CHAPTER 10: Standard Costing and Variance Analysis

E 10-58 ↓ links ↓

change here, please ↓

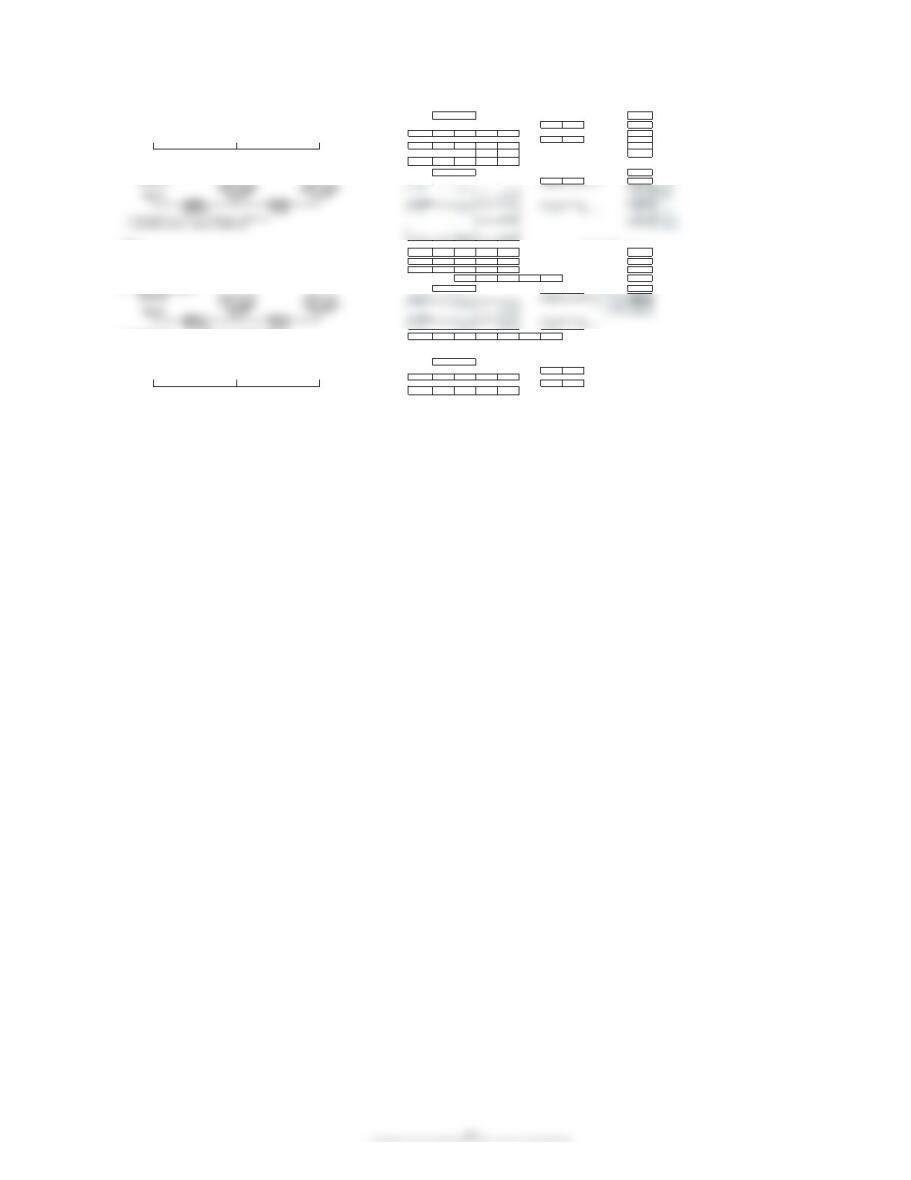

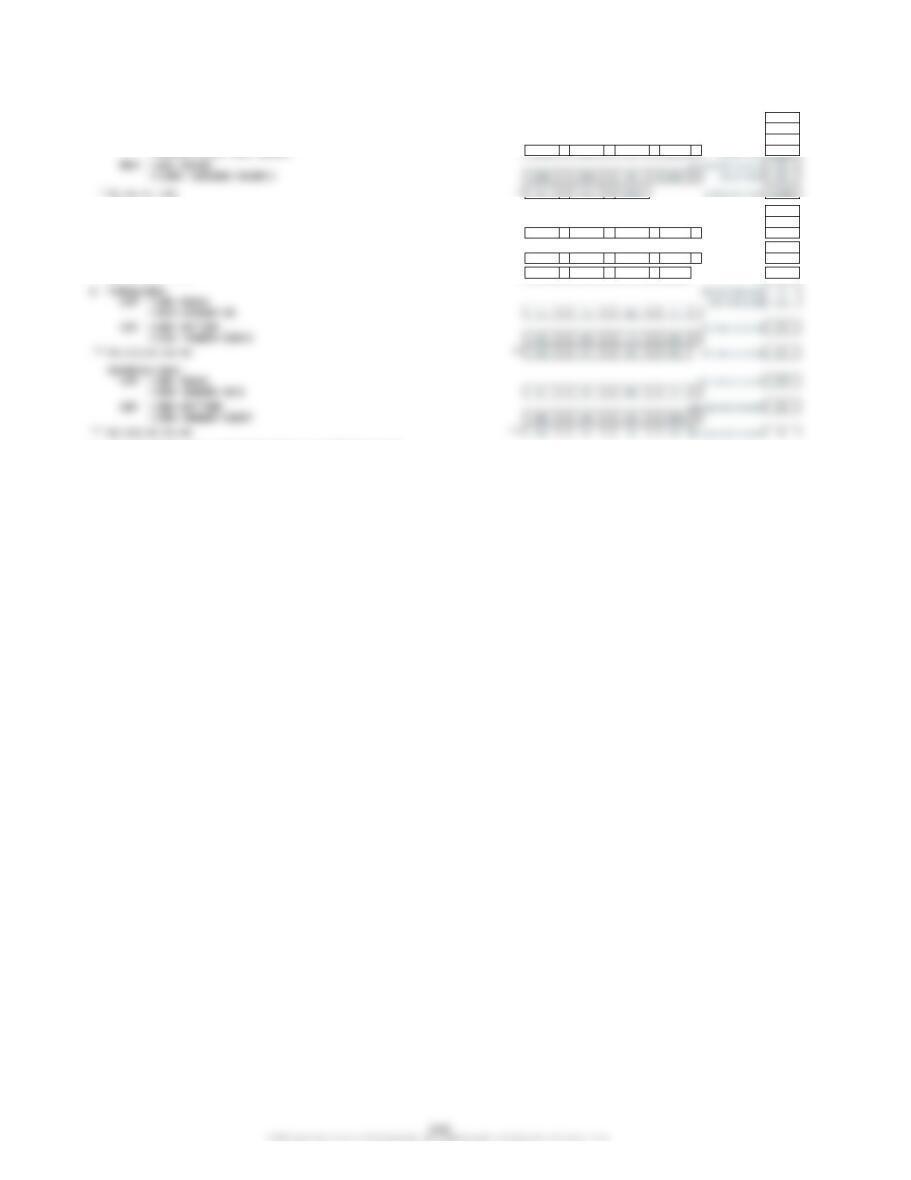

1. Variable overhead analysis: Actual VOH: 4Lbs. of RM reqd.

1,170 U Spending 36 DLH

0.70 × 158,900 = 111,230 18.00 wage rate

Applied VOH: (210) F Efficiency 2Hrs. reqd.

0.70 × 79,600 × 2 80,000 Practical volume

Standard hours: = 111,440 11.20 Direct materials

*Standard Hours = 2 hours × 79,600 units = 159,200 hours 2 × 79,600 = 159,200

2. Fixed overhead analysis: Actual FOH: 2.80 Lbs. rate

Budgeted FOH: (1,000) F Spending 18.10 Act. Wage rate

5.20 × 80,000 × 2 831,000 Fixed OH

Applied FOH: 158,900 DLH

*Practical Volume in Hours = 2 hours × 80,000 units = 160,000 hours = 827,840 5.20 Fixed O/H rate

$1,000 F

Spending

Budgeted FOH

$5.20 × 160,000*

$832,000

Actual FOH

$831,000

$4,160 U

Applied FOH

$5.20 × 159,200**

$827,840

E 10-59

change here, please ↓

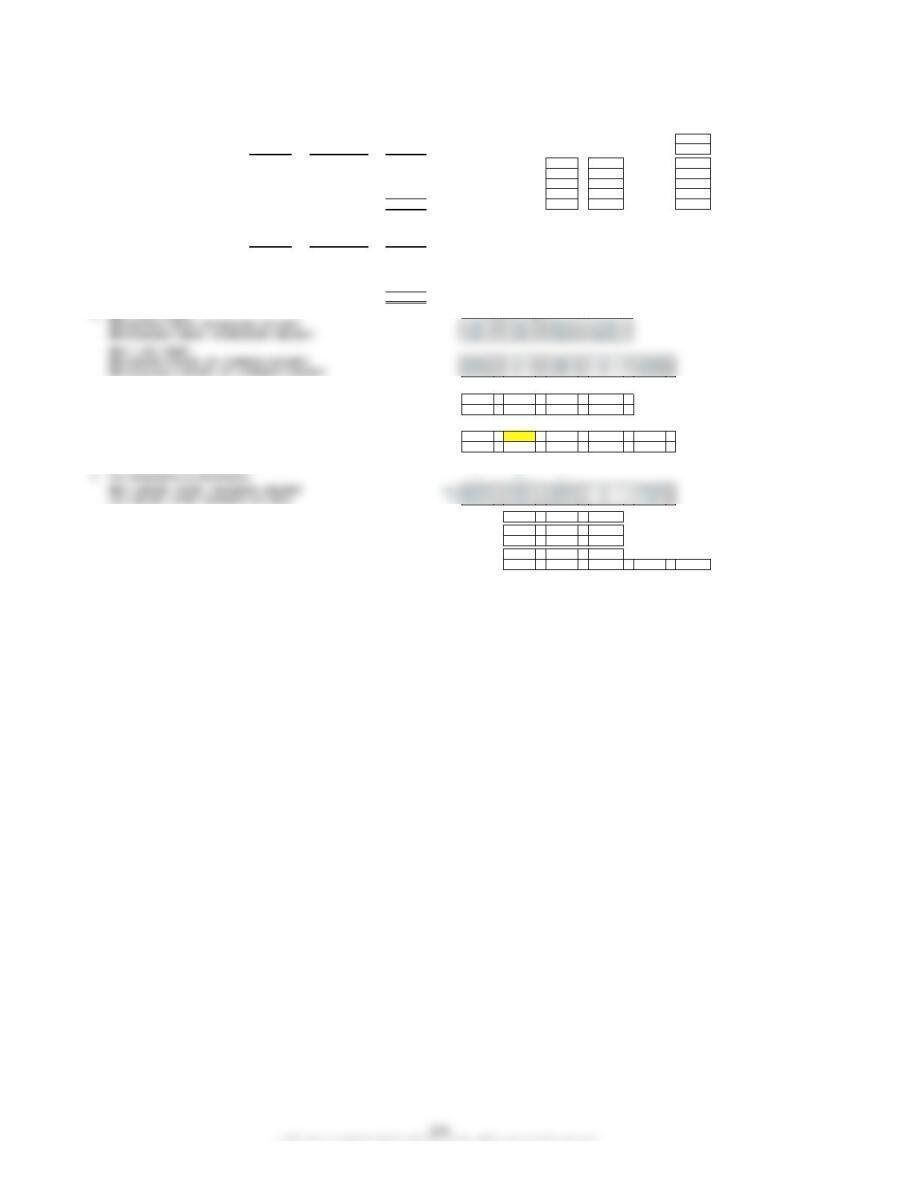

1. Fixed Overhead Rate = $832,500/450,000* = $1.85 per DLH 832,500 / 450,000 = 1.85 No. of power drills 600,000

SH = 594,000 units × 0.75 direct labor hour = 445,500 hours 594,000 × 0.75 = 445,500 Std labor hrs per drill 0.75

Applied FOH = $1.85 × 445,500 = $824,175 1.85 × 445,500 = 824,175 total budgeted OH 1,777,500

*Budgeted Hours = 600,000 units × 0.75 direct labor hours = 450,000 hours *600,000 × 0.75 = 450,000 total budgeted FOH 832,500

2. Fixed overhead analysis: Actual FOH: Actual production (units) 594,000

Budgeted FOH: 3,100 U Spending Actual DLH 446,000

1.85 × 600,000 × 0.8 Actual variable OH 928,000

835,600

Actual FOH

$835,600

$3,100 U

Spending

Budgeted FOH

$1.85 × 450,000

$832,500

$8,325 U

Applied FOH

$1.85 × 445,500

$824,175

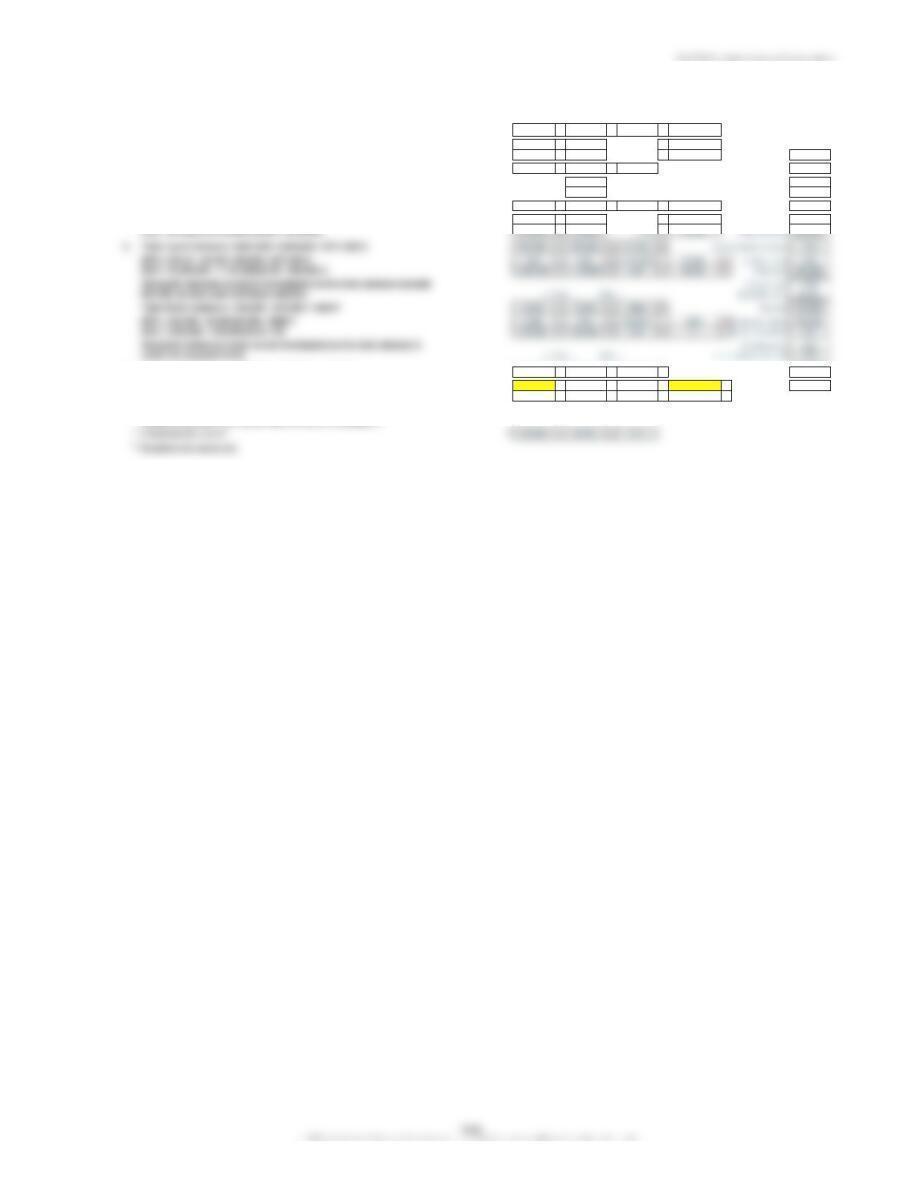

3. Variable OH Rate = ($1,777,500 – $832,500)/450,000 hours 1,777,500 – 832,500 / 450,000 = 2.10

= $2.10 per DLH

4. Variable overhead analysis:

Actual VOH:

2. AH × SFOR: (8,600) F Spending

2.10 × 446,000 = 936,600

3. SH × SFOR: 1,050 U Efficiency

2.10 × 445,500 = 935,550

928,000

Actual VOH

112,400

Budgeted VOH:

