EXERCISE 10-10 (Continued)

(c) Cash ………………………………………………………………… 11,000

Accumulated Depreciation—Equipment ……………… 36,000

Loss on Disposal of Plant Assets ………………………. 18,000

Equipment ………………………………………………….. 65,000

EXERCISE 10-11

(a) Dec. 31 Inventory …………………………..………………. 80,000

Accumulated Depletion

(100,000 X $.80) ……………………….. 80,000

Cost (a) $720,000

Units estimated (b) 900,000 tons

Depletion cost per unit [(a) ÷ (b)] $0.80

EXERCISE 10-12

Dec. 31 Amortization Expense ……………………………. 10,000

Patents ($75,000 ÷ 5 X 8/12) ……………… 10,000

EXERCISE 10-13

1/2/17 Patents …………………………………………………. 595,000

Cash ……………………………………………… 595,000

4/1/17 Goodwill …………………………..…………………… 360,000

Cash ……………………………………………… 360,000

Ending balances, 12/31/17:

Patents = $510,000 ($595,000 – $85,000).

EXERCISE 10-14

*EXERCISE 10-15

(a) Equipment (new) ……………………………………………….. 55,000

Accumulated Depreciation—Equipment (old) ……… 22,000

Loss on Disposal of Plant Assets ………………………. 4,000

Equipment (old) ………………………………………….. 64,000

Cash ………………………………………………………….. 17,000

(b) Equipment (new) ……………………………………………….. 14,000

Accumulated Depreciation—Equipment (old) ……… 4,000

Gain on Disposal of Plant Assets ………………… 3,000

Equipment (old) ………………………………………….. 12,000

Cash ………………………………………………………….. 3,000

*EXERCISE 10-16

(a) Equipment (new) ………………………………………………. 3,000

Loss on Disposal of Plant Assets ………………………. 4,000

Accumulated Depreciation—Equipment (old) …….. 15,000

Equipment (old) …………………………………………. 22,000

(b) Equipment (new) ………………………………………………. 3,000

Accumulated Depreciation—Equipment (old) …….. 8,000

Equipment (old) …………………………………………. 10,000

Gain on Disposal of Plant Assets ……………….. 1,000

