1. a. Property, plant, and equipment or fixed assets

b. Current assets (inventory)

2. Undeveloped land acquired for future resale rather than operations is classified and reported as

an investment, below the Current Assets section.

6. a. The straight-line depreciation method is most appropriate when the revenues generated

b

y the asset are about the same from period to period.

b. The units-of-activity depreciation method is most appropriate when the asset’s use (and

revenues) vary from period to period.

c. The double-declining-balance depreciation method is most appropriate when the revenues

generated by the asset are greater in the early periods of use rather than in later periods.

7. Capital expenditures include the cost of acquiring fixed assets and the cost of improving an

asset. These costs are recorded by increasing (debiting) a fixed asset account. Capital

expenditures also include the costs of extraordinary repairs, which are recorded by decreasing

(debiting) the asset’s accumulated depreciation account. Revenue expenditures are recorded as

expenses and are costs that benefit only the current period and are incurred for normal

maintenance and repairs of fixed assets.

8. Capital expenditure

CHAPTER 10

LONG-TERM ASSETS: FIXED AND INTANGIBLE

DISCUSSION QUESTIONS

CHAPTER 10 Long-Term Assets: Fixed and Intangible

PE 10-1A

a. $1,290,000 ($1,630,000 – $340,000)

b. 10% (100% ÷ 10)

c. $129,000 ($1,290,000 × 10%) or ($1,290,000 ÷ 10 years)

PE 10-2A

a. $184,800 ($202,800 – $18,000)

b. $0.42 per mile ($184,800 ÷ 440,000 miles)

c. $47,460 (113,000 miles × $0.42)

PE 10-2B

PE 10-3A

a. 5% [(100% ÷ 40) × 2]

b. $59,650 ($1,193,000 × 5%)

PE 10-3B

PE 10-4A

a. $16,400 [($304,000 – $41,600) ÷ 16]

b. $140,000 [$304,000 – ($16,400 × 10)]

c. $15,400 [($140,000 – $16,800) ÷ 8]

PE 10-4B

PRACTICE EXERCISES

CHAPTER 10 Long-Term Assets: Fixed and Intangible

PE 10-5A

14 Accumulated Depreciation—Delivery Van 4,700

Cash 4,700

14 Delivery Van 920

Cash 920

PE 10-5B

Aug. 7 Delivery Truck 2,800

PE 10-6A

a. $35,000 = $280,000 × [(100% ÷ 16) × 2] = $280,000 × 12.5%

b. $16,025 gain, computed as follows:

c. Cash 230,400

Accumulated Depreciation—Equipment 65,625

Equipment 280,000

Gain on Sale of Equipment 16,025

PE 10-6B

a. $28,900 [($287,100 – $27,000) ÷ 9]

b. $3,900 loss {$138,700 – [$287,100 – ($28,900 × 5)]}

Feb.

CHAPTER 10 Long-Term Assets: Fixed and Intangible

PE 10-7A

a. $1.12 per ton = $342,720,000 ÷ 306,000,000 tons

b. $62,272,000 = 55,600,000 tons × $1.12 per ton

c. 31 Depletion Expense 62,272,000

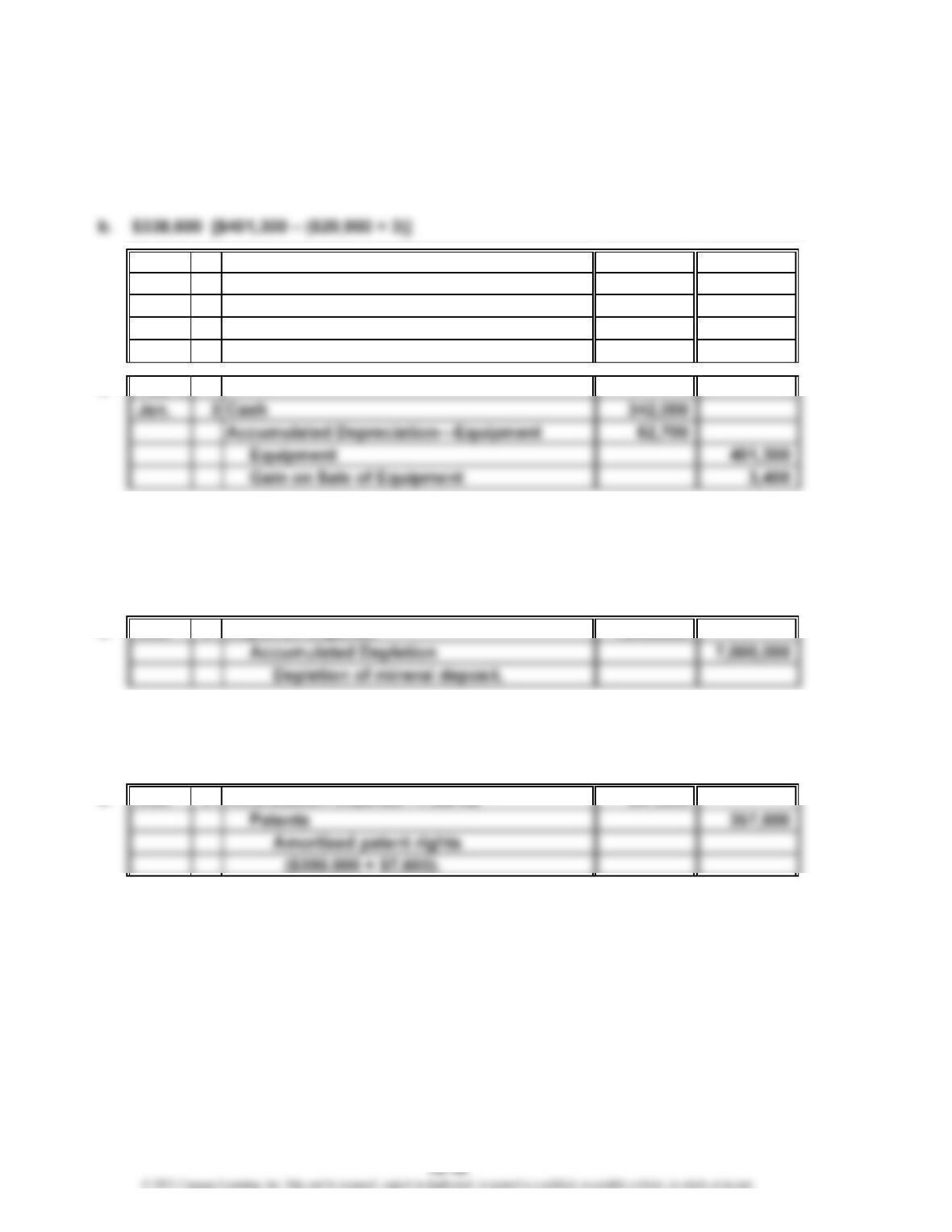

Accumulated Depletion 62,272,000

Depletion of mineral deposit.

PE 10-7B

a. $0.35 per ton = $195,650,000 ÷ 559,000,000 tons

PE 10-8A

a. Dec. 31 Loss from Impaired Goodwill 4,700,000

Goodwill 4,700,000

Impaired goodwill.

b. Dec. 31 Amortization Expense—Patents 78,750

Patents 78,750

Amortized patent rights

[($1,260,000 ÷ 12) × (9 ÷ 12)].

PE 10-8B

a. Dec. 31 Loss from Impaired Goodwill 1,600,000

Dec.

CHAPTER 10 Long-Term Assets: Fixed and Intangible

PE 10-9A

a. Fixed Asset Turnover:

Sales……………………………

…

b. The decrease in the fixed asset turnover ratio from 3.6 to 3.3 indicates an

unfavorable change in the efficiency of using fixed assets to generate sales.

PE 10-9B

a. Fixed Asset Turnover:

Sales…………………………

…

Fixed assets:

Beginning of year………

…

…

Year 2 Year 1

$1,560,000 $1,026,000

$580,000 $500,000

Year 2 Year 1

$4,521,000 $3,960,000

CHAPTER 10 Long-Term Assets: Fixed and Intangible

Ex. 10-1

a. New printing press: 1, 2, 3, 5, 6

b. Used printing press: 7, 8, 9, 11

Ex. 10-3

Initial cost of land ($90,000 + $50,000)……………………

…

$140,000

Legal fees……………………………………………………

…

$ 1,750

Delinquent taxes……………………………………………

…

25,000

Demolition of building……………………………………

…

9,000 35,750

Total costs to acquire and prepare land for use…………

…

$175,750

Less salvage of materials……………………………………

…

1,000

Cost of land to be reported on the balance sheet………

…

$174,750

Ex. 10-5

(a) 10% (100% ÷ 10), (b) 12.5% (100% ÷ 8), (c) 4% (100% ÷ 25),

(d) 2.5% (100% ÷ 40), (e) 20% (100% ÷ 5), (f) 25% (100% ÷ 4),

(g) 5% (100% ÷ 20)

Ex. 10-6

$4,400 [($66,700 – $5,100) ÷ 14]

EXERCISES

CHAPTER 10 Long-Term Assets: Fixed and Intangible

Ex. 10-8

a. Depreciation Rate per Mile:

Truck 1 ($80,000 – $15,000) ÷ 250,000 = $0.26

Truck 2 ($54,000 – $6,000) ÷ 300,000 = $0.16

Truck 3 ($72,900 – $10,900) ÷ 200,000 = $0.31

Truck 4 ($90,000 – $22,800) ÷ 240,000 = $0.28

Miles Operated

21,000

33,500

b. Dec. 31 Depreciation Expense—Trucks 18,980

Accumulated Depreciation—Trucks 18,980

Truck depreciation.

Ex. 10-10

a. 5% of ($61,000 – $9,000) = $2,600 or [($61,000 – $9,000) ÷ 20]

b. Year 1: 10% of $61,000 = $6,100

Year 2: 10% of ($61,000 – $6,100) = $5,490

Rate per Mile Depreciation

Accumulated

Truck No.