Actual VOH

831,000

$112,400

$1,170 U

Spending

Budgeted VOH

$0.70 × 158,900

$111,230

$210 F

Efficiency

Applied VOH

$0.70 × 159,200*

$111,440

$928,000

$8,600 F

Spending

Budgeted VOH

$2.10 × 446,000

$936,600

$1,050 U

Efficiency

Applied VOH

$2.10 × 445,500

$935,550

CHAPTER 10 Standard Costing and Variance Analysis

E 10-60

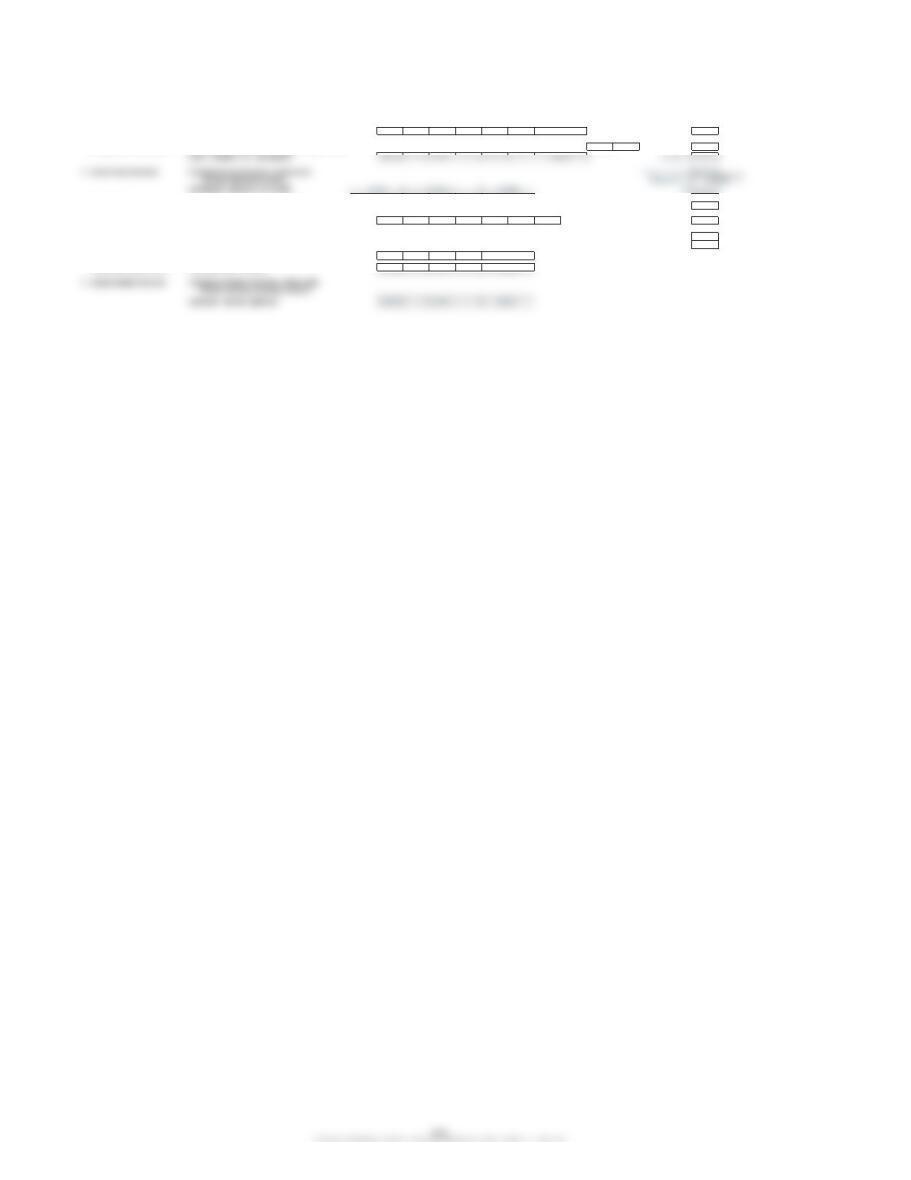

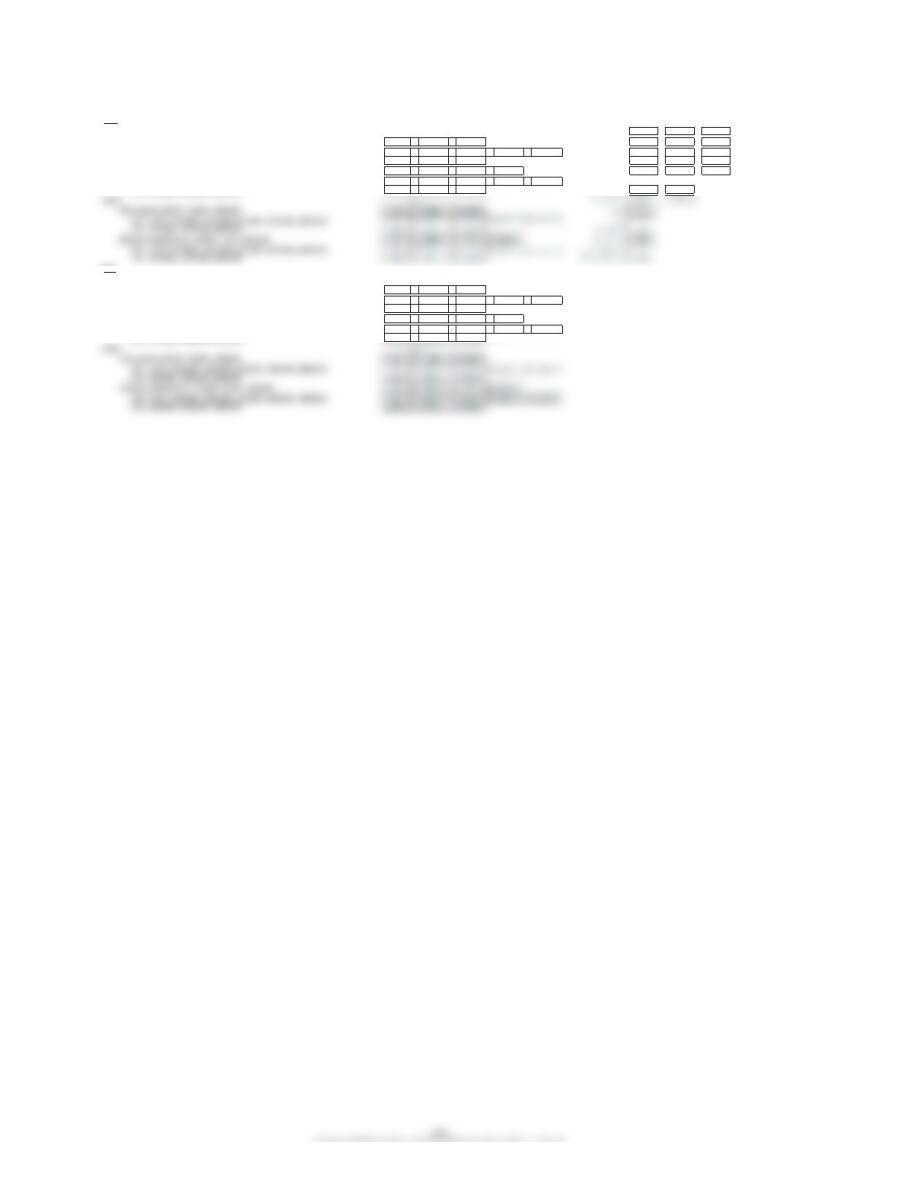

1. Total Applied Fixed Overhead

= (Standard Hours per Unit × Actual Units) × SFOR ↓ links ↓ change here, please ↓

= (0.9 × 143,000) × $11 = $1,415,700 0.9 × 143,000 × 11 = Actual units 143,000

2. Budgeted Fixed Overhead = (Standard Hours per Unit × Budgeted Units) × SFOR 29,700 U Std. units 140,000

= (0.9 × 140,000) × $11 = $1,386,000 140,000 × 0.9 × 11 = Std. labor hrs. 0.9

3. Actual Fixed Overhead = Budgeted Fixed Overhead + Unfavorable Budgeted variable OH 801,360

Overhead Spending Variance

= $1,386,000 + $24,000 = $1,410,000 + 24,000 = rate 11.00

1,386,000

1,386,000

1,386,000

1,410,000

4. Total Applied = (Standard Hours per Unit × Actual Units) × SVOR SVOR 6.36

Variable Overhead

= (0.9 × 143,000) × $6.36 = $818,532 0.9 × 143,000 × 6.36 = 818,532 Unfav. OH SP variance? 24,000

