PROBLEMS: SET B

Problem 10-1B (LO 10-1 to 10-8)

Terms

__e___ 1. PE ratio.

__i___ 2. Stockholders’ equity section of the balance sheet.

__c___ 5. 100% stock dividend.

__j___ 7. Treasury stock.

__g___ 8. Value stocks.

__d___ 10. Retained earnings,

Definitions

a. A debit balance in retained earnings.

b. Priced high in relation to current earnings as investors expect future earnings

Problem 10-2B (LO 10-2, 10-3, 10-4, 10-5)

Requirement 1

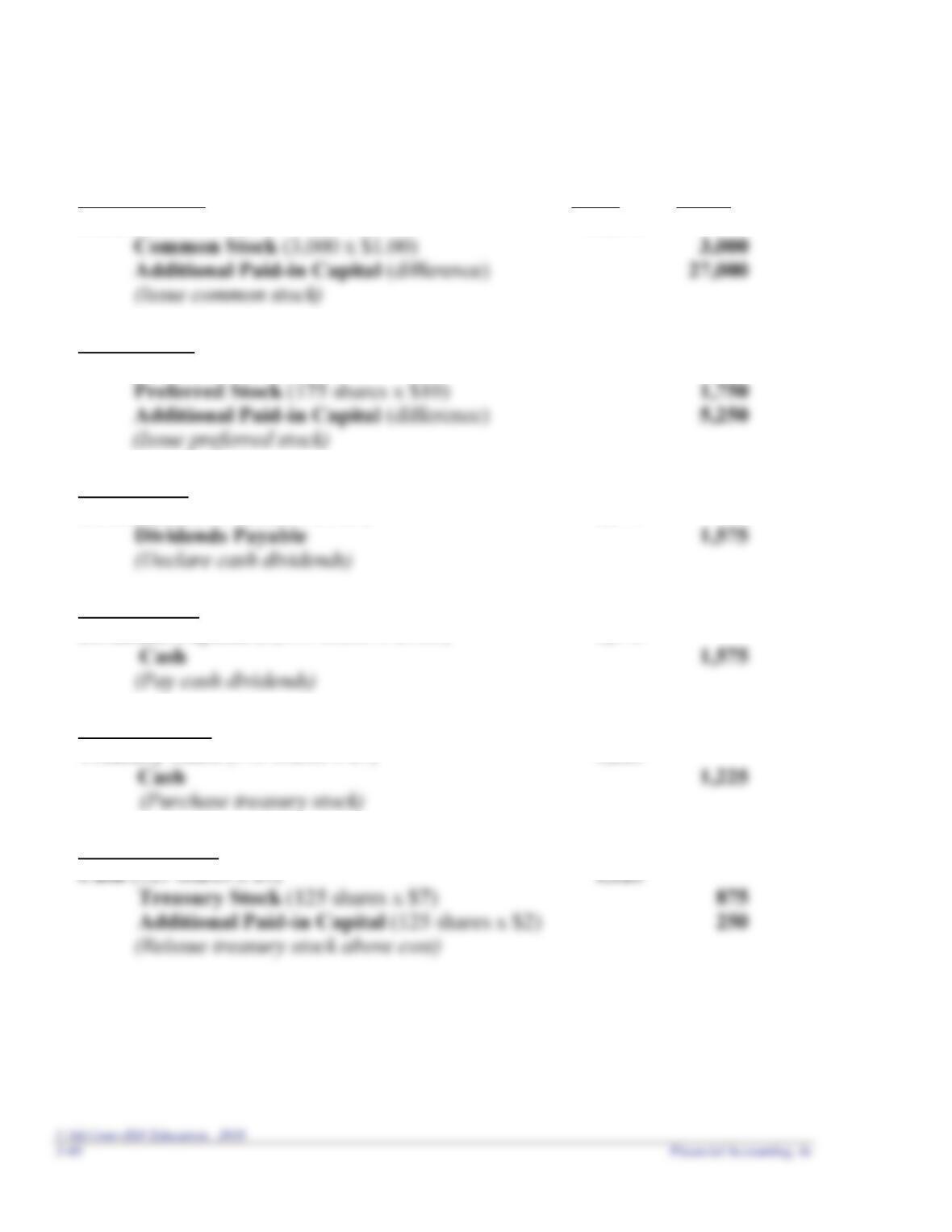

March 1, 2018

Debit

Credit

Cash (3,000 x $10)

30,000

April 1, 2018

Cash (175 shares x $40)

7,000

June 1, 2018

Dividends (6,300 shares x $0.25)

1,575

(Declare cash dividends)

June 30, 2018

Dividends Payable (6,300 shares x $0.25)

1,575

August 1, 2018

Treasury Stock (175 shares x $7)

1,225

October 1, 2018

Cash (125 shares x $9)

1,125

(Reissue treasury stock above cost)

Requirement 2

Transaction

Total

Assets

Total

Liabilities

Total

Stockholders’

Equity

Issue common stock

+

NE

+

Declare cash dividends

Pay cash dividends

NE

Reissue treasury stock

+

NE

+

Problem 10-3B (LO 10-6)

Before

After 100%

Stock Dividend

After 2-for-1

Stock Split

Common stock, $0.01 par value

$ 11

$ 22

$ 11

Additional paid-in capital

34,990

34,990

34,990

Retained earnings

Shares outstanding

Share price

Problem 10-4B (LO 10-7)

Requirement 1

Requirement 2

Requirement 3

Requirement 4

Retained earnings, beginning

$45,000,000

+ Net income

= Retained earnings, ending

Requirement 5

Problem 10-5B (LO 10-7)

Requirement 1

Nautical

Balance Sheet

(Stockholders’ Equity Section)

December 31, 2018

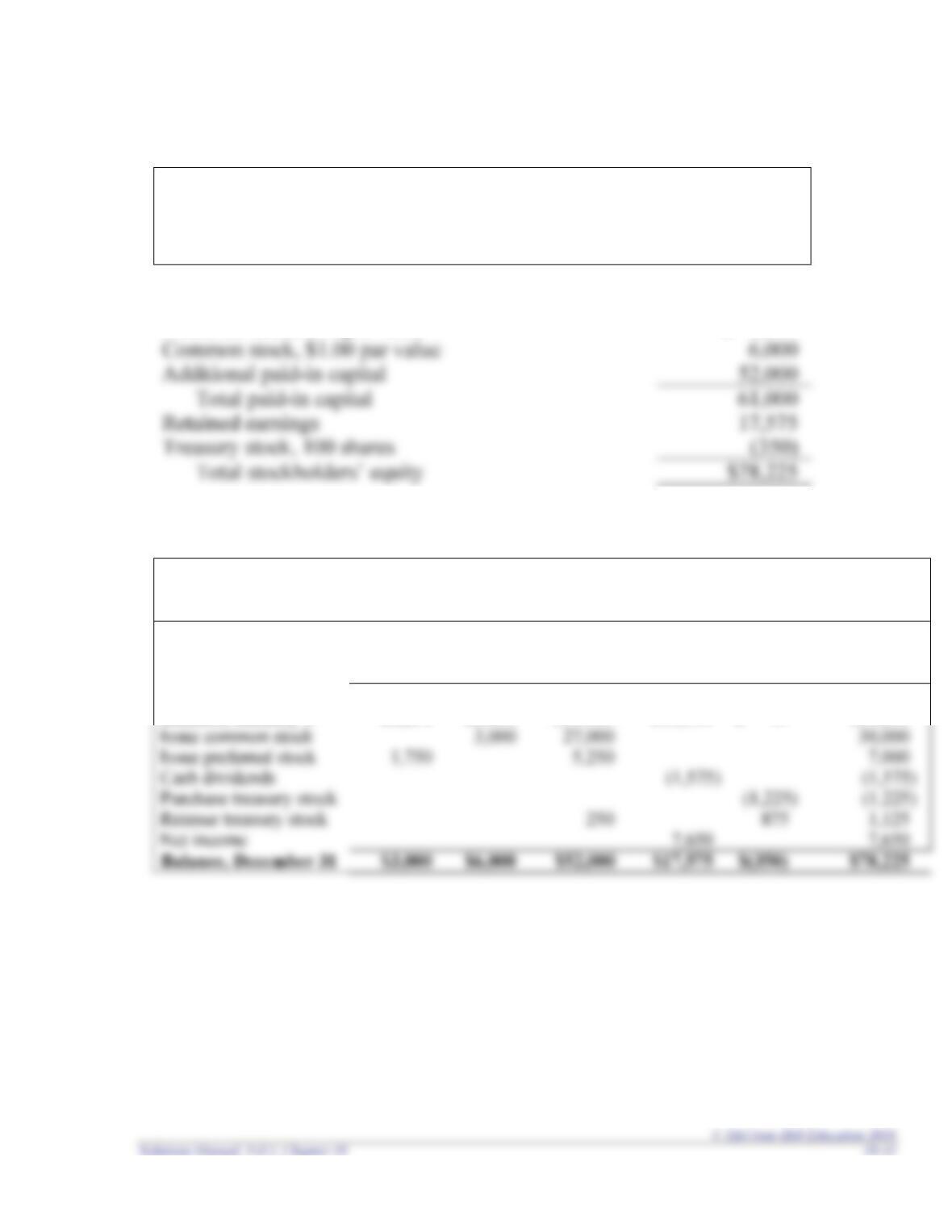

Stockholders’ equity:

Preferred stock, $10 par value

$ 3,000

Common stock, $1.00 par value

Additional paid-in capital

Retained earnings

Treasury stock, 100 shares

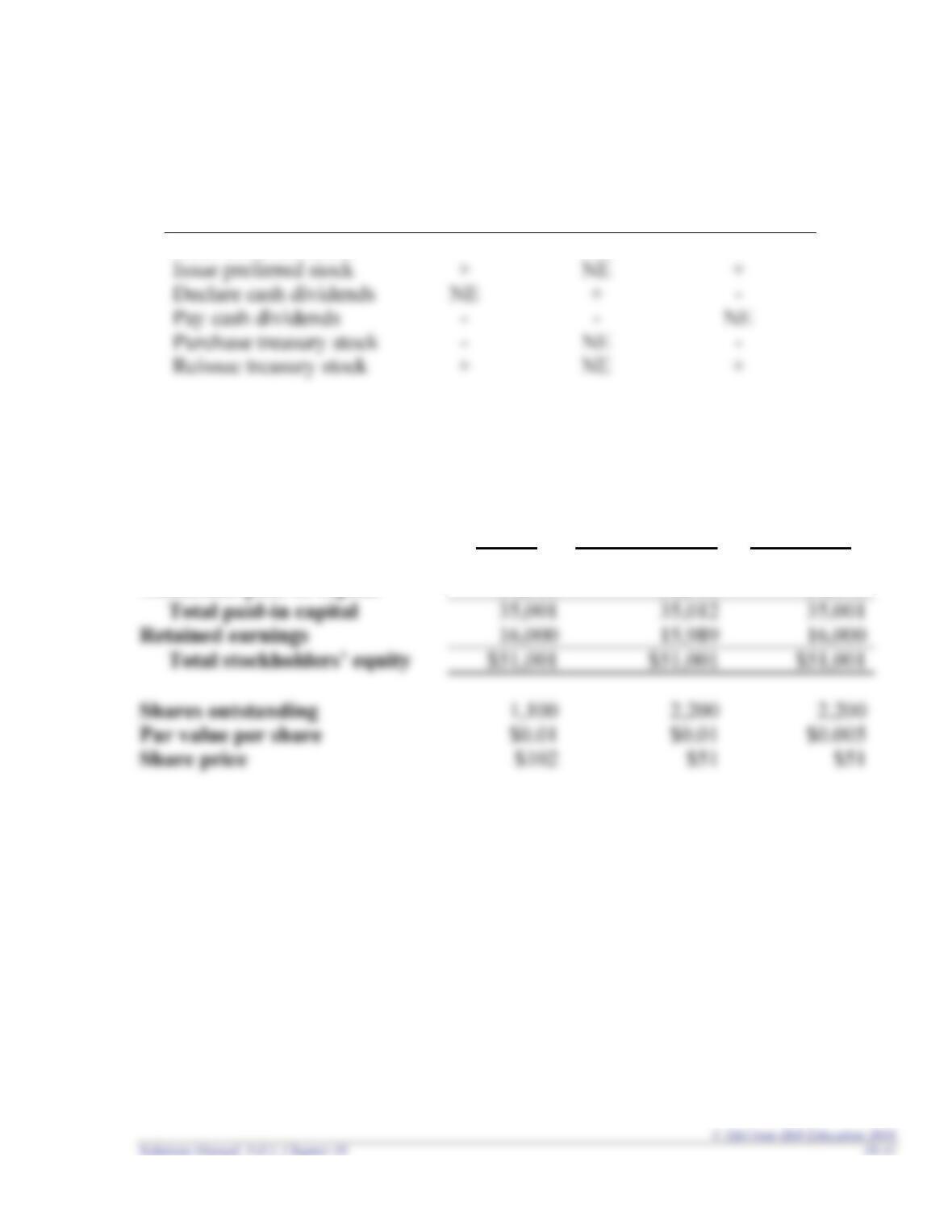

Requirement 2

Nautical

Statement of Stockholders’ Equity

For the Year Ended December 31, 2018

Preferred

Stock

Common

Stock

Additional

Paid-in

Capital

Retained

Earnings

Treasury

Stock

Total

Stockholders’

Equity

Balance, January 1

$1,250

$3,000

$19,500

$11,500

$ -0-

$35,250

Balance, December 31

Requirement 3

Items 1 and 2 are similar in that item 1 shows the equity balances in a column

format and item 2 shows these same balances across the bottom row. However,

Problem 10-6B (LO 10-2, 10-3, 10-4, 10-5, 10-7)

Requirement 1

February 2, 2018

Debit

Credit

Cash (1,500,000 x $35)

52,500,000

Common Stock (1,500,000 x $5)

7,500,000

Additional Paid-in Capital (difference)

February 4, 2018

Cash (600,000 x $23)

13,800,000

Preferred Stock (600,000 x $20)

Additional Paid-in Capital (difference)

June 15, 2018

Treasury Stock (150,000 shares x $30)

4,500,000

August 15, 2018

Cash (112,500 shares x $45)

Treasury Stock (112,500 shares x $30)

3,375,000

Additional Paid-in Capital (112,500 x $15)

November 1, 2018

Dividends (1,462,500 shares x $1.50) + $480,000)

2,673,750

November 30, 2018

Problem 10-6B (Continued)

Requirement 2

National League Gear

Balance Sheet

(Stockholders’ Equity Section)

December 31, 2018

Stockholders’ equity:

Preferred stock, $20 par value

$12,000,000

Common stock, $5 par value

7,500,000

Retained earnings*

Treasury stock, 37,500 shares

Problem 10-7B (LO 10-8)

Requirement 1

($ in millions)

Net

Income

÷

Average

Stockholders’ Equity

=

Return on

Equity

DC Menswear

$833

÷

($4,080 + 2,755) / 2

=

24.4%

Requirement 2

Dividends

Per Share

÷

Stock

Price

=

Dividend

Yield

DC Menswear

$1.00

÷

$18.93

=

5.3%

Requirement 3

($ in millions)

Stock Price

÷

Earnings Per Share

=

Price-Earnings

Ratio

DC Menswear

$18.93

÷

($833 / 485)

=

11.0

ADDITIONAL PERSPECTIVES

Continuing Problem: Great Adventures

AP10-1

Requirement 1

July 2, 2020

Debit

Credit

Cash (100,000 x $12)

1,200,000

Common Stock (100,000 x $1)

100,000

Additional Paid-in Capital (difference)

September 10, 2020

Treasury Stock (10,000 shares x $15)

November 15, 2020

Cash (5,000 shares x $16)

80,000

Treasury Stock (5,000 shares x $15)

75,000

December 1, 2020

Dividends

115,000

December 31, 2020

Dividends Payable

115,000

115,000

Requirement 2

Great Adventures, Inc.

Balance Sheet

(Stockholders’ Equity Section)

December 31, 2020

Stockholders’ equity:

Common stock, $1 par value

$ 120,000

Additional paid-in capital

Retained earnings*

Treasury stock, 5,000 shares

Financial Analysis: American Eagle

AP10-2

Requirement 1

$0.01 par value per share. The par value per share is listed in the stockholders’

Requirement 2

249,566,000 shares. The number of shares issued (in thousands) is listed in the

$0.01 par value.

Requirement 3

Yes, 55,050,000 shares. The number of shares of treasury stock (in thousands) is

Requirement 4

$99,585,000. The cash dividends paid (in thousands) is listed in the retained

Financial Analysis: Buckle

AP10-3

Requirement 1

$0.01 par value per share. The par value per share is listed in the stockholders’

Requirement 2

48,379,613 shares. The number of shares issued is listed in the stockholders’ equity

Requirement 3

No. There is no treasury stock reported in the stockholders’ equity section of the

Requirement 4

$176,604,000. The cash dividends paid (in thousands) is listed in the retained

Comparative Analysis: American Eagle vs. Buckle

AP10-4

Requirement 1

($ in thousands)

Net

Income

÷

Average

Stockholders’

Equity

=

Return on

Equity

American Eagle

$80,322

÷

$1,152,962*

=

7.0%

Requirement 2

Dividends Per Share

÷

Stock

Price

=

Dividend

Yield

American Eagle

$99,585,000 / 194,516,000*

÷

$14.04

=

3.6%

Buckle

÷

$50.79

=

Requirement 3

Stock

Price

÷

Earnings

Per Share*

=

Price-Earnings

Ratio

American Eagle

$14.04

÷

$0.42

=

33.4

Buckle

÷

=

14.0

Ethics

AP10-5

Answers regarding the allocation of the additional $5 million in operating cash flows

will vary. Other areas to spend the money, not specifically mentioned in the case,

include increasing employee benefits such as retirement and healthcare, investing in

Internet Research

AP10-6

This case provides an opportunity for students to learn more about Form 10-K,

Written Communication

AP10-7

Requirement 1

Requirement 2

The balance sheet has always distinguished between liabilities and stockholders’

equity. Financial accounting information is designed to provide information useful to

Requirement 3

Arguments in support of eliminating the distinction relate to the difficulty, in certain

cases, in distinguishing between liabilities and stockholders’ equity. For instance,

preferred stock can be structured so that it is nearly identical to common stock by

Requirement 4

Earnings Management

AP10-8

Requirement 1

Net Income

÷

Shares outstanding

=

Earnings

Per Share

Before Repurchase

$878,000

÷

950,000

=

$0.92

Net Income

÷

Average

Stockholders’ Equity

=

Return on

Equity

Before Repurchase

$878,000

÷

=

Requirement 2

Net Income

÷

Shares outstanding

=

Earnings

Per Share

After Repurchase

$878,000

÷

=

$0.98

Net Income

÷

Average

Stockholders’ Equity

=

Return on

Equity

After Repurchase

$878,000

÷

=

Requirement 3

The repurchase of stock near year-end improves earnings per share by reducing the

number of outstanding shares used to calculate earnings per share. It also improves the