1

2

$0.26

0.16

Credit to

$ 5,460

5,360

CHAPTER 10 Long-Term Assets: Fixed and Intangible

Ex. 10-11

a. Year 1: ($105,000 – $12,000) ÷ 10 = $9,300; $9,300 × (8 ÷ 12) = $6,200

Year 2: ($105,000 – $12,000) ÷ 10 = $9,300

b. Year 1: 8 ÷ 12 × 20% of $105,000 = $14,000

Year 2: 20% of ($105,000 – $14,000) = $18,200

Ex. 10-13

Capital expenditures: 1, 3, 5, 7, 8, 9, 10

Revenue expenditures: 2, 4, 6

Ex. 10-15

Mar. 20 Accumulated Depreciation—Delivery Truck 1,890

Cash 1,890

June 11 Delivery Truck 1,350

Cash 1,350

CHAPTER 10 Long-Term Assets: Fixed and Intangible

Ex. 10-16

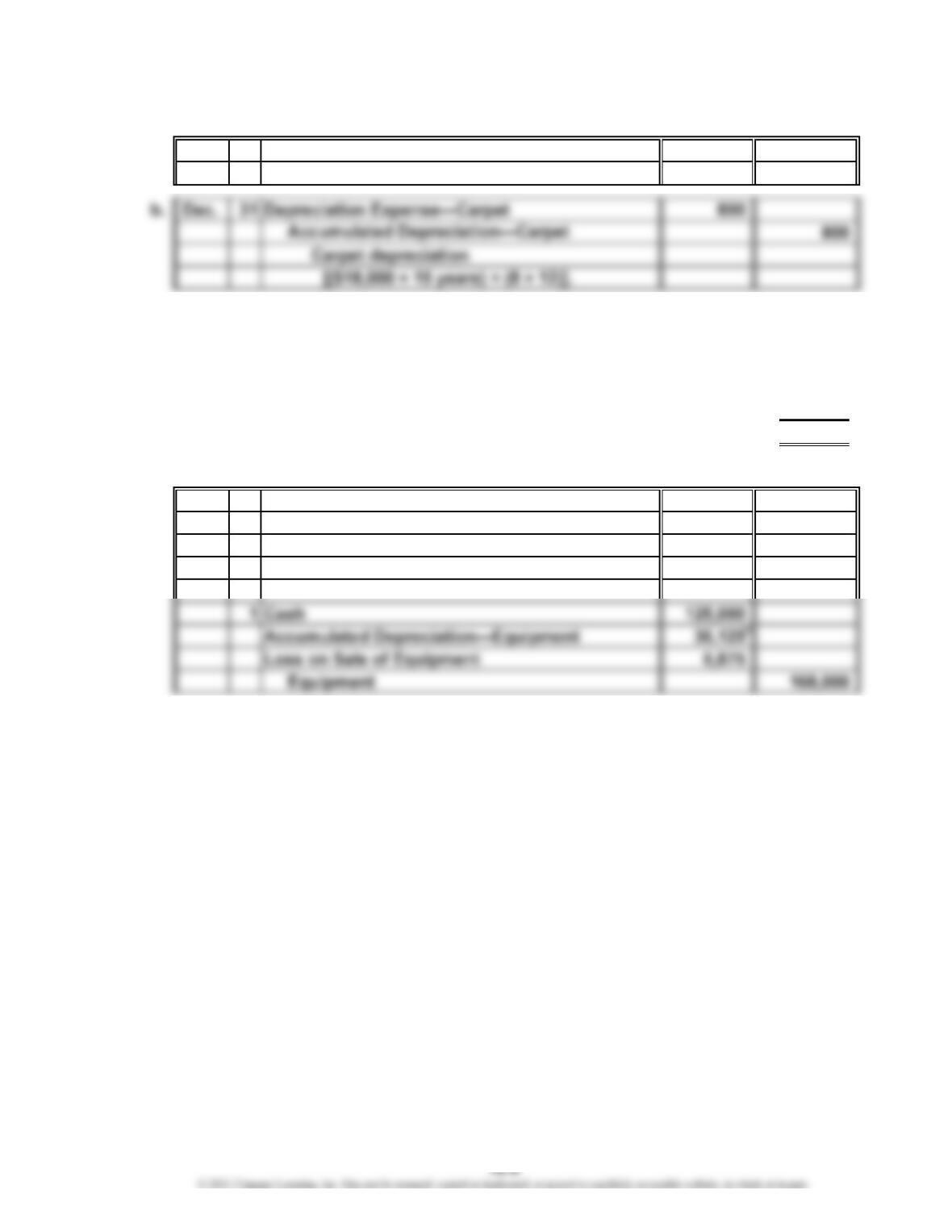

a. Apr. 30 Carpet 18,000

Cash 18,000

Ex. 10-17

a. Cost of equipment…………………………………………………………………

…

$168,000

Less accumulated depreciation at end of fourth year, December 31

(4 years at $8,500 per year)……………………………………………………

…

34,000

Book value at end of fourth year, December 31………………………………

…

$134,000

Yearly depreciation = ($168,000 – $15,000) ÷ 18 = $8,500

b. Apr. 1 Depreciation Expense—Equipment 2,125

Accumulated Depreciation—Equipment 2,125

Equipment depreciation

($8,500 × 3 ÷ 12).

* Accumulated Depreciation—Equipment = $34,000 + $2,125 = $36,125

CHAPTER 10 Long-Term Assets: Fixed and Intangible

Ex. 10-18

a. Year 1 depreciation expense: $20,900 [($401,300 – $25,100) ÷ 18]