5. Budgeted Variable Overhead = Applied Variable Overhead + Unfavorable Unfav. variable OH EF variance? 1,272

Based on Actual Hours

Variable Overhead Efficiency Variance

Unfavor. variable OH SP variance? 9,196

= $818,532 + $1,272 = $819,804 818,532 + 1,272 =

= $819,804/$6.36 = 128,900 819,804 /6.36 =

6. Actual Variable Overhead = Budgeted Variable Overhead + Unfavorable

Variable Overhead Spending Variance

= $819,804 + $9,196 = $829,000 819,804 + 9,196 =

829,000

128,900

1,415,700

819,804

CHAPTER 10 Standard Costing and Variance Analysis

Chapter 10 Standard Costing and Variance Analysis

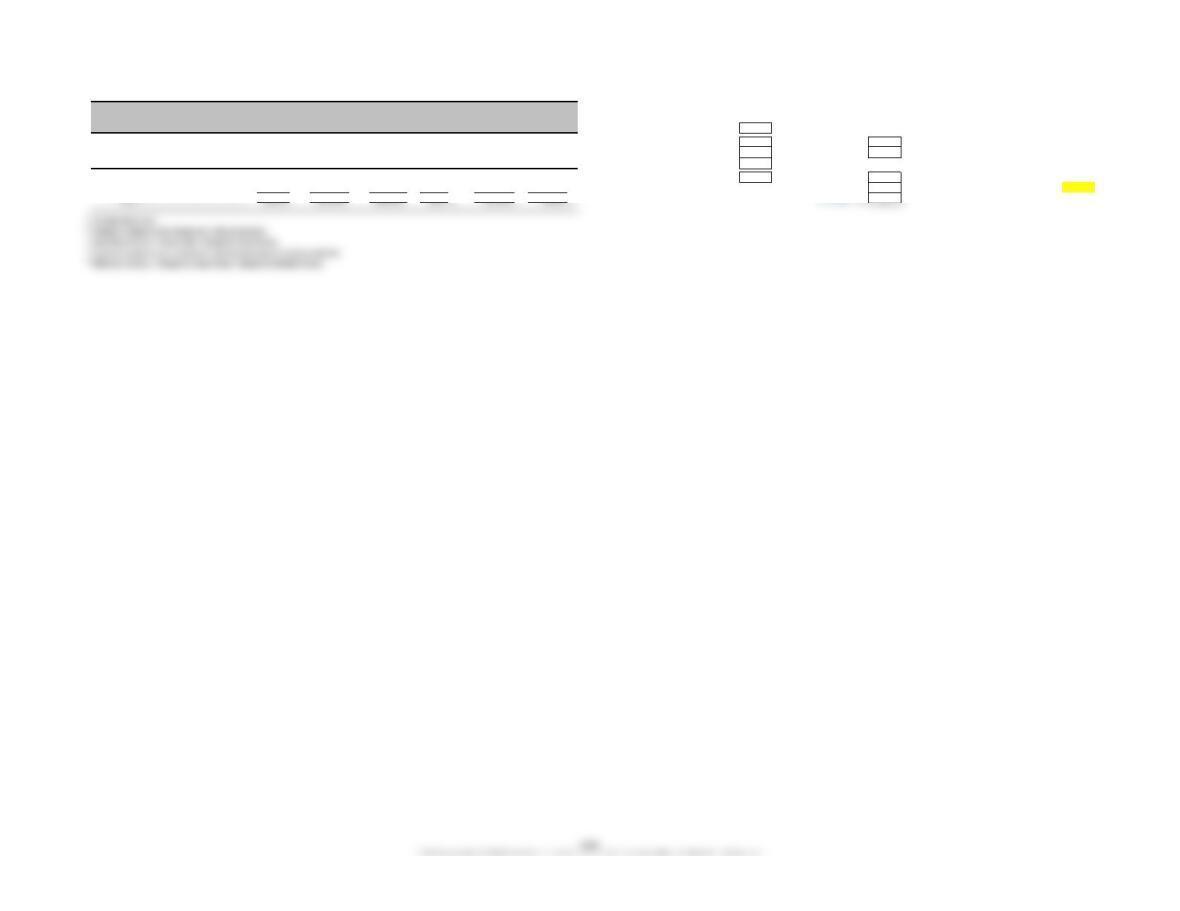

E 10-61

change here, please ↓

↓

Actual Variable

Indirect labor 36,000 Indirect labor

Supplies 3,800 hrs. reqd. 0.15

Cost Actual Actual Standard Actual hours worked 1,490 Wage rate 24.0

FormulaaCost HoursbHoursdUnits produced 10,000 Supplies

Indirect labor………………………………………………………………………………………………………………………………..

$24.00 $36,000 $35,760 $240 U$36,000 $(240) F Hours allowed 1,500 hrs. reqd. 0.15

Supplies………………………………………………………………………………………………………………………………..

2.40 3,800 3,576 224 U3,600 (24) F production Wage rate 2.40

Anker Company

Performance Report

Cost

Spending

Variancec

Budget for

Budget for

Efficiency

Variancee

For the Year Ended December 31

Chapter 10 Standard Costing and Variance Analysis

CHAPTER 10 Standard Costing and Variance Analysis

P 10-62

1. a. The managers of each cost center should be involved in setting standards.

They understand the actual conditions and are the primary source for

information on quantity used and wages paid. The newly designated

materials purchasing manager is the information source for material

prices. Since this is a new position, that individual may not have much

information to share, and Annette should go directly to those that did the

purchasing in the past. The accounting department, in conjunction with

Production, should be able to develop standards and should provide

information about past prices and usage.

waste, breakdowns, etc. Market prices for materials as well as labor

(unions) should be a consideration for setting standards.

