15 Minutes, Easy

PROBLEM 10.5B

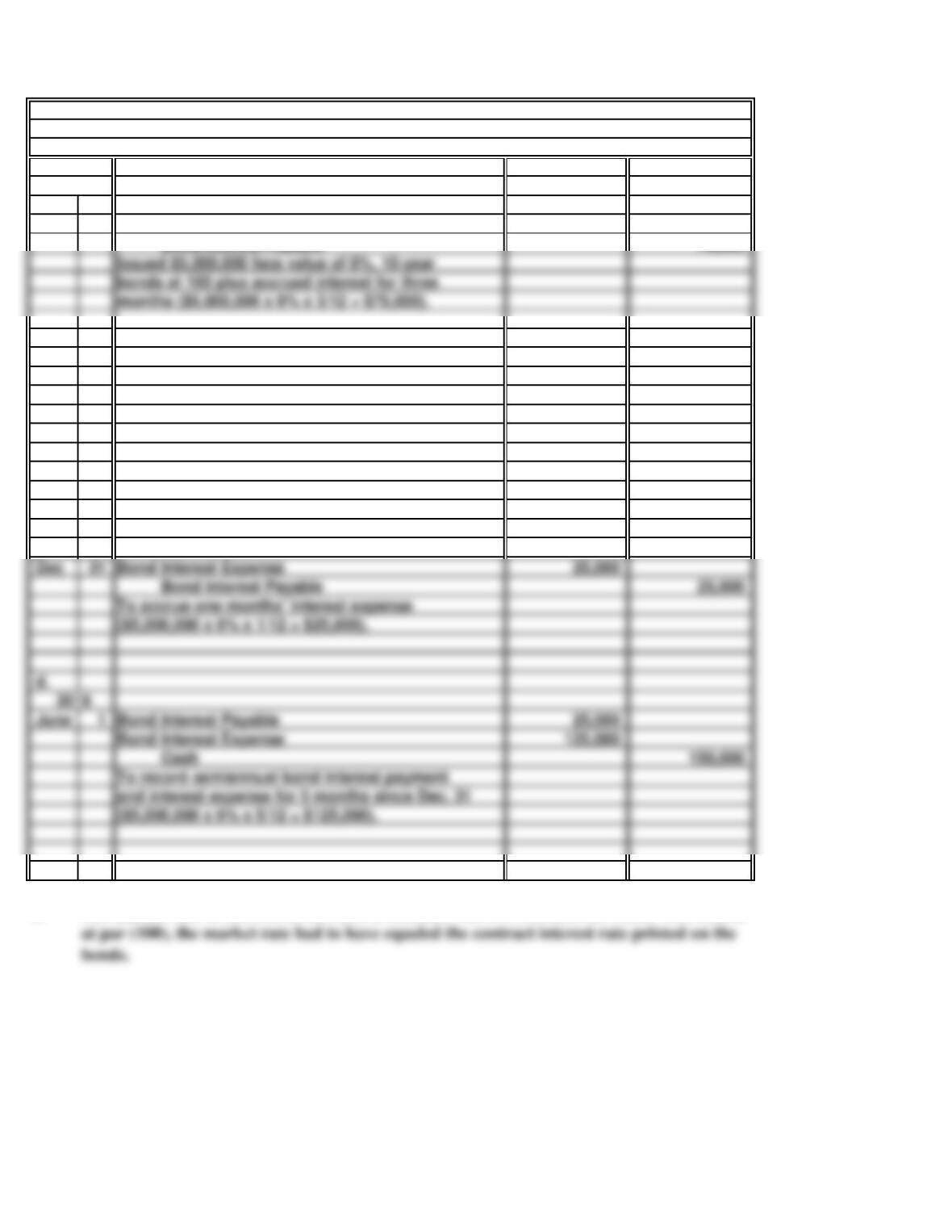

Sept 1 Cash 5,075,000

Bonds Payable 5,000,000

Bond Interest Payable 75,000

b.

Dec 1 75,000

75,000

Cash 150,000

c.

Dec 31 25,000

Bond Interest Payable 25,000

d.

June 1 25,000

Cash 150,000

Bond Interest Expense

Bond Interest Expense

($5,000,000 x 6% x 5/12 = $125,000).

and interest expense for 5 months since Dec. 31

($5,000,000 x 6% x 1/12 = $25,000).

Bond Interest Payable

To record semiannual bond interest payment

To accrue one months’ interest expense

e.

$150,000).

The market rate of interest on the date of issuance was 6%. Because the bonds were issued

Paid semiannual interest ($5,000,000 x 6% x 1/2 =

2018

Bond Interest Payable

Bond Interest Expense

STEVENS MANUFACTURING COMPANY

a.

General Journal

bonds at 100 plus accrued interest for three

months ($5,000,000 x 6% x 3/12 = $75,000).

Issued $5,000,000 face value of 6%, 10-year

35 Minutes, Strong

RODRIGUEZ PLUMBING COMPANY

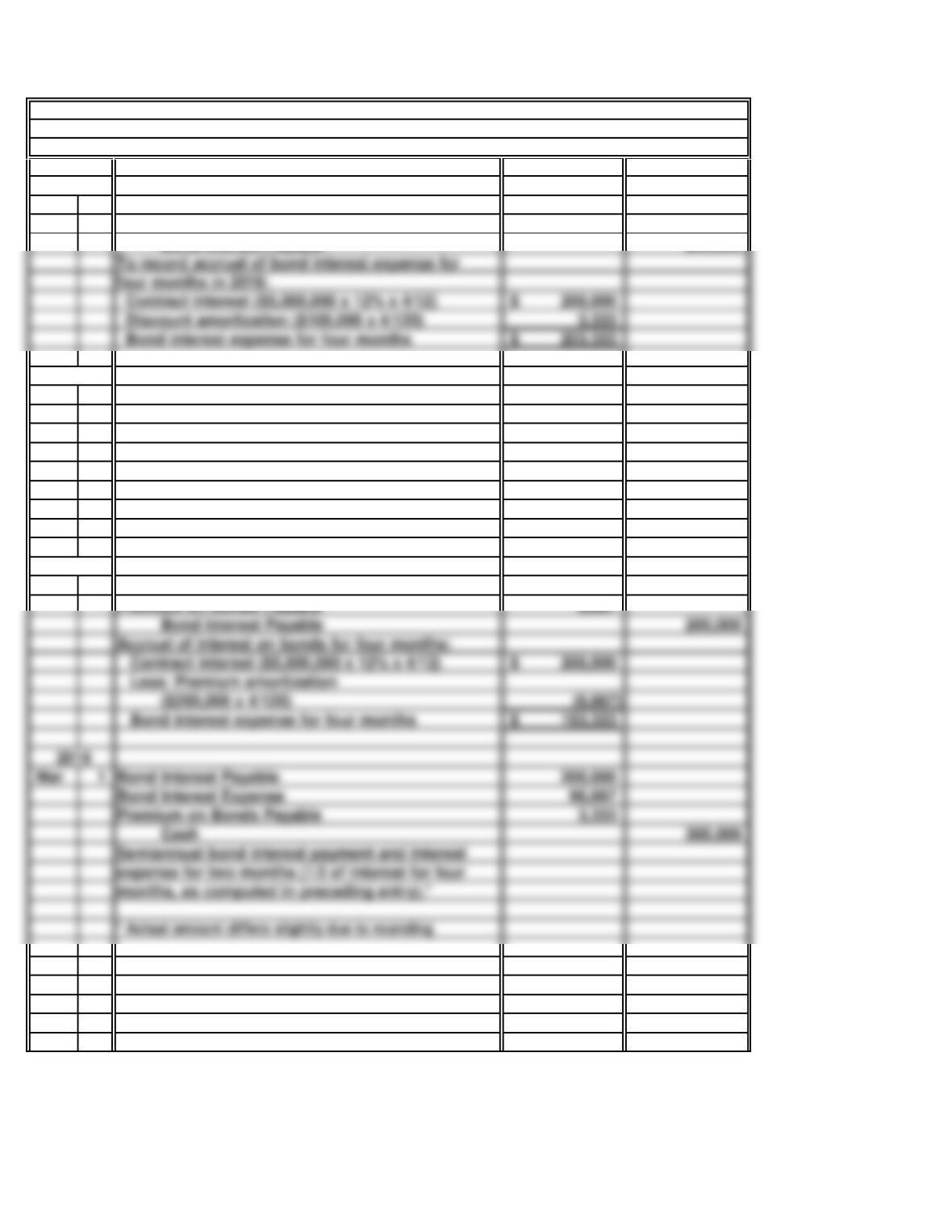

Dec 31 Bond Interest Expense 203,333

3,333

Bond Interest Payable 200,000

Mar 1 200,000

101,667

1,667

Cash 300,000

(2)

Dec 31 193,333

6,667

Bond Interest Payable 200,000

193,333$

Mar 1 200,000

Cash 300,000

Less: Premium amortization

($200,000 x 4/120)

Premium on Bonds Payable

Contract interest ($5,000,000 x 12% x 4/12)

Bond interest expense for four months

2019

Bond Interest Expense

expense for two months (1/2 of interest for four

months, as computed in preceding entry).*

Bond Interest Payable

Semiannual bond interest payment and interest

Premium on Bonds Payable

2018

2019

Discount on Bonds Payable

interest expense for two months (1/2 of interest for

four months, as computed in preceding entry). *

Bond Interest Expense

Bond Interest Payable

PROBLEM 10.6B

a.

General Journal

(1)

Bonds issued at 98:

Bonds Interest Expense

Bonds issued at 104:

2018

Discount on Bonds Payable

To record semiannual bond interest payment and

Bond interest expense for four months

Contract interest ($5,000,000 x 12% x 4/12)

To record accrual of bond interest expense for

four months in 2018:

Discount amortization ($100,000 x 4/120)

b.

Net bond liability at Dec. 31, 2019: Bonds Bonds

Issued Issued

at 98 at 104

*

Premium amortized at Dec. 31, 2019:

c.

PROBLEM 10.6B

RODRIGUEZ PLUMBING COMPANY (concluded)

The effective rate of interest would be higher under assumption 1. The less that investors

Discount amortized at Dec. 31, 2019:

* Less: Discount on bonds payable ($100,000 – $13,333) (86,667)

Net bond liability

45 Minutes, Strong

a.

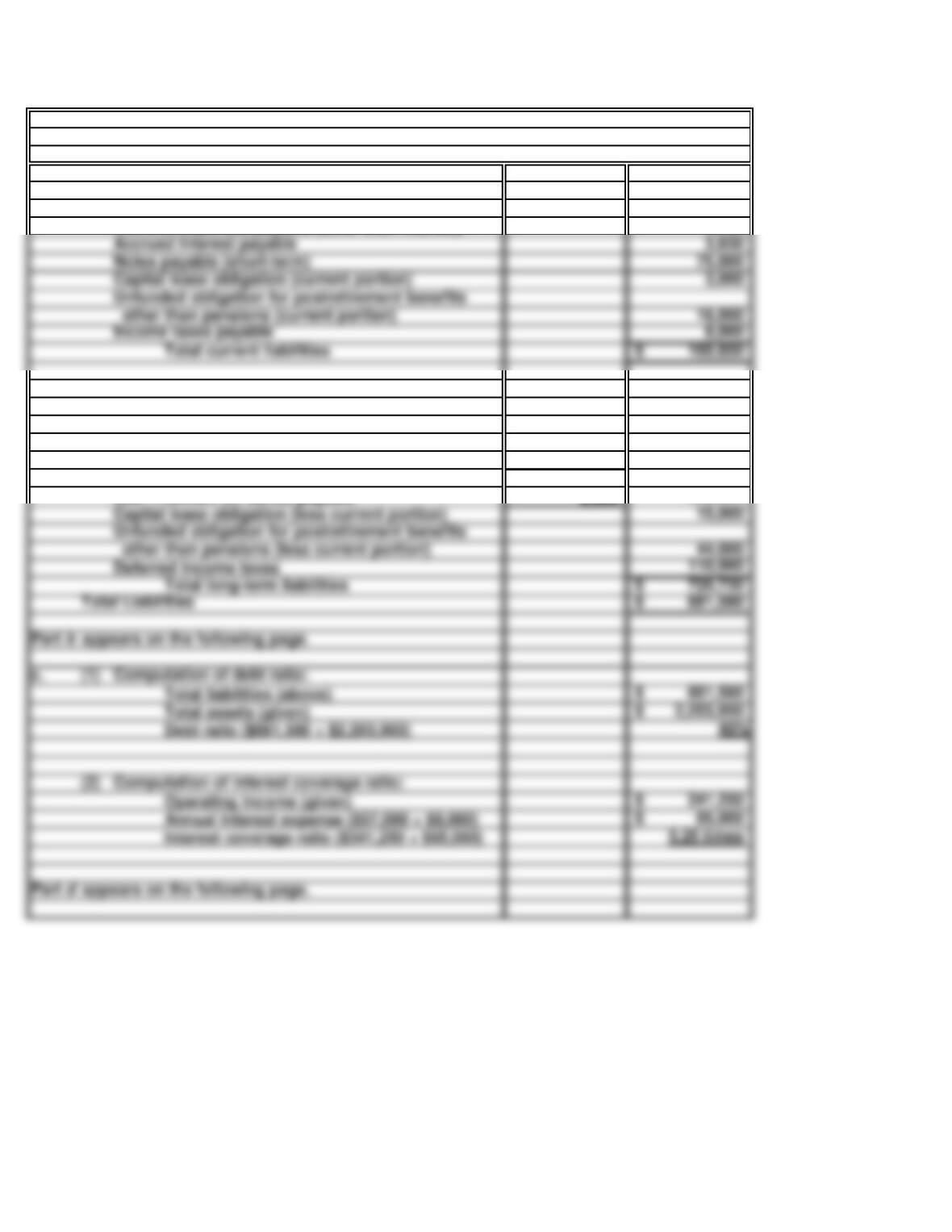

Liabilities:

(in thousands)

Accounts payable 48,000$

7,200

100,000$

150,000$

270 149,730

300,000$

Total liabilities (above) 881,580$

Total assets (given) 2,203,950$

(2) Computation of interest coverage ratio:

Part b appears on the following page.

Capital lease obligation (less current portion)

Deferred income taxes

PROBLEM 10.7B

NEVADA UTILITY COMPANY

December 31, 2018

Partial Balance Sheet

NEVADA UTILITY COMPANY

Add: Premium on bonds payable

Current liabilities:

Accrued expenses payable (other than interest)

Long-term liabilities:

10% Bonds payable, due April 1, 2019

8% Bonds payable, due October 1, 2019

Less: Discount on bonds payable

12% Bonds payable, due April 1, 2018

Accrued interest payable 3,650

b. (1)

(3)

(4)

(5)

The $16,000 portion of the unfunded liability for postretirement benefits that will be

(6)

d.

PROBLEM 10.7B

NEVADA UTILITY COMPANY

(concluded)

In summary, the fact that Nevada Utility is a profitable utility company with a reasonable

As the 10% bond issue is being refinanced on a long-term basis (that is, paid from the

The portion of the capital lease obligation that will be repaid within one year ($3,000) is

Income taxes payable relate to the current year’s income tax return and, therefore, are

Based solely upon its debt ratio and interest coverage ratio, Nevada Utility appears to be a

good credit risk. One must consider, however, that Nevada Utility is a utility company, not a

(2)

The 8% bonds will be repaid from a bond sinking fund rather than from current assets.

20 Minutes, Strong

a.

Liabilities:

Unearned revenues 268,000$

750,000$

Total Liabilities 1,540,500$

Notes payable*

Deferred income taxes**

b.

PROBLEM 10.8B

ALEXANDER COMPANY

Bonds payable

Current liabilities:

Long-term liabilities:

The following items listed by the company have been excluded from current and long-term

liabilities for the reasons indicated:

Notes payable (current portion) 27,000

Income taxes payable

30 Minutes, Medium

a.

b.

c.

d.

e.

f.

SOLUTIONS TO CRITICAL THINKING CASES

LIABILITIES IN PUBLISHED

CASE 10.1

FINANCIAL STATEMENTS

Wausau Paper’s liability for “current maturities” of long-term debt is common to most large

Club Med’s liability for future vacations is unearned revenue. This liability arises when

Wells Fargo’s liability for interest-bearing deposits represents the amounts on deposit in

The New York Times’ liability for unexpired subscriptions is a form of unearned revenue

Horse racing tracks issue mutual tickets as evidence of the bets that customers have made on

As American Greetings is a manufacturer, it probably sells primarily to wholesalers or

retailers rather than directly to consumers. Apparently, the company allows its customers to

g.

h.

GM’s liability for postretirement costs is an obligation to pay retirement benefits to

Case 10.1

LIABILITIES IN PUBLISHED

Apple’s accrued marketing and distribution liability represents accrued marketing and

FINANCIAL STATEMENTS (concluded)

20 Minutes, Strong

BOND PRICES

a.

c.

CASE 10.2

ABBOTT LABS

Differences in the length of time remaining until the bond issues mature is the major factor

influencing the current market prices. As bonds near their maturity dates, their market

The effective rate of interest is higher on issue A bonds. The less that investors pay for

25 Minutes, Medium

a.

1

2

3

4

b.

Management is responsible to disclose loss contingencies which are significant in nature and

that they might affect an investor’s or creditor’s analysis and subsequent decisions regarding

This lawsuit is based upon past events (treatment of displaced passengers) and involves

CASE 10.3

LOSS CONTINGENCIES

The risk of a future airplane crash does not stem from past events. Therefore, it is not a loss

contingency. A loss contingency would exist if an airplane had crashed, but the amount of the

The estimated loss from uncollectible accounts is a loss stemming from past events (credit

in the amount of the estimated loss.

The health, retirement, or even death of company executives are not loss contingencies and

20 Minutes, Medium

a.

b.

c.

If Delta Airlines had structured all of its lease agreements as capital leases (Type A) instead

of operating leases (Type B), its operating leases would be reported in the company’s

CASE 10.4

DELTA AIRLINES

ETHICS, FRAUD & CORPORATE GOVERNANCE

GAAP associated with the financial reporting treatment of lease agreements has been

criticized for its many loopholes. Nevertheless, if Delta remains in compliance with GAAP

In the case of Delta’s lease agreements, it is important that investors and creditors read and

understand the notes to the company’s financial statements. This is particularly true in

20 Minutes, Strong

a.

●

●

●

●

Junk bonds typically pay very high interest rates and are sometimes referred to as

high-yield bonds.

Because junk bonds have a high default risk, they are speculative.

Zero coupon bonds securities

●

●

In a zero coupon bond, the stated rate is zero, meaning that the bonds do not pay

annual interest.

b.

c.

CASE 10.5

This requirement is for students to state in their own words several technical terms. It is

not possible to state a solution that reflects exactly what students will say, but following are

basic ideas that should be included in their definitions:

INTERNET

CREDIT RATINGS

With traditional bonds, the coupon rate is the rate of annual interest the issuer pays

to the bondholder.

BONDS ONLINE

Convertible bonds

Gives the investor the right to convert its bond into stock of the company.

Junk bonds

Junk bonds are low-grade bonds issued by companies without long track records or

within questionable ability to meet their debt obligations.

No definitive answer can be given because market conditions and the information reported

Again, no definitive answer can be given because individual students will have different

●

●

●

You will want to know how many shares of stock you can get for each bond.

The number of shares you can receive, as well as their price, is preset at the bond’s

issue and remains fixed throughout the life of the bond.

market value, is equal to the amount of the bond’s conversion value.