1. No. A discounted note payable has no stated interest rate, but provides interest by discounting the

2. a. Employee’s federal income taxes, social security, and Medicare

3. The deductions from employees’ earnings are for amounts owed (liabilities) to others for

such items as federal taxes, state and local income taxes, and contributions to pension plans.

4. 1. a

3. c

b

5.

b

5. An advantage of using a separate payroll bank account is that reconciling the bank statements

6. a. Constants are data that remain unchanged from payroll to payroll. These include employee

names, social security numbers, marital status, number of income tax withholding

7. The vacation pay expense should be recorded during the period in which the vacation privilege

is earned.

8. In a defined contribution plan, the company invests contributions on behalf of the employee

p

9. To match revenues and expenses properly, the liability to cover product warranties should be

recorded in the period during which the sale of the product is recorded.

CHAPTER 10

CURRENT LIABILITIES AND PAYROLL

DISCUSSION QUESTIONS

10-1

CHAPTER 10 Current Liabilities and Payroll

PE 10–1A

PE 10–1B

PE 10–2A

Total wage payment………………………………………………………

…

$2,500.00

One allowance (provided by IRS)………………………………………

…

$75.00

Multiplied by allowances claimed on Form W-4……………………

…

2150.00

PE 10–2B

Total wage payment………………………………………………………

…

$1,250.00

One allowance (provided by IRS)………………………………………

…

$75.00

Multiplied by allowances claimed on Form W-4……………………

…

175.00

PRACTICE EXERCISES

×

×

10-2

CHAPTER 10 Current Liabilities and Payroll

PE 10–3A

Total wage payment…………………………………………

…

$2,500.00

PE 10–3B

Total wage payment…………………………………………

…

$1,250.00

PE 10–4A

Salaries Expense 220,000

PE 10–4B

Salaries Expense 90,000

CHAPTER 10 Current Liabilities and Payroll

PE 10–5A

Payroll Tax Expense 18,670

PE 10–5B

Payroll Tax Expense 7,370

PE 10–6A

a. Vacation Pay Expense 19,500

PE 10–6B

a. Vacation Pay Expense 35,000

10-4

CHAPTER 10 Current Liabilities and Payroll

PE 10–7A

a. Jan. 31 Product Warranty Expense 15,000

PE 10–7B

July, 4.5% × $325,000.

PE 10–8A

a. December 31, current year

b. The quick ratio of Nabors Company has declined from 1.5 in the previous year to

1.2 in the current year. This decrease is the result of a large increase in accounts

10-5

CHAPTER 10 Current Liabilities and Payroll

PE 10–8B

a. December 31, current year

Quick Ratio = Quick Assets ÷ Current Liabilities

b. The quick ratio of Adieu Company has improved from 1.5 in the previous year to 1.6

10-6

CHAPTER 10 Current Liabilities and Payroll

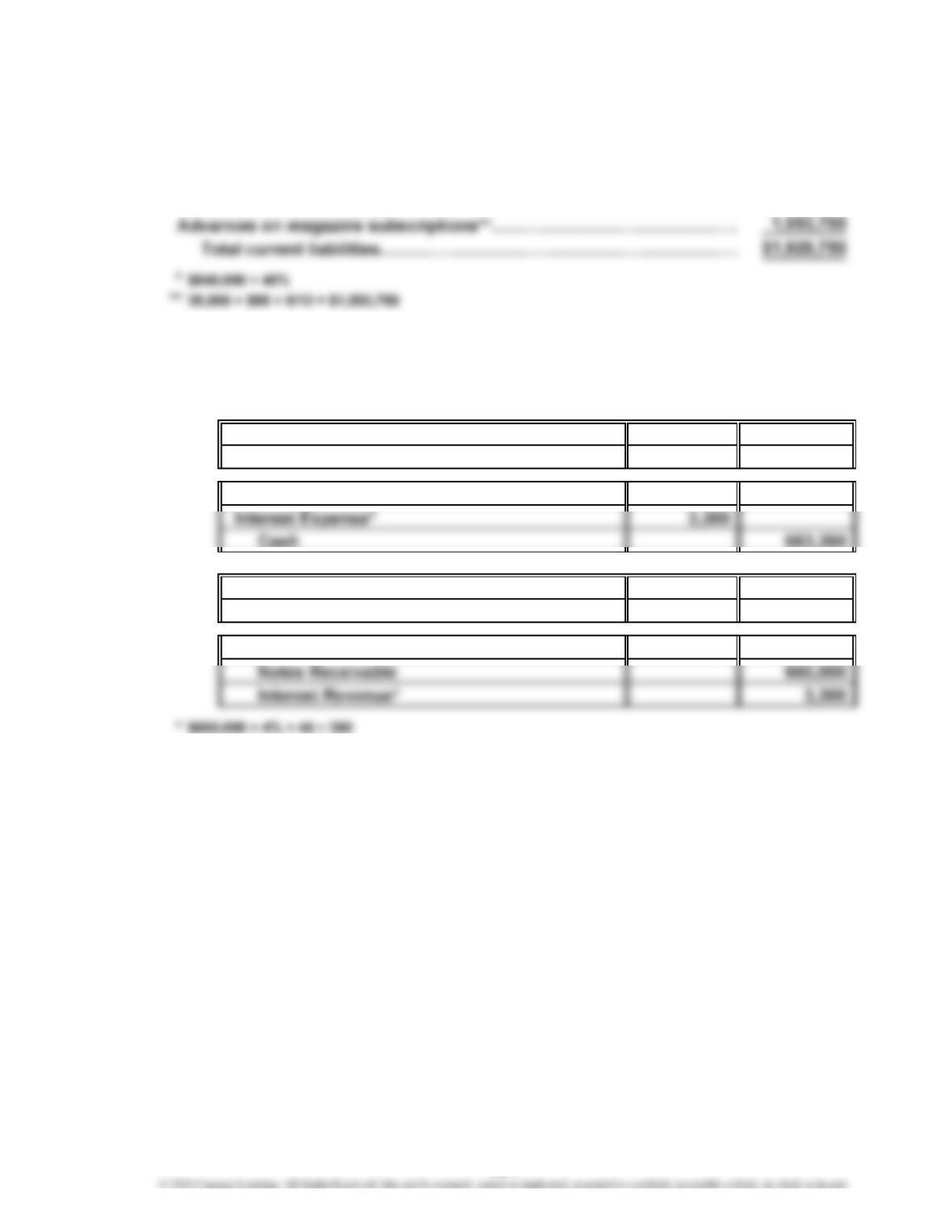

Ex. 10–1

Current liabilities:

Federal income taxes payable*………………………………………………

…

$ 336,000

The nine months of unfilled subscriptions are a current liability because Bon Nebo

received payment prior to providing the magazines.