SOLUTIONS TO PROBLEMS

PROBLEM 10-1A

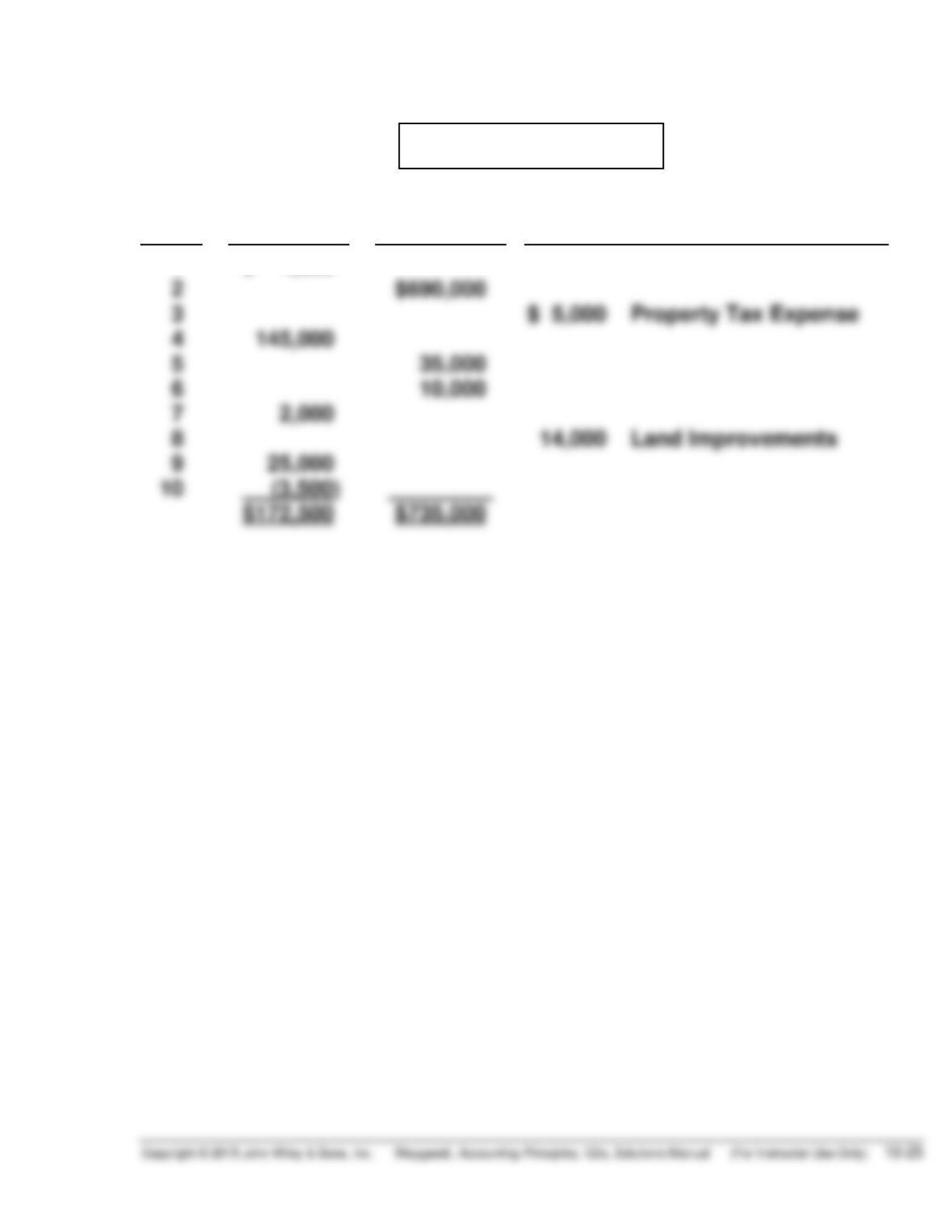

Item

Land

Buildings

Other Accounts

1

2

3

4

($ 4,000)

( 145,000)

$690,000

$ 5,000 Property Tax Expense

PROBLEM 10-2A

(a)

Year

Computation

Accumulated

Depreciation

12/31

BUS 1

2015

2016

2017

$ 90,000 X 20% = $18,000

$ 90,000 X 20% = $18,000

$ 90,000 X 20% = $18,000

$18,000

36,000

54,000

2015

$55,000

BUS 3

(b)

Year

Computation

Expense

BUS 2

(1)

2015

$110,000 X 50% X 9/12 = $41,250

$41,250

PROBLEM 10-3A

(a) (1) Purchase price ……………………………………………………….. $ 48,000

Sales tax ………………………………………………………………… 1,700

Shipping costs ……………………………………………………….. 150

Insurance during shipping ………………………………………. 80

(2) Recorded cost ………………………………………………………… $ 50,000

Less: Salvage value ……………………………………………….. 5,000

(b) (1) Recorded cost ………………………………………………………… 180,000

Less: Salvage value ……………………………………………….. 10,000

(2)

Book Value at

Beginning

of Year

DDB

Rate

Annual Depreciation

Expense

Accumulated

Depreciation

$180,000

90,000

*50%*

*50%*

$90,000

45,000

$ 90,000

135,000

PROBLEM 10-3A (Continued)

(3) Depreciation cost per unit = ($180,000 – $10,000)/125,000 units =

$1.36 per unit.

Annual Depreciation Expense

2017: $1.36 X 45,000 = $61,200

(c) The declining-balance method reports the highest amount of depreciation

expense the first year while the straight-line method reports the lowest.

In the fourth year, the straight-line method reports the highest amount of

depreciation expense while the declining-balance method reports the

lowest.

PROBLEM 10-4A

Year

Depreciation

Expense

Accumulated

Depreciation

2015

2016

(b)$18,000(a)

18,000

$18,000

36,000

(a)

