COMPREHENSIVE PROBLEM (Continued)

10. Amortization Expense ………………………………….. 900

Patents …………………………………………………… 900

COMPREHENSIVE PROBLEM (Continued)

(b) HASSELLHOUF COMPANY

Trial Balance

December 31, 2017

Debits

Credits

Cash …………………………………………………………..

Accounts Receivable …………………………………..

Notes Receivable ………………………………………..

Interest Receivable ……………………………………..

Inventory …………………………………………………….

Prepaid Insurance ……………………………………….

Land …………………………………………………………..

Buildings ……………………………………………………

Equipment ………………………………………………….

Owner’s Capital …………………………………………..

Owner’s Drawings ……………………………………….

Sales Revenue …………………………………………….

Interest Revenue …………………………………………

Rent Revenue ……………………………………………..

Gain on Disposal of Plant Assets …………………

$ 8,700

45,800

10,000

600

29,900

1,200

20,000

150,000

77,800

12,000

113,600

914,000

600

2,000

750

COMPREHENSIVE PROBLEM (Continued)

(c) HASSELLHOUF COMPANY

Income Statement

For the Year Ended December 31, 2017

Sales Revenue ……………………………………………

Cost of Goods Sold …………………………………….

Gross Profit ……………………………………………….

Operating Expenses

Income From Operations …………………………….

Other Revenues and Gains

Rent Revenue ………………………………………..

Gain on Disposal of Plant Assets ……………

2,000

750

$914,000

636,300

277,700

76,750

HASSELLHOUF COMPANY

Owner’s Equity Statement

For the Year Ended December 31, 2017

Owner’s Capital, 1/1/17 ………………………………………………..

Add: Net Income ………………………………………………………….

$113,600

76,410

COMPREHENSIVE PROBLEM (Continued)

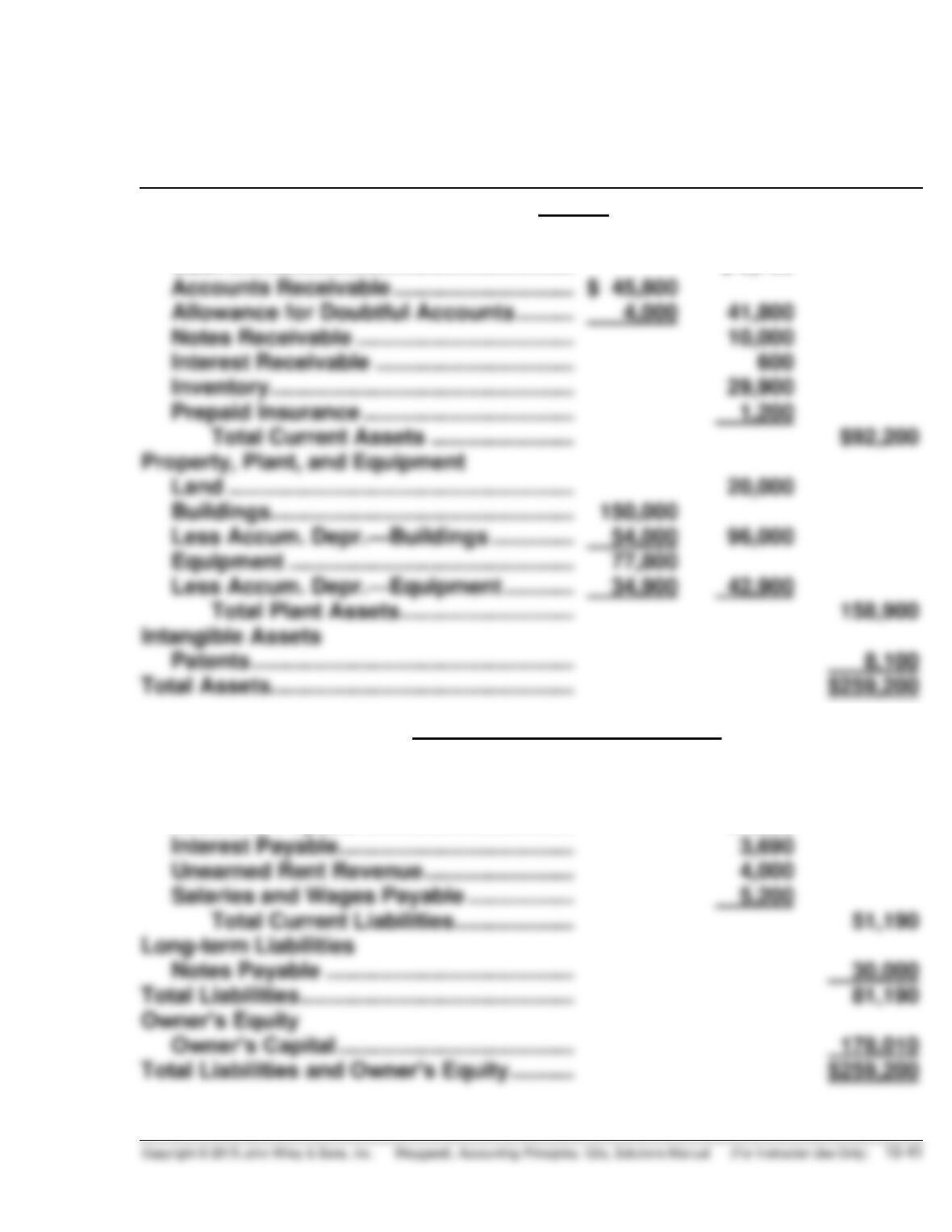

(d) HASSELLHOUF COMPANY

Balance Sheet

December 31, 2017

Assets

Current Assets

Cash ………………………………………………….

Accounts Receivable ………………………….

Allowance for Doubtful Accounts ………..

Notes Receivable ……………………………….

Equipment …………………………………………

Less Accum. Depr.—Equipment ………….

Total Plant Assets …………………………

Intangible Assets

$ 45,800

4,000

77,800

34,900

$ 8,700

41,800

10,000

42,900

158,900

Liabilities and Owner’s Equity

Current Liabilities

Notes Payable ……………………………………

Accounts Payable ………………………………

Interest Payable ………………………………….

Unearned Rent Revenue ……………………..

$11,000

27,300

3,690

4,000

BYP 10-1 FINANCIAL REPORTING PROBLEM

(a) Property, plant, and equipment is reported net, book value, on the

September 28, 2013, balance sheet at $16,597,000,000. The cost of the

property, plant, and equipment is $28,519,000,000 as shown in Note 3.

(b) Depreciation and amortization expense was:

(c) Apple’s capital spending was:

BYP 10-2 COMPARATIVE ANALYSIS PROBLEM

(a)

PepsiCo

Coca-Cola

(b) The asset turnover measures how efficiently a company uses its assets

to generate sales. It shows the dollars of sales generated by each dollar

BYP 10-3 COMPARATIVE ANALYSIS PROBLEM

(a)

Amazon

Wal-Mart

Asset

(b)The asset turnover measures how efficiently a company uses its assets

to generate sales. It shows the dollars of sales generated by each dollar

BYP 10-4 REAL-WORLD FOCUS

Answers will vary depending on the company selected.

BYP 10-5 DECISION MAKING ACROSS THE ORGANIZATION

(a) Pinson Company—Straight-line method

Annual Depreciation

Buildings [($360,000 – $20,000) ÷ 40] ………………………… $ 8,500

Equipment [($130,000 – $10,000) ÷ 10] ………………………. 12,000

Year

Asset

Computation

Annual

Depreciation

Accumulated

Depreciation

2015

2016

Buildings

Equipment

Buildings

$360,000 X 5%

$130,000 X 20%

$342,000 X 5%

$18,000

26,000

17,100

$44,000

(b)

Year

Pinson

Company

Net Income

Estes

Company

Net Income

As Adjusted

Computations for Estes Company

2015

2016

$ 84,000

88,400

$ 91,500

93,400

$68,000 + $44,000 – $20,500 = $91,500

$76,000 + $37,900 – $20,500 = $93,400

(c) As shown above, when the two companies use the same depreciation

method, Estes Company is more profitable than Pinson Company. When

BYP 10-5 (Continued)

(1) its earnings are generating more cash than the earnings of Pinson

Company, and (2) depreciation expense has no effect on cash. Cash

generated by operations can be arrived at by adding depreciation expense

BYP 10-6 COMMUNICATION ACTIVITY

To: Instructor

From: Student

Re: American Exploration Company footnote

American Exploration Company accounts for its oil and gas activities using

the successful efforts approach. Under this method, only the costs of

successful exploration are included in the cost of the natural resource, and

BYP 10-7 ETHICS CASE

(a) The stakeholders in this situation are:

• Robert Griffin, president of Turner Container Company.

• Potential investors in Turner Container Company.

(b) The intentional misstatement of the life of an asset or the amount of the

salvage value is unethical for whatever the reason. There is nothing per se

unethical about changing the estimate either of the life of an asset or of

an asset’s salvage value if the change is an attempt to better match cost

(c) Income before income taxes in the year of change is increased $160,000

by implementing the president’s proposed changes.

Old Estimates

Asset cost

Estimated salvage

Depreciable cost

$3,500,000

300,000

3,200,000

BYP 10-8 ALL ABOUT YOU

(a) 1 c 2 b 3 a 4 d

(b) For the most part, the value of a brand is not reported on a company’s

balance sheet. Most companies are required to expense all costs related

to the maintenance of a brand name. Also any research and development

BYP 10-9 FASB CODIFICATION ACTIVITY

(a) Capitalize is used to indicate that the cost would be recorded as the

cost of an asset. That procedure is often referred to as deferring a cost,

and the resulting asset is sometimes described as a deferred cost.

IFRS EXERCISES

IFRS10-1

Component depreciation is a method of allocating the cost of a plant asset

into separate parts based on the estimated useful lives of each component.

IFRS requires an entity to use component depreciation whenever significant

parts of a plant asset have significantly different useful lives.

IFRS10-2

IFRS10-4 INTERNATIONAL FINANCIAL STATEMENT ANALYSIS

(a) Property, plant and equipment is depreciated on a straight-line basis

over its estimated useful life. The depreciation rates range from 2%

(50 yrs.) to 33% (3 yrs.) (Note 1.12).