Ex. 10–2

a. 1. Merchandise Inventory 660,000

Notes Payable 660,000

2. Notes Payable 660,000

b. 1. Notes Receivable 660,000

Sales 660,000

2. Cash 663,300

EXERCISES

10-7

CHAPTER 10 Current Liabilities and Payroll

Ex. 10–3

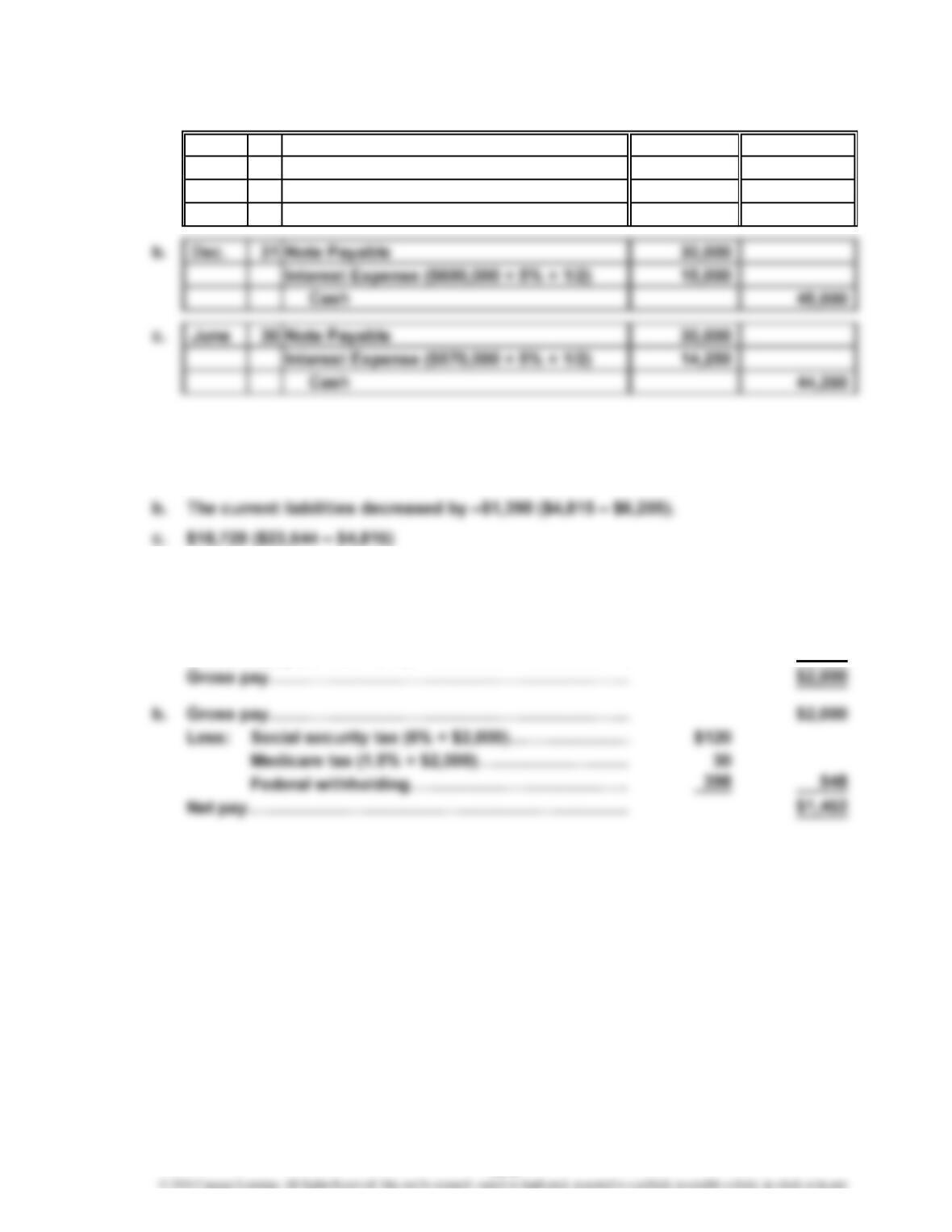

a. $360,000 × 5% × 60 ÷ 360 = $3,000 for each alternative.

b. (1) $360,000 simple-interest note: $360,000 proceeds

(2) $360,000 discounted note: $360,000 – $3,000 interest = $357,000 proceeds

c. Alternative (1) is more favorable to the borrower. This can be verified by

comparing the effective interest rates for each loan as follows:

Situation (1): 5.0% effective interest rate

($3,000 × 360 ÷ 60) ÷ $360,000 = 5%

Ex. 10–4

a. Accounts Payable 210,000

Notes Payable 210,000

Ex. 10–5

a. Accounts Payable 74,125

Interest Expense* 875

10-8

CHAPTER 10 Current Liabilities and Payroll

Ex. 10–6

a. June 30 Building 560,000

Land 400,000

Note Payable 600,000

Cash 360,000

Ex. 10–7

a. $4,815 is the amount disclosed as the current portion of long-term debt.

