CHAPTER 10

Budgetary Control and Responsibility Accounting

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Describe budgetary control

and static budget reports.

1, 2, 3, 4, 5

1, 2

1

1, 2, 8, 9

3A

2. Prepare flexible budget

reports.

6, 7, 8, 9, 10,

11, 12

3, 4, 5

2

1, 3, 4, 5, 6, 7,

8, 9, 10, 11,

12

1A, 2A, 3A

3. Apply responsibility

accounting to cost and profit

centers.

13, 14, 15, 16,

17, 18, 19, 20,

21, 24

6, 7

3

10, 11, 13, 14,

15, 16

4A, 6A

4. Evaluate performance in

investment centers.

22, 23, 24

8, 9, 10

4

16, 17, 18, 19

5A

*5. Explain the difference

between ROI and residual

income.

25, 26

11, 12

20, 21

7A

*Note: All asterisked Questions, Exercises, and Problems relate to material contained in the appendix to the

chapter.

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Prepare flexible budget and budget report for manufacturing

overhead.

Simple

20–30

2A

Prepare flexible budget, budget report, and graph for

manufacturing overhead.

Moderate

30–40

3A

State total budgeted cost formula, and prepare flexible

budget reports for two time periods.

Simple

20–30

5A

Prepare responsibility report for an investment center,

Moderate

40–50

6A

Prepare reports for cost centers under responsibility

Moderate

40–50

Compare ROI and residual income.

ANSWERS TO QUESTIONS

1. (a) Budgetary control is the use of budgets in controlling operations.

(b) The steps in budgetary control are:

(1) Develop the planned objectives (budget).

2.

Purpose

Name of Report

Frequency

Primary Recipient(s)

(a)

(b)

(c)

Scrap

Departmental overhead costs

Income statement

Daily

Monthly

Monthly and Quarterly

Production manager

Department manager

Top management

3. The budget report for the second quarter can include year-to-date information as well as data for

the second quarter.

4. There is no justification for Ken’s concern. The sales budget is derived from the sales forecast

and it represents management’s best estimate of sales. Thus, it is a useful basis for evaluating

sales performance.

5. A static budget is an appropriate basis for evaluating a manager’s effectiveness in controlling

costs when:

6. Yes, this is true. A flexible budget is a series of static budgets at different levels of activity.

7. The performance is unfavorable. The budgeted indirect labor cost in the static budget is $1.35 per

direct labor hour ($54,000 ÷ 40,000). At 45,000 direct labor hours, budgeted costs are $60,750

(45,000 X $1.35). Thus, indirect labor is $3,250 over budget ($64,000 – $60,750).

8. The performance is favorable. Factory insurance is a fixed cost. At 50,000 direct labor hours, the

budgeted cost is still $6,500. Thus, factory insurance is $200 under budget ($6,500 – $6,300).

9. The steps in preparing a flexible budget are:

(1) Identify the activity index and the relevant range of activity.

10. Cali Company can say that total budgeted costs are $20,000 fixed plus $6.50 per direct labor

hour [($85,000 – $20,000) ÷ 10,000].

11. (a) At 9,000 hours, total budgeted costs are $86,000, or [$50,000 + ($4 X 9,000)].

(b) At 12,345 hours, total budgeted costs are $99,380, or [$50,000 + ($4 X 12,345)].

Questions Chapter 10 (Continued)

12. Management by exception means that top management’s review of a budget report is focused

either entirely or primarily on differences between actual results and planned objectives. The

criteria for identifying exceptions are materiality and controllability of the item.

13. Responsibility accounting is a method of controlling operations that involves accumulating and

reporting costs (and revenues, where relevant) on the basis of the manager who has the authority

to make the day-to-day decisions about the items. The purpose of responsibility accounting is to

evaluate a manager’s performance on the basis of matters directly under that manager’s control.

15. A cost is controllable at a given level of managerial responsibility if the manager has the power to

incur the cost within a given period of time. Most costs incurred directly are controllable, whereas costs

incurred indirectly and allocated to a responsibility level are noncontrollable at that level.

16. Responsibility reports differ from budget reports in two respects: (1) a distinction is made between

controllable and noncontrollable items and (2) performance reports either emphasize, or only

include, items controllable by the individual manager.

18. There are three types of responsibility centers:

(a) A cost center incurs costs (and expenses) but does not generate revenues.

19. (a) Only controllable costs are included in a performance report for a cost center.

(b) Variable and fixed costs are not identified in the report.

20. Direct fixed costs relate specifically to one center and are incurred for the sole benefit of that

center. An indirect fixed cost relates to the company’s overall activities and is incurred for the

Questions Chapter 10 (Continued)

22. The primary basis for evaluating the performance of the manager of an investment center is

return on investment (ROI). The formula is: Controllable Margin divided by Average Operating Assets.

23. ROI can be improved by: (1) increasing controllable margin and (2) reducing average operating

assets. Controllable margin can be increased by increasing sales or by reducing variable and

controllable fixed costs.

24. (a) The manager being evaluated should have direct input into the process of establishing budget

goals and have the opportunity to respond to the evaluation. (b) Top management should make

the evaluation entirely on matters controllable by the manager, and should fully support the

evaluation process.

SOLUTIONS TO BRIEF EXERCISES

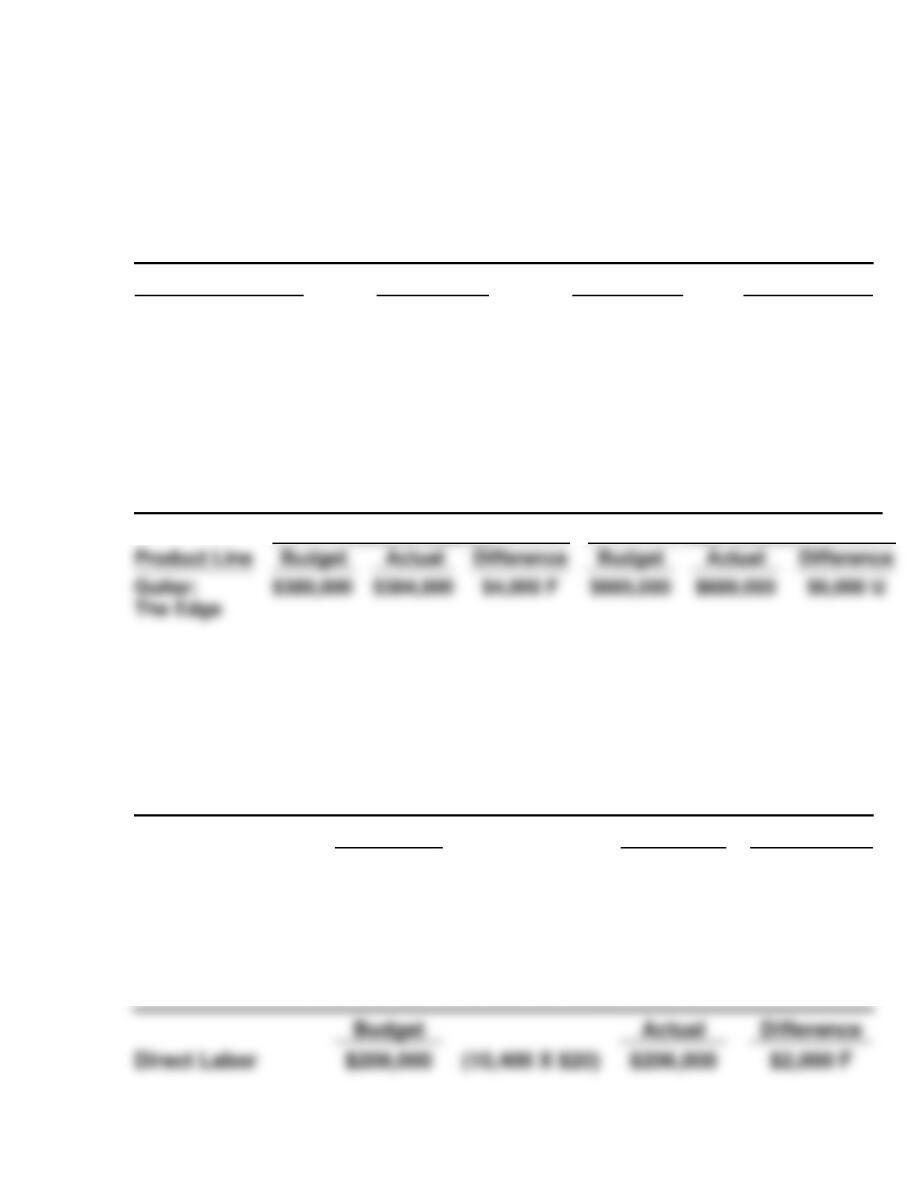

BRIEF EXERCISE 10-1

CROIX COMPANY

Sales Budget Report

For the Quarter Ended March 31, 2017

Product Line

Budget

Actual

Difference

Guitar: The Edge

$315,000

$305,000

$10,000 U

BRIEF EXERCISE 10-2

CROIX COMPANY

Sales Budget Report

For the Quarter Ended June 30, 2017

Second Quarter

Year to Date

The Edge

BRIEF EXERCISE 10-3

(a) ROONEY COMPANY

Static Direct Labor Budget Report

For the Month Ended January 31, 2017

Budget

Actual

Difference

Direct Labor

$200,000

(10,000 X $20)

$206,000

$6,000 U

(b) ROONEY COMPANY

Flexible Direct Labor Budget Report

For the Month Ended January 31, 2017

Direct Labor

(10,400 X $20)

$2,000 F

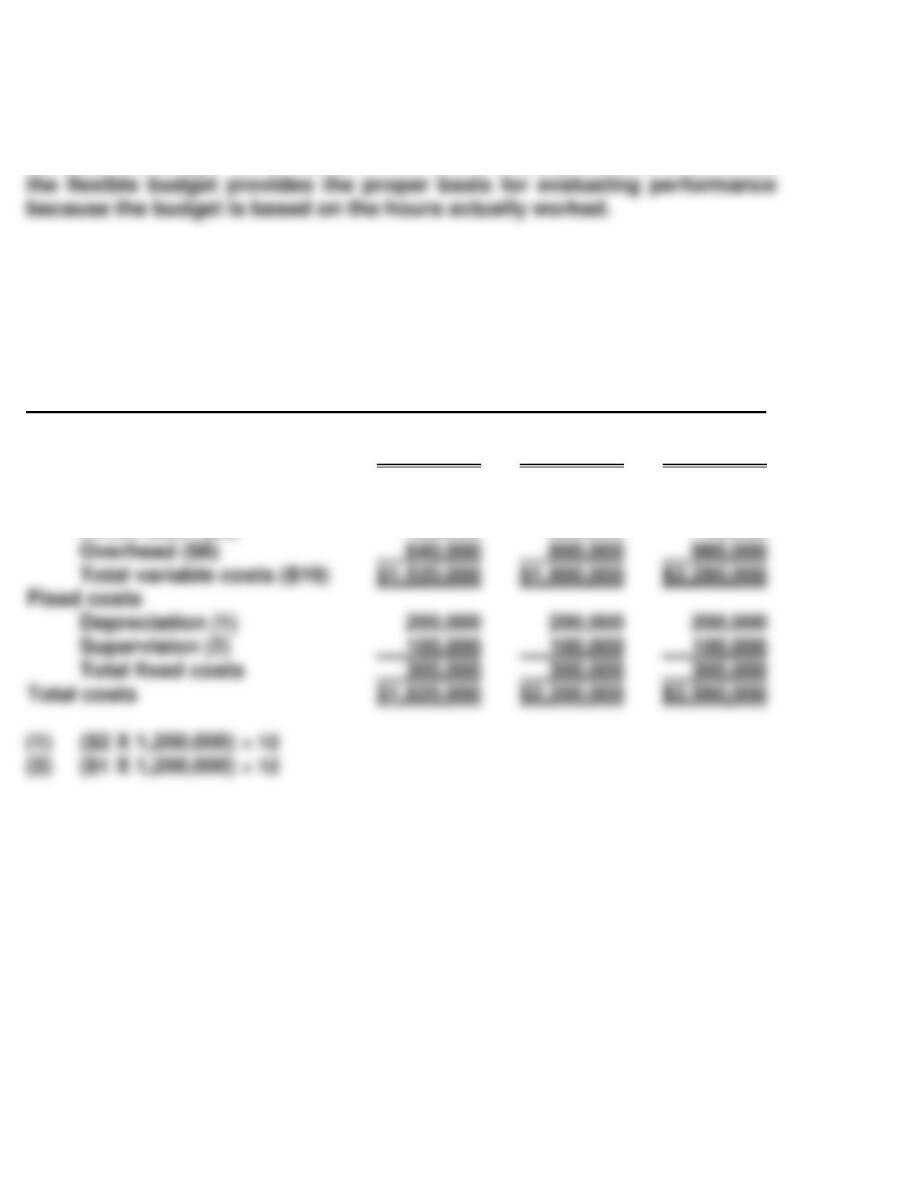

BRIEF EXERCISE 10-3 (Continued)

The static budget does not provide a proper basis for evaluating performance

because the budget is not based on the hours actually worked. In contrast,

BRIEF EXERCISE 10-4

GUNDY COMPANY

Monthly Flexible Manufacturing Budget

For the Year 2017

Activity level

Finished units

Variable costs

Direct materials ($5)

Direct labor ($6)

80,000

$ 400,000

480,000

100,000

$ 500,000

600,000

120,000

$ 600,000

720,000

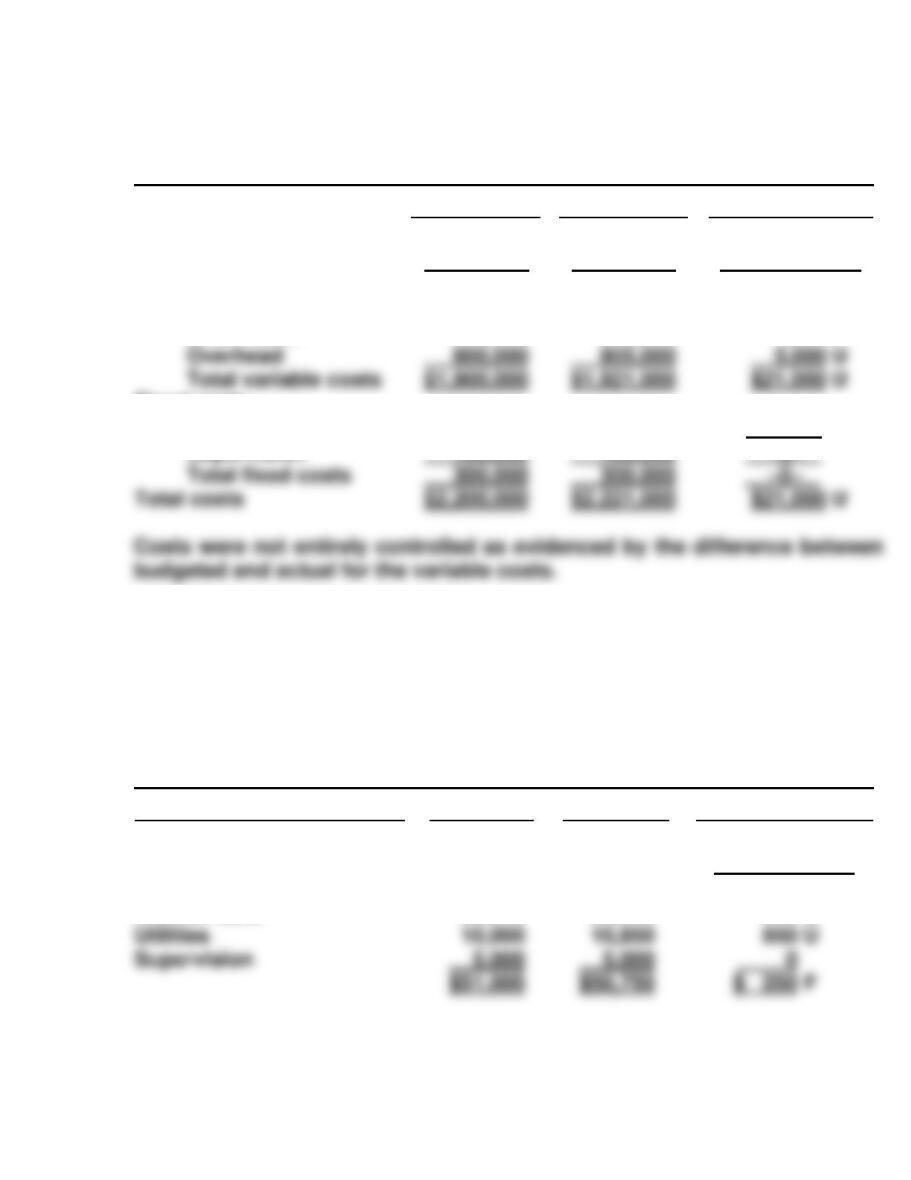

BRIEF EXERCISE 10-5

GUNDY COMPANY

Manufacturing Flexible Budget Report

For the Month Ended March 31, 2017

Budget

Actual

Difference

Units produced

Variable costs

Direct materials

Direct labor

Fixed costs

Depreciation

Supervision

100,000

$ 500,000

600,000

200,000

100,000

100,000

$ 520,000

596,000

200,000

100,000

Favorable F

Unfavorable U

$20,000 U

4,000 F

–0–

–0–

BRIEF EXERCISE 10-6

HANNON COMPANY

Assembly Department

Manufacturing Overhead Cost Responsibility Report

For the Month Ended April 30, 2017

Controllable Cost

Budget

Actual

Difference

Utilities

$50,750

Indirect materials

Indirect labor

$16,000

20,000

$14,300

20,600

Favorable F

Unfavorable U

$1,700 F

600 U

BRIEF EXERCISE 10-7

TORRES COMPANY

Water Division

Responsibility Report

For the Year Ended December 31, 2017

Budget

Actual

Difference

Sales

Variable costs

$2,000,000

1,000,000

$2,080,000

1,050,000

Favorable F

Unfavorable U

$80,000 F

50,000 U

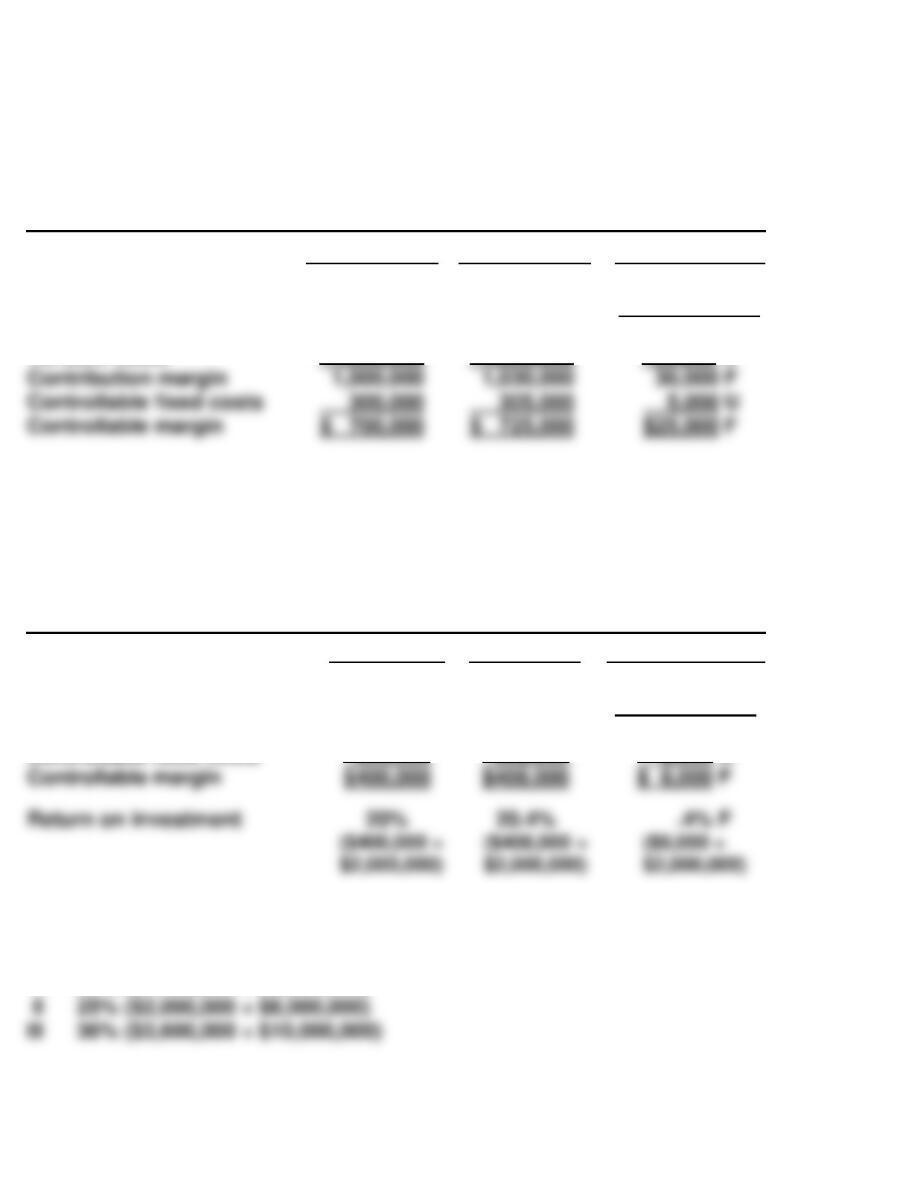

BRIEF EXERCISE 10-8

COBB COMPANY

Plastics Division

Responsibility Report

For the Year Ended December 31, 2017

Budget

Actual

Difference

Contribution margin

Controllable fixed costs

$700,000

300,000

$710,000

302,000

Favorable F

Unfavorable U

$10,000 F

2,000 U

BRIEF EXERCISE 10-9

III 28% ($1,400,000 ÷ $5,000,000)

$25,000 F

BRIEF EXERCISE 10-10

III A $300,000 ($2,000,000 X .15) increase in sales will increase contribution

margin and controllable margin $210,000 ($300,000 X 70%). The new

ROI is 32.2% ($1,610,000 ÷ $5,000,000).

*BRIEF EXERCISE 10-11

Controllable Margin

÷

Average Operating Assets

=

ROI

$630,000

÷

$3,000,000

=

21%

Controllable Margin

(Minimum Rate of Return X Average Operating Assets)

=

Residual Income

$630,000

=

Residual Income

=

*BRIEF EXERCISE 10-12

Controllable Margin

÷

Average Operating Assets

=

ROI

$800,000

÷

$4,000,000

=

20%

(Minimum Rate of Return X Average Operating Assets)

=

Residual Income

$800,000

=

Residual Income

$800,000

=

SOLUTIONS FOR DO IT! EXERCISES

DO IT! 10-1

Difference

Favorable F

Unfavorable U

Budget

6,000

Actual

6,500

Production in units

Variable costs

Direct materials ($7)

$ 42,000

$ 38,850

$3,150 F

The static budget indicates that actual variable costs exceeded budgeted

amounts by $3,930. Fixed costs were unfavorable by $200. The static

budget gives the impression that the company did not control its variable

DO IT! 10-2

Using the graph data, fixed costs are $90,000, and variable costs are $5.20

Overhead ($18)

Total variable costs

Fixed costs

Depreciation*

Total fixed costs

11,800

12,000

200 U

Total costs

$239,800

$243,930

DO IT! 10-3

ROCKIES DIVISION

Responsibility Report

For the Year Ended December 31, 2017

Difference

Favorable F

Budget Actual Unfavorable U

Sales $2,000,000 $1,890,000 $110,000 U

DO IT! 10-4

(a) Controllable margin for 2017:

Sales ……………………………………………..

$500,000

Variable costs ………………………………..

300,000

Contribution margin ……………………….

200,000

Controllable fixed costs ………………….

75,000

Controllable margin ………………………..

$125,000*

(b) Expected return on investment for alternative 1:

DO IT! 10-4 (Continued)

Controllable margin for alternative 2:

Sales ($500,000 + 100,000) ……………………….

$600,000

Variable costs

($300,000/$500,000 X $600,000) ……………..

360,000

Contribution margin ………………………………..

240,000

Controllable fixed costs …………………………..

75,000

Controllable margin …………………………………

$165,000

SOLUTIONS TO EXERCISES

EXERCISE 10-1

1. True.

2. False. Budget reports are prepared as frequently as needed.

3. True.

4. True.

5. False. Budgetary control works best when a company has a formalized

EXERCISE 10-2

(a) CREDE COMPANY

Selling Expense Report

For the Quarter Ending March 31

By Month

Year–to–Date

Month

Budget

Actual

Difference

Budget

Actual

Difference

January

$30,000

$31,200

$1,200 U

$ 30,000

$ 31,200

$1,200 U

February

$35,000

$34,525

$ 65,000

March

$40,000

$46,000

$6,000 U

$105,000

$111,725

$6,725 U

(b) The purpose of the Selling Expense Report is to help management

control selling expenses. The primary recipient is the sales manager.

(c) Most likely, when management scrutinized the results for January and

February, they would determine that the difference was insignificant

EXERCISE 10-3

MYERS COMPANY

Monthly Manufacturing Overhead Flexible Budget

For the Year 2017

Activity level

Direct labor hours

Variable costs

Indirect labor ($1)

Indirect materials ($.70)

7,000

$ 7,000

4,900

8,000

$ 8,000

5,600

9,000

$ 9,000

6,300

10,000

$10,000

7,000

EXERCISE 10-4

(a) MYERS COMPANY

Manufacturing Overhead Flexible Budget Report

For the Month Ended July 31, 2017

Difference

Direct labor hours (DLH)

Variable costs

Indirect labor

Budget at

9,000 DLH

$ 9,000

Actual Costs

9,000 DLH

$ 8,800

Favorable F

Unfavorable U

$200 F

EXERCISE 10-4 (Continued)

(b) MYERS COMPANY

Manufacturing Overhead Flexible Budget Report

For the Month Ended July 31, 2017

Difference

Direct labor hours (DLH)

Variable costs

Indirect labor ($1.00)

Indirect materials ($0.70)

Budget at

8,500 DLH

$ 8,500

5,950

Actual Costs

8,500 DLH

$ 8,800

5,800

Favorable F

Unfavorable U

$300 U

150 F

(c) In case (a) the performance for the month was satisfactory. In case

(b) management may need to determine the causes of the differences

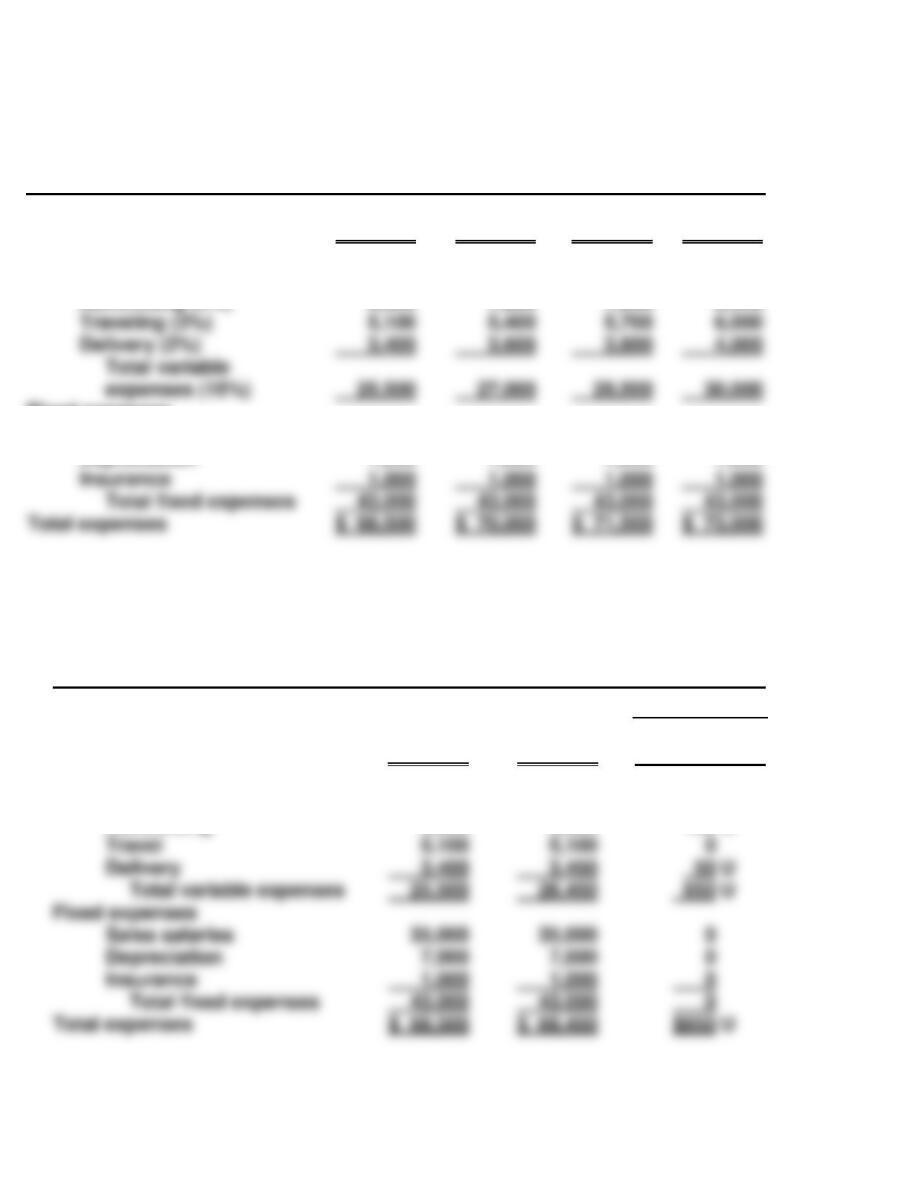

EXERCISE 10-5

FALLON COMPANY

Monthly Selling Expense Flexible Budget

For the Year 2017

Activity level

Sales

Variable expenses

Sales commissions (6%)

Advertising (4%)

Fixed expenses

Sales salaries

Depreciation

$170,000

$ 10,200

6,800

35,000

7,000

$180,000

$ 10,800

7,200

35,000

7,000

$190,000

$ 11,400

7,600

35,000

7,000

$200,000

$ 12,000

8,000

35,000

7,000

EXERCISE 10-6

(a) FALLON COMPANY

Selling Expense Flexible Budget Report

For the Month Ended March 31, 2017

Difference

Sales

Variable expenses

Sales commissions

Advertising

Budget

$170,000

$ 10,200

6,800

Actual

$170,000

$ 11,000

6,900

Favorable F

Unfavorable U

$800 U

100 U

EXERCISE 10-6 (Continued)

(b) FALLON COMPANY

Selling Expense Flexible Budget Report

For the Month Ended March 31, 2017

Difference

Sales

Variable expenses

Sales commissions

Fixed costs

Sales salaries

Depreciation

Budget

$180,000

$ 10,800

35,000

7,000

Actual

$180,000

$ 11,000

35,000

7,000

Favorable F

Unfavorable U

$200 U

0 U

0 U

(c) Flexible budgets are essential in evaluating a manager’s performance

in controlling variable expenses because the budget allowance varies

EXERCISE 10-7

(a) APPLIANCE POSSIBLE INC.

Flexible Production Cost Budget

Activity level

Production levels 90,000 100,000 110,000

Variable costs:

Manufacturing ($6) $ 540,000 $ 600,000 $ 660,000

Fixed costs:

Manufacturing 160,000 160,000 160,000

(b) Let (X) represent number of units

Sales price(X) = Variable costs(X) + Fixed costs + Profit

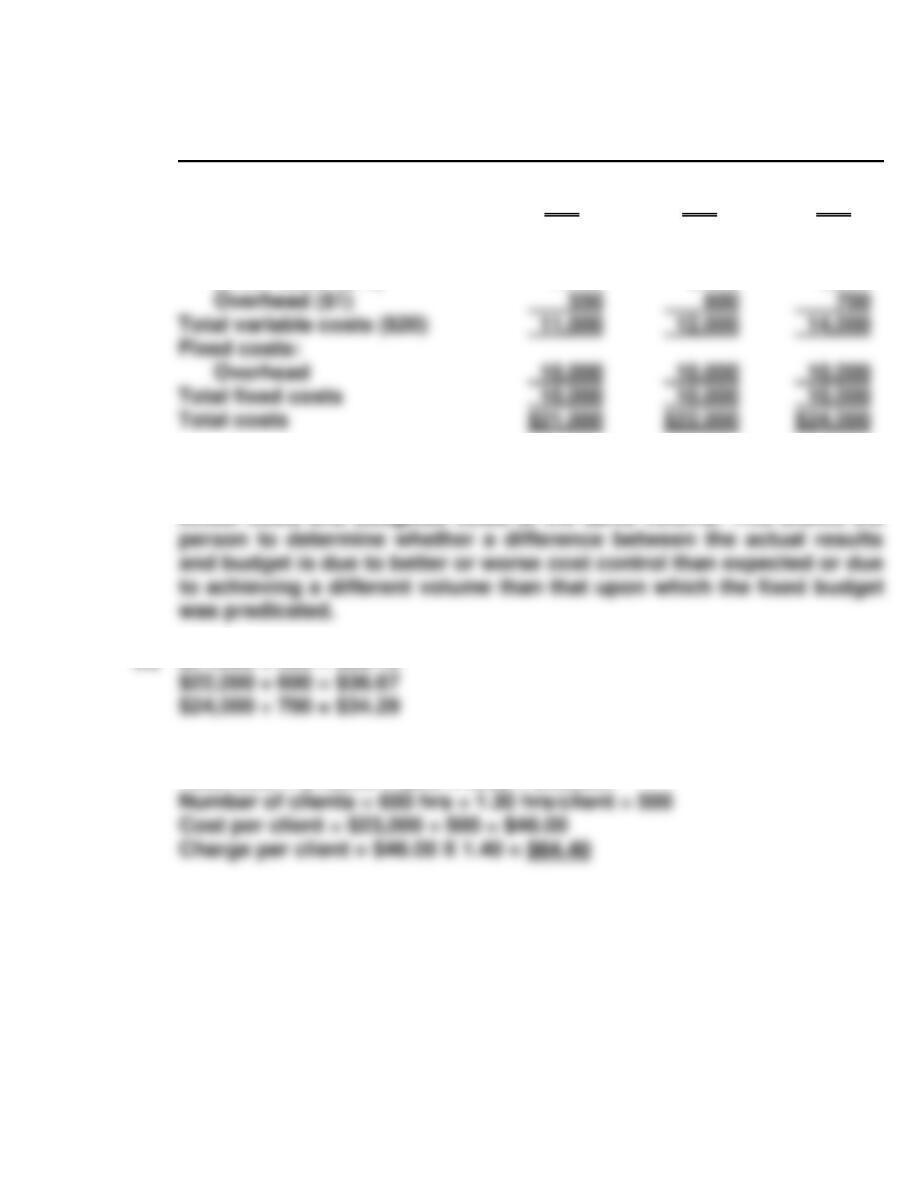

EXERCISE 10-8

(a) RENSING GROOMERS

Flexible Budget

Activity level

Direct labor hours 550 600 700

Variable costs:

Grooming supplies ($5) $ 2,750 $ 3,000 $ 3,500

Direct labor ($14) 7,700 8,400 9,800

(b) A flexible budget presents expected costs at various levels of produc–

tion volume, not just one, so that comparisons can be made between

actual costs and budgeted costs at the same volume. This allows the

(c) $21,000 ÷ 550 = $38.18

(d) Cost formula is $10,000 + $20(X), where (X) = direct labor hours

Total cost = $10,000 + ($20 X 650) = $23,000.

EXERCISE 10-9

(a) SORIA COMPANY

Selling Expense Flexible Budget Report

Clothing Department

For the Month Ended October 31, 2017

Difference

Sales in units

Variable expenses

Sales commissions ($.30)

Advertising expense ($.09)

Fixed expenses

Rent

Sales salaries

Budget

10,000

$ 3,000

900

1,500

1,200

Actual

10,000

$ 2,600

850

1,500

1,200

Favorable F

Unfavorable U

$ 400 F

50 F

0 U

0 U

(b) No, Joe should not have been reprimanded. As shown in the flexible

budget report, variable costs were $1,450 below budget.

EXERCISE 10-10

(a) CHUBBS INC.

Manufacturing Overhead Flexible Budget Report

For the Quarter Ended March 31, 2017

Difference

Budget

Actual

Favorable F

Unfavorable U

Variable costs

Indirect materials

Indirect labor

$12,000

10,000

$13,500

9,500

$1,500 U

500 F

(b) CHUBBS INC.

Manufacturing Overhead Responsibility Report

For the Quarter Ended March 31, 2017

Difference

Controllable Costs

Budget

Actual

Favorable F

Unfavorable U

Indirect materials

Indirect labor

$12,000

10,000

$13,500

9,500

$1,500 U

500 F

EXERCISE 10-11

(a) URLINK COMPANY

Home Internet Services Segment

Responsibility Report

For the Quarter Ended March 31, 2017

Budget

Actual

Difference

Favorable F

Unfavorable U

Service revenue

$25,000

$26,200

$1,200 F

Variable costs:

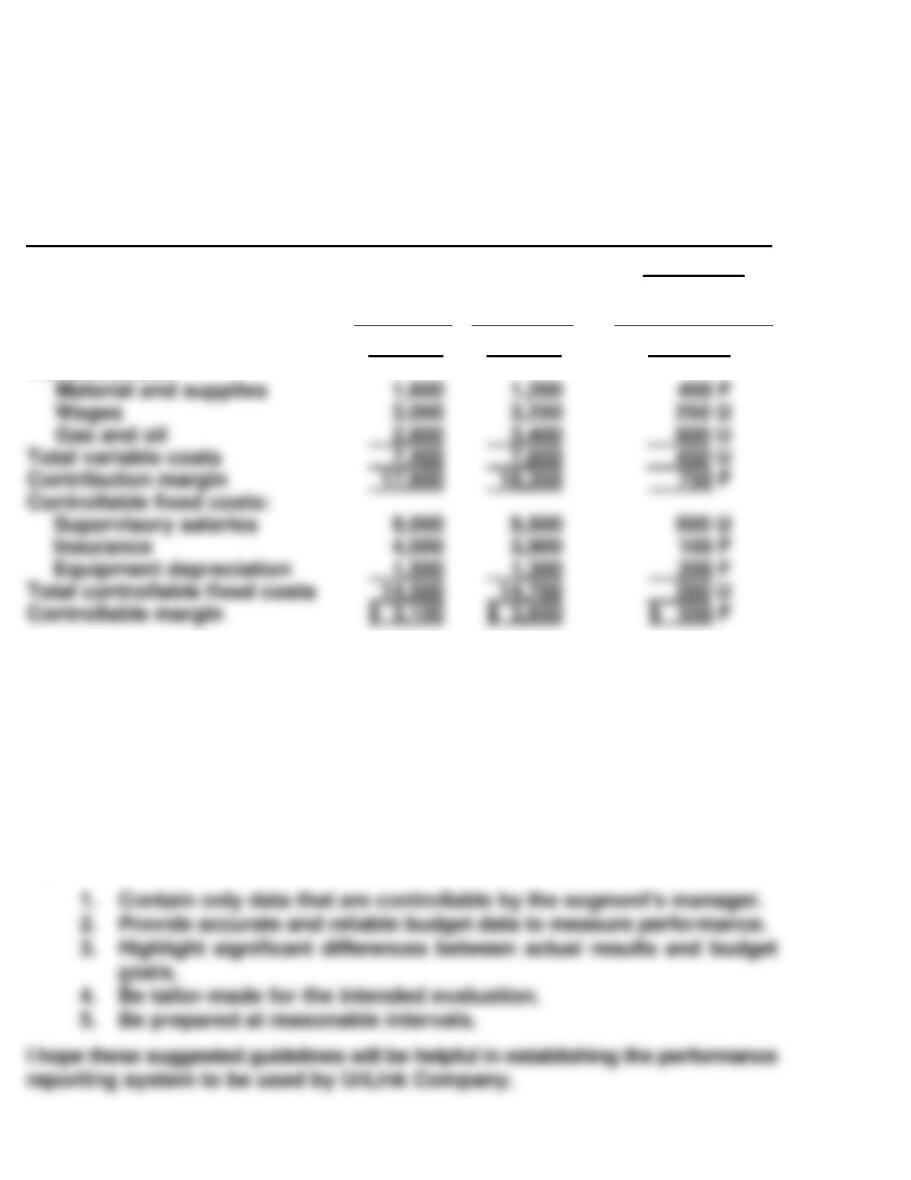

(b)

MEMO

TO: Lenny Kirkland

FROM: Student

SUBJECT: The Reporting Principles of Performance Reports

When evaluating the performance of a company’s segments, the performance

reports should:

2,800

3,400

Total variable costs

7,400

7,850

Contribution margin

Controllable fixed costs:

1,500

1,300

Total controllable fixed costs

Controllable margin

$ 3,100

$ 3,650

EXERCISE 10-12

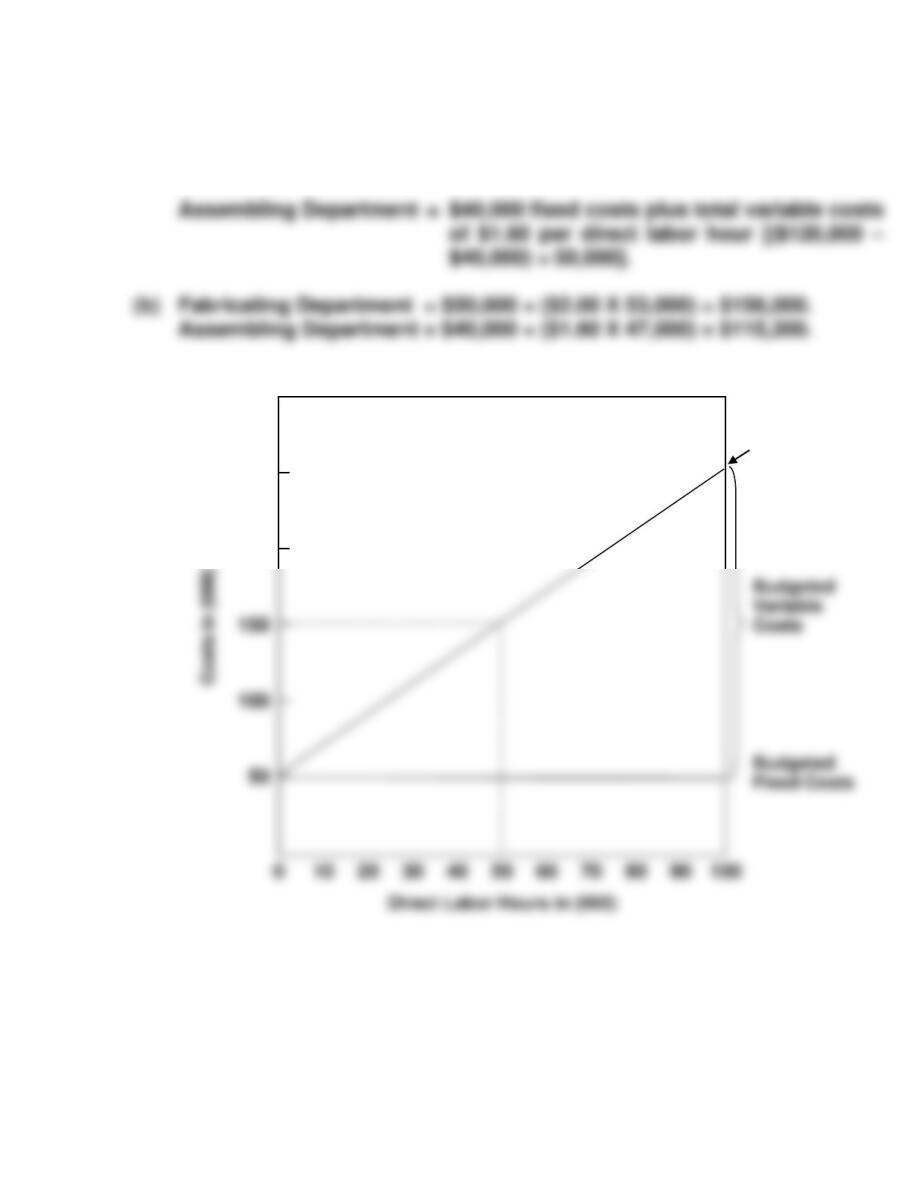

(a) Fabricating Department = $50,000 fixed costs plus total variable costs

of $2.00 per direct labor hour [($150,000 –

$50,000) ÷ 50,000].

(c)

$300

150

100

Total

Budgeted

Cost Line

250

200

EXERCISE 10-13

(a)

To Dallas Department Manager—Finishing Month: July

Controllable Costs:

Budget

Actual

Fav/Unfav

Direct Materials

$ 44,000

$ 42,500

$1,500 F

(b)

To Assembly Plant Manager—Dallas Month: July

Controllable Costs:

Budget

Actual

Fav/Unfav

Dallas Office

$ 92,000

$ 95,000

$3,000 U

(c)

To Vice President—Production Month: July

Controllable Costs:

Budget

Actual

Fav/Unfav

V P Production

Assembly plants:

Atlanta

$ 130,000

420,000

$ 132,000

424,000

$2,000 U

4,000 U

EXERCISE 10-14

(a) MALONE COMPANY

Mixing Department

Responsibility Report

For the Month Ended January 31, 2017

Controllable Cost

Budget

Actual

Difference

Indirect labor

$12,000

$12,250

$ 250 UU

(b) Most likely, when management examined the responsibility report for

January, they would determine that the differences were insignificant

for indirect labor (2.1% of budget), lubricants (1.5%), and maintenance

EXERCISE 10-15

(a) 1. Controllable margin ($270,000 – $100,000) $170,000

EXERCISE 10-15 (Continued)

(b) HORATIO INC.

Women’s Shoe Division

Responsibility Report

For the Month Ended June 30, 2017

Difference

Budget

Actual

Favorable F

Unfavorable U

Sales

$600,000

$600,000

$ 0 U

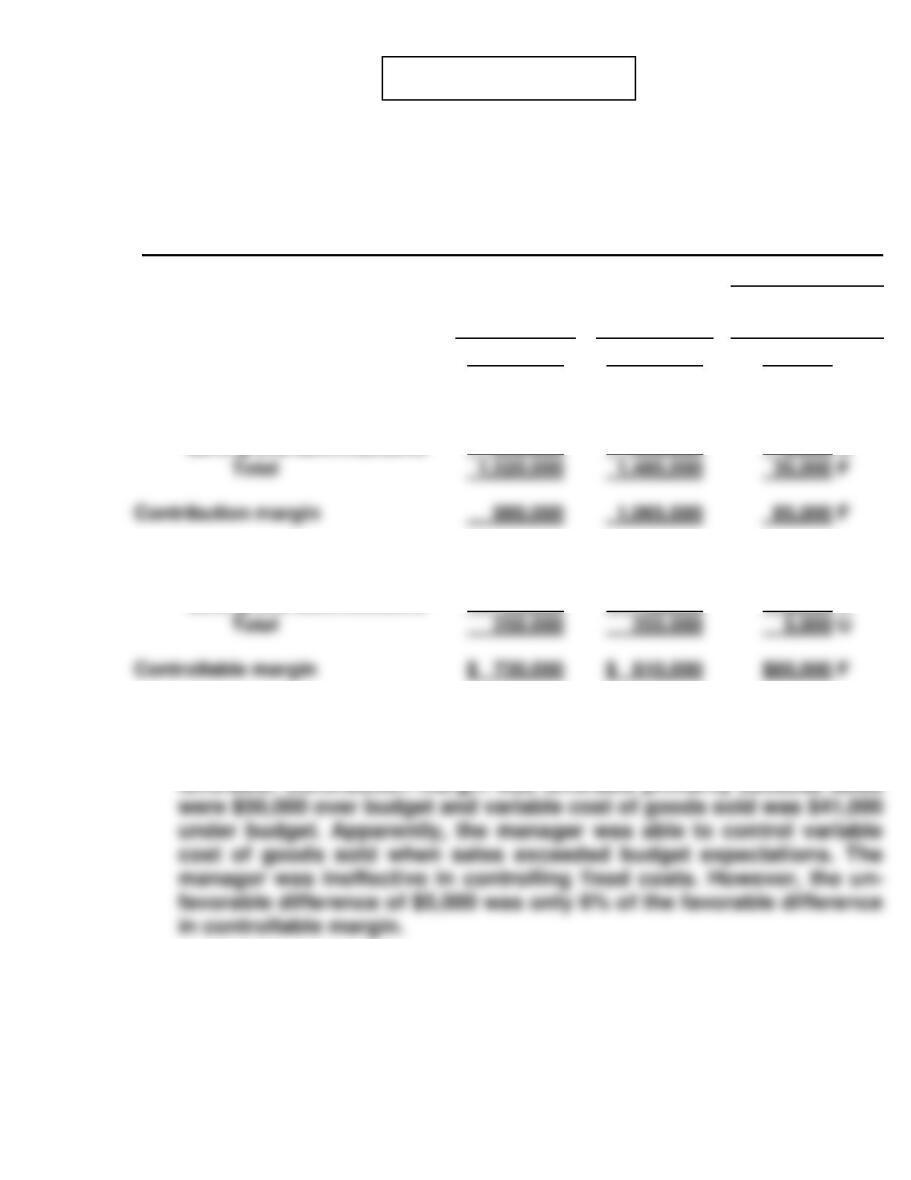

EXERCISE 10-16

(a) HARRINGTON COMPANY

Sports Equipment Division

Responsibility Report

2017

Budget

Actual

Difference

Sales

$900,000

$880,000

$20,000 U

Variable costs

Cost of goods sold

440,000

408,000

32,000 F

Selling and administrative

60,000

61,000

1,000 U

Total

Contribution margin

400,000

411,000

11,000 F

105,000

Selling and administrative

90,000

66,000

Total

Controllable margin

$210,000

$240,000

$30,000 F

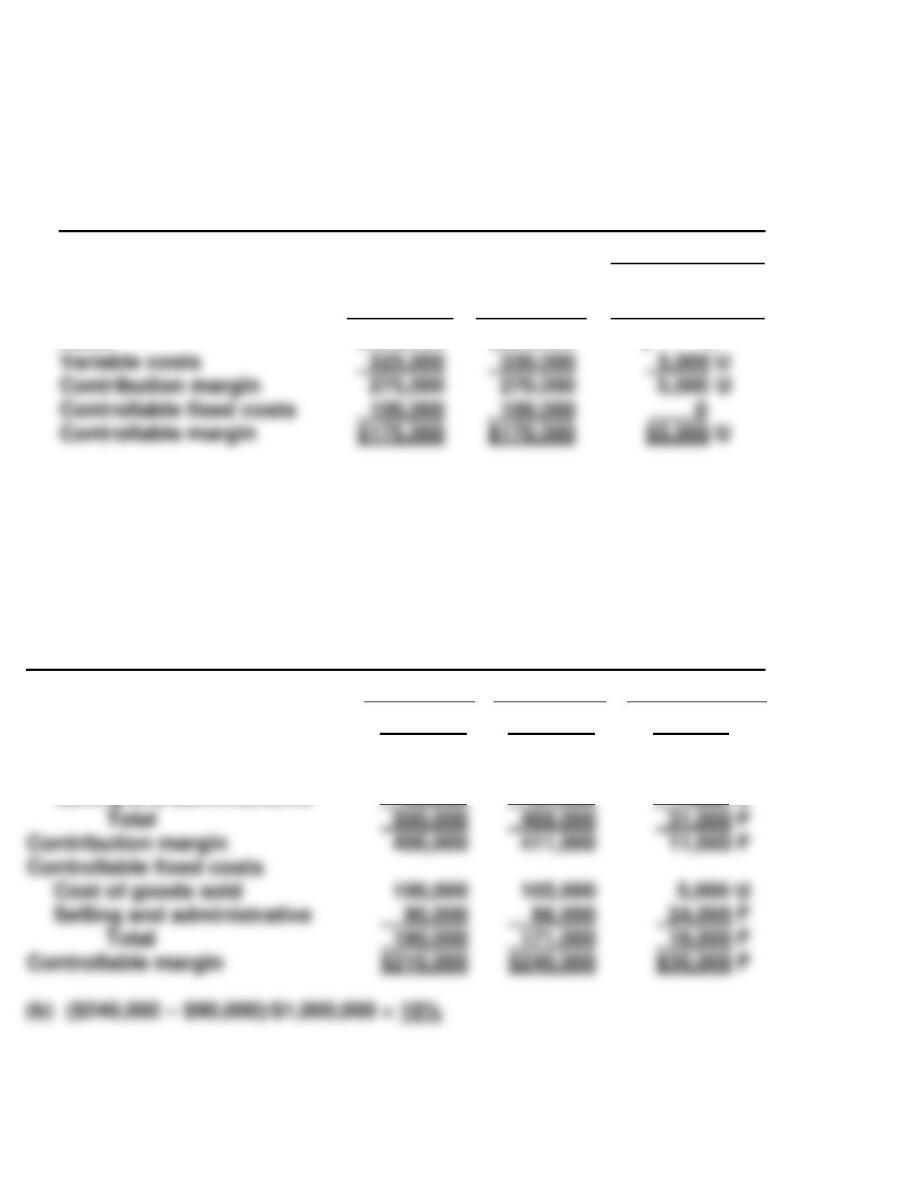

EXERCISE 10-17

(a) Controllable margin = ($3,000,000 – $1,950,000 – $600,000) = $450,000

(b) 1. Contribution margin percentage is 35%, or ($1,050,000 ÷ $3,000,000)

Increase in controllable margin = $300,000 X 35% = $105,000

ROI = ($450,000 + $105,000) ÷ $5,000,000 = 11.1%

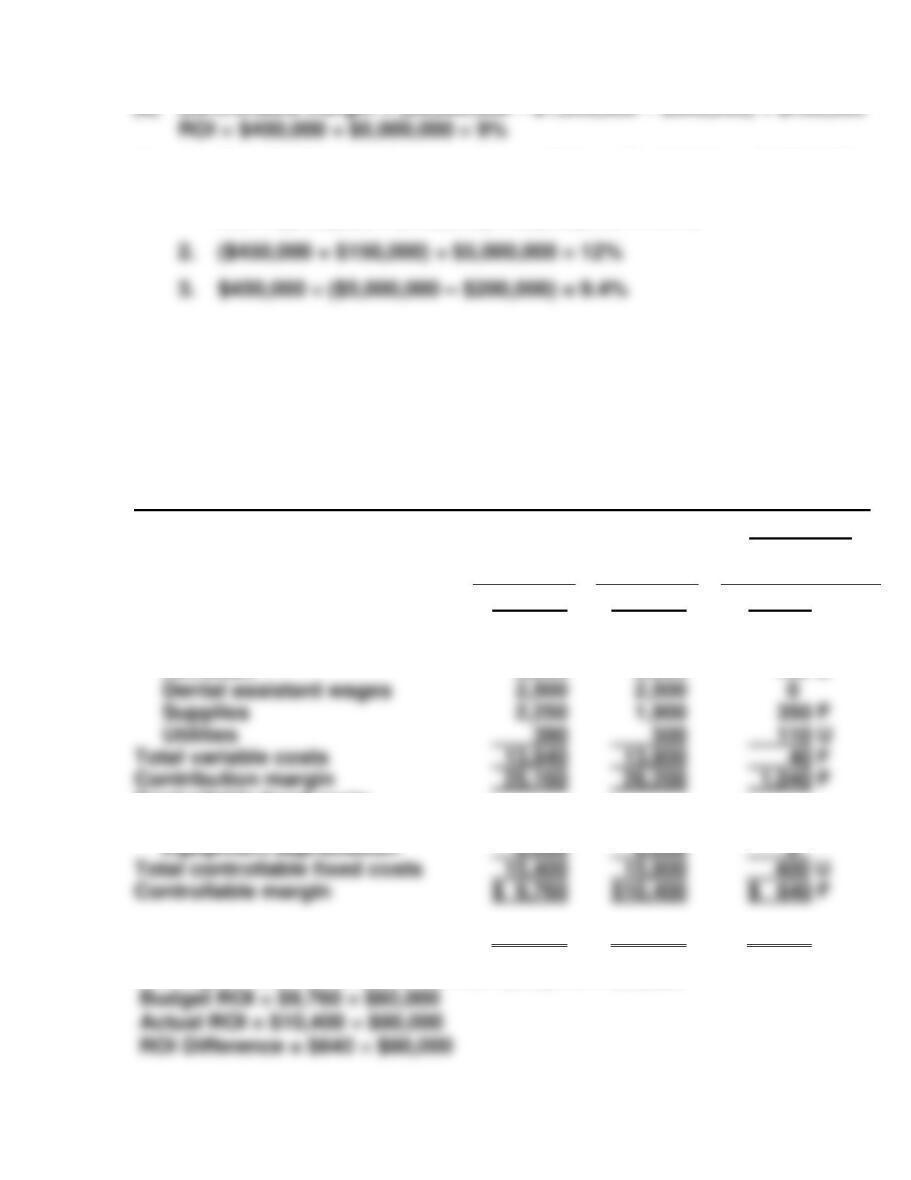

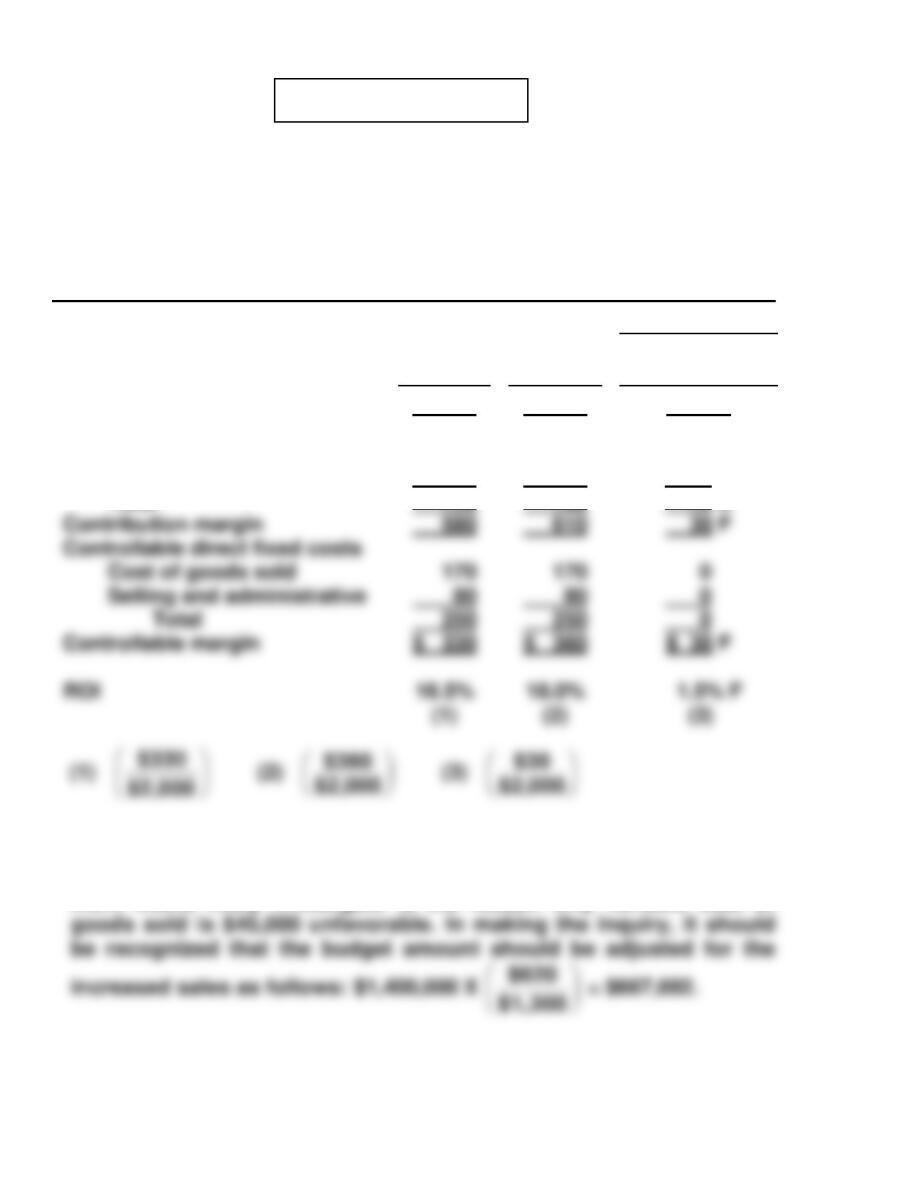

EXERCISE 10-18

(a) DINKLE AND FRIZELL DENTAL CLINIC

Preventive Services

Responsibility Report

For the Month Ended May 31, 2017

Budget

Actual

Difference

Favorable F

Unfavorable U

Service revenue

$39,000

$40,000

$1,000 F

Variable costs

Filling materials

4,900

5,000

100 U

Novocain

3,800

3,900

100 U

Dental assistant wages

2,500

2,500

Supplies

2,250

1,900

Utilities

390

500

110 U

Total variable costs

40 F

Contribution margin

Controllable fixed costs

Dentist salary

9,400

9,800

400 U

Equipment depreciation

6,000

6,000

Controllable margin

$ 9,760

$10,400

$ 640 F

Return on investment*

12.2%

13.0%

0.8% F

*Average investment = ($82,400 + $77,600) ÷ 2 = $80,000

EXERCISE 10-18 (Continued)

(b)

MEMO

TO: Drs. Reese Dinkle and Anita Frizell

FROM: Student

SUBJECT: Deficiencies in the Current Responsibility Reporting System

The current reporting system has the following deficiencies:

1. It does not clearly show both budgeted goals and actual performance.

2. It does not indicate the contribution margin generated by the center,

EXERCISE 10-19

Planes:

ROI = Controllable margin ÷ Average operating assets

12% = Controllable margin ÷ $25,000,000

Contribution margin = Controllable margin + Controllable fixed costs

= $3,000,000 + $1,500,000

Taxis:

ROI

=

Controllable margin

÷

Average operating assets

10%

=

$80,000

÷

Average operating assets

Average operating assets

=

$80,000 ÷ 10%

Contribution margin

Controllable fixed costs

$250,000 – $80,000

Contribution margin

=

Service revenue – Variable costs

=

$500,000 – Variable costs

=

$250,000

EXERCISE 10-19 (Continued)

Limos:

ROI = Controllable margin ÷ Average operating assets

= $210,000 ÷ $1,500,000

= 14%

Controllable margin

=

Contribution margin

–

Controllable fixed costs

$210,000

=

$480,000

–

Controllable fixed costs

*EXERCISE 10-20

(a) North Division: ROI = $140,000 ÷ $1,000,000 = 14%

West Division: ROI = $360,000 ÷ $2,000,000 = 18%

Service revenue

Variable costs

$780,000

*EXERCISE 10-20 (Continued)

(c) 1. If ROI is used to measure performance, only the North Division

(with a 14% ROI) and the South Division (with a 14% ROI) would

make the additional investment that provides a 16% ROI. The West

*EXERCISE 10-21

(a)

ROI

=

Controllable margin

÷

Average operating assets

(b)

Controllable margin

–

(Minimum rate of return X Average operating assets)

=

Residual income

$200,000

–

(Minimum rate of return X $1,250,000)

=

$100,000

$100,000

=

Minimum rate of return

(c)

Controllable margin

–

(Minimum rate of return X Average operating assets)

=

Residual income

Controllable margin

–

(11% X $1,200,000)

=

$204,000

Controllable margin

SOLUTIONS TO PROBLEMS

PROBLEM 10-1A

(a) BUMBLEBEE COMPANY

Packaging Department

Monthly Manufacturing Overhead Flexible Budget

For the Year 2017

Activity level

Direct labor hours

Variable costs

Indirect labor ($.42)*

Indirect materials ($.30)

($1.25)

Fixed costs

Supervision**

Depreciation

27,000

$11,340

8,100

8,000

6,000

2,500

30,000

$12,600

9,000

8,000

6,000

2,500

33,000

$13,860

9,900

8,000

6,000

2,500

36,000

$15,120

10,800

8,000

6,000

2,500

PROBLEM 10-1A (Continued)

(b) BUMBLEBEE COMPANY

Packaging Department

Manufacturing Overhead Flexible Budget Report

For the Month Ended October 31, 2017

Difference

Direct labor hours (DLH)

Variable costs

Indirect labor

Indirect materials

Repairs

Budget at

27,000 DLH

$11,340

8,100

6,210

Actual Costs

27,000 DLH

$12,432

7,680

6,100

Favorable F

Unfavorable U

$1,092 U

420 F

110 F

(c) The overall performance of management was slightly unfavorable.

Total costs

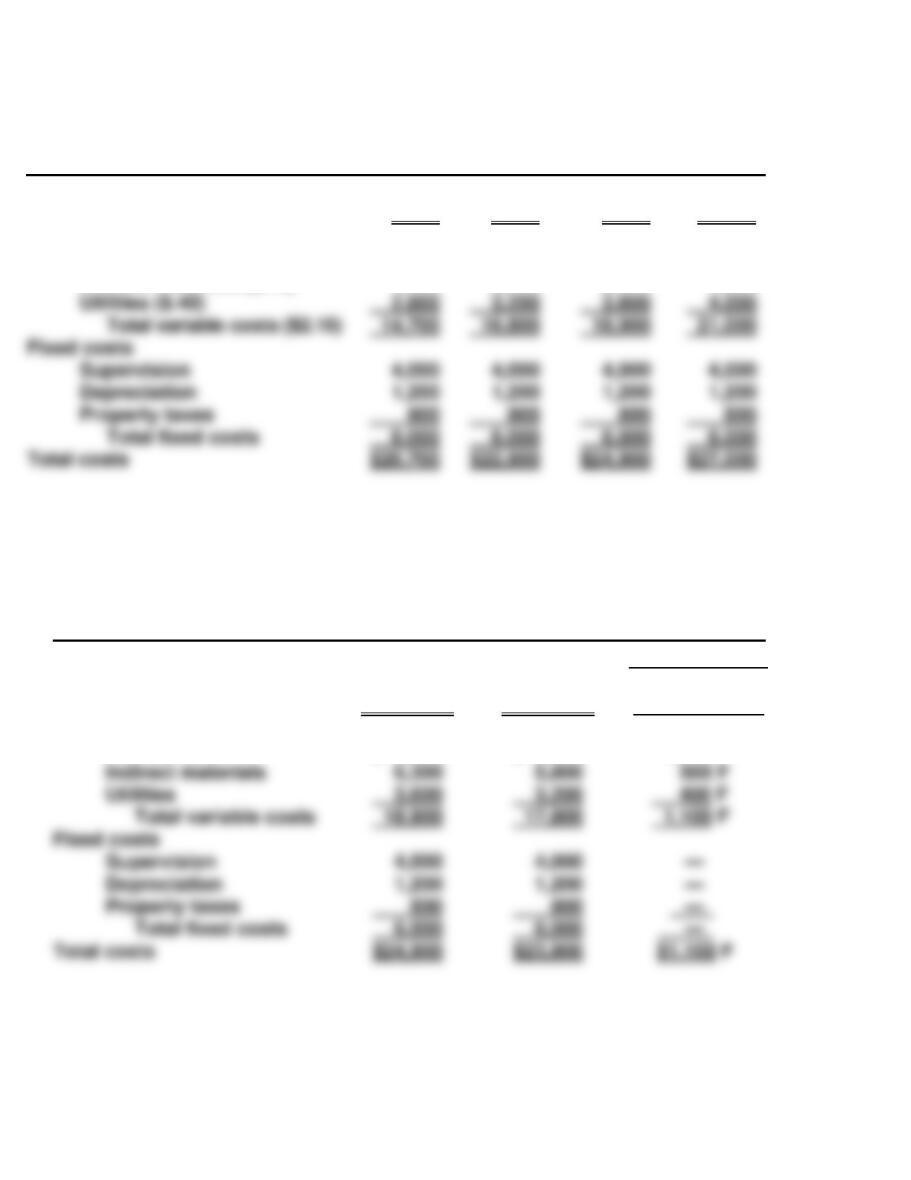

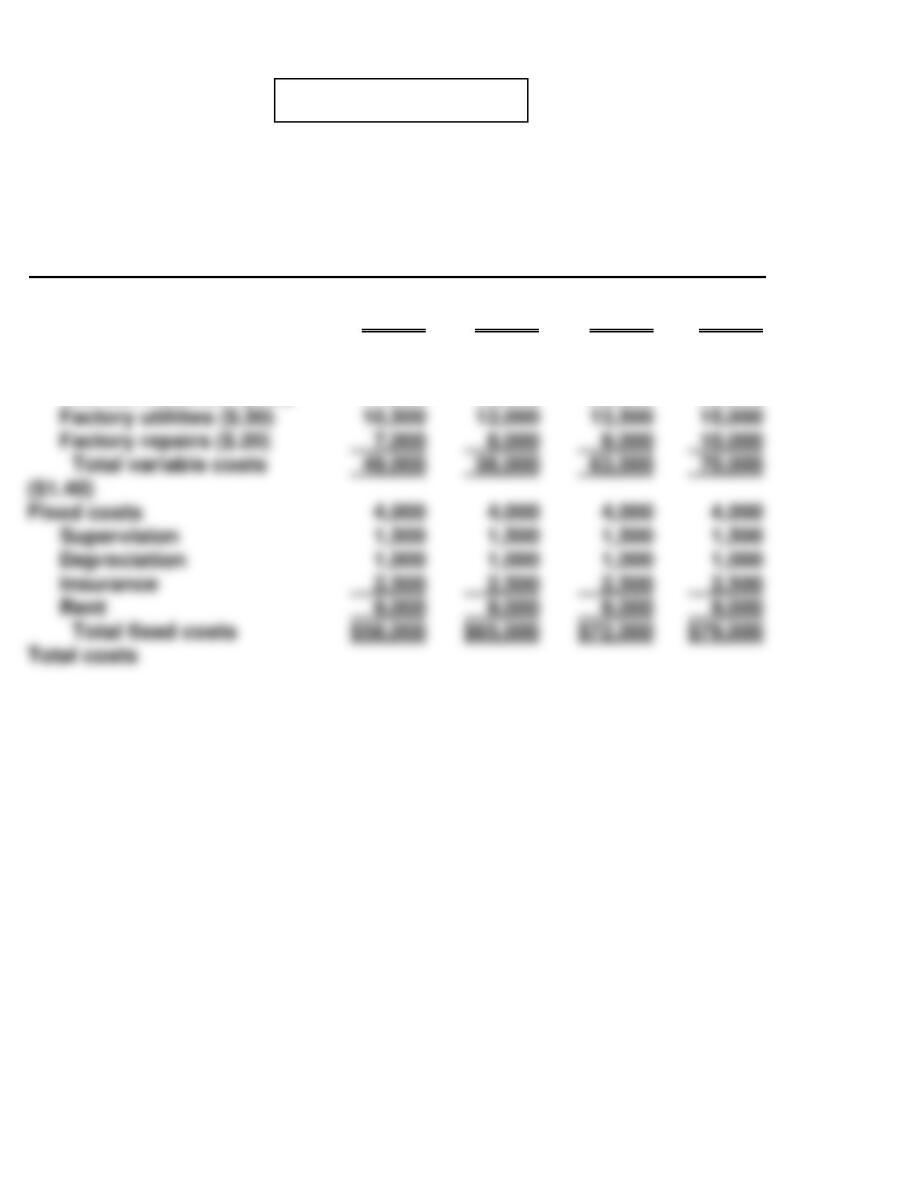

PROBLEM 10-2A

(a) ZELMER COMPANY

Monthly Manufacturing Overhead Flexible Budget

Ironing Department

For the Year 2017

Activity level

Direct labor hours

Variable costs

Indirect labor ($.40)

Indirect materials ($.50)

35,000

$14,000

17,500

40,000

$16,000

20,000

45,000

$18,000

22,500

50,000

$20,000

25,000

PROBLEM 10-2A (Continued)

(b) ZELMER COMPANY

Ironing Department

Manufacturing Overhead Flexible Budget Report

For the Month Ended June 30, 2017

Difference

Direct labor hours (DLH)

Variable costs

Indirect labor

Indirect materials

Fixed costs

Supervision*

Depreciation

Insurance

Budget at

41,000 DLH

$16,400 (1)

20,500 (2)

4,000

1,500

1,000

Actual Costs

41,000 DLH

$18,040 (5)

19,680 (6)

4,000

1,500

1,000

Favorable F

Unfavorable U

$1,640 U

820 F

0 U

0 U

0 U

(c) The manager was ineffective in controlling variable costs ($3,690 U).

Fixed costs were effectively controlled.

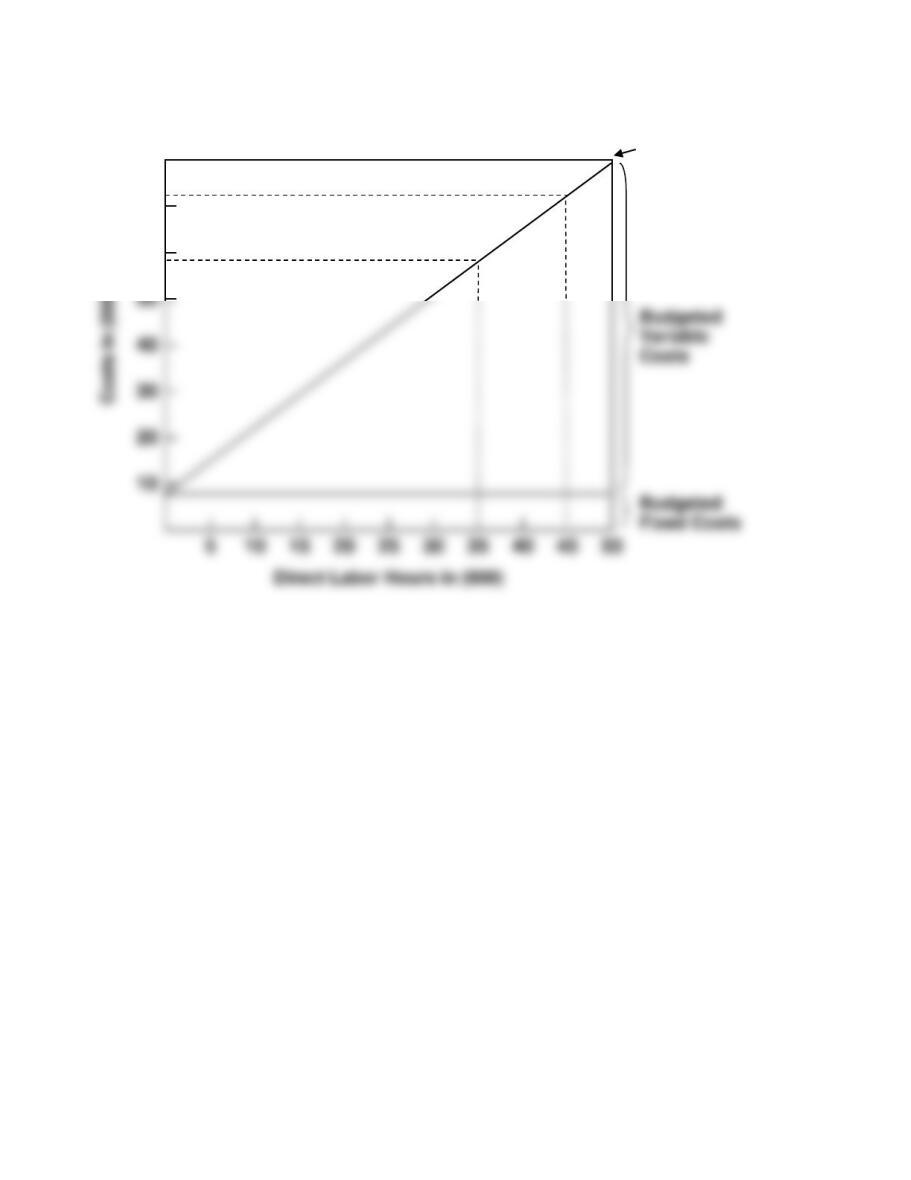

PROBLEM 10-2A (Continued)

(e)

$80

Total

Budgeted

Cost Line

70

60

40

30

10

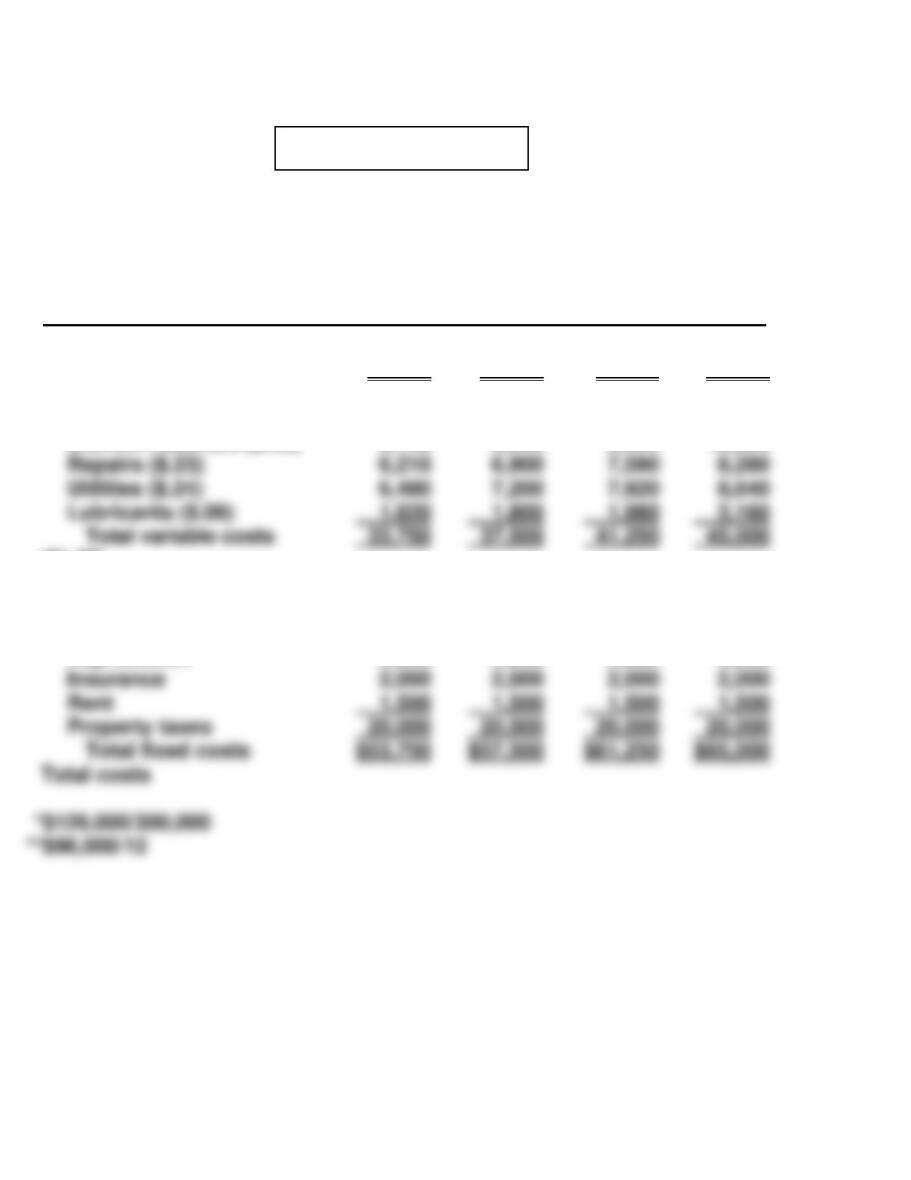

PROBLEM 10-3A

(a) The formula is fixed costs $35,000 plus variable costs of $2.85 per unit

($171,000 ÷ 60,000 units).

(b) RATCHET COMPANY

Assembling Department

Flexible Budget Report

For the Month Ended August 31, 2017

Difference

Units

Variable costs*

Direct materials ($.80 X 58,000)

Direct labor ($.90 X 58,000)

Fixed costs

Rent

Supervision

Depreciation

Total fixed

Total costs

Budget at

58,000 Units

$ 46,400

52,200

12,000

17,000

6,000

35,000

$200,300

Actual Costs

58,000 Units

$ 47,000

51,200

12,000

17,000

6,000

35,000

$202,200

Favorable F

Unfavorable U

$ 600 U

1,000 F

0 U

0 U

0 U

0 U

$1,900 U

*Note that the per unit variable costs are computed by taking the

budget amount at 60,000 units and dividing it by 60,000. For example,

$48,000

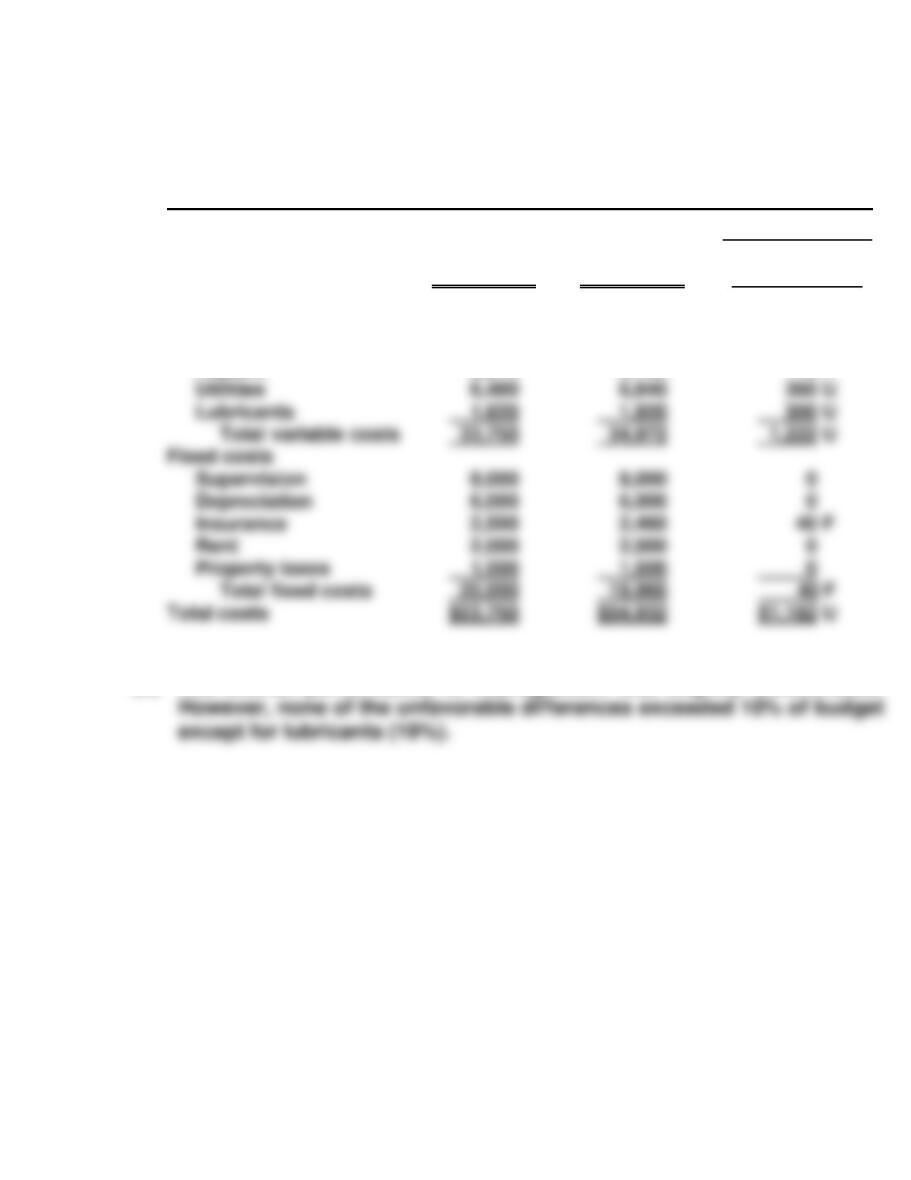

PROBLEM 10-3A (Continued)

(c) RATCHET COMPANY

Assembling Department

Flexible Budget Report

For the Month Ended September 30, 2017

Difference

Units

Variable costs

Direct materials ($.80 X 64,000)

Direct labor ($.90 X 64,000)

Indirect materials ($.40 X 64,000)

Indirect labor ($.30 X 64,000)

Budget at

64,000 Units

$ 51,200

57,600

25,600

19,200

Actual Costs

64,000 Units

$ 51,700

56,320

26,620

19,250

Favorable F

Unfavorable U

$ 500 U

1,280 F

1,020 U

50 U

The manager’s performance was slightly better in September than it

was in August. However, each variable cost was slightly over budget

again except for direct labor.

Note that actual variable costs in September were 10% higher than

the actual variable costs in August. Therefore to find the actual vari–

able costs in September, the actual variable costs in August must be

increased 10% as follows:

August

(actual)

September

(actual)

Direct materials

Direct labor

$ 47,000 X 110%

51,200 X 110%

=

$ 51,700

56,320

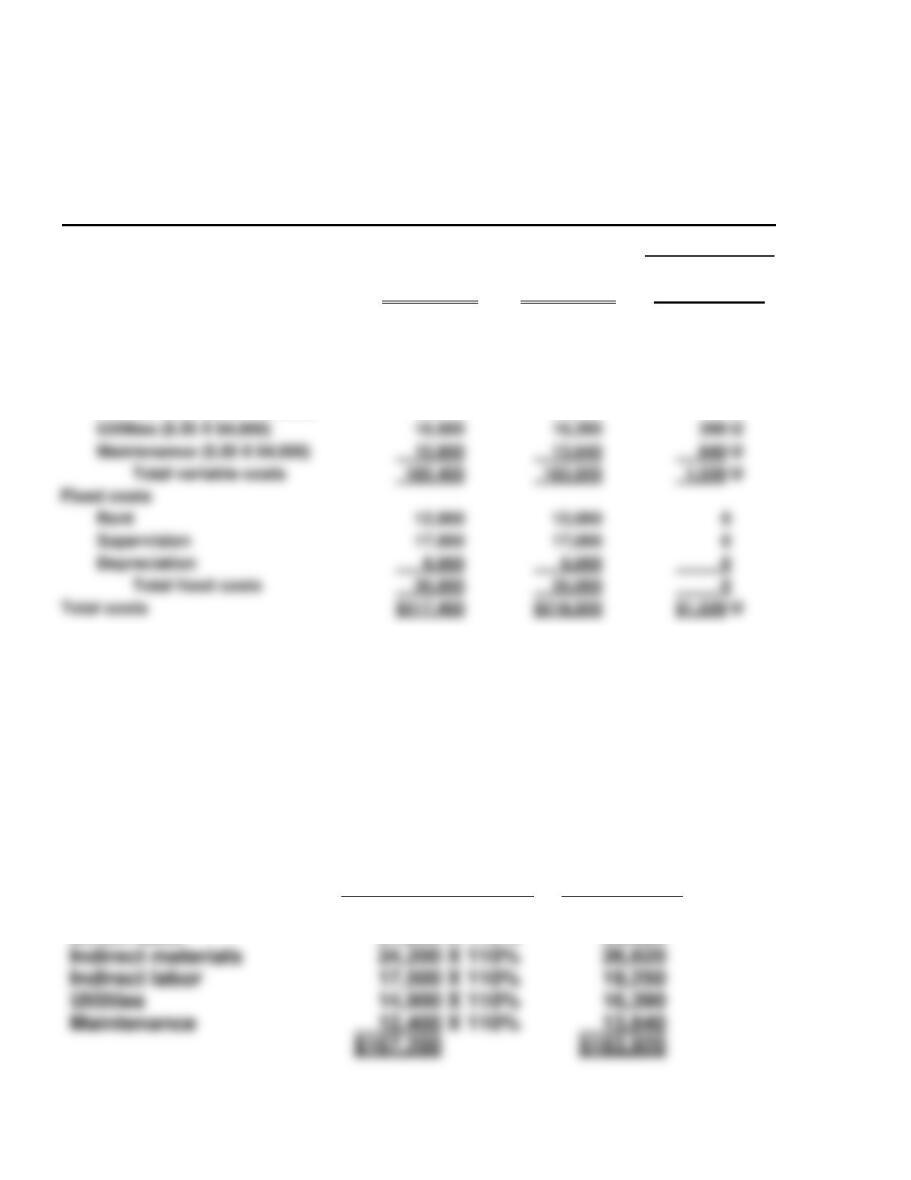

PROBLEM 10-4A

(a) CLARKE INC.

Patio Furniture Division

Responsibility Report

For the Year Ended December 31, 2017

Difference

Budget

Actual

Favorable F

Unfavorable U

Sales

Variable costs

Cost of goods sold

Selling and administrative

Controllable fixed costs

Cost of goods sold

Selling and administrative

$2,500,000

1,300,000

220,000

200,000

50,000

$2,550,000

1,259,000

226,000

203,000

52,000

$50,000 F

41,000 F

6,000 U

3,000 U

2,000 U

(b) The manager effectively controlled revenues and costs. Contribution

margin was $85,000 favorable and controllable margin was $80,000

(c) Two costs are excluded from the report: (1) noncontrollable fixed costs

and (2) indirect fixed costs. The reason is that neither cost is control-

lable by the Patio Furniture Division Manager.

PROBLEM 10-5A

(a) OPTIMUS COMPANY

Home Division

Responsibility Report

For the Year Ended December 31, 2017

(in thousands of dollars)

Difference

Budget

Actual

Favorable F

Unfavorable U

Sales

Variable costs

Cost of goods sold

Selling and administrative

Total

$1,300

620

100

720

$1,400

665

125

790

$100 F

45 U

25 U

70 U

(b) The performance of the manager of the Home Division was slightly

above budget expectations for the year. The item that top manage-

ment would likely investigate is the reason why variable cost of

(3)

PROBLEM 10-5A (Continued)

(c) 1.

$360,000 + ($665,000 X 5%)

$2,000,000

= 19.7%.

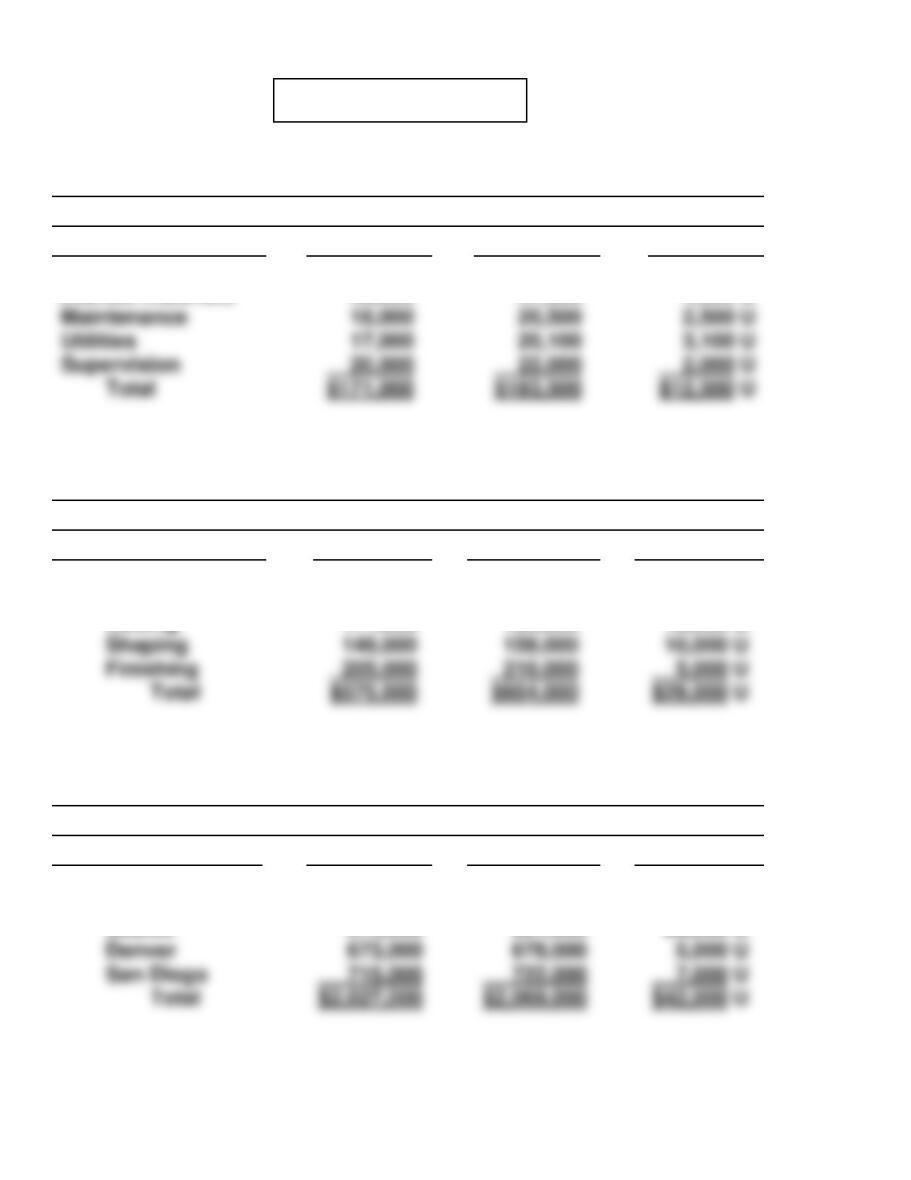

PROBLEM 10-6A

(a) No. 1

To Cutting Department Manager—Seattle Division Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

Indirect labor

Indirect materials

$ 70,000

46,000

$ 73,000

47,900

$ 3,000 U

1,900 U

No. 2

To Division Production Manager—Seattle Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

Seattle Division

Departments:

Cutting

$ 51,000

171,000

$ 52,500

183,500

$ 1,500 U

12,500 U

No. 3

To Vice President—Production Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

V-P Production

Divisions:

Seattle

$ 64,000

575,000

$ 65,000

604,000

$ 1,000 U

29,000 U

PROBLEM 10-6A (Continued)

No. 4

To President Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

President

Vice-Presidents:

Production

$ 74,200

2,027,000

$ 76,400

2,069,000

$ 2,200 U

42,000 U

(b) 1. Within the Seattle division the rankings of the department man-

agers were: (1) Finishing, (2) Shaping, and (3) Cutting. If the rankings

*PROBLEM 10-7A

(a) 1. ROI = Controllable Margin ÷ Average Operating Assets

ROI = $2,460,000 ÷ $12,300,000

ROI = 20%

2. Residual Income = Controllable Margin – (Minimum Rate of

Return X Average Operating Assets)

investment opportunity it had in 2017 if residual income had been

used as the performance measure because an increase in residual

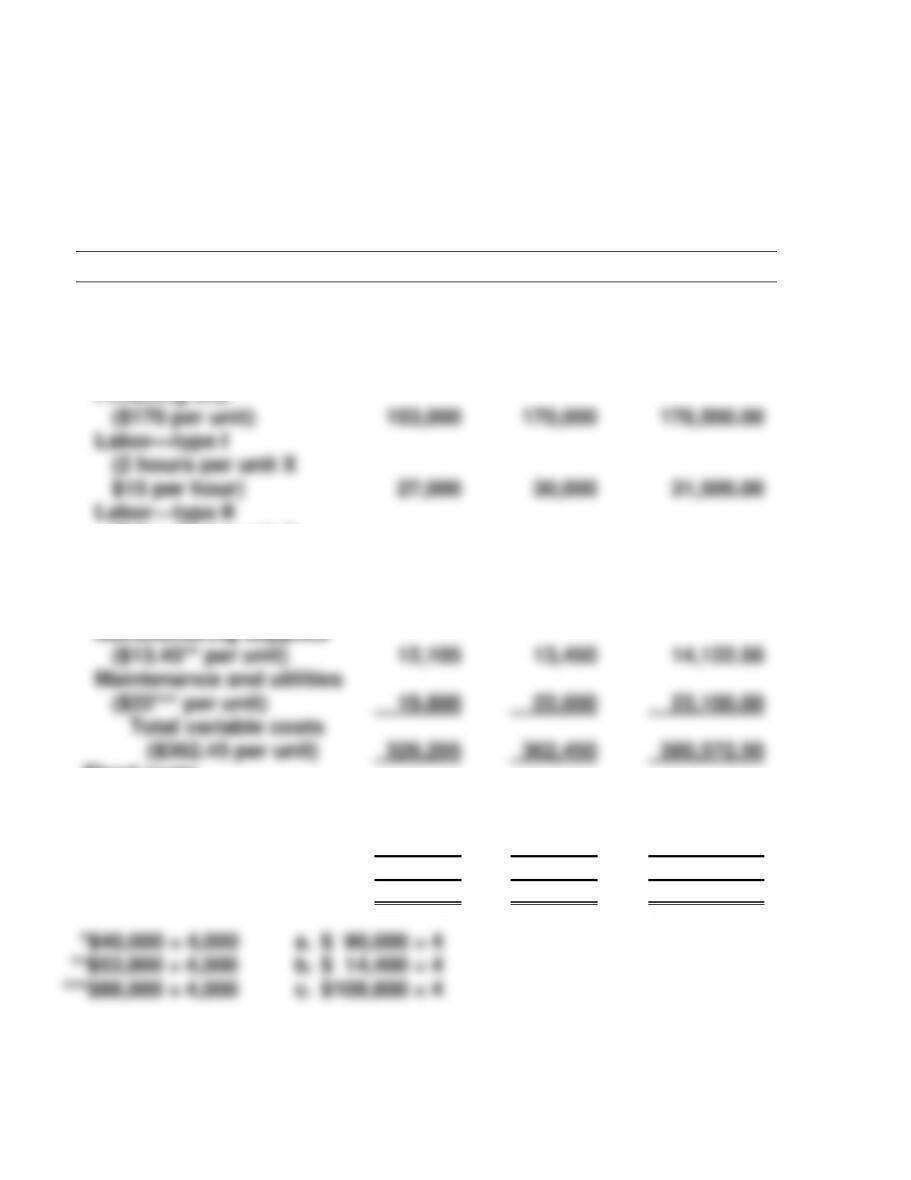

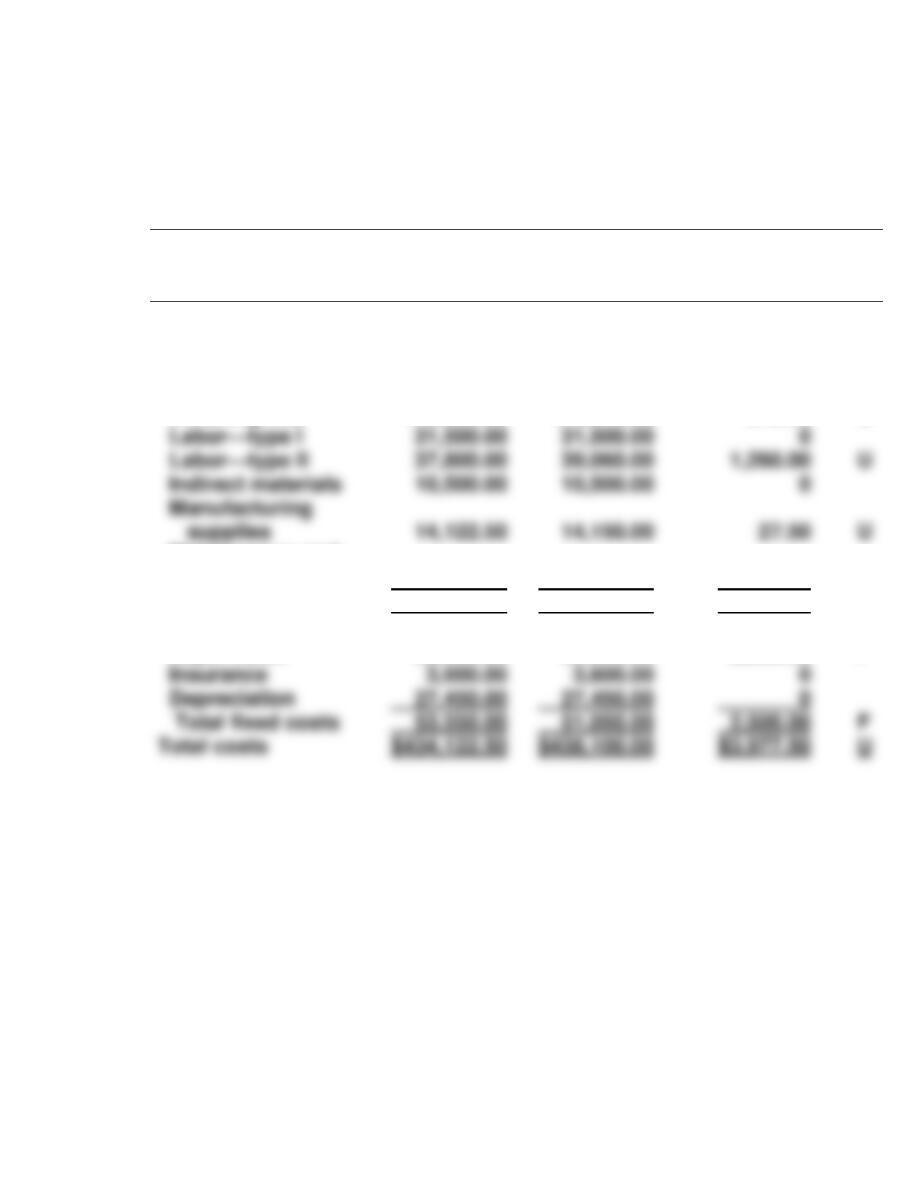

CD10 CURRENT DESIGNS

(a) Current Designs

Rotomolded Line

Manufacturing Budget

For the Year Ended December 31, 2017

4,000 kayaks

Units to be produced

Calculation

Amount budgeted

Costs:

Variable costs

Polyethylene powder

4,000 X 54 X $1.50

$ 324,000

Finishing kits

4,000 X $170

680,000

Labor—type I

4,000 X 2 X $15

120,000

Labor—type II

4,000 X 3 X $12

Indirect materials

Manufacturing supplies

Maintenance and utilities

88,000

Total variable costs

Fixed costs

Supervision

Insurance

Depreciation

Total fixed costs

214,200

Total costs

CD10 (Continued)

(b) Current Designs

Rotomolded Line

Manufacturing Flexible Budget Report

For the Quarter Ended March 31, 2017

Units to be produced

900 kayaks

1,000 kayaks

1,050 kayaks

Costs:

Variable costs

Polyethylene powder

(54 X 1.50 per unit)

$ 72,900

$ 81,000

$ 85,050.00

(3 hours per unit X

$12 per hour)

32,400

36,000

37,800.00

Indirect materials

($10* per unit)

9,000

10,000

10,500.00

($13.45** per unit)

12,105

13,450

14,122.50

Maintenance and utilities

($22*** per unit)

19,800

22,000

23,100.00

Total variable costs

($362.45 per unit)

Fixed costs

Supervision (a.)

22,500

22,500

22,500.00

Insurance (b.)

3,600

3,600

3,600.00

Depreciation (c.)

27,450

27,450

27,450.00

Total fixed costs

53,550

53,550

53,550.00

Total costs

$379,755

$416,000

$434,122.50

Finishing kits

($170 per unit)

170,000

(2 hours per unit X

$15 per hour)

27,000

30,000

31,500.00

CD10 (Continued)

(c) Current Designs

Rotomolded Line

Manufacturing Flexible Budget Report

For the Quarter Ended March 31, 2017

Units to be produced

Budget for

1,050 kayaks

Actual costs for

1,050 kayaks

Difference

F = favorable

U = unfavorable

Costs:

Variable costs

Polyethylene

powder

$ 85,050.00

$ 87,000.00

$1,950.00

U

Finishing kits

178,500.00

178,840.00

340.00

U

Maintenance and

utilities

23,100.00

26,000.00

2,900.00

U

Total variable costs

380,572.50

387,050.00

6,477.50

U

Fixed costs

Supervision

22,500.00

20,000.00

2,500.00

F

Depreciation

27,450.00

27,450.00

Total fixed costs

53,550.00

51,050.00

2,500.00

F

Total costs

$434,122.50

$438,100.00

$3,977.50

U

Labor—type I

31,500.00

31,500.00

U

Indirect materials

10,500.00

10,500.00

supplies

U

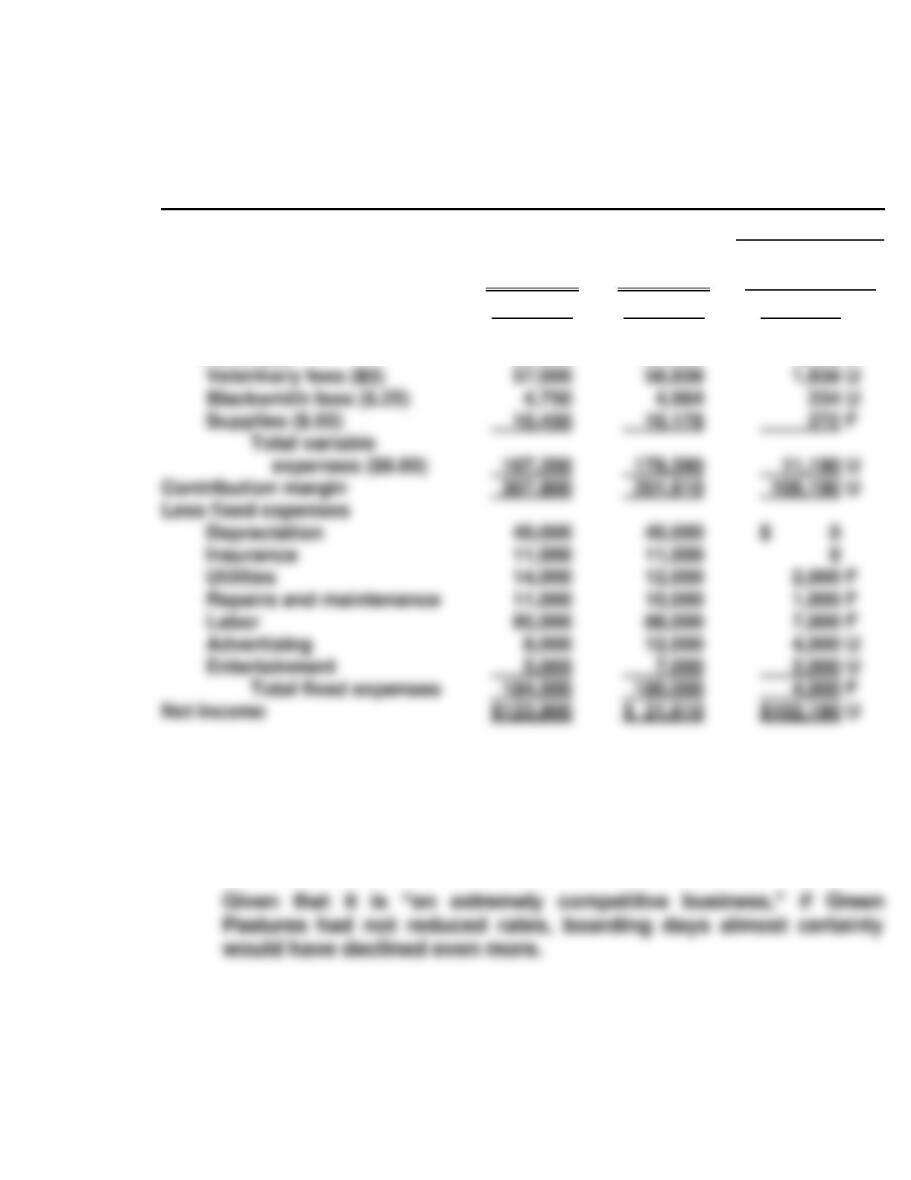

BYP 10-1 DECISION-MAKING ACROSS THE ORGANIZATION

(a) 1. The primary causes of the loss in net income were the decrease in

the number of boarding days and the decrease in the boarding

fee. The number of boarding days decreased by 2,900 or approxi-

mately 13% (2,900 days ÷ 21,900 days), and the boarding fee

2. Management did a poor job in controlling variable expenses.

Given that boarding days declined by about 13%, variable

expenses should decline by about 13%, or more precisely,

variable expenses should decline by $25,520

3. Management’s decisions to stay competitive probably were sound.

Given the decline in boarding days, the decision not to replace the

BYP 10-1 (Continued)

(b) GREEN PASTURES

Income Statement

Flexible Budget Report

For the Year Ended December 31, 2017

Difference

Boarding days (BD)

Sales ($25)

Less variable expenses

Feed ($5)

Budget at

19,000 BD

$475,000

95,000

Actual at

19,000 BD

$380,000

104,390

Favorable F

Unfavorable U

$ 95,000 U

9,390 U

(c) 1. The primary causes of the decrease in net income are the decreases

in boarding rates and volume. The average daily rate charged

was $20 = ($380,000 ÷ 19,000). This rate resulted in a decrease in

sales revenue of $95,000 or 20% = ($95,000 ÷ $475,000).

BYP 10-1 (Continued)

2. Management did a poor job of controlling variable expenses. These

expenses in total were $11,190 over budget or 6.7%, or ($11,190 ÷

$167,200).

(d) Given that the industry is “extremely competitive,” management should

consider two options. One, become the lowest cost operator. If Green

Pastures is the company with the lowest operating costs, it can under–

price its competitors and take customers away from them (increasing

BYP 10-2 MANAGERIAL ANALYSIS

(a) Mary Gammel—Profit Center: Responsible for sales, inventory cost,

advertising, sales personnel, printing, and travel. She is not responsible

for the assets invested in her division and probably does not control

the rent or depreciation costs either. As a profit center manager she

might have control of the insurance, but she probably does not.

(b) Mary Gammel Budget differences: The cost of goods sold is 28%

($42,000 ÷ $150,000) above budget and so should definitely be brought

to her attention. Travel is 30% ($6,000 ÷ $20,000) below budget.

Students may differ as to whether they believe that this should be

brought to her attention. The differences in rent and depreciation should

not be brought to her attention because she does not control those

costs.

BYP 10-2 (Continued)

Jose Gomez Budget differences: As manager of an investment center,

Mr. Gomez is responsible for all categories of the budget. The

selection in this case would be which differences merit his attention.

Any decrease in a company’s gross profit rate (gross profit ÷ sales) is

BYP 10-3 REAL-WORLD FOCUS

(a) The company’s costs do not increase proportionately with the revenues

increase in the third and fourth quarter because the behavior of the

costs is primarily fixed.

BYP 10-4 REAL-WORLD FOCUS

(a) The two most common pain points are (1) dealing with other managers

and (2) technology issues, mainly frustration of budgeting in Excel

spreadsheets.

(b) Of those companies that participated in the survey, 97 percent said

that they prepare annual budgets. Of those that prepare annual budgets,

60 percent say that they begin the process by determining sales

forecasts.

BYP 10-5 COMMUNICATION ACTIVITY

(a) Fred Bedner should be able to control all the variable costs and the

fixed costs of supervision (but not his portion) and inspection.

Insurance and depreciation ordinarily are not the responsibility of the

department manager.

(1,500 X $25) plus fixed costs ($35,000) or $72,500 ($37,500 + $35,000).

(c) FLEMING COMPANY

Production Department

Manufacturing Overhead Flexible Budget Report

For the Month Ended

Difference

Variable costs

Indirect materials ($11)

Indirect labor ($6)

Budget at

1,500 units

$16,500

9,000

Actual at

1,500 units

$22,500

13,500

Favorable F

Unfavorable U

$ 6,000 U

4,500 U

(d) A production department is a cost center. Thus, the report should include

only the costs that are controllable by the production manager. This

BYP 10-5 (Continued)

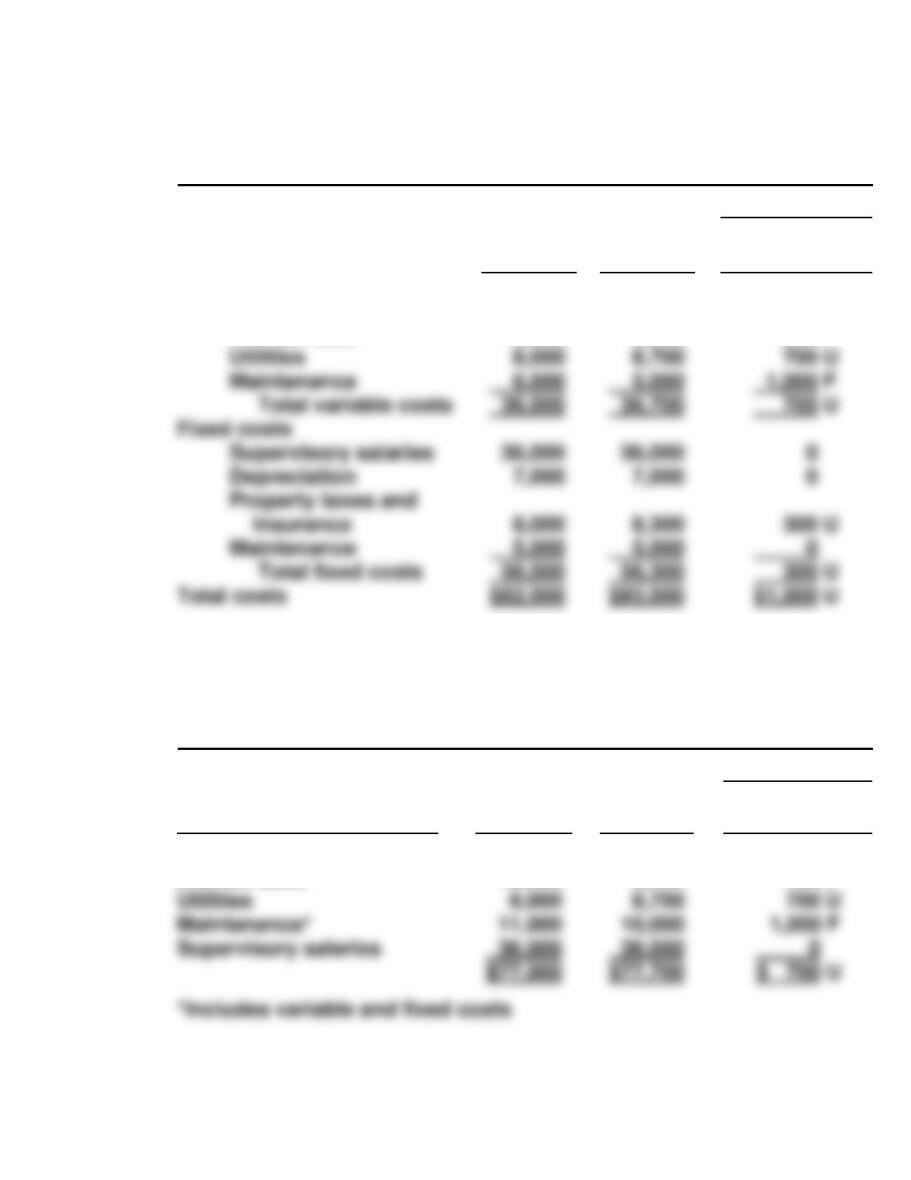

FLEMING COMPANY

Production Department

Manufacturing Overhead Responsibility Report

For the Month Ended

Difference

Controllable Cost

Budget

Actual

Favorable F

Unfavorable U

Indirect materials

Indirect labor

$16,500

9,000

$22,500

13,500

$ 6,000 U

4,500 U

*$10,000 is deducted from both budget and actual for Mr. Bedner’s cost.

To: Mr. Fred Bedner, Production Manager

From: , Vice President of Production

Subject: Performance Evaluation for the Month of XXXXX

BYP 10-5 (Continued)

Fred, it is imperative that you get costs under control in your department

as soon as possible.

BYP 10-6 ETHICS CASE

(a) The stakeholders in this ethical situation are:

The employees and managers of each investment center.

The central management and chief executive officer.

The customers who buy the product.

The owners or stockholders.

(b) Pressure to perform is a frequently identified cause for unethical

conduct. Employees are more prone to engage in unethical conduct

(c) The company might maintain open lines of communication with its em-

ployees to better know the pressures of its managers. By “keeping in

touch,” the company may avoid making unreasonable demands on its

managers and employees. The company might also develop a company

BYP 10-7 ALL ABOUT YOU

(a) The basic idea is to set up individual envelopes for different expense

categories. Once you have used up the money in a particular envelope,

you can’t use more. Begin by preparing a monthly budget. Identify

those items that you will pay in cash. These would include things like

groceries, eating out at restaurants, clothing, gasoline, car repairs, gifts,

(b) Answers will vary by student.

BYP 10-8 CONSIDERING YOUR COSTS AND BENEFITS

In general, in past years it has usually been considered prudent to

purchase a home rather than to rent. As noted, over time, home prices have

usually appreciated in most parts of the country. Mortgage interest

provides some tax relief, and by purchasing a home you get some control

over your housing costs. However, recent turbulence in the housing market

has made the decision more complicated. In some parts of the country

home prices have fallen considerably, and there is no indication how soon