$120,000 – $12,000

6 years

= $18,000

PROBLEM 10-5A

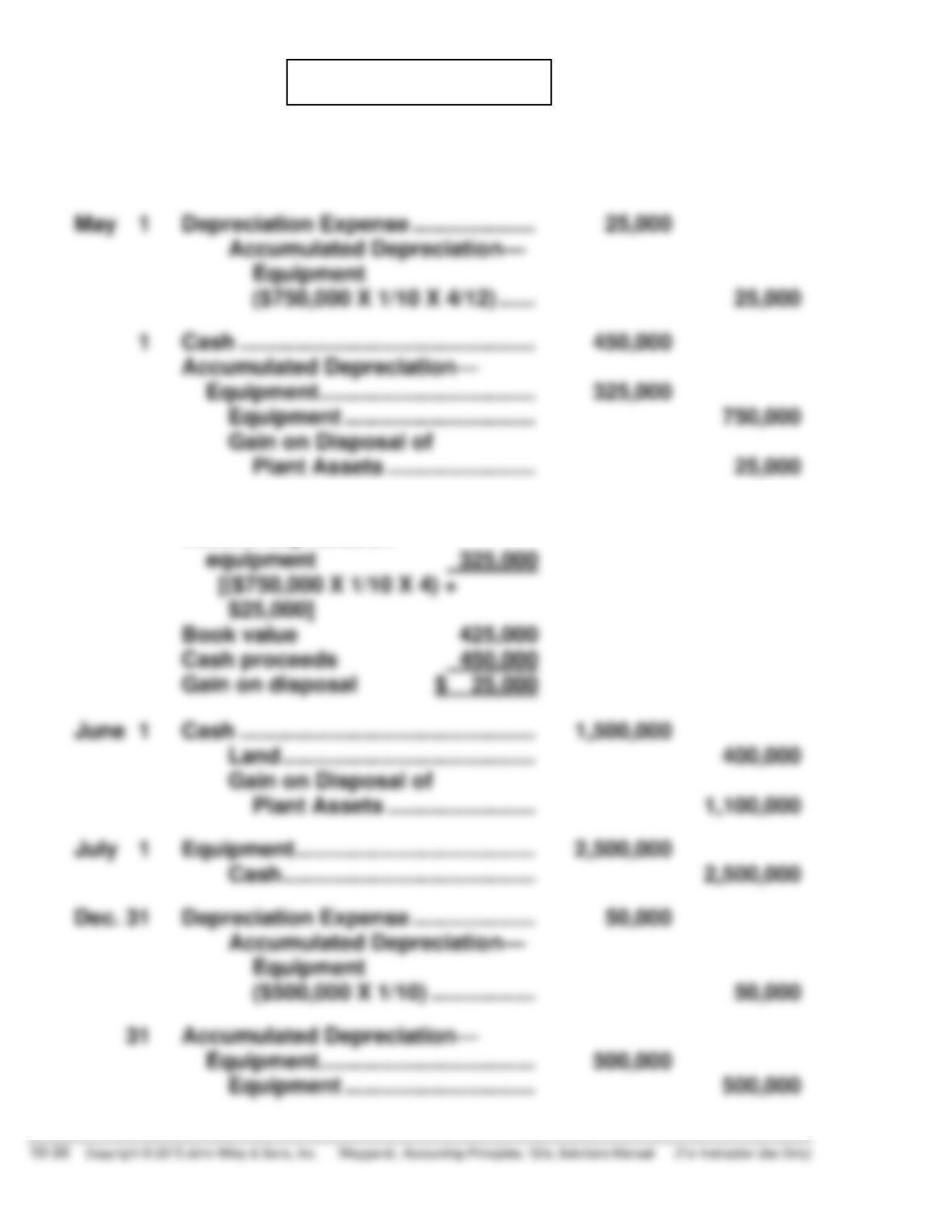

(a) Apr. 1 Land…………………………………………. 2,130,000

Cash ………………………………….. 2,130,000

Cost $750,000

Accum. depreciation—

equipment 325,000

[($750,000 X 1/10 X 4) +

$25,000]

Book value 425,000

Cash proceeds 450,000

Gain on disposal $ 25,000

PROBLEM 10-5A (Continued)