Ex. 10–8

a. Regular pay (40 hrs. × $32)…………………………………

…

$1,280

Overtime pay (15 hrs. × $48)………………………………… 720

10-9

CHAPTER 10 Current Liabilities and Payroll

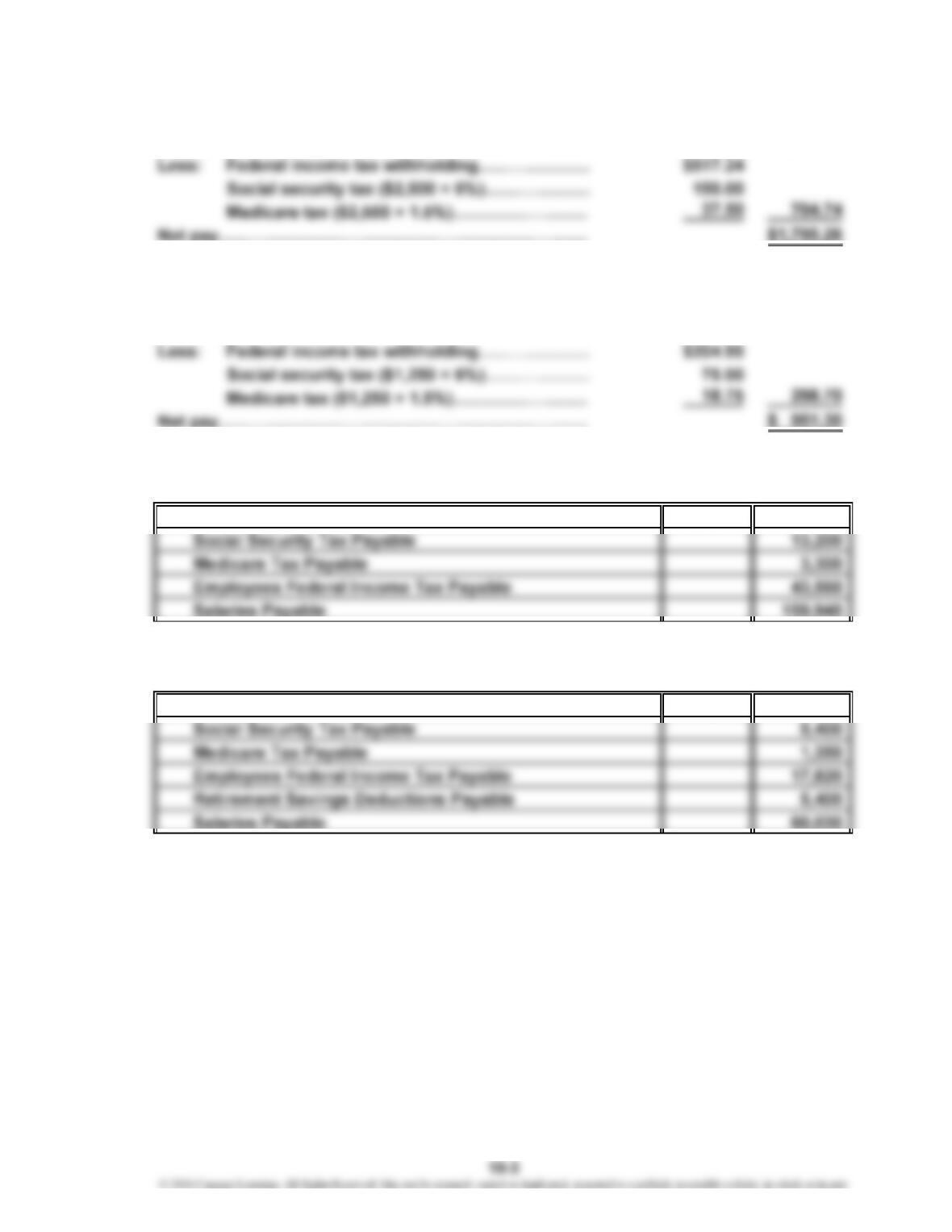

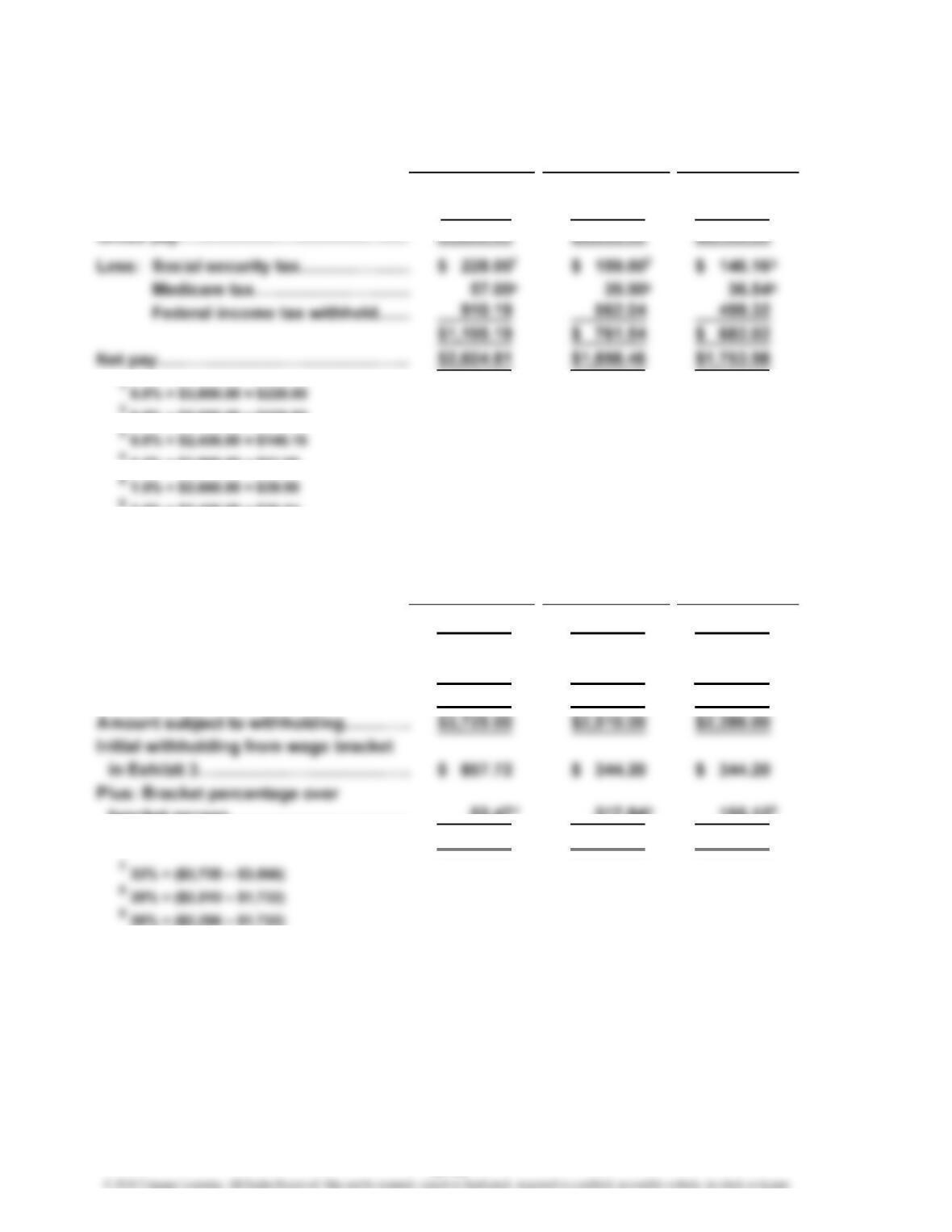

Ex. 10–9

Regular earnings…………………………

…

$3,800.00 $1,520.00 $1,680.00

Overtime earnings………………………

…

1,140.00 756.00

$3,800.00 $2,660.00 $2,436.00

6.0% × $2,660.00 = $159.60

1.5% × $3,800.00 = $57.00

1.5% × $2,436.00 = $36.54

Withholding supporting calculations:

