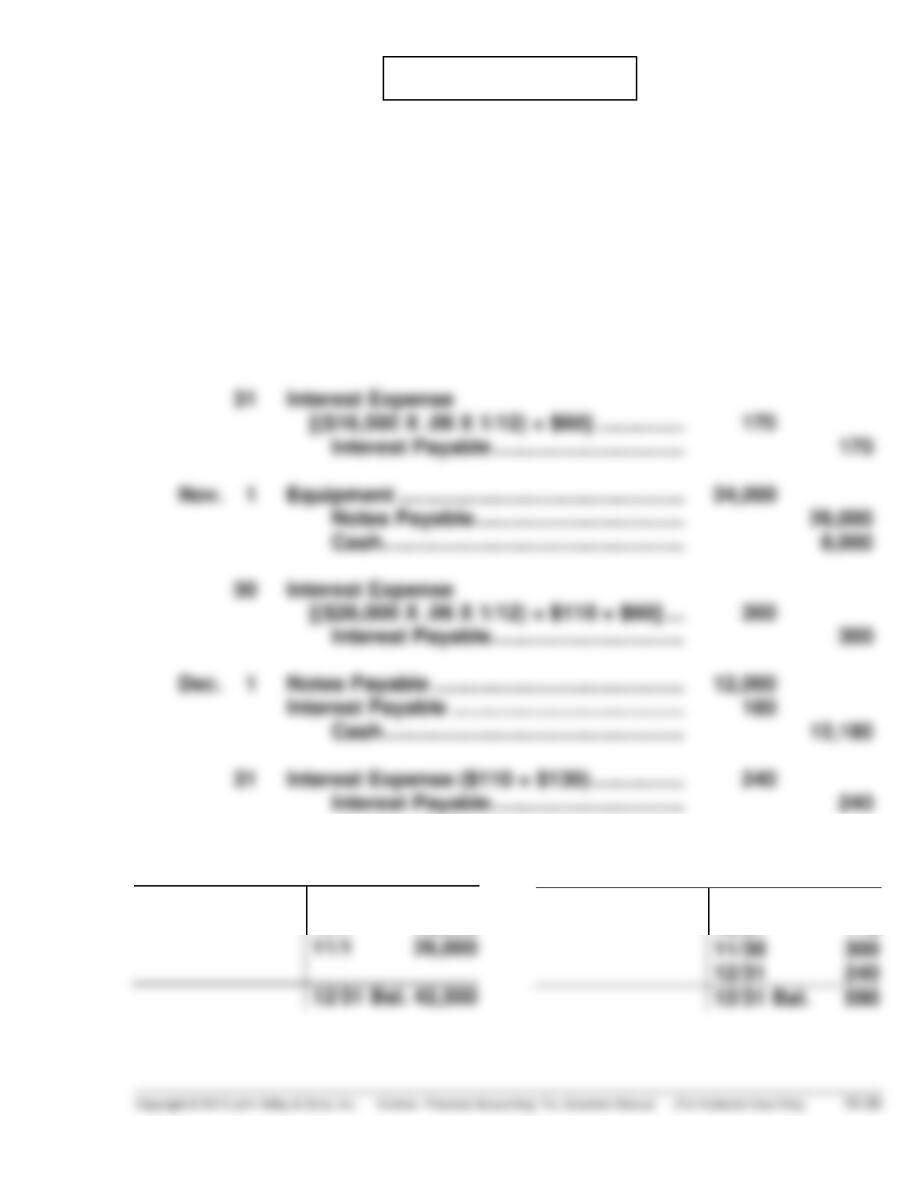

30 Interest Expense

($12,000 X .06 X 1/12) ………………………. 60

Interest Payable …………………………… 60

Oct. 1 Equipment …………………………………………. 16,500

Notes Payable ……………………………… 16,500

(b)

Notes Payable

12/1 12,000 9/1 12,000

10/1 16,500

Interest Payable

12/1 180 9/30 60

10/31 170

PROBLEM 10-2A (Continued)

Interest Expense

9/30 60

10/31 170

(c) Current liabilities

Notes payable ……………………………………………………………. 42,500

PROBLEM 10-3A

(a) Jan. 1 Interest Payable …………………………… 40,000

Cash …………………………………….. 40,000**

PROBLEM 10-4A

2013

(a) Oct. 1 Cash …………………………………………… 700,000

Bonds Payable …………………….. 700,000

2014

(d) Oct. 1 Interest Expense

($700,000 X 5% X 9/12) ……………… 26,250

Interest Payable ………………………….. 8,750

PROBLEM 10-5A

2014

(a) Jan. 1 Cash ($6,000,000 X 98%) ……………. 5,880,000

Discount on Bonds Payable ………. 120,000

PROBLEM 10-6A

(a)

2014 2013

1. Current ratio $2,893 ÷ $2,806

$4,443 ÷ $4,836

(b) The company’s position as measured through all ratios except the

current ratio has deteriorated. Southwest appears to be much less liquid

and solvent when comparing 2014 to 2013.