Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 10

Chapter 10

Plant Assets, Natural Resources,

and Intangibles

QUESTIONS

1. A plant asset is tangible; it is used in the production or sale of other assets or services;

and it has a useful life longer than one accounting period.

3. Land is an asset with an unlimited life and, therefore, is not subject to depreciation.

Land improvements have limited lives and are subject to depreciation.

4. Often the lump-sum or basket purchase includes assets with different lives that must be

5. The Accumulated Depreciation—Machinery account is a contra asset account with a

credit balance that cannot be used to buy anything. The balance of the Accumulated

6. The Modified Accelerated Cost Recovery System is not generally acceptable for financial

8. Ordinary repairs are made to keep a plant asset in normal, good operating condition, and

9. A company might sell or exchange an asset when it reaches the end of its useful life, or

10. The process of allocating the cost of natural resources to expense over the periods

11. No, depletion expense should be calculated on the units that are extracted (similar to the

units-of–production basis) and sold.

12. An intangible asset: (1) has no physical existence; (2) derives value from the unique

13. Intangible assets are generally recorded at their cost and amortized over their predicted

useful life. (However, some costs are not included, such as the research and

14. A company has goodwill when its value exceeds the value of its individual assets and

15. No; this type of goodwill would not be amortized. Instead, the FASB (SFAS 142) requires

that goodwill be annually tested for impairment. If the book value of goodwill does not

16. Total asset turnover is calculated by dividing net sales by average total assets.

17. The word “net” means that Apple is reporting its property and equipment after deducting

accumulated depreciation to date.

18. Google lists “Property and equipment, net” on the balance sheet. The net book value of

these assets is $29,016 million.

20. Samsung reports the following long-term assets that are discussed in this chapter:

Property, plant and equipment; Intangible assets.

21. (a) The main difference between plant assets and current assets is that current assets

are consumed or converted into cash within a short period of time, while plant assets

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 10

617

QUICK STUDIES

Quick Study 10-1 (10 minutes)

Quick Study 10-2 (10 minutes)

Expensed or Capitalized Asset Category (if any) .

1. Expensed —

2. Capitalized Equipment

Quick Study 10-3 (10 minutes)

Quick Study 10-4 (10 minutes)

618

Quick Study 10-5 (10 minutes)

Quick Study 10-6 (10 minutes)

Note: Double-declining-balance rate = (100% / 8 years) x 2 = 25%

First year:

Quick Study 10-7 (10 minutes)

619

Quick Study 10-8 (10 minutes)

1. (a) CE Capital expenditure

2.

(a) Equipment……………………………………………………….

40,000

Quick Study 10-9 (15 minutes)

1.

2.

3.

Quick Study 10-10 (10 minutes)

1.

Ore Mine ………………………………………………………………..

1,800,000

1,800,000

Quick Study 10-11 (10 minutes)

a. Oil well NR

Quick Study 10-12 (10 minutes)

1.

2.

Dec. 31

Amortization Expense–Leasehold Improvements …………

13,125

621

Quick Study 10-13 (10 minutes)

Quick Study 10-14A (10 minutes)

Quick Study 10-15 (10 minutes)

a. Accounting for plant assets involving cost determination,

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 10

622

EXERCISES

Exercise 10-1 (15 minutes)

Invoice price of machine …………………………………………………

$ 12,500

Exercise 10-2 (15 minutes)

Cost of land

Purchase price for land …………………………………………………..

$ 280,000

Purchase price for old building …………………………..

110,000

Total construction costs …………………………………………………

Land Improvements ……………………………………………….

Less discount (.02 x $12,500) ………………………………………….

Assembly ……………………………………………………………………….

Materials used in adjusting ……………………………………………..

Exercise 10-3 (20 minutes)

Allocation of total cost

Appraised

Value

Percent

of Total

Applying %

to Cost

Apportioned

Cost

Land …………………………

$157,040

40%

$395,380 x .40

$158,152

15

59,307

$395,380 x .45

$392,600

$395,380

395,380

Exercise 10-4 (10 minutes)

Exercise 10-5 (10 minutes)

Units–of-production

624

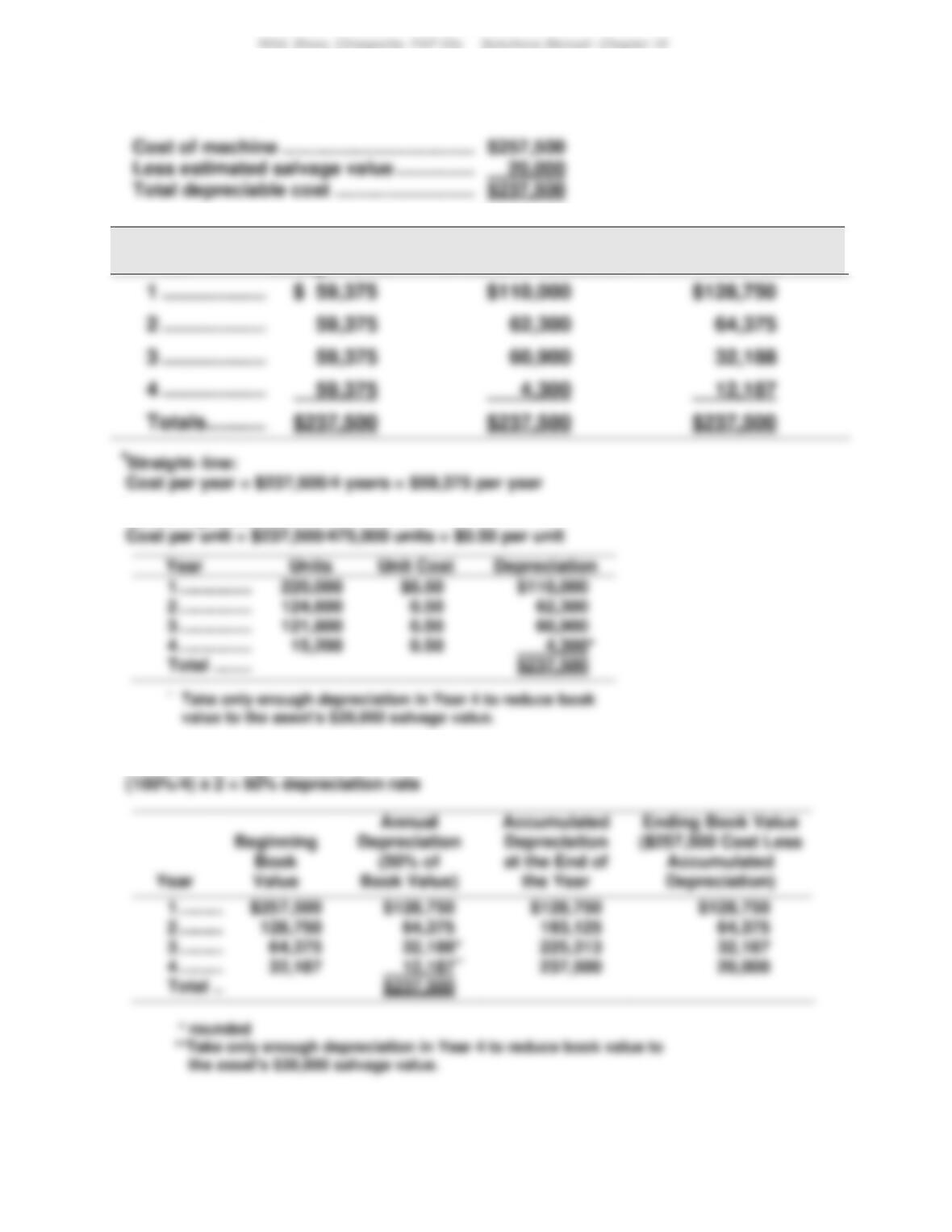

Exercise 10-6 (15 minutes)

Double-declining-balance

Exercise 10-7 (15 minutes)

Exercise 10-8 (20 minutes)

Double-declining-balance depreciation

625

Exercise 10-9 (30 minutes)

Straight-line depreciation

Income

before

Depreciation

Depreciation

Expense*

Net

Income

Exercise 10-10 (30 minutes)

Double-declining-balance depreciation

Income

before

Depreciation

Depreciation

Expense*

Net

Income

626

Exercise 10-11 (10 minutes)

Straight-line depreciation for 2016

Exercise 10-12 (15 minutes)

Double-declining-balance depreciation for 2016 and 2017:

Rate = (100% / 5 years) x 2 = 40%

Exercise 10-13 (15 minutes)

1.

Original cost of machine …………………………………………………….

$ 23,860

[($23,860 – $2,400) / 4 years] x 2 years …………………………..

$ 13,130

2.

$ 13,130

627

Exercise 10-14 (15 minutes)

1.

Equipment ……………………………………………………………

2.

Repairs Expense …………………………………………………..

6,250

3.

Equipment …………………………..……………………………….

Exercise 10-15 (25 minutes)

2. Entry to record the extraordinary repairs

3.

Cost of building

Before repairs……………………………………………………….

$572,000

Add cost of repairs …………………………………………………

$640,350

Less accumulated depreciation …………………………..

4.

Revised book value of building (part 3) ………………………

$211,350

New estimate of useful life (20 – 15 + 5) ………………………

Depreciation Expense …………………………………………….

628

Exercise 10-16 (20 minutes)

1. Disposed at no value

Jan. 3

Loss on Disposal of Milling Machine …………………….

68,000

2. Sold for $35,000 cash

Jan. 3

Cash …………………………..……………………………………….

35,000

Loss on Sale of Milling Machine …………………………..

33,000

3. Sold for $68,000 cash

Jan. 3

Cash …………………………..……………………………………….

68,000

4. Sold for $80,000 cash

Jan. 3

Cash …………………………..……………………………………….

80,000

629

Exercise 10-17 (25 minutes)

2021

July 1

1. Sold for $45,500 cash

July 1

Cash …………………………..……………………………………….

45,500

67,500

2. Destroyed by fire with $25,000 cash insurance settlement

July 1

Cash …………………………..……………………………………….

25,000

12,500

Exercise 10-18 (10 minutes)

630

Exercise 10-19 (10 minutes)

Jan. 1

Copyright ……………………………………………………….

418,000

Exercise 10-20 (10 minutes)

Exercise 10-21 (15 minutes)

Exercise 10-22 (15 minutes)

631

Exercise 10-23A (15 minutes)

Exercise 10-24A (25 minutes)

1. Sold for $18,250 cash

Jan. 2

Cash …………………………..……………………………………….

18,250

2. $25,000 trade-in allowance exceeds book value (yielding a gain)

Jan. 2

60,200

24,625

3. $15,000 trade-in allowance is less than book value (yielding a loss)

Jan. 2

60,200

632

Exercise 10-25 (20 minutes)

(Amounts for this exercise are in euros millions)

3.

Cash ……………………………………………………………………..

720

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 10

633

PROBLEM SET A

Problem 10-1A (50 minutes)

Part 1

Estimated

Market Value

Percent

of Total

Apportioned

Cost

Building ……………………..

$508,800

53%

$477,000

Part 2

Year 2017 straight-line depreciation on building

Part 3

Year 2017 double-declining-balance depreciation on land improvements

31

634

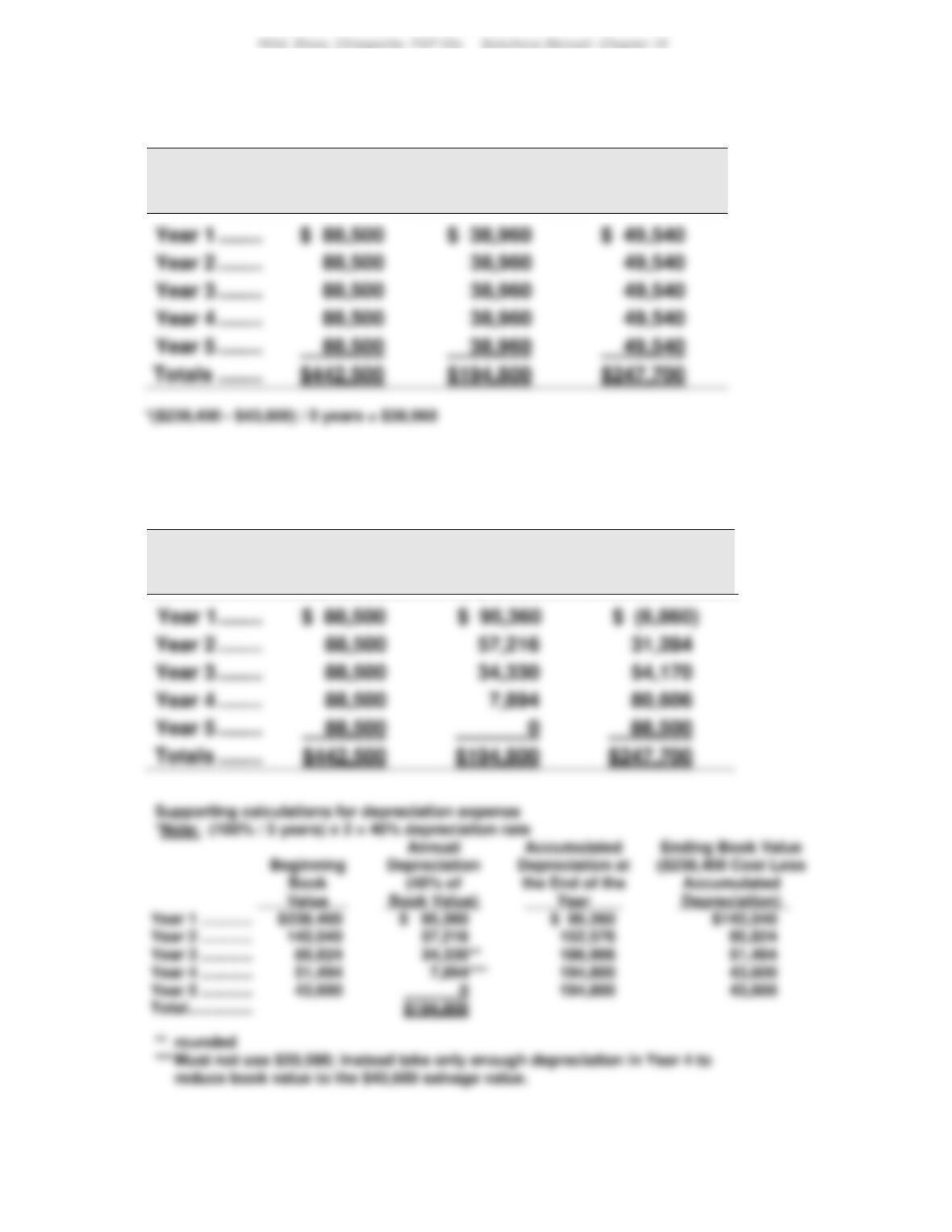

Problem 10-2A (25 minutes)

Year

Straight–Linea

Units–of-Productionb

Double-Declining-

Balancec

bUnits-of-production:

cDouble-declining-balance: