10–41

PROBLEM 10-46 (50 MINUTES)

1.

a.

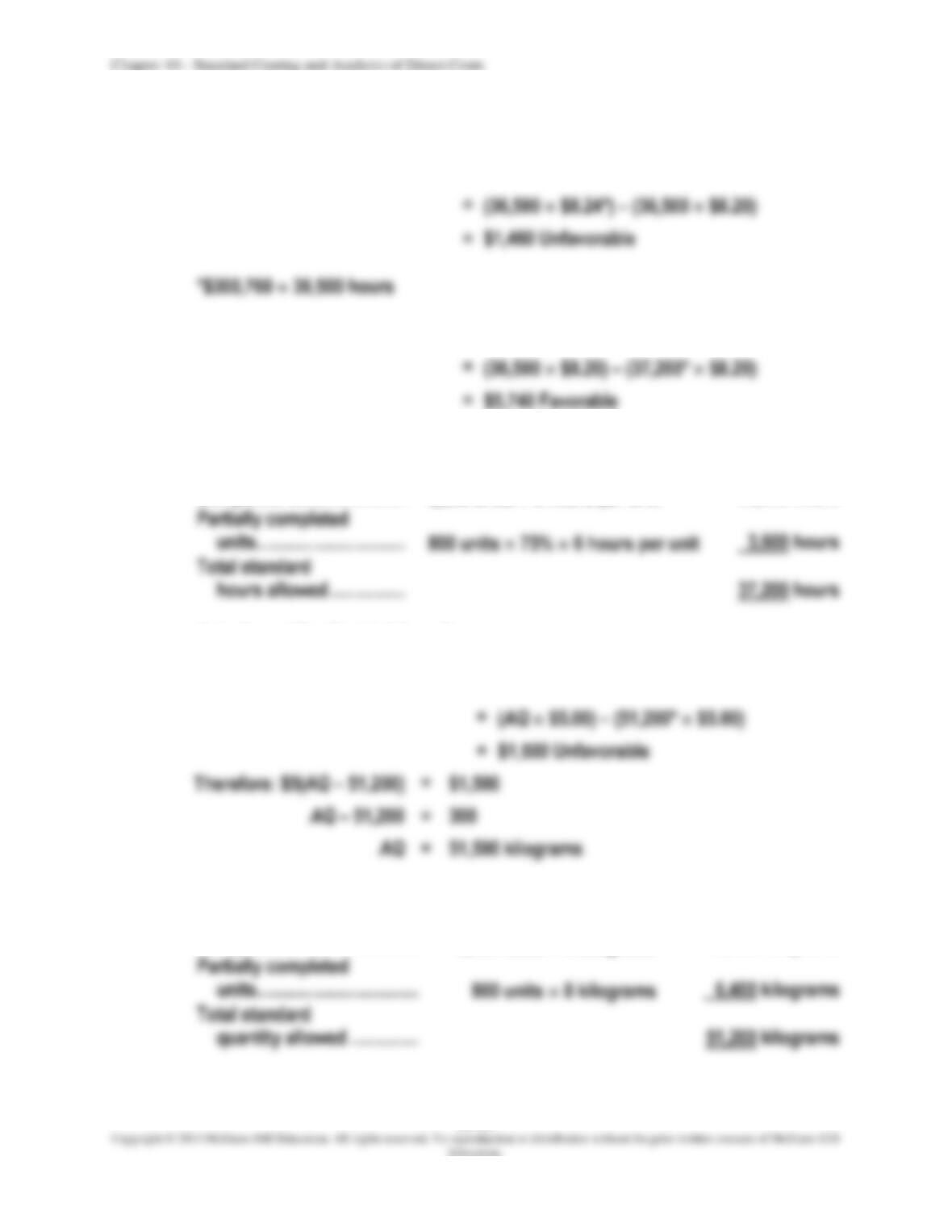

Direct-labor rate variance

=

(AH

AR) – (AH

SR)

=

$1,460 Unfavorable

*$300,760 36,500 hours

b.

Direct-labor efficiency variance

=

(AH

SR) – (SH

SR)

=

$5,740 Favorable

*Standard allowed direct-labor hours:

Completed units …………….

5,600 units 6 hours per unit

33,600 hours

hours allowed …………….

c.

Actual quantity of material used:

Direct-material quantity variance

=

(AQ

SP) – (SQ SP)

=

51,500 kilograms

*Standard quantity of material allowed:

Completed units ……………….

5,600 units 8 kilograms

44,800 kilograms

quantity allowed ……………

10–42

PROBLEM 10-46 (CONTINUED)

d.

=

$249,250/50,000

=

$4.985 per kilogram

Actual price paid per kilogram of direct material:

e.

Direct-material and direct-labor cost transferred to finished goods:

Direct-labor

Total cost transferred ………………………………

Direct-material

f.

Direct-material and direct-labor cost in September 30 balance of Work–in-Process

Inventory:

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–43

PROBLEM 10-46 (CONTINUED)

Raw-Material Inventory ………………………………………………..

Direct-Material Purchase Price Variance ……………..

Accounts Payable ………………………………………………

*Direct-material purchase price variance

=

PQ(AP – SP)

=

50,000($4.985 – $5.00) = $750 Favorable

To record the purchase of raw material and the direct-material purchase price

variance.

Direct-Material Quantity Variance …………………………………

Raw-Material Inventory ……………………………………….

To add the direct-material cost to work in process and record the direct-material

quantity variance.

Direct-Labor Rate Variance ………………………………………….

Direct-Labor Efficiency Variance …………………………

Wages Payable …………………………………………………..

To add the direct-labor cost to work-in-process, record the direct-labor rate and

efficiency variances, and recognize the actual direct-labor cost.

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–44

PROBLEM 10-47 (60 MINUTES)

1.

Standard cost schedule:

DIRECT MATERIAL

Construction

Department

Finishing

Department

Standard quantity

Direct material and parts in finished product:

Veneered wood …………………………………

7 lbs

Bridge and strings …………………………….

1 set

Allowance for normal waste …………………..

Total standard quantity per guitar ……………..

8 lbs

1 set

Standard price:

Direct material and parts:

Veneered wood …………………………………

Bridge and strings …………………………….

Standard direct-material cost:

Standard quantity ………………………………….

8 lbs

1 set

Standard cost per guitar ………………………..

Total standard cost of direct material

DIRECT LABOR

Construction

Department

Finishing

Department

Standard direct-labor cost:

Standard quantity ………………………………….

6 hrs

3 hrs

Standard cost per guitar ………………………..

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–45

PROBLEM 10-47 (CONTINUED)

