Chapter 10—Liabilities

Financial and Managerial Accounting, 18e 10-1

10 LIABILITIES

Chapter Summary

At the outset, the chapter distinguishes between current and long-term liabilities before

addressing the accounting issues surrounding each category.

Among current liabilities, notes payable and payroll related costs are analyzed in detail.

Journal entries are introduced to record the issuance of a note, the accrual of interest expense,

and the payment of interest and principal. Payroll costs such as FICA and Medicare taxes,

unemployment insurance, workers’ compensation, and the employer’s share of benefits are

explained and contrasted with other amounts withheld from the employees’ paychecks. A

number of other current liabilities with which the student is already familiar are reviewed in

brief. Long-term liabilities are introduced using installment notes payable. An example of an

amortization schedule illustrates the allocation of installment payments between interest expense

and principal reduction. The amortization table serves as the basis for preparing journal entries

relative to the note and is also used to demonstrate that the portion of principal scheduled to be

paid in the next 12 months is classified as a current liability.

Bonds payable are discussed in some detail with emphasis on the nature and advantages

of bond financing. Accounting treatment covers bonds issued at par, at a premium, and at a

discount. A number of advanced topics are covered including issuance between interest payment

dates, price fluctuations after issuance, and early retirement. Estimated liabilities, commitments,

and contingencies are discussed. Other long-term liabilities introduced include leases, pensions

and other post-retirement costs, and deferred income taxes.

The chapter includes an analysis of the interest coverage ratio and financial leverage.

This discussion emphasizes how creditors use accounting data to evaluate the safety of their

claims.

Learning Objectives

1. Define liabilities and distinguish between current and long-term liabilities.

2. Account for notes payable and interest expense.

3. Describe the costs and the basic accounting activities relating to payrolls.

4. Prepare an amortization table allocating payments between interest and principal.

5. Describe corporate bonds and explain the tax advantage of debt financing.

6. Account for bonds issued at a discount or premium.

Chapter 10—Liabilities

10-2 Instructor’s Resource Manual

7. Explain the concept of present value as it relates to bond prices.

8. Explain how estimated liabilities, loss contingencies, and commitments are disclosed in

financial statements.

9. Evaluate the safety of creditors’ claims.

10. Describe reporting issues related to leases, postretirement benefits, and deferred taxes.

Brief Topical Outline

A. The nature of liabilities

1. Distinction between debt and equity

2. Many liabilities bear interest

3. Estimated liabilities

B. Current liabilities

1. Accounts payable

2. Notes payable

3. The current portion of long-term debt

4. Accrued liabilities

5. Payroll liabilities

a. Payroll taxes and mandated costs

b. Other payroll-related costs

c. Amounts withheld from employees’ pay

d. Recording payroll activities

6. Unearned revenue

C. Long-term liabilities

1. Maturing obligations intended to be refinanced—see International Case in

Point (page 440)

2. Installment notes payable

a. Allocating installment payments between interest and principal

b. Preparing an amortization table

c. Using an amortization table

d. The current portion of long-term debt

3. Bonds payable

4. What are bonds?

a. The issuance of bonds payable

b. Transferability of bonds

c. Quoted market prices

d. Types of bonds

e. Junk bonds

5. Tax advantage of bond financing

6. Accounting for bonds payable

a. Bonds issued between interest dates

7. Bonds issued at a discount or a premium

8. Accounting for a bond discount: an illustration

Chapter 10—Liabilities

Financial and Managerial Accounting, 18e 10-3

a. Bond discount: part of the cost of borrowing

b. Amortization of the discount

9. Accounting for a bond premium: an illustration

a. Bond premium: a reduction in the cost of borrowing

b. Amortization of the premium

10. Bond discount and premium in perspective

11. The concept of present value

a. The present value concept and bond prices

12. Bond prices after issuance—see Case in Point (page 453)

a. Volatility of short-term and long-term bond prices—see Your Turn (page

454)

13. Early retirement of bonds payable

D. Estimated liabilities, loss contingencies, and commitments

1. Estimated liabilities

2. Loss contingencies

a. Loss contingencies in financial statements

3. Commitments

E. Evaluating the safety of creditors’ claims

1. Methods of determining creditworthiness

a. Interest coverage ratio

b. Less formal means of determining creditworthiness

2. How much debt should a business have? See Pathways Connection and Your

Turn (page 458), and Ethics, Fraud, & Corporate Governance (page 459)

F. Special types of liabilities

1. Lease payment obligations

2. Operating leases

3. Capital leases

a. Distinguishing between capital leases and operating leases

4. Liabilities for pensions and other postretirement benefits

a. Determining pension expense

b. Postretirement benefits other than pensions

c. Unfunded postretirement costs are noncash expenses

d. Unfunded liabilities for postretirement costs: are they significant amounts?