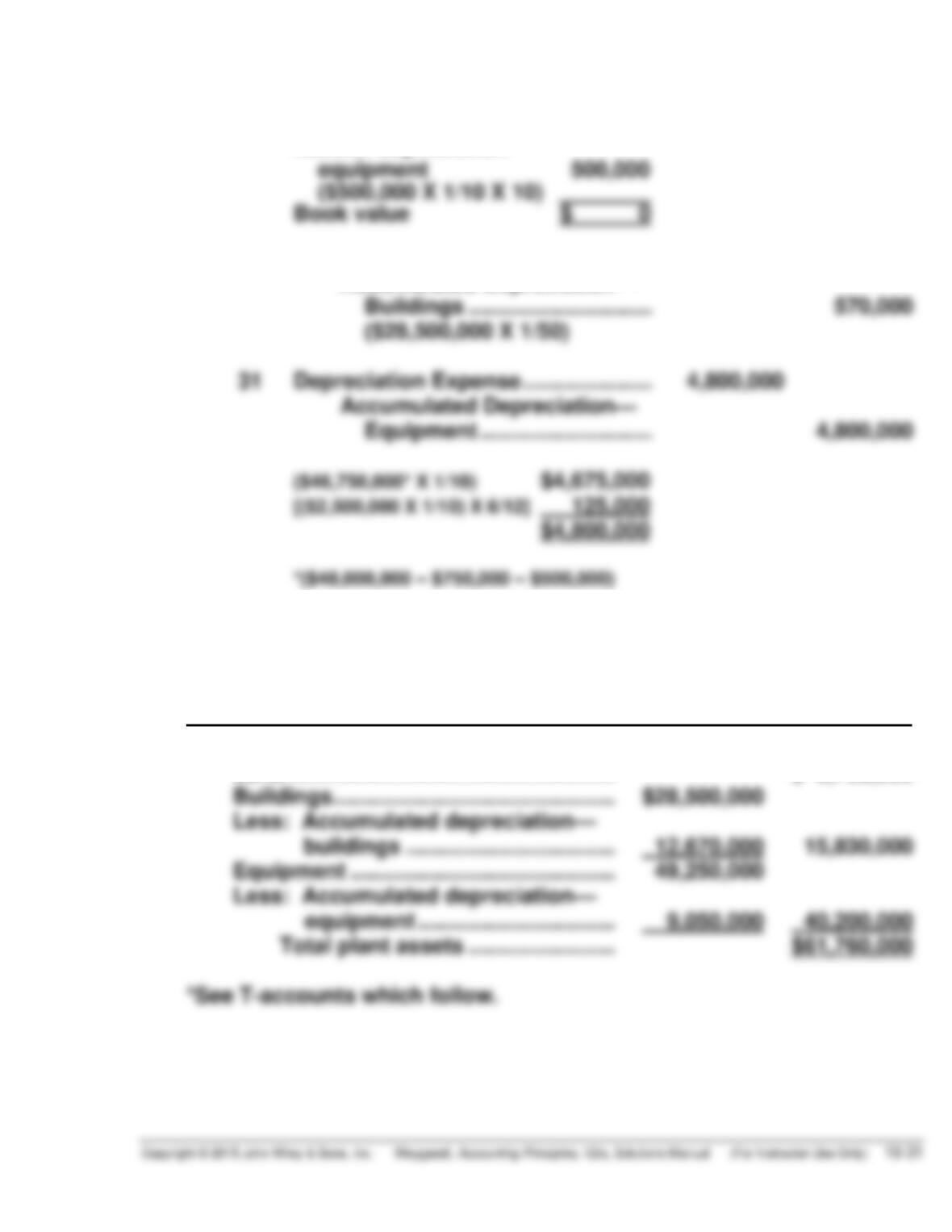

Cost $500,000

Accum. depreciation—

(b) Dec. 31 Depreciation Expense ………………… 570,000

Accumulated Depreciation—

Buildings ………………………… 570,000

($28,500,000 X 1/50)

(c) GRAND COMPANY

Partial Balance Sheet

December 31, 2018

Plant Assets*

Land …………………………………………….. $ 5,730,000

Buildings ………………………………………. $28,500,000

Less: Accumulated depreciation—

PROBLEM 10-5A (Continued)

Land

Bal. 5,730,000

Bal. 4,000,000

June 1 400,000

Buildings

Bal. 28,500,000

Bal. 28,500,000

Accumulated Depreciation—Buildings

Bal. 12,670,000

Bal. 12,100,000

Equipment

Bal. 49,250,000

Bal. 48,000,000

May 1 750,000

Accumulated Depreciation—Equipment

May 1 325,000

Dec. 31 500,000

Bal. 9,050,000

Bal. 5,000,000

May 1 25,000

PROBLEM 10-6A

(a) Accumulated Depreciation—Equipment ……………… 50,000

Loss on Disposal of Plant Assets ………………………. 30,000

Equipment …………………………………………………. 80,000

PROBLEM 10-7A

(a) Jan. 2 Patents …………………………..………………… 27,000

Cash ………………………………………….. 27,000

(b) Dec. 31 Amortization Expense ……………………….. 10,000

Patents ………………………………………. 10,000

[($70,000 X 1/10) + ($27,000 X 1/9)]

(c) Intangible Assets

Patents ($97,000 cost – $17,000 amortization) (1) …………… $ 80,000

PROBLEM 10-8A

1. Research and Development Expense ………………. 136,000

Patents …………………………..……………………….. 136,000

PROBLEM 10-9A

(a)

LaPorta

Lott

Asset turnover

$1,300,000

$1,180,000

CHAPTER 10 COMPREHENSIVE PROBLEM SOLUTION

(a) 1. Equipment …………………………………………………… 22,800

Cash ……………………………………………………….. 22,800

2. Depreciation Expense …………………………………… 450

Accumulated Depreciation—Equipment ……. 450

3. Accounts Receivable ……………………………………. 9,000

Sales Revenue …………………………………………. 9,000

Cost of Goods Sold …………………………..………….. 6,300

Inventory …………………………………………………. 6,300

6. Insurance Expense ($3,600 X 4/6) ………………….. 2,400

Prepaid Insurance ……………………………………. 2,400

7. Depreciation Expense …………………………………… 4,000

Accumulated Depreciation—Buildings ……… 4,000