Year 2 depreciation expense: $20,900

Year 3 depreciation expense: $20,900

c. Year 4

Jan. 3 Cash 315,000

Accumulated Depreciation—Equipment 62,700

Loss on Sale of Equipment 23,600

Equipment 401,300

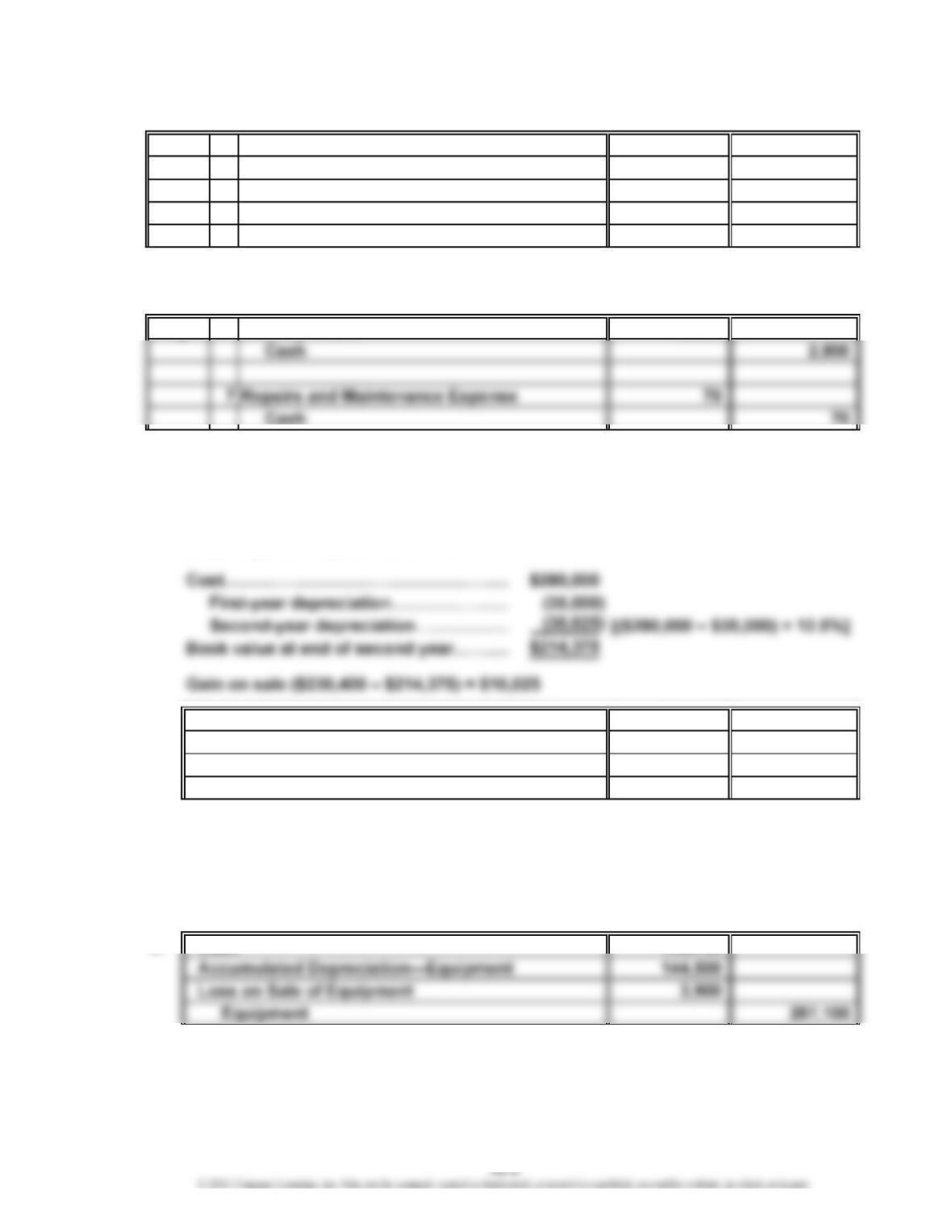

Ex. 10-19

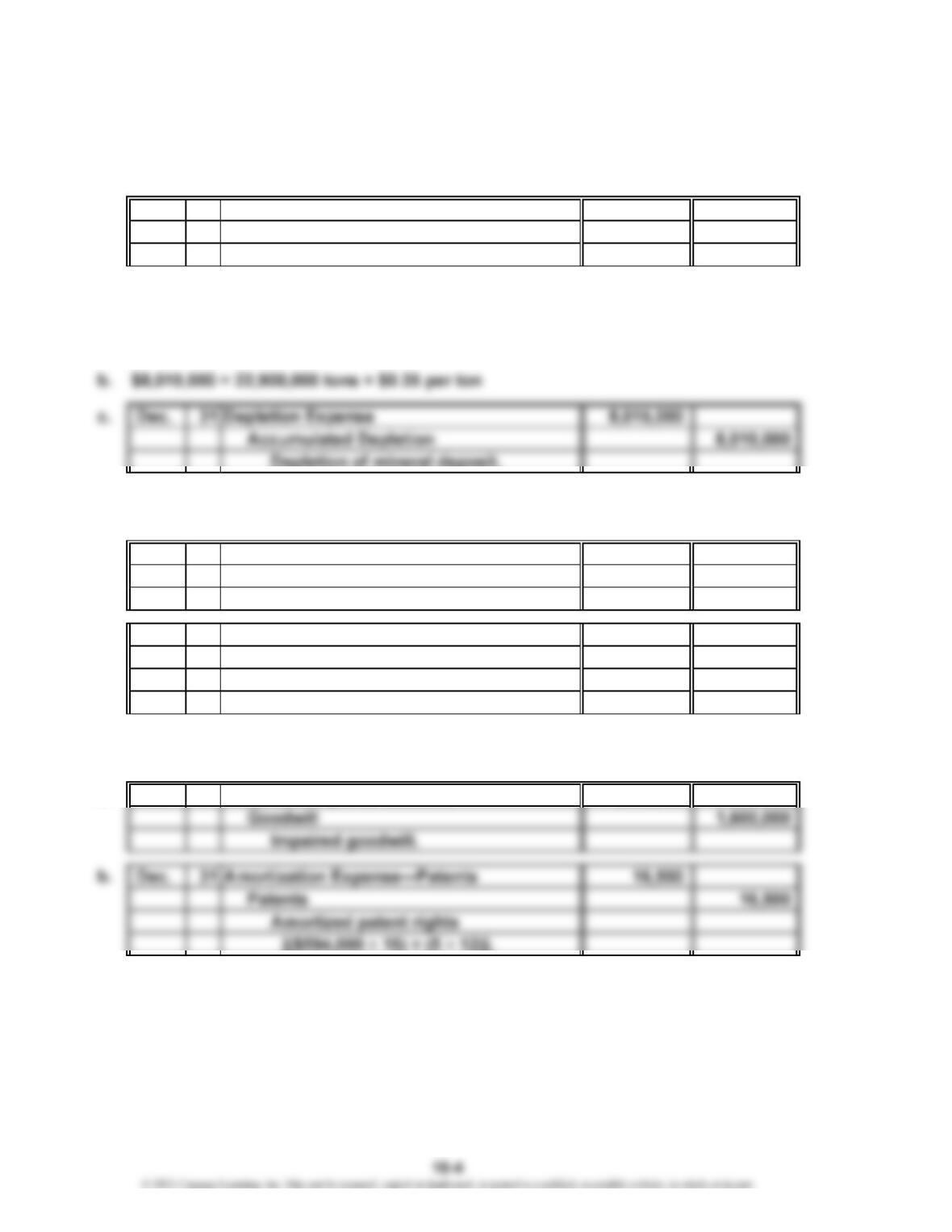

a. $53,200,000 ÷ 19,000,000 tons = $2.80 depletion per ton

2,500,000 tons × $2.80 = $7,000,000 depletion expense

Ex. 10-20

a. ($2,800,000 ÷ 8) + ($38,000 ÷ 5) = $357,600 total patent amortization expense

CHAPTER 10 Long-Term Assets: Fixed and Intangible

Ex. 10-21

a. Property, Plant, and Equipment (in millions):

Current Preceding

Year Year

Land and buildings………………………………………………

…

$16,216 $13,587

Machinery, equipment, and internal-use software…………

…

65,982 54,210

8,205 7,279