5. Deferred income taxes

G. Concluding remarks

Chapter 10—Liabilities

10-4 Instructor’s Resource Manual

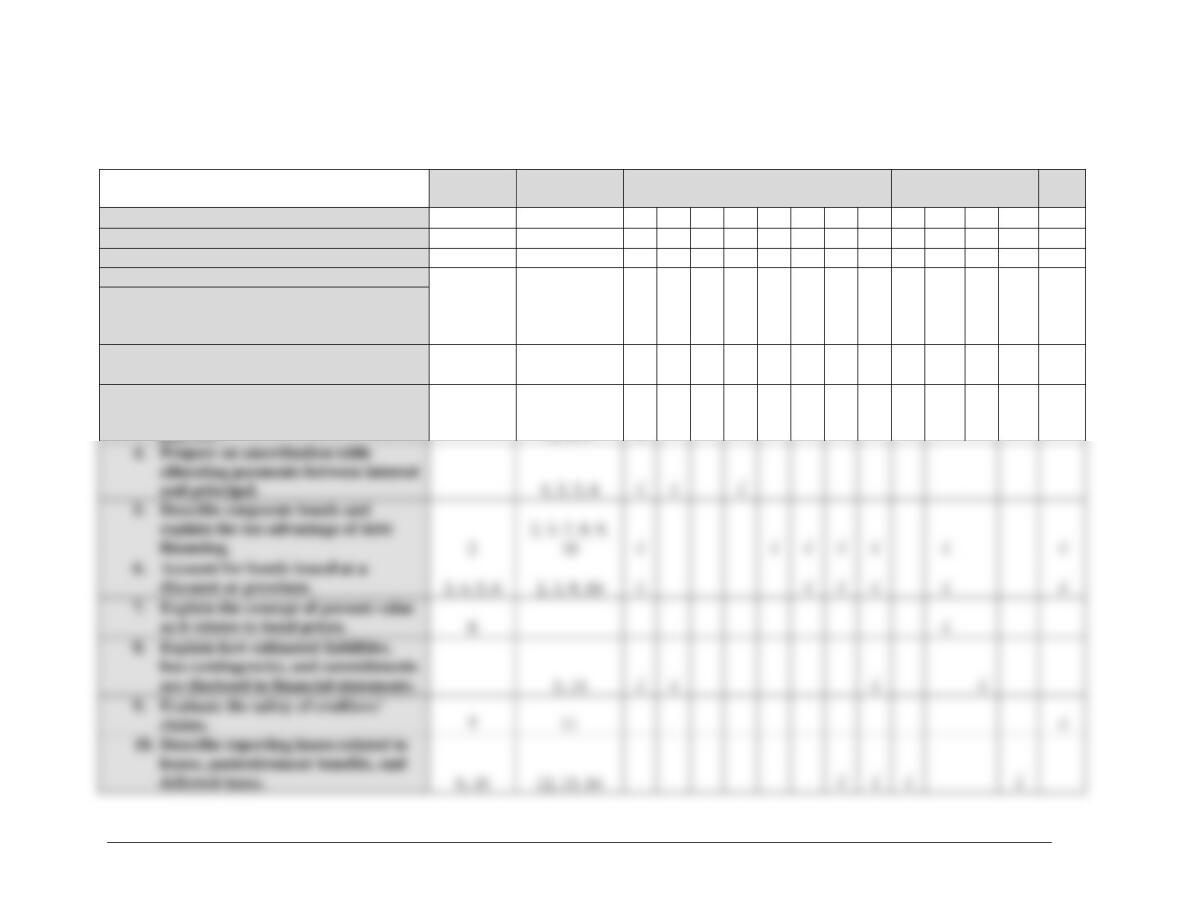

Topical Coverage and Suggested Assignment

Class

Meetings

on Chapter

Topical

Outline

Coverage

Discussion

Questions*

Brief

Exercises*

Exercises*

Problems*

Critical

Thinking

Cases*

1

A – B

1, 2, 3

1, 2

1, 2, 3, 4

2, 3

2

C – D

6, 7, 8

3, 4, 5, 6

7, 8, 9

4, 6

2

3

E – I

11, 12, 13

9, 10

12, 13, 14

8

*Homework assignment (to be completed prior to class)

Comments and Observations

Teaching Objectives for Chapter 10

In presenting the broad topic of liabilities, our teaching objectives in this chapter are to:

1. Define liabilities. Distinguish between liabilities and owners’ equity.

2. Distinguish between current and long-term liabilities (including classification of the current

portions of long-term debt and of short-term liabilities expected to be refinanced on a long-

term basis).

3. Account for notes payable when interest is stated separately.

4. Explain the nature of payroll liabilities including payroll taxes and other mandated costs.

5. Explain the purpose of an amortization table. Illustrate the preparation and use of such a

table in the context of an installment note payable.

6. Discuss the characteristics of corporate bonds including their tax advantages, and the basic

journal entries to record their issuance, payment of interest, and redemption.

7. Explain the nature of bonds issued at a discount or premium.

8. Introduce the concept of present value and its relationship to bond prices.

9. Distinguish between capital leases and operating leases and briefly explain their accounting

treatment.

10. Introduce other long-term liabilities including pensions, post-retirement benefits, and

deferred taxes. Describe the presentation of these items in the financial statements.

11. Describe the cash effects of transactions involving liabilities.

12. Explain the usefulness of the debt ratio and the interest coverage ratio.

Chapter 10—Liabilities

Financial and Managerial Accounting, 18e 10-5

13. Explain the nature of estimated liabilities, loss contingencies, and commitments. Describe the

presentation of these items in financial statements.

General Comments

Chapter 10 opens with a general discussion of the nature of current liabilities. We

recommend Problem 1 to distinguish between current and contingent liabilities and to show that

liabilities relate to past, rather than future, transactions.

What actually constitutes a “liability” is not a cut-and-dried issue, either for introductory

accounting students, or in accounting practice. Hence, we always review in class an assignment

such as Exercise 3 and/or Case 1. These assignments address the nature and classification of

liabilities, and of obligations that do not qualify as “liabilities.” We believe that if students

understand the concepts involved in these assignments, they have acquired a good working

knowledge of how various types of obligations are reported and disclosed in financial statements.

In discussing the general nature of liabilities, we point out that only interest that has

accrued through the balance sheet date is a liability. No liability currently exists with respect to

interest charges applicable to future periods. This concept provides the foundation for

accounting for notes payable.

We devote little class time to payroll taxes. We do explain that taxes withheld from

employees are current liabilities of the employer, but do not increase the overall cost of having

employees on the payroll (except for administration costs). On the other hand, payroll taxes

levied upon the employer increase the cost of employing a work force to an amount greater than

the wages and salaries expense. In view of the various current proposals for financing health

care, this has become a particularly important point.

We also devote little class time to bonds payable. The basic entries concerning a bond

issue—issuance, interest payments, and retirements—may be illustrated quickly by reviewing an

assignment such as Exercise 8, Exercise 9, Exercise 10, or Problem 5.

Many corporations have recorded the one time charge for post-retirement benefits. We

have therefore commented upon the significance of these unfunded liabilities and their cash flow

effects.

Loss contingencies are of vital importance but can be covered quickly as the topic

generally does not involve computations or entries in the accounting records. We highly

recommend an in-class review of Case 3 to give students “a feel” for what types of loss

contingencies should be accrued, disclosed, or ignored. Examples of critically important loss

contingencies abound, as indicated in the Asides below:

An aside. We like to use a few “real world” examples to indicate the potential impact of loss

contingencies. For example, the Texas State Courts awarded Pennzoil an $11 billion judgment

against Texaco for Texaco’s alleged “improper actions” in outbidding Pennzoil for the

acquisition of Getty Oil. This judgment forced Texaco, one of the world’s largest and most

profitable oil companies, to seek the protection of the Bankruptcy Court under Chapter 11 of the

Bankruptcy Code. During the following year, Texaco emerged from Chapter 11 when this $11

billion loss contingency was settled for approximately $3 billion.

The large pharmaceutical company A. H. Robbins was forced into bankruptcy by product

liability suits, brought against the company by users of the Dalkon Shield, an intrauterine birth

control device.

Chapter 10—Liabilities

10-6 Instructor’s Resource Manual

In most cases, the footnotes to the companies’ financial statements disclose the nature of

the pending litigation long before a company is forced into bankruptcy. However, it remains for

the reader of the financial statements to evaluate the financial risk associated with the pending

litigation.

Supplemental Exercises

Group Exercise

Current liabilities are defined as obligations that will be paid from current assets. As a

result creditors and potential creditors are keenly interested in the relationship between a

company’s current assets and is current liabilities. This relationship is often measured by

dividing current assets by current liabilities to produce what is called the current ratio. The ratio

shows how many dollars of current assets are available for each dollar of current liabilities.

Clearly, the larger the ratio the more secure are the claims of short-term creditors.

Choose four publicly held companies and using their annual reports, compute the current

ratio for each. Based on your results, discuss how secure the claims of these companies’ short-

term creditors seem to be.

Internet Exercise

1. Obtain the annual report of the Harley Davidson Company either from the Harley-Davidson

website or from the SEC’s EDGAR site. Read the footnote regarding commitments and

contingencies and describe the information you find.

2. It is widely appreciated that the Federal Reserve System controls interest rates in the United

States. Visit the Federal Reserve System website and write a short report on the history of the

Federal Reserve Board, how they establish interest rates, and how those rates impact the

present value of a bond issuance.

Chapter 10—Liabilities

Financial and Managerial Accounting, 18e 10-7

CHAPTER 10 NAME #

10-MINUTE QUIZ A SECTION

Indicate the best answer for each question in the space provided.

On November 30, 2018, Central Food purchased two trucks for a total of $140,000, issuing a one-year,

6% note payable, all due at maturity. The interest on this loan is stated separately.

1. Refer to the above data. The December 31, 2018, adjusting entry for this note includes:

a A credit to Cash for $1,400.

b A credit to Interest Payable for $8,400.

c A credit to Interest Payable for $1,400.

d A credit to Interest Payable for $700.

2. Refer to the above data. The total liabilities related to this note reported in Central Food’s

December 31, 2018, balance sheet is:

a $140,000. b $148,400. c $140,700. d $141,400.

3. Refer to the above data. What is the amount of interest expense Central Food’s recognizes on this

note in 2019?

a $700. b $8,400. c $7,700. d $1,400.

4. Refer to the above data. How much must Central Food pay the lender upon maturity of this note?

a $140,700. b $140,000. c $147,700. d $148,400.

5. Refer to the above data. The liability for this loan as of December 31, 2018:

a Is equal to its maturity value.

b Is equal to the book value of the two trucks that were acquired in exchange.

c Is classified as a long-term liability, since it was used to acquire non-current assets.

d Is classified as a long-term liability if Central Food has the intent and ability to refinance by

taking out a new loan not due for several years.

Chapter 10—Liabilities

10-8 Instructor’s Resource Manual

CHAPTER 10 NAME #

10-MINUTE QUIZ B SECTION

Shown below is a summary of the annual payroll data of Rose Co.:

Wages and salaries expense (gross pay)

$2,250,000

Amounts withheld from employees’ pay:

Income taxes ……………………………………………………

$170,000

Social Security and Medicare …………………………….

$150,000

320,000

Payroll taxes expense:

Social Security and Medicare …………………………….

$150,000

Unemployment taxes ………………………………………..

58,000

208,000

Workers’ compensation premiums ……………………………..

130,000

Group health insurance premiums (paid by employer)

252,000

Contributions to employees’ pension plan (paid by

employer and fully funded) ……………………………….

140,000

Cost of other postretirement benefits:

Funded ……………………………………………………………

$90,000

Unfunded ………………………………………………………..

120,000

210,000

1. Refer to the above data. Rose Company’s total payroll-related expense for the year is:

a $2,250,000. b $3,510,000. c $2,840,000. d $3,190,000.

2. Refer to the above data. Compute the company’s cash outlays during the year for payroll-related

costs. Assume short-term obligations such as insurance premiums and payroll taxes have been paid.

a $2,750,000. b $3,070,000. c $1,930,000. d $3,510,000.

3. Refer to the above data. The annual “take-home-pay” of Rose’ employees is:

a $2,520,000. b $2,250,000. c $1,930,000. d $2,750,000.

4. Refer to the above data. Amounts paid during the year to retirees for pension and other

postretirement benefits total:

a $140,000. b $350,000. c $230,000. d None of above.

5. Refer to the above data. When a company has a fully-funded pension plan:

a The dollar amounts paid to retirees are greater than the amounts recognized as pension

expense by the employer.

b Pension expense is equal to the cash payments made to retirees during the current period.

c No pension expense is recognized in the income statement.

d It does not use the services of a trustee to operate the pension plan.

Chapter 10—Liabilities

Financial and Managerial Accounting, 18e 10-9

CHAPTER 10 NAME #

10-MINUTE QUIZ C SECTION

Seaview Industries received authorization on December 31, Year 1, to issue $7,000,000 face value of 6%,

10-year bonds. The interest payment dates are June 30 and December 31. All the bonds were issued at

par, plus accrued interest, April 1, Year 2. The bonds are callable by Seaview Industries at any time at

102.

1. Prepare the journal entry to record issuance of the bonds on April 1, Year 2.

2. Prepare the journal entry to record the first semiannual interest payment on the bonds at June 30,

Year 2.

3. What is the amount of bond interest expense that appears in Seaview’s Year 2 income statement

relating to these bonds?

$_________________________

4. What is the amount of accrued bond interest expense that appears in Seaview’s balance sheet at

December 31, Year 2, with respect to these bonds?

$_________________________

5. Seaview exercises the call provision and retires one-half of the bond issue on July, 1, Year 4. Prepare

the journal entry to record this transaction on July 1, Year 4.

Chapter 10—Liabilities

10–10 Instructor’s Resource Manual

CHAPTER 10 NAME #

10-MINUTE QUIZ D SECTION

On December 1, 2019, Fisher Corporation incurs a 30-year, $400,000 mortgage liability upon purchase of

a warehouse. This mortgage is payable in monthly installments of $4,116, which include interest

computed at the rate of 12% per year. The first monthly payment is made on December 31, 2019.

1. How much of the first payment made on December 31, 2019, is allocated to repayment of

principal?

$________

2. What is the total liability related to this mortgage to be reported in Fisher’s balance sheet at

December 31, 2019? (Do not separate into current and long-term portions.)

$________

3. The portion of the second monthly payment made on January 31, 2020, which represents interest

expense is:

$________

4. What is the aggregate amount paid by Fisher over the 30-year life of the mortgage?

$________

5. Over the 30-year life of the mortgage, the total amount Fisher will pay for interest charges is

$________

Chapter 10—Liabilities

Financial and Managerial Accounting, 18e 10–11

SOLUTIONS TO CHAPTER 10 10–MINUTE QUIZZES

QUIZ A

1 D

QUIZ B

QUIZ C

1

Cash …………………………………………………………………………………….. 7,105,000

Bonds Payable ………………………………………………………………….. 7,000,000

5

Chapter 10—Liabilities

10–12 Instructor’s Resource Manual

QUIZ D

Chapter 10—Liabilities

Financial and Managerial Accounting, 18e 10–13

Assignment Guide to Chapter 10

Brief

Exercises

Exercises

Problems

Cases

Net

Item Number

1-10

1-15

1

2

3

4

5

6

7

8

1

2

3

4

5

Time estimate (in minutes)

<15

<15

25

30

25

25

15

35

45

30

30

20

25

20

20

Difficulty rating

E

E

E

M

M

M

E

S

S

M

M

S

M

M

S

Learning Objectives:

2, 3

1. Define liabilities and distinguish

between current and long-term

liabilities.

2. Account for notes payable and

interest expense.

1

2, 3

3. Describe the costs and the basic

accounting activities relating to

payrolls.

2, 4, 5

financing.

2

6. Account for bonds issued at a

discount or premium.

3, 4, 5, 6

7. Explain the concept of present value

are disclosed in financial statements.

claims.

7

deferred taxes.

12, 13, 14