Gross weekly pay…………………………

…

$3,800.00 $2,660.00 $2,436.00

Number of withholding allowances…… 1 2 2

Multiplied by: Value of one allowance

…

× $75.00 × $75.00 × $75.00

Amount to be deducted…………………

…

$ 75.00 $ 150.00 $ 150.00

…

bracket excess…………………………

…

52.47 217.84 155.12

Amount withheld…………………………

…

$ 910.19 $ 562.04 $ 499.32

Computer

Consultant Programmer Administrator

Consultant Programmer

Computer

Administrator

10-10

CHAPTER 10 Current Liabilities and Payroll

Ex. 10–10

a. Summary: (1) $460,000; (3) $540,000; (8) $6,750; (12) $135,000

Net amount paid……………………………………………

…

$338,850

Total deductions……………………………………………

…

201,150

Total deductions……………………………………………

…

$201,150

…

(8) Union dues…………………………………………………… $ 6,750

Total earnings………………………………………………

…

$540,000

…

(12) Sales salaries………………………………………………

…

$135,000

b. Factory Wages Expense 285,000

Sales Salaries Expense 135,000

Office Salaries Expense 120,000

Social Security Tax Payable 32,400

Medicare Tax Payable 8,100

10-11

…

CHAPTER 10 Current Liabilities and Payroll

Ex. 10–11

a. Social security tax (6% × $750,000)…………………………………………… $45,000

Medicare tax (1.5% × $750,000)………………………………………………

…

11,250

b. Payroll Tax Expense 59,350

Social Security Tax Payable 45,000

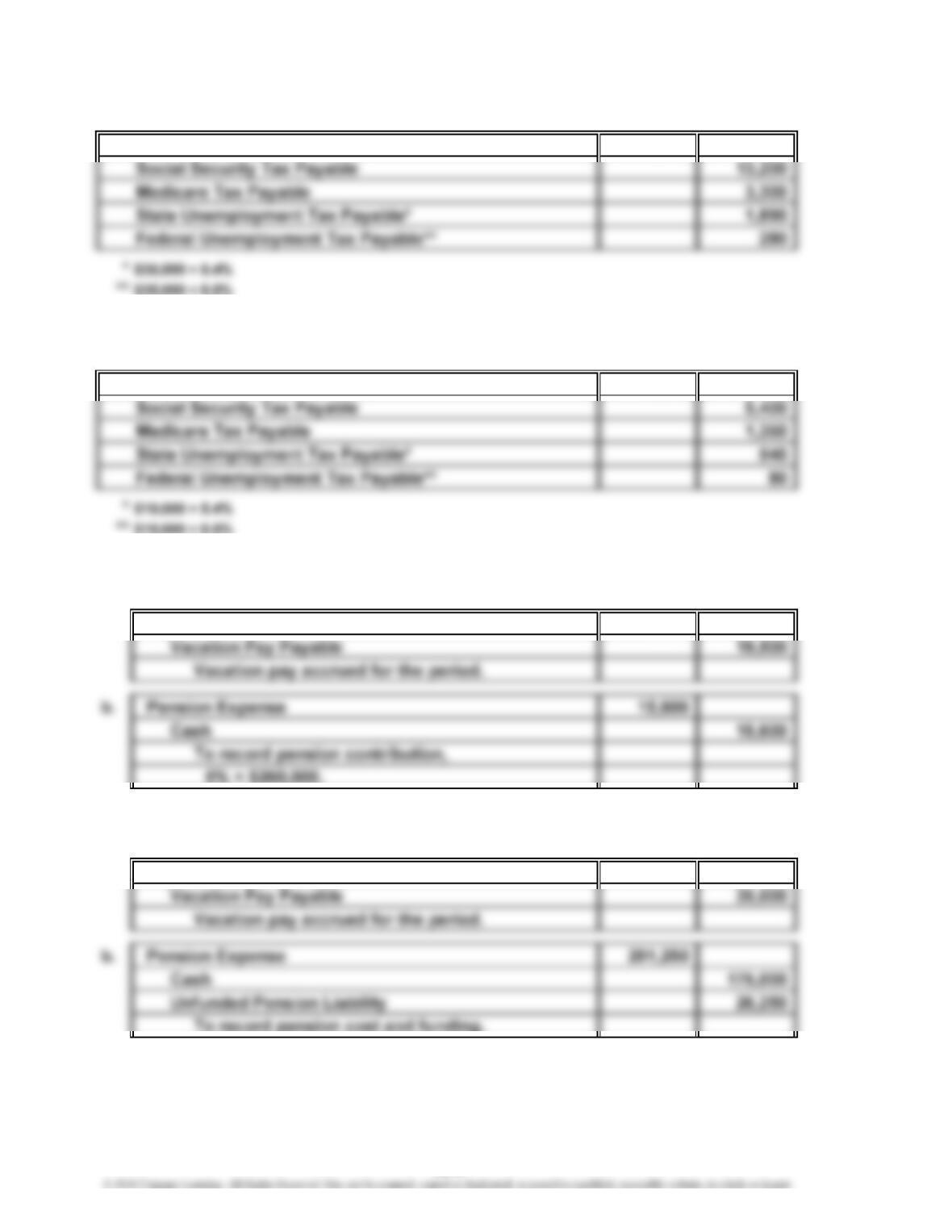

Ex. 10–12

a. Salaries Expense 1,500,000

Social Security Tax Payable 90,000

Medicare Tax Payable 22,500

Employees Federal Income Tax Payable 300,000