A comparison of the book values of the current and preceding years indicates

that the book value increased. A comparison of the total cost and accumulated

depreciation reveals that Apple purchased $15,327 million ($90,403 – $75,076) of

additional fixed assets, which was offset by the additional depreciation expense

of $7,806 million ($49,099 – $41,293) taken during the current year.

b. We would expect Apple’s book value of fixed assets to increase during the year as

Ex. 10-22

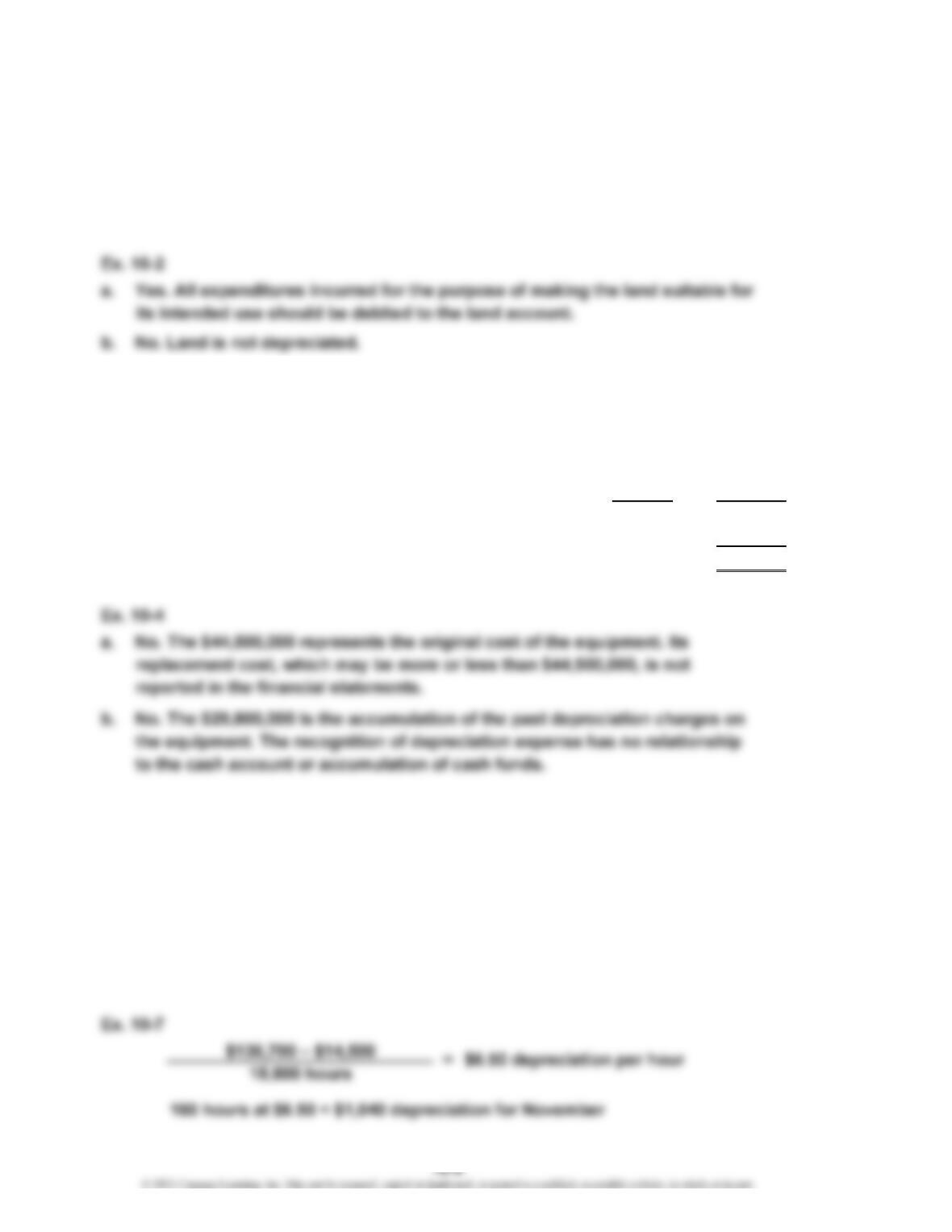

1. Fixed assets should be reported at cost and not replacement cost.

2. Land does not depreciate.

3. Patents and goodwill are intangible assets that should be listed in a separate section

…

CHAPTER 10 Long-Term Assets: Fixed and Intangible

Ex. 10-23

b. Netflix is more efficient than Amazon in generating revenue from fixed assets.

Netflix’s fixed asset turnover ratio is 42.8, which means it is able to generate $42.80

of revenue for every dollar of fixed assets. Amazon’s fixed asset turnover ratio is 4.2,

which is only $4.20 of revenue for every dollar of fixed assets. Netflix’s fixed asset

turnover ratio is more than 10 times larger than Amazon’s (42.8 ÷ 4.2).

c. The difference in their fixed asset turnover ratios reflects the difference in their

core businesses. Netflix is mostly an Internet streaming and DVD rental company.

These services do not require significant fixed assets. The most significant fixed

fixed assets are the cause of Amazon’s lower fixed asset turnover ratio.

Ex. 10-24

b. Verizon earns $1.50 revenue for every dollar of fixed assets. Telecommunications

requires a significant investment in the network in order to generate revenues.

The industry average fixed asset turnover ratio is just over 1.0. Thus, Verizon is

Fixed Asset Turnover Ratio = Sales

a.

($89,286 + $88,568) ÷ 2

a.

Verizon: $130,863 = 1.5

Sales

Average Book Value of Fixed Assets

Fixed Asset Turnover Ratio =

CHAPTER 10 Long-Term Assets: Fixed and Intangible

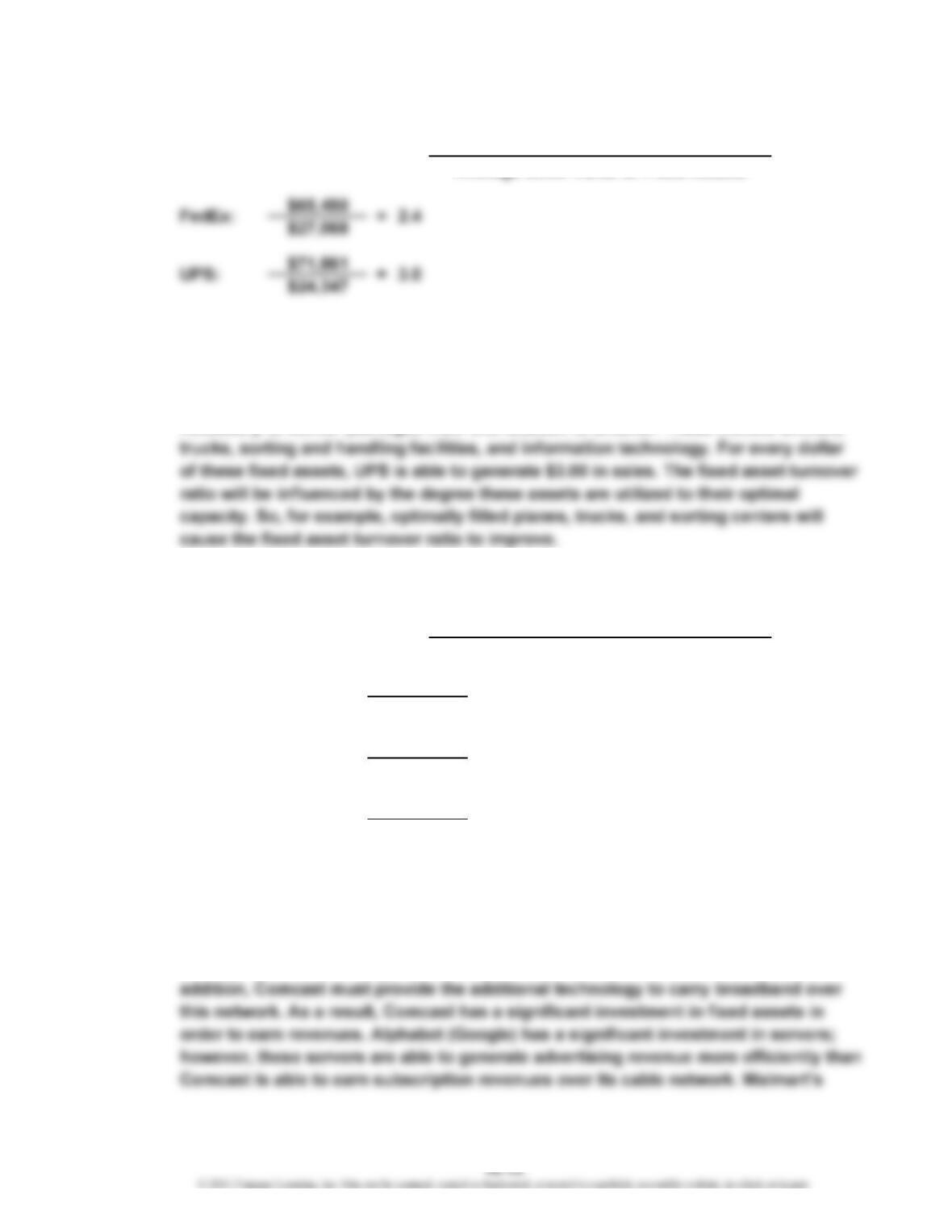

Ex. 10-25

b. The ratios show that UPS is 25% more efficient at using its fixed assets than

FedEx [(3.0 – 2.4) ÷ 2.4].

c. The fixed asset turnover is a measure of how efficiently revenue is generated from

underlying fixed assets. In the case of UPS, the fixed assets represent all fixed asset

s

Ex. 10-26

b. Comcast’s fixed asset turnover is less than the other two companies. This means

Comcast is less efficient at generating sales from fixed assets than the other two

companies. This can be explained by the nature of Comcast’s business. Comcast

must build a complete cable network in order to earn revenues. This includes

underground cable through cities, neighborhoods, and individual residences. In

Sales

Average Book Value of Fixed Assets

2.3

2.7

4.5

$136,819

$51,051

$94,507

$41,454

$510,329

$113,107

=

=

Comcast:

=Walmart:

Alphabet (Google) Inc.:

a.

Fixed Asset Turnover Ratio =

a. Fixed Asset Turnover Ratio = Sales

CHAPTER 10 Long-Term Assets: Fixed and Intangible

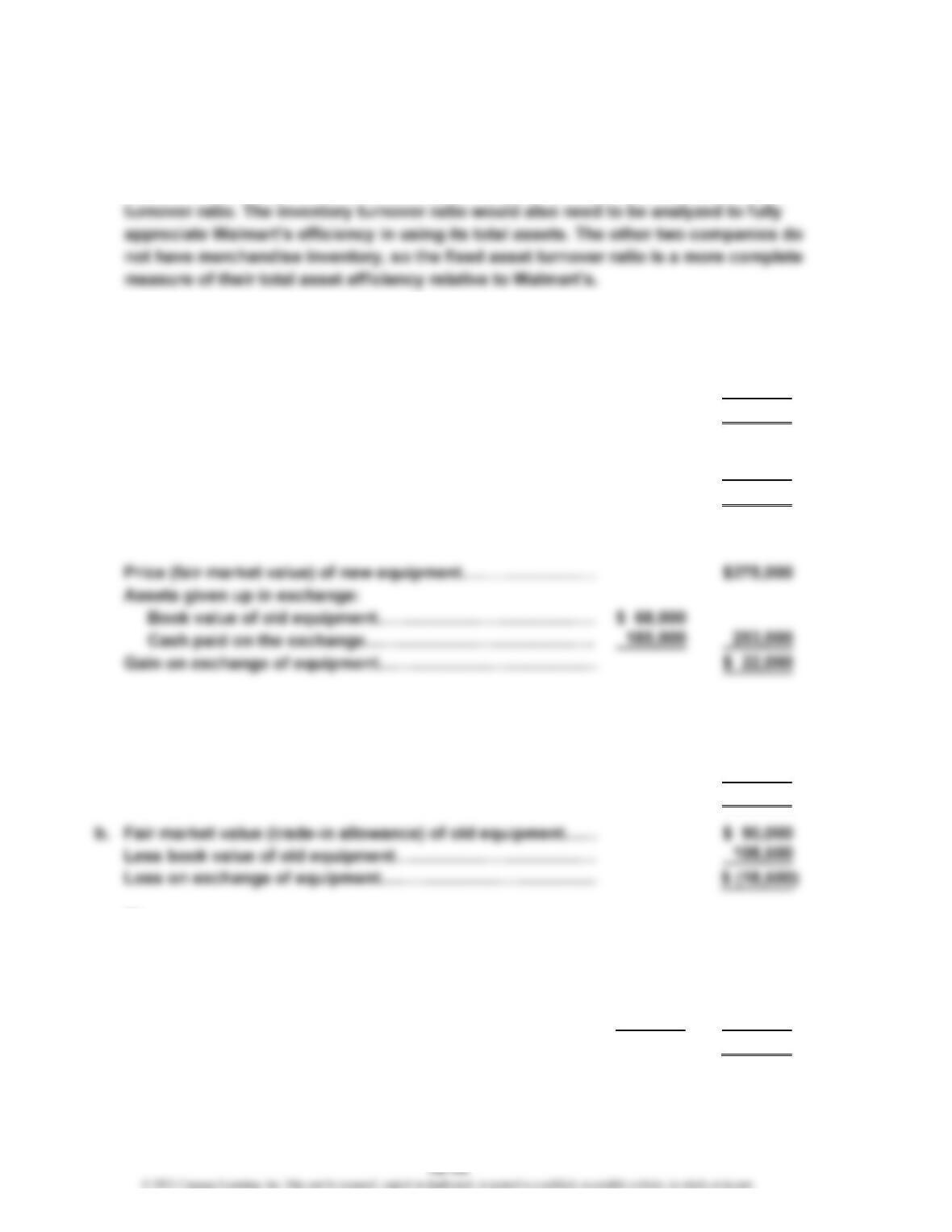

Ex. 10-26 (Concluded)

major fixed assets are its stores. However, Walmart’s other major asset is

merchandise inventory, which is not included in the fixed asset turnover ratio.

Thus, Walmart’s higher asset efficiency is only partially explained by the fixed asset

Appendix Ex. 10-27

a. Price (fair market value) of new equipment…………………… $275,000

Less trade-in allowance of old equipment……………………

…

90,000

Cash paid on the date of exchange……………………………

…

$185,000

b. Fair market value (trade-in allowance) of old equipment…

…

$ 90,000

Less book value of old equipment……………………………… 68,000

Gain on exchange of equipment………………………………… $ 22,000

or

…

Appendix Ex. 10-28

a. Price (fair market value) of new equipment…………………… $275,000

Less trade-in allowance of old equipment……………………

…

90,000

Cash paid on the date of exchange……………………………

…

$185,000

…

…

or

Price (fair market value) of new equipment…………………… $275,000

Assets given up in exchange:

Book value of old equipment………………………………… $108,500

Cash paid on the exchange…………………………………

…

185,000 293,500

Loss on exchange of equipment………………………………

…

$ (18,500)

CHAPTER 10 Long-Term Assets: Fixed and Intangible

Appendix Ex. 10-29

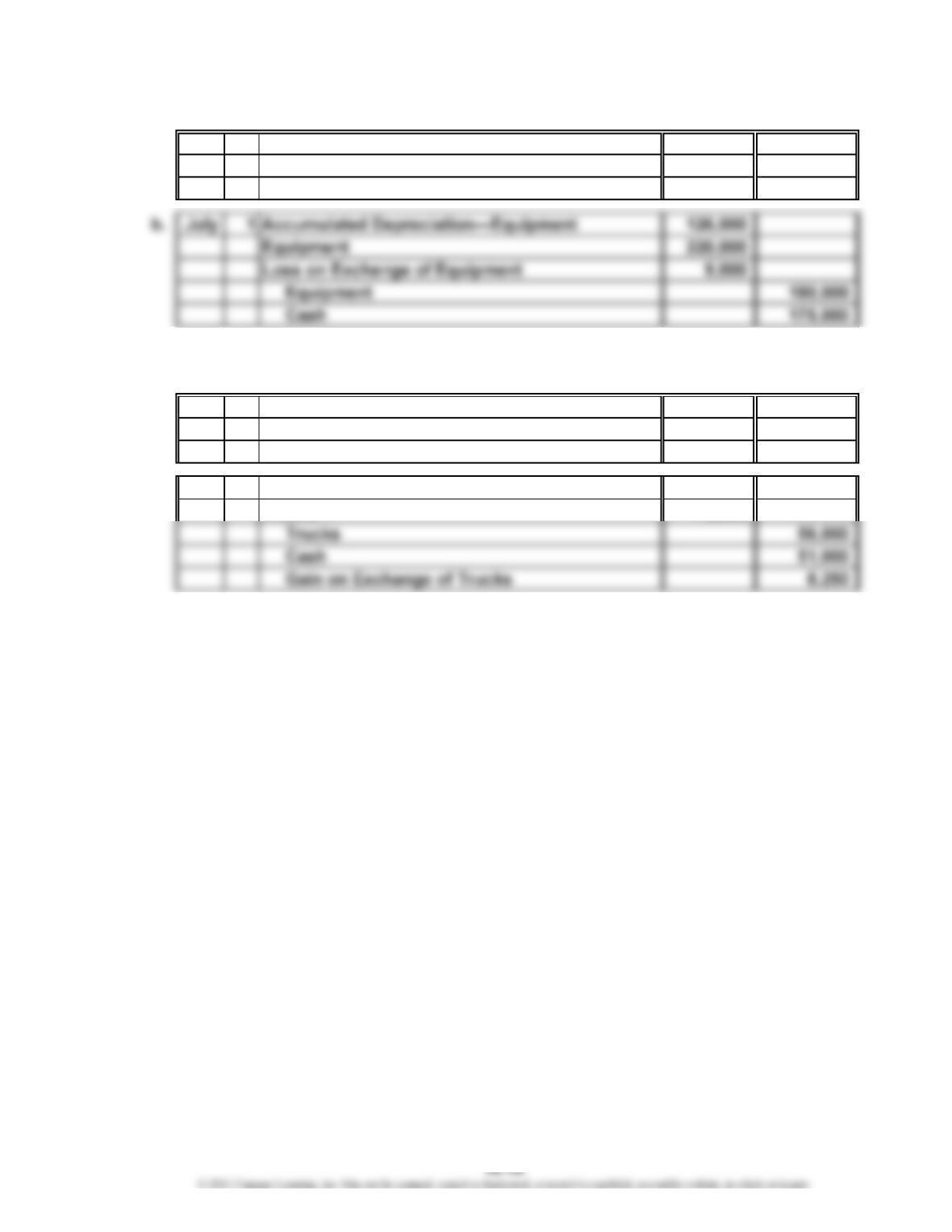

a. July 1 Depreciation Expense—Equipment 6,000

Accumulated Depreciation—Equipment 6,000

Equipment depreciation ($12,000 × 6 ÷ 12).

Appendix Ex. 10-30

a. Oct. 1 Depreciation Expense—Trucks 5,250

Accumulated Depreciation—Trucks 5,250

Truck depreciation ($7,000 × 9 ÷ 12).

b. Oct. 1 Accumulated Depreciation—Trucks 40,250

Trucks 75,000

CHAPTER 10 Long-Term Assets: Fixed and Intangible

Prob. 10-1A

1. Land Other

Item Land Improvements Building Accounts

a. $ 2,500

b. 340,000

c. 15,500

d. 5,000

j. $(900,000)

k. 5,500

l. $32,000

m. 11,000

n. 2,000

o. 2,500

p. (7,500)

3. Land used as a plant site does not lose its ability to provide services; thus, it is

not depreciated. However, land improvements do lose their ability to provide

services as time passes and are, therefore, depreciated.

4. Because land improvements are depreciated, depreciation expense of $1,200

[$12,000 × (100% ÷ 20) × 2] would be overstated and net income would be

PROBLEMS

*

*