2. Once the standards are set, actual results can be compared with the standards

and variances can be calculated. Of course, the variances themselves are only

indicators of potential problems. The underlying causes of the variances must

be determined to decide whether or not corrective action is needed. For this

reason, responsibility for the variances will be assigned to those with the most

information about them. The variances that will most likely be calculated are:

Materials Purchase Price Variance—responsibility for this variance lies with

the supervisor who was designated the materials purchasing manager. This

individual can explain why materials prices were or were not equal to the

standard amounts.

Materials Usage Variance—responsibility for this variance lies with the

manager in charge of the production department. This individual knows how

much was produced and whether or not the amount of materials used equaled

the standard.

Labor Rate Variance—responsibility for this variance lies with the manager in

charge of the production department. Again, this individual knows whether

or not the wage rate used equaled the standard.

Labor Usage Variance—responsibility for this variance lies with the manager

in charge of the production department. This individual knows how much was

produced and whether or not the amount of labor used equaled the standard.

PROBLEMS

CHAPTER 10: Standard Costing and Variance Analysis

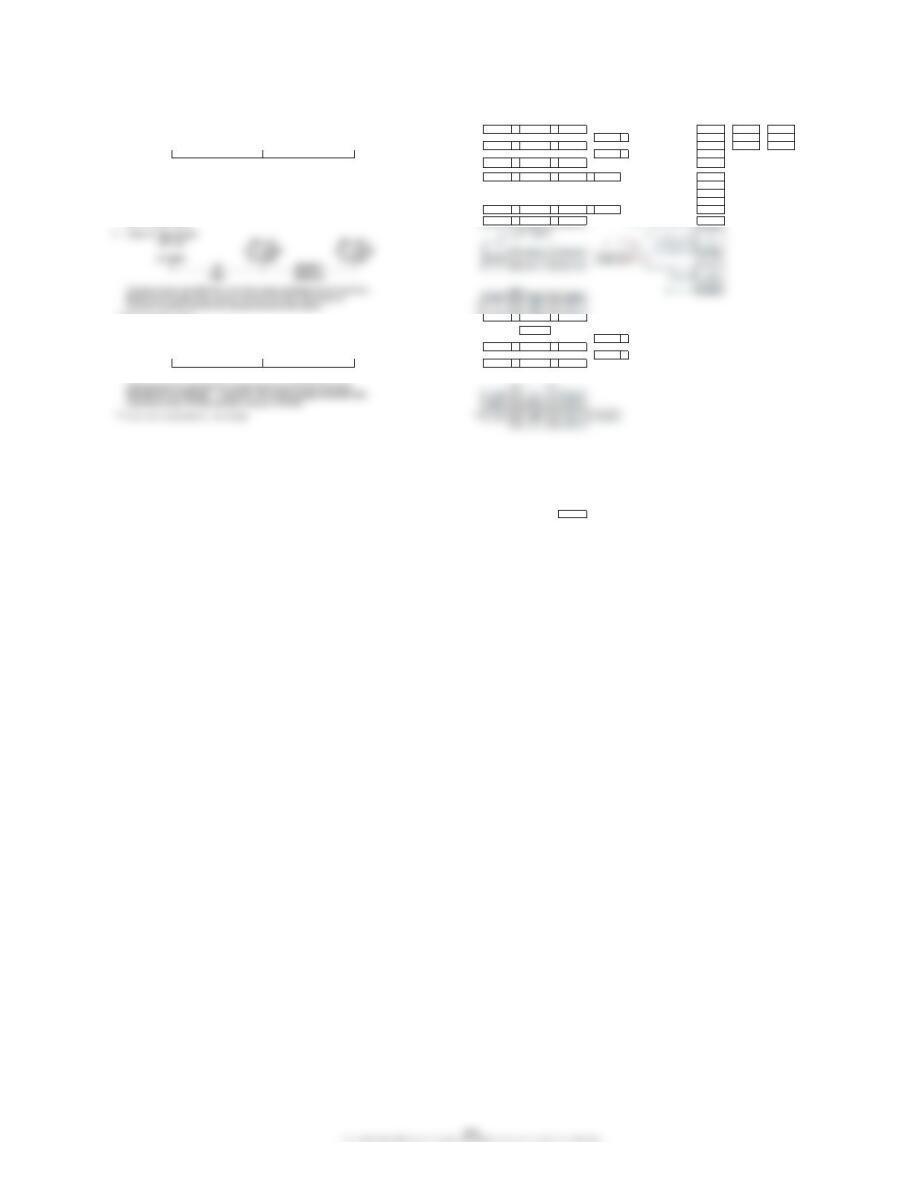

P 10-63 ↓ links ↓

change here, please →

1. Materials: AP × AQ: Std. Qty. Std. price Std. cost

3.55

×

69,000

=

244,950 Direct materials 12 3.50 42.00

SP × AQ: 3,450 U Price Direct labor 1.7 11 18.7

3.50

×

69,000

=

241,500 Variable overhead 1.7 3 5.1

SP × SQ: 10,500 F Usage Units produced 6,000

3.50

×

72,000

=

252,000 105,000

The new process saves 0.25 × 6,000 × $3.50 = $5,250. The decision to use the 0.25

×

6,000

×

3.50

=

5,250 Actual labor costs 118,800

higher-quality material is a trade-off between the higher material cost (price

variance) and the usage variance caused by the higher-quality material. Thus,

the net savings attributable to the higher-quality material is $5,250 – $3,450 = Actual labor hours 10,800

$1,800. Keep the higher-quality material! 10,500

–

5,250

–

3,450

=

1,800 Materials purchased and used 69,000

×

=

×

=

×

=

–

=

×

=

$118,800

$0

$112,200

$6,600 U

Efficiency

Rate

$118,800

AR × AH

$11 × 10,800

SR × AH

$11 × 10,200

** SH = 1.70 × 6,000 = 10,200 ** 1.70

×

6,000

=

10,200

3. Labor for new process, 1 week later: AR × AH: 99,000

SR × AH: 0Rate

11

×

9,000

=

99,000

SR × SH: (13,200) F Efficiency

11

×

10,200

=

112,200

×

=

+

=

×

×

+

–

=

SP × SQ*

$3.50 × 72,000

$3,450 U

$10,500 F

AP × AQ

$3.55 × 69,000

SP × AQ

$3.50 × 69,000

$252,000

$244,950

$241,500

Efficiency

AR × AH

SR × AH

SR × SH

Rate

$11 × 9,000

$0

$13,200 F

$11 × 10,200

$99,000

$99,000

$112,200

Price

Usage

CHAPTER 10 Standard Costing and Variance Analysis

change here, please →

P 10-64 Granite, per square foot 50.00

1. Granite: Glue 1.50

MPV

= Actual Cost – (AQ × SP) ↓ links ↓ links ↓ Cutting labor 1.50

MUV

Glue: Act. hrs cutting labor 180

MPV

= Actual Cost – (AQ × SP) Glue purch., used 2,560

= $2,560 – (16,000 × $0.15) = $160 U 2,560 – 16,000 × 0.15 = 160 U Sq. ft. per granite 1,640