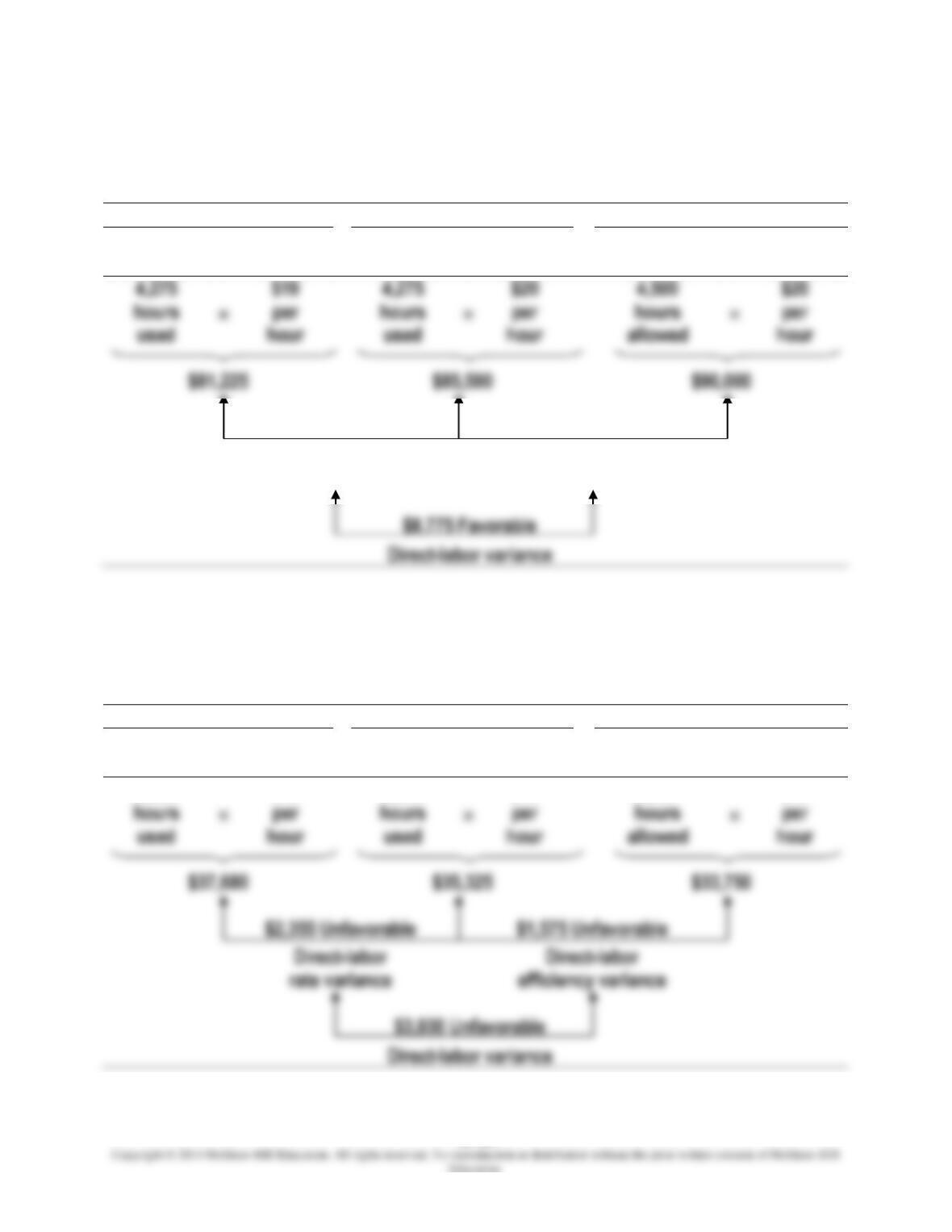

2.

(a)

Construction Department:

DIRECT-MATERIAL PRICE AND QUANTITY VARIANCES

ACTUAL MATERIAL COST

PROJ. MATERIAL COST

STANDARD MATERIAL COST

Actual

Quantity

Actual

Price

Actual

Quantity

Standard

Price

Standard

Quantity

Standard

Price

6,750

$12.50

6,750

$12.00

6,000

$12.00

$84,375

$81,000

$72,000

DIRECT-MATERIAL PURCHASE PRICE VARIANCE

ACTUAL MATERIAL COST

PROJ. MATERIAL COST

Actual

Quantity

Actual

Price

Actual

Quantity

Standard

Price

$12.50

$12.00

$112,500

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–46

PROBLEM 10-47 (CONTINUED)

DIRECT-LABOR RATE AND EFFICIENCY VARIANCES

ACTUAL LABOR COST

PROJ. LABOR COST

STANDARD LABOR COST

Actual

Hours

Actual

Rate

Actual

Hours

Standard

Rate

Standard

Hours

Standard

Rate

4,275

$19

4,275

$20

4,500

$20

$4,275 Favorable

$4,500 Favorable

Direct-labor

rate variance

Direct-labor

efficiency variance

(b)

Finishing Department:

DIRECT-LABOR RATE AND EFFICIENCY VARIANCES

ACTUAL LABOR COST

PROJ. LABOR COST

STANDARD LABOR COST

Actual

Hours

Actual

Rate

Actual

Hours

Standard

Rate

Standard

Hours

Standard

Rate

2,355

$16

2,355

$15

2,250

$15

10–47

PROBLEM 10-47 (CONTINUED)

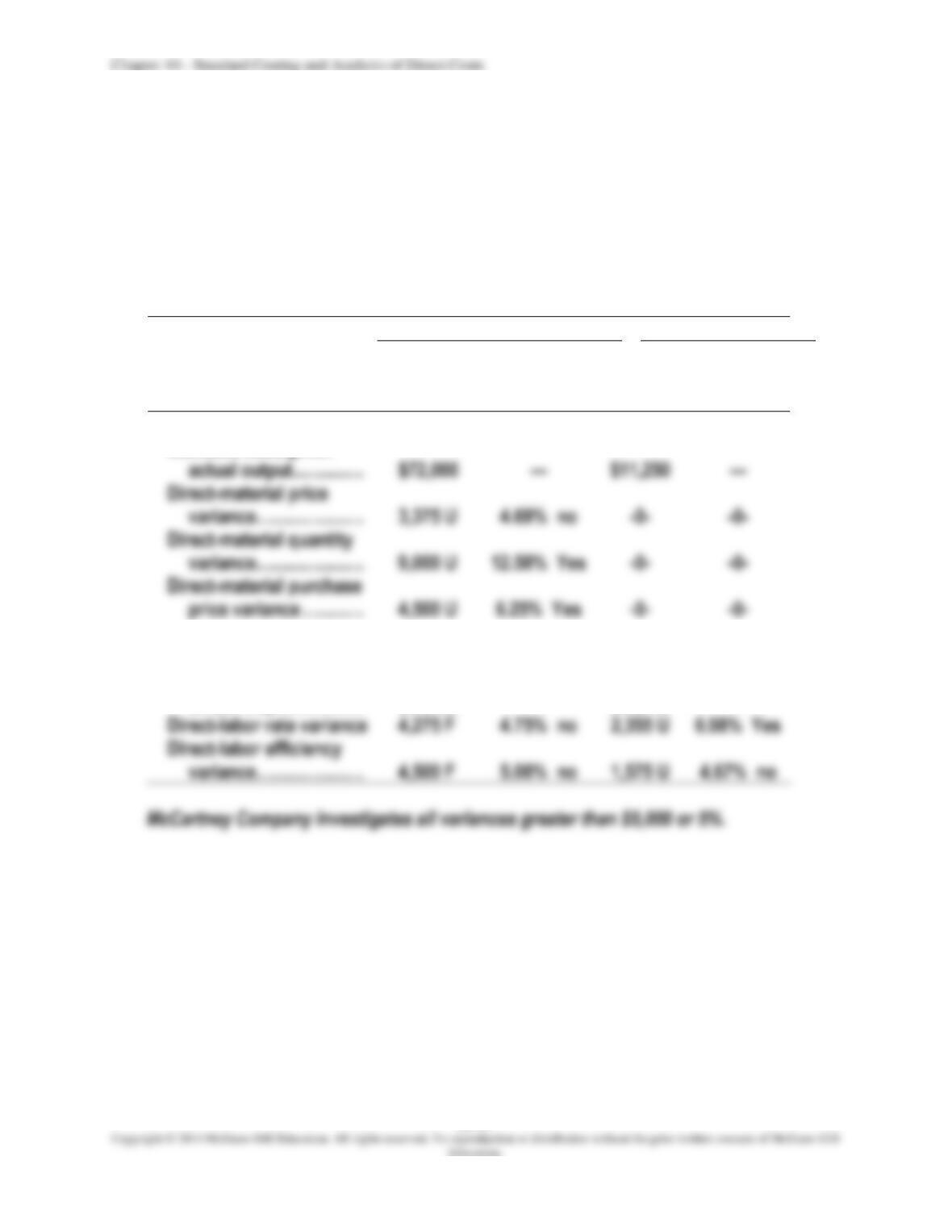

3.

Cost variance report:

MCCARTNEY COMPANY

COST VARIANCE REPORT

FOR THE MONTH OF JULY

Construction Dept

Finishing Dept

Amount

% of

Standard

Cost

Amount

% of

Standard

Cost

Direct material:

actual output ……………

$72,000

—

$11,250

—

Direct-material price

Standard cost, given

Direct labor:

Standard cost, given

actual output ……………

$90,000

—

$33,750

—

Direct-labor rate variance

4,275 F

Direct-labor efficiency

10–48

PROBLEM 10-48 (45 MINUTES)

1.

Journal entries:

Raw-Material Inventory ………………………………………………..

108,000

Direct-Material Purchase Price Variance ……………………….

Accounts Payable ………………………………………………

To record purchase of veneered wood.

Raw-Material Inventory ………………………………………………..

Accounts Payable ………………………………………………

To record purchase of bridges and strings.

Direct-Material Quantity Variance …………………………………

Raw-material Inventory ………………………………………

To record usage of veneered wood.

Raw-Material Inventory ……………………………………….

To record usage of bridges and strings.

Direct-Labor Rate Variance …………………………..…….

Direct-Labor Efficiency Variance …………………………

Wages Payable …………………………………………………..

To record Construction Department direct-labor costs and variances.

Direct-Labor Rate Variance ………………………………………….

Direct-Labor Efficiency Variance ………………………………….

Wages Payable …………………………………………………..

To record Finishing Department direct-labor costs and variances.

10–49

PROBLEM 10-48 (CONTINUED)

Finished-Goods Inventory …………………………..……………….

207,000

Work-in-Process Inventory …………………………………

To record completion of 750 guitars at a standard cost of $276 each

($276 = $96 + $15 + $120 + $45).

Accounts Receivable …………………………………………………..

175,500

Sales Revenue……………………………………………………

Cost of Goods Sold

124,200

Finished-Goods Inventory …………………………………..

Cost of Goods Sold ……………………………………………………..

8,655

Direct-Labor Rate Variance ………………………………………….

Direct-Labor Efficiency Variance ………………………………….

Direct-Material Purchase Price Variance ……………..

Direct-Material Quantity Variance ………………………..

To close variances into Cost of Goods Sold.

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–50

PROBLEM 10-48 (CONTINUED)

2.

Posting of journal entries:

Raw-Material Inventory

Accounts Receivable

108,000

81,000

175,500

13,500

11,250

72,000

207,000

112,500

11,250

90,000

33,750

Wages Payable

207,000

124,200

81,225

37,680

Cost of Goods Sold

Sales Revenue

124,200

175,500

8,655

Direct-Material Purchase

Price Variance

Direct-Labor Rate Variance

4,500

4,500

4,275

9,000

4,500

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–51

SOLUTIONS TO CASES

CASE 10-49 (60 MINUTES)

1.

Standard cost of lots N42, N43, and N44:

METRO FASHIONS, INC.

STANDARD COST OF PRODUCTION

FOR NOVEMBER

Lot

Quantity

(boxes)

Standard

Cost per

Box

Total

Standard

Cost

N42 ………………………………………………………..

2,000

$106.50

$213,000

N43 ………………………………………………………..

3,400

N44 ………………………………………………………..

2,400

$26.40 + (80%)($44.10 + $36.00).

2.

Variances (U denotes unfavorable; F denotes favorable):

a.

METRO FASHIONS, INC.

DIRECT-MATERIAL PURCHASE PRICE VARIANCE

FOR NOVEMBER

Actual cost of materials purchased ………………………………………………….

Direct-material purchase price variance …………………………………………..

10–52

CASE 10-49 (CONTINUED)

b.

METRO FASHIONS, INC.

DIRECT-MATERIAL QUANTITY VARIANCES

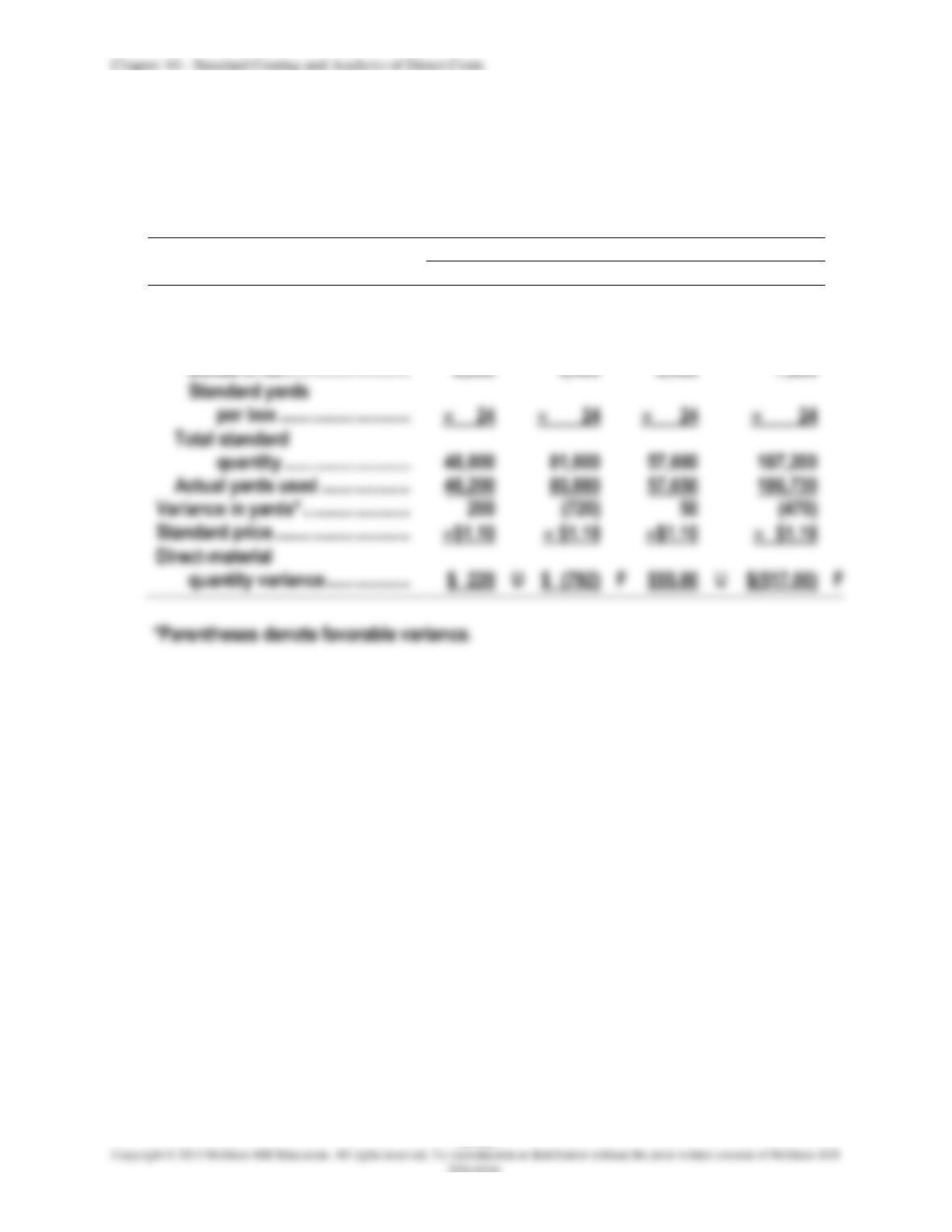

FOR NOVEMBER

Lot no.

N42

N43

N44

Total

Direct-material quantity

variance:

Standard yards:

Boxes in lot ………………………

3,400

Total standard

quantity ………………………

Actual yards used ……………….

Variance in yards* …………………..

(720)

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–53

CASE 10-49 (CONTINUED)

c. and d.

METRO FASHIONS, INC.

DIRECT-LABOR VARIANCES

FOR NOVEMBER

Lot no.

N42

N43

N44

Total

Direct-labor efficiency variance:

Standard hours:

Boxes in lot ……………………….

2,000

3,400

2,400

Total ………………………………….

6,000

10,200

7,200

Total standard hours ………….

6,000

10,200

5,760

21,960

Actual hours worked …………..

5,960

10,260

5,780

22,000

Variance in hours* ………………….

Standard hours

Lot no.

N42

N43

N44

Total

Direct-labor rate variance:

Actual hours worked ………….

5,960

10,260

5,780

22,000

Rate paid in excess of standard

CASE 10-49 (CONTINUED)

3.

Journal entries:

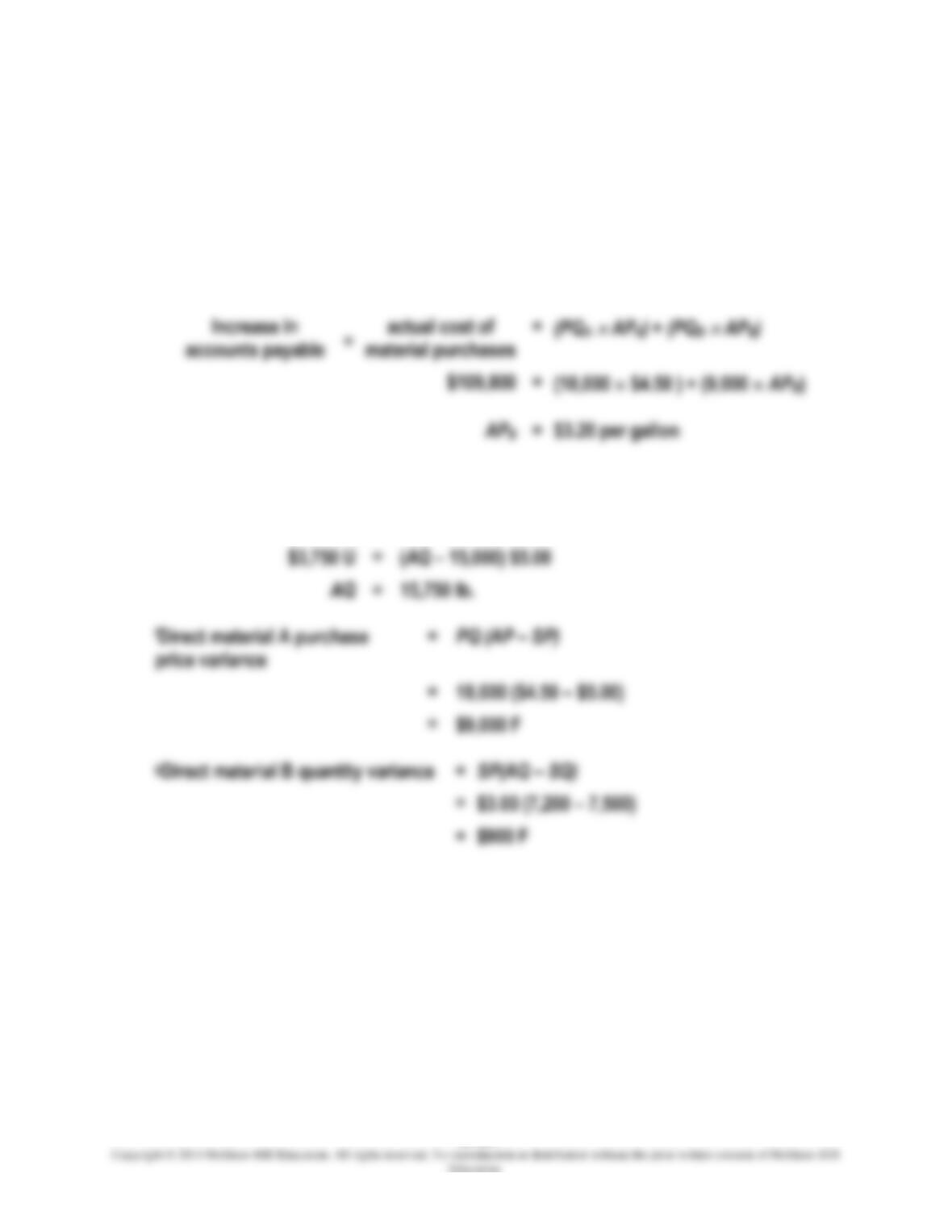

Raw-material Inventory ………………………………………………..

209,000*

Direct-Material Purchase Price Variance ……………………….

Accounts Payable ………………………………………………

To record the purchase of raw material.

Work-in-Process Inventory …………………………………………..

205,920*

Direct-Material Quantity Variance ………………………..

Raw-Material Inventory ……………………………………….

To add direct-material cost to work-in-process inventory and record the direct-material

quantity variance.

Work-in-Process Inventory …………………………………………..

322,812*

Direct-Labor Rate Variance ………………………………………….

Direct-Labor Efficiency Variance ………………………………….

Wages Payable …………………………………………………..

10–55

CASE 10-50 (75 MINUTES)

The completed list is shown below. Begin by filling in the facts you know. The reasoning

used to reduce the remaining data is explained after the list of answers.

1.

Actual output (in drums)

=

drum per Amaterialdirect of quanity standard

output actual given allowed, Amaterialdirect of quantity standard

2.

Direct material

A

B

a.

Standard quantity per drum ………………………………….

10 lb.

5 gal.a

b.

Standard price …………………………………………………….

$5.00/lb.

$3.00/gal.b

c.

Standard cost per drum ……………………………………….

$50.00c

$15.00

d.

Standard quantity allowed, given actual output …….

15,000 lb.

7,500 gal.

e.

Actual quantity purchased ……………………………………

18,000 lb.

9,000 gal.

Actual price …………………………………………………………

$4.50/lb.

$3.20/gal.d

h.

Purchase price variance ………………………………………

$9,000 Ff

$1,800 U

Quantity variance ………………………………………………..

$3,750 U

$900 Fg

aStandard quantity of direct material B per drum

=

output actual

output actual given allowed, B materialdirect of quantity standard

bStandard price of direct material B

=

drum per allowed quantity standard

drum per B material ofcost standard

=

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–56

CASE 10-50 (CONTINUED)

cStandard cost of direct material A per drum = 10 lbs. $5.00 per lb. = $50.00.

dThe reasoning for the actual price of direct material B is as follows, where the

subscripts denote materials A and B:

=

$3.20 per gallon

eThis conclusion comes from the following formula for the quantity variance:

Quantity variance (A)

=

SP(AQ – SQ)

=

15,750 lb.

=

$9,000 F

=

$900 F

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–57

CASE 10-50 (CONTINUED)

3.

Direct labor:

I

(mixers)

II

(packers)

a.

Standard hours per drum ……………………………………..

2 hr.a

4 hr.

b.

Standard rate per hour …………………………………………

$15.00

$12.00b

c.

Standard cost per drum ………………………………………..

$30.00

$48.00

d.

Standard quantity allowed, given actual output ……..

3,000 hr.c

6,000 hr.d

e.

Actual rate per hour ……………………………………………..

$15.30i

$11.90

Actual hours ………………………………………………………..

3,000 hrh

6,150 hr.e

g.

Rate variance ……………………………………………………….

$900 U

$615 Ff

h.

Efficiency variance……………………………………………….

-0-g

$1,800 U

aStandard hours of direct labor type I per drum

=

hour per rate standard

drum per I labordirect ofcost standard

=

bDirect labor type II, standard rate per hour

=

drum per hours standard

drum per II typelabordirect ofcost standard

=

cDirect labor type I, standard quantity allowed, given actual output

=

3,000 hr.

dDirect labor type II, standard quantity allowed given actual output

=

6,000 hr.

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–58

CASE 10-50 (CONTINUED)

eDirect labor type II, actual hours = 6,150 hr. Use the formula for the direct-labor

efficiency variance, as follows:

Direct-labor (II) efficiency variance

=

SR (AH – SH)

=

$12.00 (AH – 6,000)

gDirect labor type I, efficiency variance = zero.

iDirect labor type I, actual rate per hour = $15.30. Use the formula for the direct-labor

=

3,000 (AR – $15.00)

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–59

CASE 10-50 (CONTINUED)

Now fill in the remaining variances in the following tabulation:

Direct-material variances:

A:

Purchase price variance …………………………………………………………..

$9,000

F

A:

Quantity variance …………………………………………………………………….

U

B:

Purchase price variance …………………………………………………………..

U

B:

Quantity variance …………………………………………………………………….

F

Direct-labor variances:

Rate variance …………………………………………………………………………..

U

Efficiency variance …………………………………………………………………..

Rate variance …………………………………………………………………………..

F

Efficiency variance …………………………………………………………………..

U

Total (favorable variance because of credit to cost of Goods Sold) ……..

$2,265

F

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–60

FOCUS ON ETHICS (See page 431 in the text.)

Was sacrificing quality to cut standards ethical in this situation?

Smith did not act ethically when he ordered wood of an inferior quality as he knew that

his actions would harm customers (through provision of inferior products) and the

company (both through product replacement costs and through damage to its