10-12

CHAPTER 10 Current Liabilities and Payroll

Ex. 10–13

a. Wages Expense 240,000

Social Security Tax Payable* 14,400

** 1.5% × $240,000

b. Payroll Tax Expense 20,170

*5.4% × $35,000

** 0.8% × $35,000

Ex. 10–14

Big Howie’s Hot Dog Stand does have an internal control procedure that should detect

the payroll error. Before funds are transferred from the regular bank account to the

payroll account, the owner/manager authorizes the total amount of the week’s payroll.

Ex. 10–15

a. Appropriate. All changes to the payroll system, including wage rate increases,

should be authorized by someone outside the Payroll Department.

10-13

CHAPTER 10 Current Liabilities and Payroll

Ex. 10–16

a. Vacation Pay Expense 3,500

Ex. 10–17

a. Dec. 31 Pension Expense 365,000

Unfunded Pension Liability 365,000

To record quarterly pension cost.

Ex. 10–18

The $5,599 million unfunded pension liability is the approximate amount of the pension

obligation that exceeds the value of the net assets of the pension plan. Apparently,

Procter & Gamble has underfunded its plan relative to the obligation that has accrued

over time. This can occur when the company contributes less to the plan than the

annual pension cost.

10-14

CHAPTER 10 Current Liabilities and Payroll

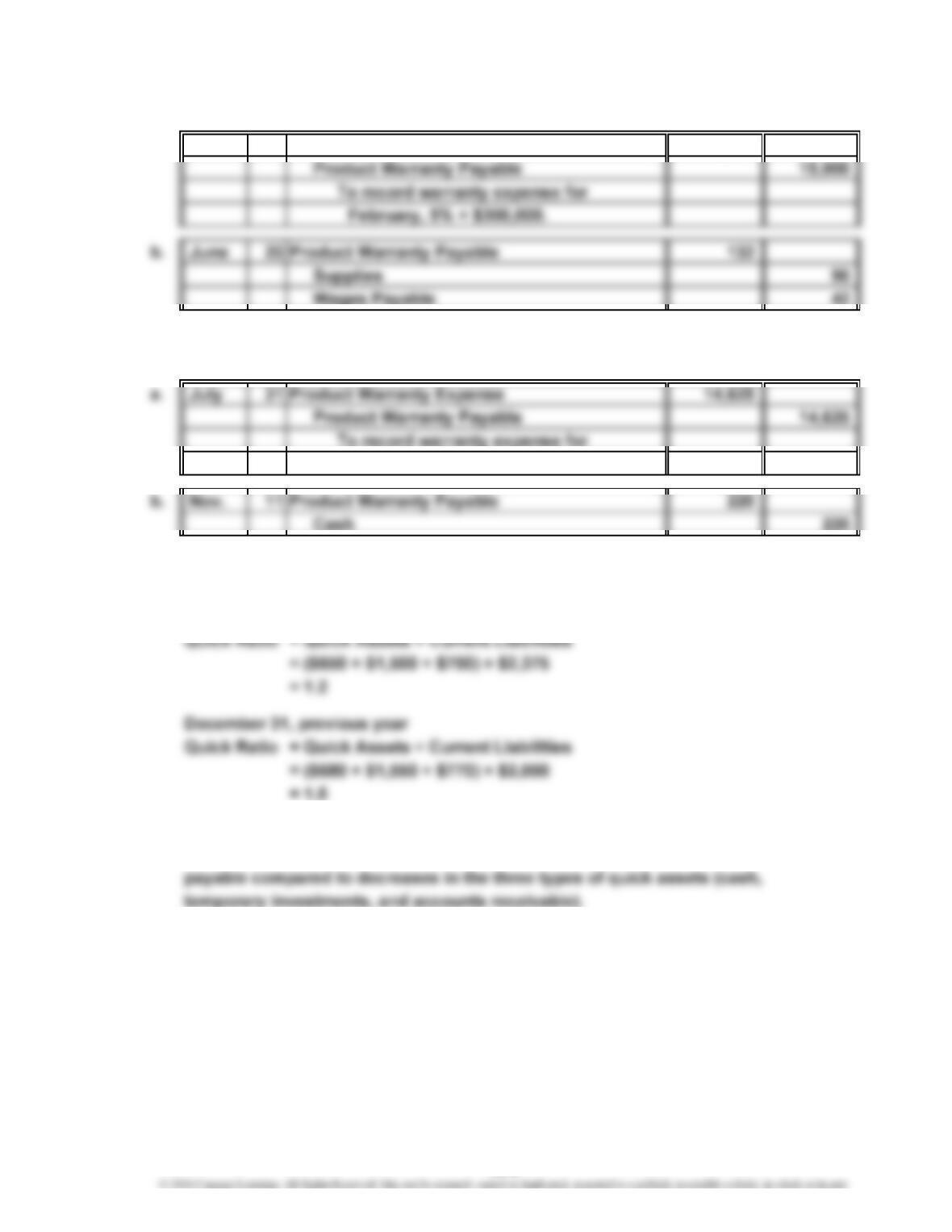

Ex. 10–19

a. Product Warranty Expense 22,400

Product Warranty Payable 22,400

To record warranty expense for June,

4% × $560,000.

Ex. 10–20

a. The warranty liability represents estimated outstanding automobile warranty

claims. Of these claims, $2,884 million is estimated to be due during Year 2, while

the remainder ($4,147 million) is expected to be paid after Year 2. The distinction

10-15

CHAPTER 10 Current Liabilities and Payroll

Ex. 10–21

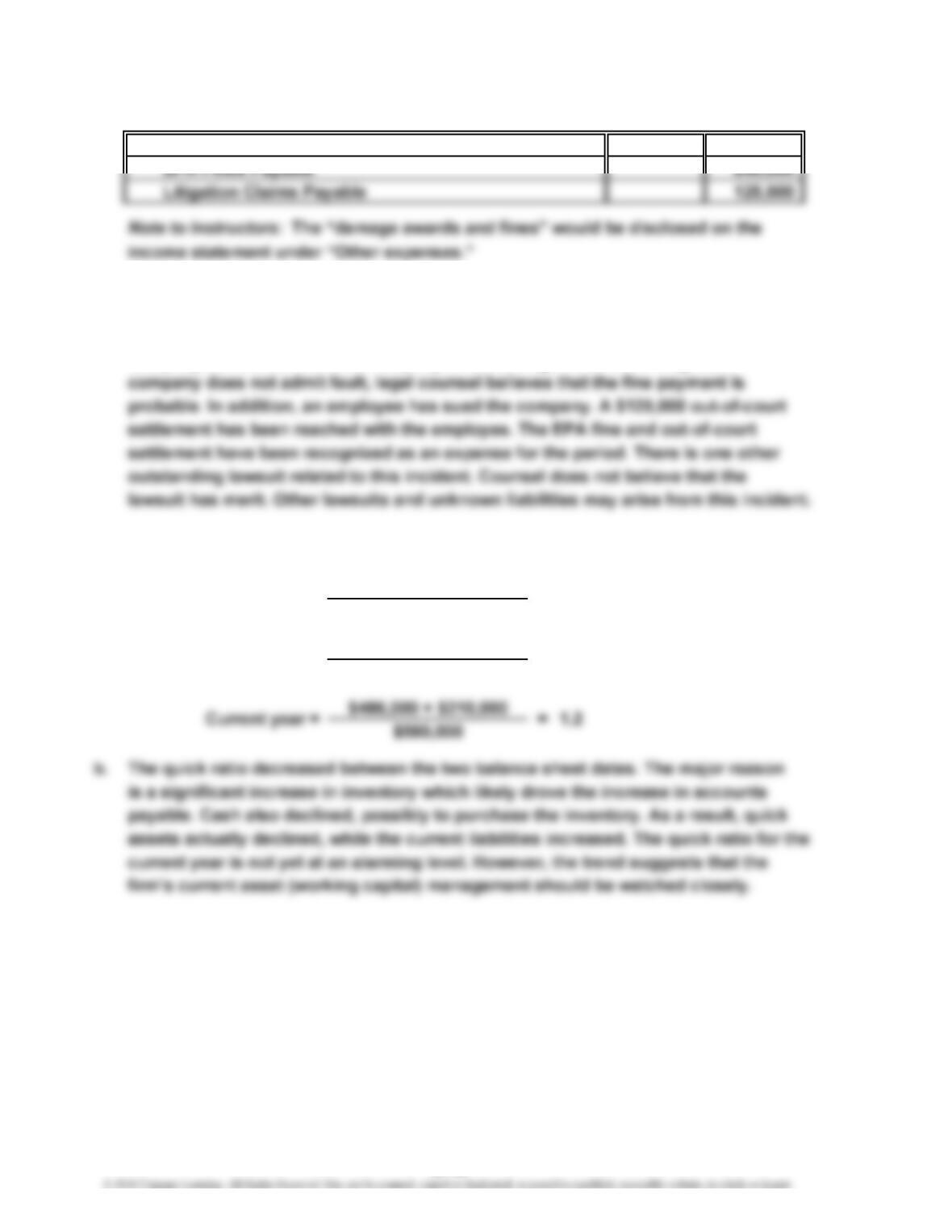

a. Damage Awards and Fines 365,000

b. The company experienced a hazardous materials spill at one of its plants during

the previous period. This spill has resulted in a number of lawsuits to which the

company is a party. The Environmental Protection Agency (EPA) has fined the

company $240,000, which the company is contesting in court. Although the

Ex. 10–22

Quick Assets

Current Liabilities

$500,000 + $200,000

$500,000

Previous year =

a. Quick Ratio =

= 1.4

10-16

CHAPTER 10 Current Liabilities and Payroll

Ex. 10–23

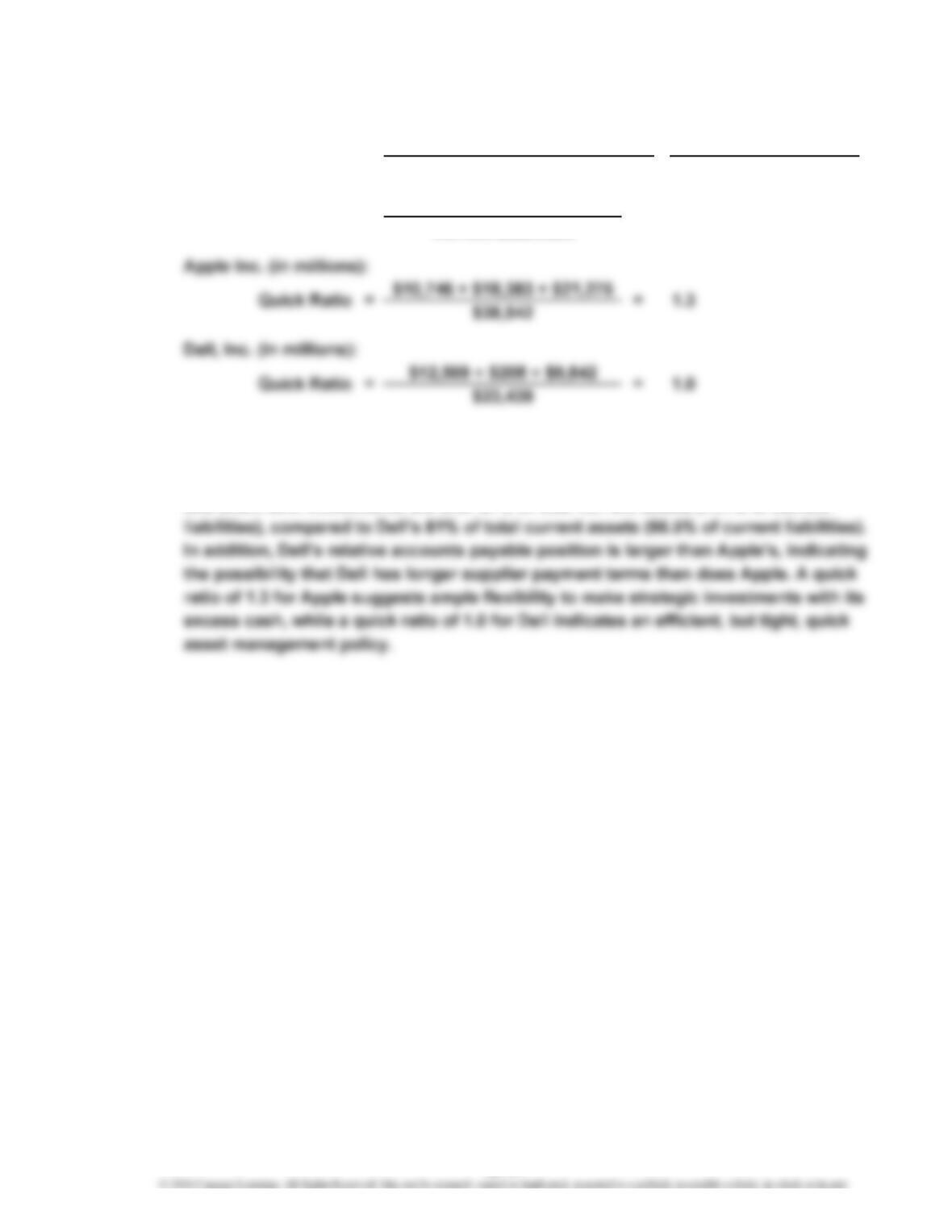

a. Dell, Inc.

Quick Ratio 1.0

Quick Assets

Current Liabilities

b. It is clear that Apple Inc.’s short-term liquidity is stronger than Dell’s. Apple’s quick

ratio is 23% [(1.3 – 1.0) ÷ 1.0] higher. Apple has a much stronger relative cash and

short-term investment position than does Dell. Apple’s cash, accounts receivable,

and short-term investments are over 87% of total current assets (131% of current

Apple Inc.

1.3

Quick Ratio =

10-17

CHAPTER 10 Current Liabilities and Payroll

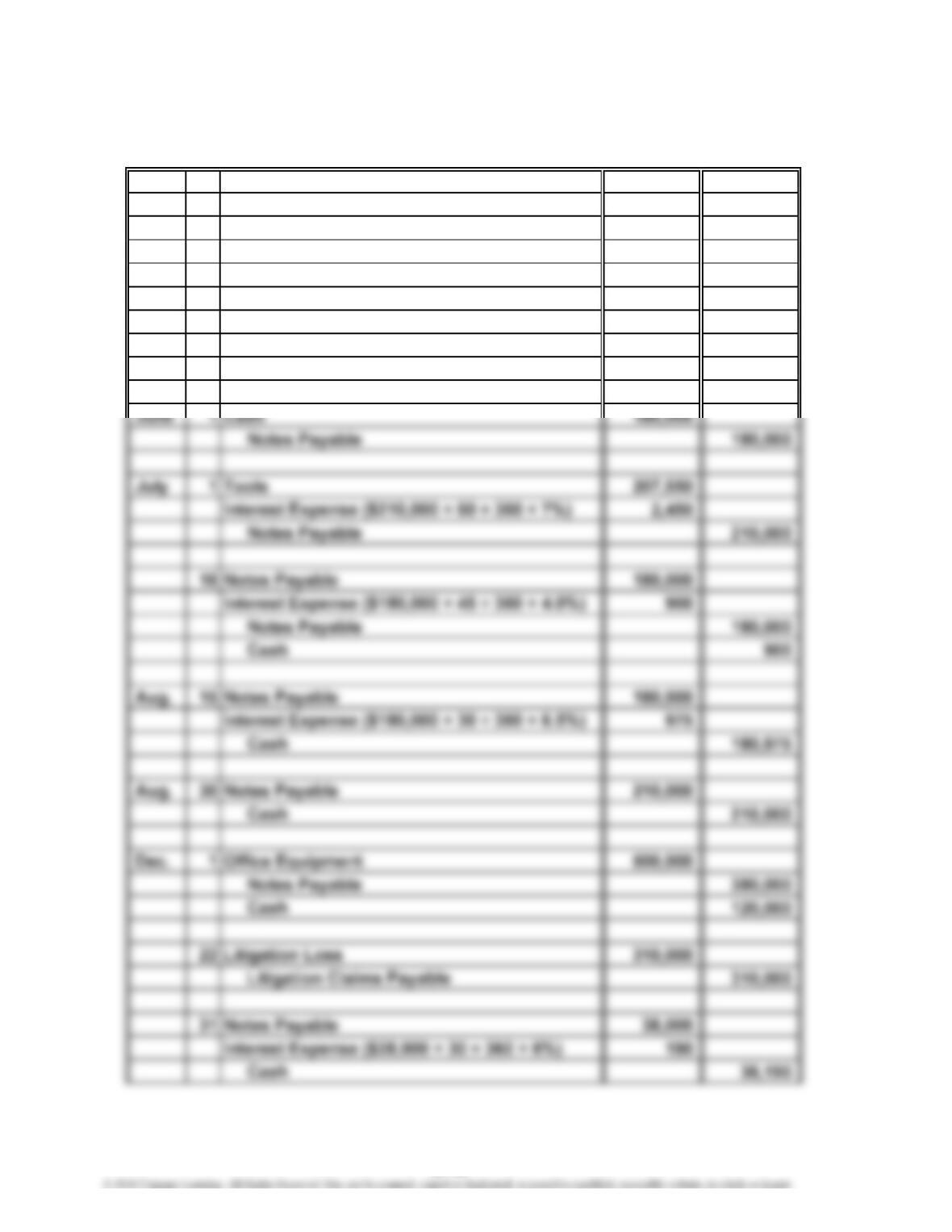

Prob. 10–1A

1. Mar. 1 Merchandise Inventory 360,000

Accounts Payable—Galston Co. 360,000

31 Accounts Payable—Galston Co. 360,000

Notes Payable 360,000

Apr. 30 Notes Payable 360,000

Interest Expense ($360,000 × 30 ÷ 360 × 5%) 1,500

Cash 361,500

PROBLEMS

10-18

CHAPTER 10 Current Liabilities and Payroll

Prob. 10–1A (Concluded)

2. a. Product Warranty Expense 27,500

Product Warranty Payable 27,500

10-19

CHAPTER 10 Current Liabilities and Payroll

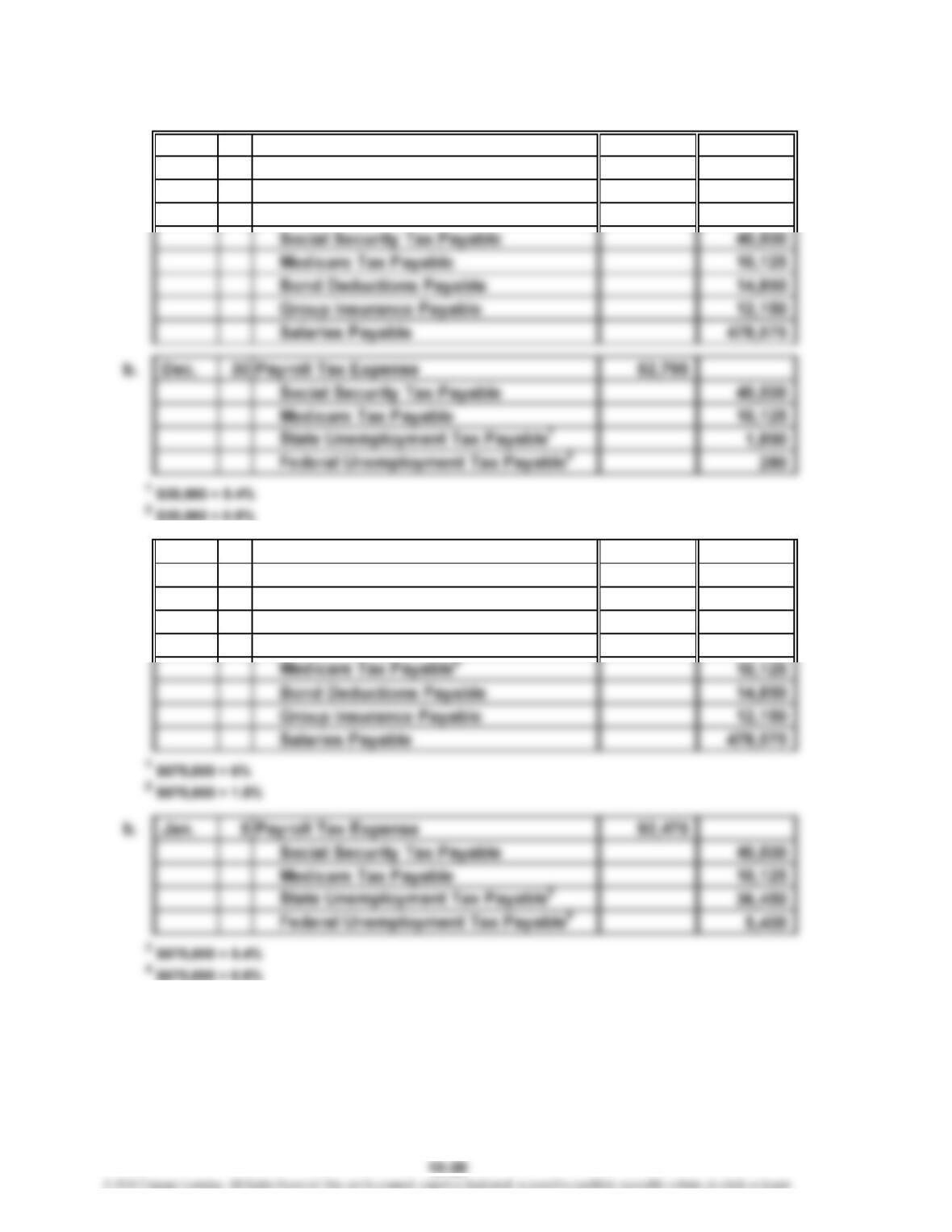

Prob. 10–2A

1. a. Dec. 30 Sales Salaries Expense 350,000

Warehouse Salaries Expense 180,000

Office Salaries Expense 145,000

Employees Income Tax Payable 118,800

2. a. Dec. 30 Sales Salaries Expense 350,000

Warehouse Salaries Expense 180,000

Office Salaries Expense 145,000

Employees Income Tax Payable 118,800

Social Security Tax Payable140,500