MUV

= (AQ – SQ**)SP Act. hrs install. labor 390

= (16,000 – 16,000)$0.15 = $0 16,000 – 16,000 × 0.15 = 0 Oz. glue purchased 16,000

** SQ = 50 × 32 × 10 = 16,000 ** 50 × 32 × 10 = 16,000 Std. price of glue 0.15

LRV

LEV

LRV

LEV

3. It would probably not be worthwhile for Charlene to establish standards

for every different type of installation. Tom and Tony have a small enough

operation that they can mentally decide whether or not another type of

installation (e.g., one with multiple sink cuts) will be more expensive than

the typical one.

P 10-65

change here, please →

1. Standard Standard Units Serviced Cum. Av. Time pu

Usage Cost No. of vehicles requiring service 150 40 2.5

Direct materials…………………………………………………………………………………………….

$ 4 25.000 $100.00 Std. usage 25 80 2

Direct labor………………………………………………………………………………………….

15 0.768 11.52 Std.labor rate 15 160 1.6

Variable overhead………………………………………………………………………………………….

8 0.768 6.14 Std. cost 4320 1.28

Fixed overhead………………………………………………………………………………………….

12 0.768 9.22 Std. var. O/H rate 8

3.

The cumulative average time per unit is an average . For example, the first 40 / 16.0 = 2.5 0.8

40 units take an average of 2.50 hours per unit. The second 40 take an

average of 1.5 hours per unit [(80 × 2) – (40 × 2.5)]/40 = 1.5, and, therefore, 80 × 2 – 40 × 2.5

the average for the first 80 is 2.0 per unit. Thus, as more units are produced /40 = 1.5

the cumulative average time per unit will decrease. The standard should

be 0.768 hour per unit as this is the average time taken per unit once

average time per 1st 80 units 2.0

Standard

Price

CHAPTER 10 Standard Costing and Variance Analysis

P 10-66

1. Normal delivery:

change here, please →

Standard Standard Total labor cost 580,350

Price Cost Normal Cesarean Act price per lb 9.50

Direct materials…………………………………………………………………………………………….

###### # 9.0 lbs. $ 90.00 Direct materials (lbs.) 921 Std price per lb 10.00

Direct labor………………………………………………………………………………………….

16.00 2.5 hrs. 40.00 Nursing labor (hrs.) 2.5 5 Std labor rate 16.00

Variable overhead………………………………………………………………………………………….

30.00 2.5 hrs. 75.00 Patient days 4,000 8,000 Var. O/H rate 30

Fixed overhead………………………………………………………………………………………….

40.00 2.5 hrs. 100.00 DM purchased 35,000 165,000 Fixed O/H rate 40

Unit cost………………………………………………………………………………………….

$305.00 Nursing labor (hrs.) 10,200 40,500 11.45

Cesarean delivery:

Standard Standard

Price Cost

Direct materials…………………………………………………………………………………………….

###### # 21.0 lbs. $210.00

Direct labor………………………………………………………………………………………….

16.00 5 hrs. 80.00

Variable overhead………………………………………………………………………………………….

30.00 5 hrs. 150.00

Fixed overhead………………………………………………………………………………………….

40.00 5 hrs. 200.00

Unit cost………………………………………………………………………………………….

$640.00

–

×

=

–

×

=

–

×

×

=

–

×

×

=

3. LRV = (AR – SR)AH ↓ links ↓ links ↓

LRV (Normal) = ($11.45* – $16.00)10,200 = $46,410 F

11.45

–

16.00

×

10,200

=

(46,410) F

LRV (Cesarean) = ($11.45* – $16.00)40,500 = $184,275 F 11.45

–

16.00

×

40,500

=

(184,275) F

LEV = (AH – SH)SR

LEV (Normal) = [10,200 – (2.5 × 4,000)]$16 = $3,200 U 10,200

–

2.5

×

4,000

×

16

=

3,200 U

LEV (Cesarean) = [40,500 – (5 × 8,000)]$16 = $8,000 U 40,500

–

5

×

8,000

×

16

=

8,000 U

* ($580,350/$50,700) which is rounded to the nearest cent.

–

–

×

=

–

–

×

=

5. Answers will vary. MUV: a 35,000

+

165,000

=

200,000

b4,000

×

9

=

36,000

c21

×

8,000

=

168,000

LEV: a 40,500

+

10,200

=

50,700

b4,000

×

3

+

8,000

×

5

=

50,000

Usage

Standard

Usage

Standard

P 10-67 ↓ links ↓ links ↓

change here, please →

1. Liquid Standard = 4.5 × 250,000 × $0.40 = $450,000 4.5 × 250,000 × 0.40 = 450,000 #

Upper control limit (UCL): $495,000 or $470,000; lesser = $470,000 495,000

or

470,000 lesser = 470,000

#Direct materials:

Lower control limit (LCL): $405,000 or $430,000; lesser = $430,000 405,000

or

430,000 greater = 430,000

4Liquids 1.80

Bottle Standard = 250,000 × $0.05 = $12,500 250,000 × 0.05 = 12,500 1.8 1Bottles 0.05

UCL: $13,750 UCL: 13,750 #REF! # Direct labor 3

LCL: $11,250 LCL: 11,250 1125000 Std wage rate per hr. 15.00

Direct Labor Standard = 0.2 × 250,000 × $15.00 = $750,000 0.20 × 250,000 × 15.00 = 750,000 #

ne bottles purchased

4

UCL: $825,000 or $770,000; lesser = $770,000 825,000

or

770,000 lesser = 770,000

0

nvestigation lesser of

20,000

LCL: $675,000 or $730,000; lesser = $730,000 675,000

or

2. Total Liquid Variance = $567,000 – $450,000 = $117,000 U 567,000 – 450,000 = 117,000 U Ounces of liquid purchased 1.35

The liquid variances would be investigated as the total variance exceeds 9168 0Price per bottle 0.048

The bottle variances would not be investigated as the total variance is Std price per oz. 0.40

within the accepted limits. ↓ links ↓ links ↓ Std. hrs required per bottle 0.20

3. Total Labor Variance = $733,000 – $750,000 = $17,000 F 733,000 – 750,000 = (17,000) F ?1,125,000

LRV = ($15.19* – $15.00)48,250 = $9,168 U

15.19 – 15.00 × 48,250 = 9,168 U 10%

LEV = (48,250 – 50,000)$15.00 = $26,250 F

48,250 – 50,000 × 15.00 = (26,250) F

The total variance is within the limits. However, the labor efficiency

variance is greater than $20,000 and should be investigated.

CHAPTER 10 Standard Costing and Variance Analysis

P 10-68

change here, please →

1.

April (UCL = Upper control limit, and LCL = Lower control limit) April May June

Materials: ↓ links ↓ Production (units) 90,000 100,000 110,000

Price standard: $0.25 × 723,000 = $180,750 0.25

×

723,000

=

180,750 DM Cost 189,000 218,000 230,000

UCL: (0.08 × $180,750) + $180,750 = $14,460 + $180,750 = $195,210 8%

×

180,750

=

14,460

+

180,750

=

195,210 DM Usage (lbs.) 723,000 870,000 885,000

LCL: ($14,460) + $180,750 = $166,290

14,460

+

180,750

=

166,290 DL Cost 270,000 323,000 360,000

Quantity standard: 8 × 90,000 × $0.25 = $180,000 8

×

90,000

×

0.25

=

180,000 DL Usage (hrs.) 36,000 44,000 46,000

UCL: (0.08 × $180,000) + $180,000 = $14,400 + $180,000 = $194,400 8%

×

180,000

=

14,400

+

180,000

=

194,400

LCL: ($14,400) + $180,000 = $165,600

+

=

×

=

×

=

+

=

LCL: ($21,600) + $270,000 = $248,400

+

=

×

×

=

×

=

+

=

LCL: ($21,600) + $270,000 = $248,400

+

May

Materials: ↓ links ↓

Price standard: $0.25 × 870,000 = $217,500 0.25

×

870,000

=

217,500

UCL: (0.08 × $217,500) + $217,500 = $17,400 + $217,500 = $234,900 8%

×

217,500

=

17,400

+

217,500

=

234,900

LCL: ($17,400) + $217,500 = $200,100

17,400

+

217,500

=

200,100

Quantity standard: 8 × 100,000 × $0.25 = $200,000 8

×

100,000

×

0.25

=

200,000

UCL: (0.08 × $200,000) + $200,000 = $16,000 + $200,000 = $216,000 8%

×

200,000

=

16,000

+

200,000

=

216,000

LCL: ($16,000) + $200,000 = $184,000

+

=

×

=

×

=

+

=

LCL: ($26,400) + $330,000 = $303,600

+

=

×

×

=

×

=

+

=

LCL: ($24,000) + $300,000 = $276,000

+

=

CHAPTER 10: Standard Costing and Variance Analysis

P 10-68 (Continued)

June April May June

Materials: ↓ links ↓ Production (units) 90,000 100,000 110,000

Price standard: $0.25 × 885,000 = $221,250 0.25 × 885,000 = 221,250 DM Cost 189,000 218,000 230,000

UCL: (0.08 × $221,250) + $221,250 = $17,700 + $221,250 = $238,950

8% × 221,250 = 17,700 + 221,250 = 238,950 DM Usage (lbs.) 723,000 870,000 885,000

LCL: ($17,700) + $221,250 = $203,550 17,700 + 221,250 = 203,550 DL Cost 270,000 323,000 360,000

Quantity standard: 8 × 110,000 × $0.25 = $220,000 8 × 110,000 × 0.25 = 220,000 DL Usage (hrs.) 36,000 44,000 46,000

UCL: (0.08 × $220,000) + $220,000 = $17,600 + $220,000 = $237,600

8% × 220,000 = 17,600 + 220,000 = 237,600

Cost of investigation

2,000 3,000

UCL: (0.08 × $345,000) + $345,000 = $27,600 + $345,000 = $372,600

UCL: (0.08 × $330,000) + $330,000 = $26,400 + $330,000 = $356,400

2. April

MPV = ($0.2614* – $0.25)723,000 = $8,242 U ± $14,460 4.6 →0.2614 – 0.25 × 723,000 = 8,242 U

MUV = (723,000 – 720,000)$0.25 = $750 U ± 14,400 0.4 723,000 – 720,000 × 0.25 = 750 U

LRV = ($7.5000 – $7.50)36,000 = $0 ± 21,600 0.0 7.50 – 7.50 × 36,000 = 0

LEV = (36,000 – 36,000)$7.50 = $0 ± 21,600 0.0 36,000 – 36,000 × 7.50 = 0

May

aClick a second time in the formula bar to show active cells.

MPV = ($0.2506* – $0.25)870,000 = $522 U ± 17,400 0.2 →0.2506 – 0.25 × 870,000 = 522 U

MUV = (870,000 – 800,000)$0.25 = $17,500 U ± 16,000 8.8 870,000 – 800,000 × 0.25 = 17,500 F

LRV = ($7.3409* – $7.50)44,000 = $7,000 F ± 26,400 (2.1) →7.3409 – 7.50 × 44,000 = (7,000) F

LEV = (44,000 – 40,000)$7.50 = $30,000 U ± 24,000 10.0 44,000 – 40,000 × 7.50 = 30,000 F

Actual**

Limit

(links to previous page)

Click in a cell to view links or calculations.a

***

***

%

%

CHAPTER 10 Standard Costing and Variance Analysis

P 10-68 (Continued)

3. Control charts allow us to see when the variances are outside an

acceptable range. They may also show a pattern that might help in

pinpointing when the problem began.

Control charts: To simplify the presentation, the variances are expressed

as a percentage of the total quantity or price standard, and the y-axis is

used for variances. April (Month 1), May (Month 2), and June (Month 3)

are presented on the x-axis. These percentages were calculated in

Requirement 2.

8.0

MPV:

8.00

MUV: