30 Minutes, Medium

a.

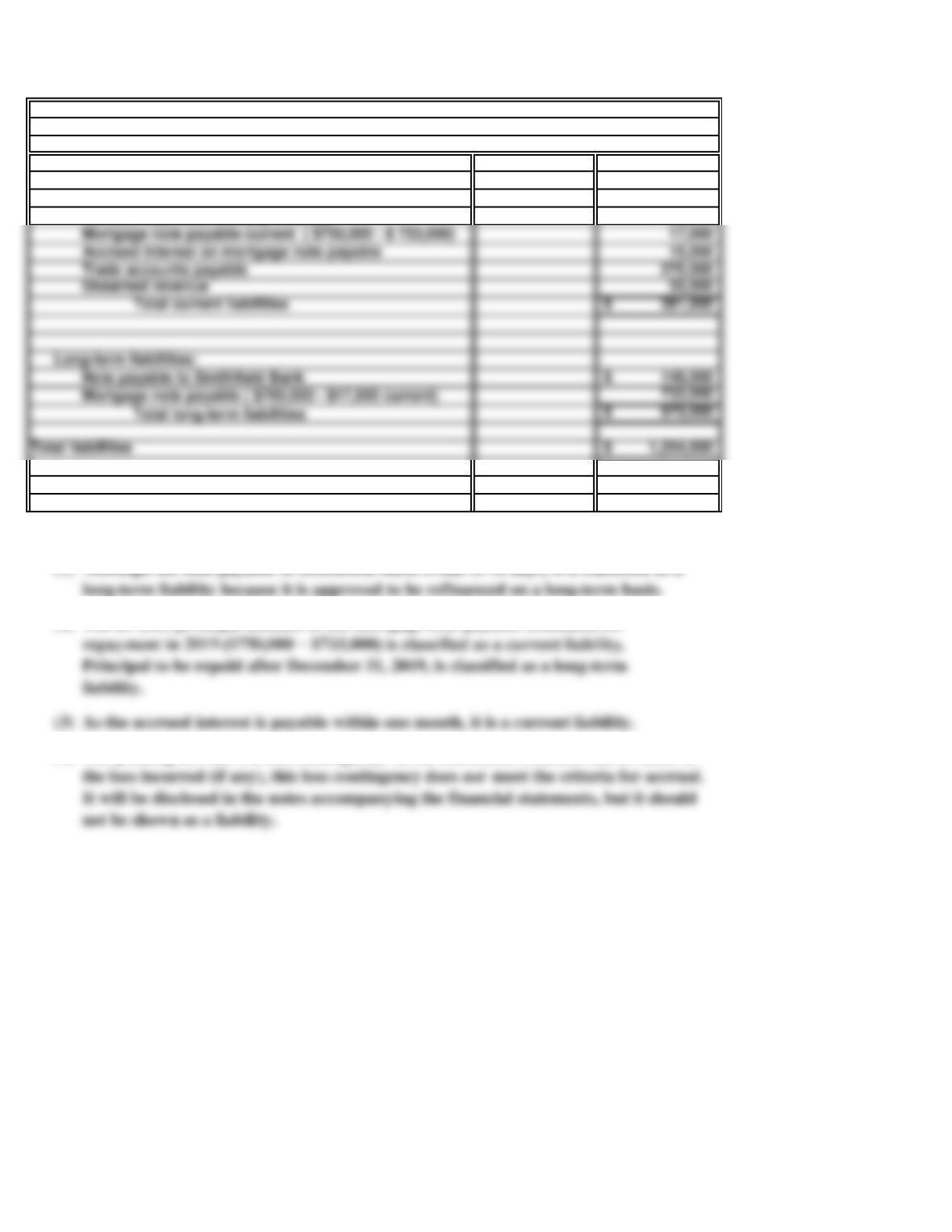

Liabilities:

Income taxes payable 40,000$

60,000

b.

(1

(2

(3

As the accrued interest is payable within one month, it is a current liability.

(4

Current liabilities:

Accrued expenses and payroll taxes

PROBLEM 10.2A

DENVER CHOCOLATES

December 31, 2018

Partial Balance Sheet

DENVER CHOCOLATES

The pending lawsuit is a loss contingency. As no reasonable estimate can be made of the loss

Comments on information in the numbered paragraphs:

Mortgage note payable-current portion ( $750,000 – $739,000) 11,000

Long-term liabilities:

25 Minutes, Medium

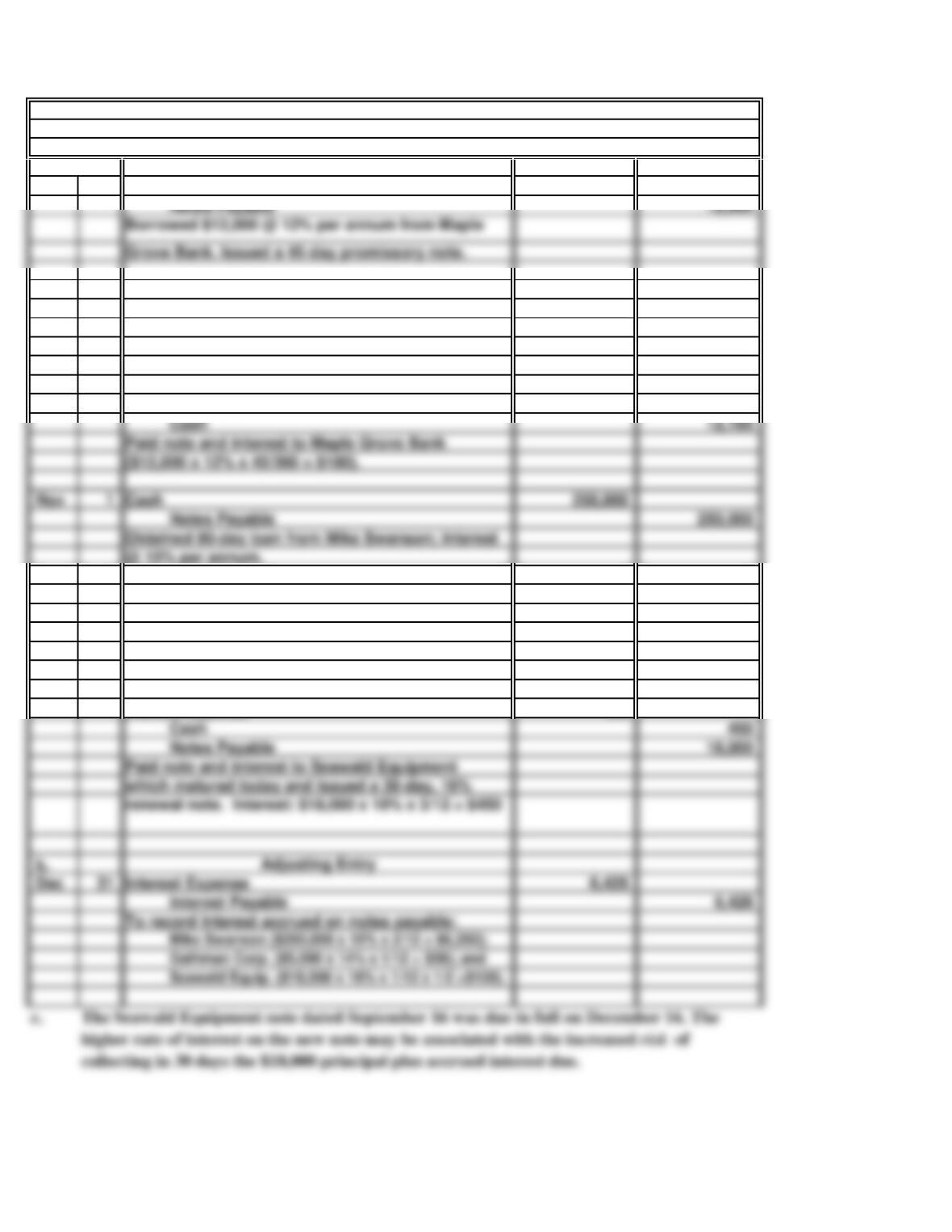

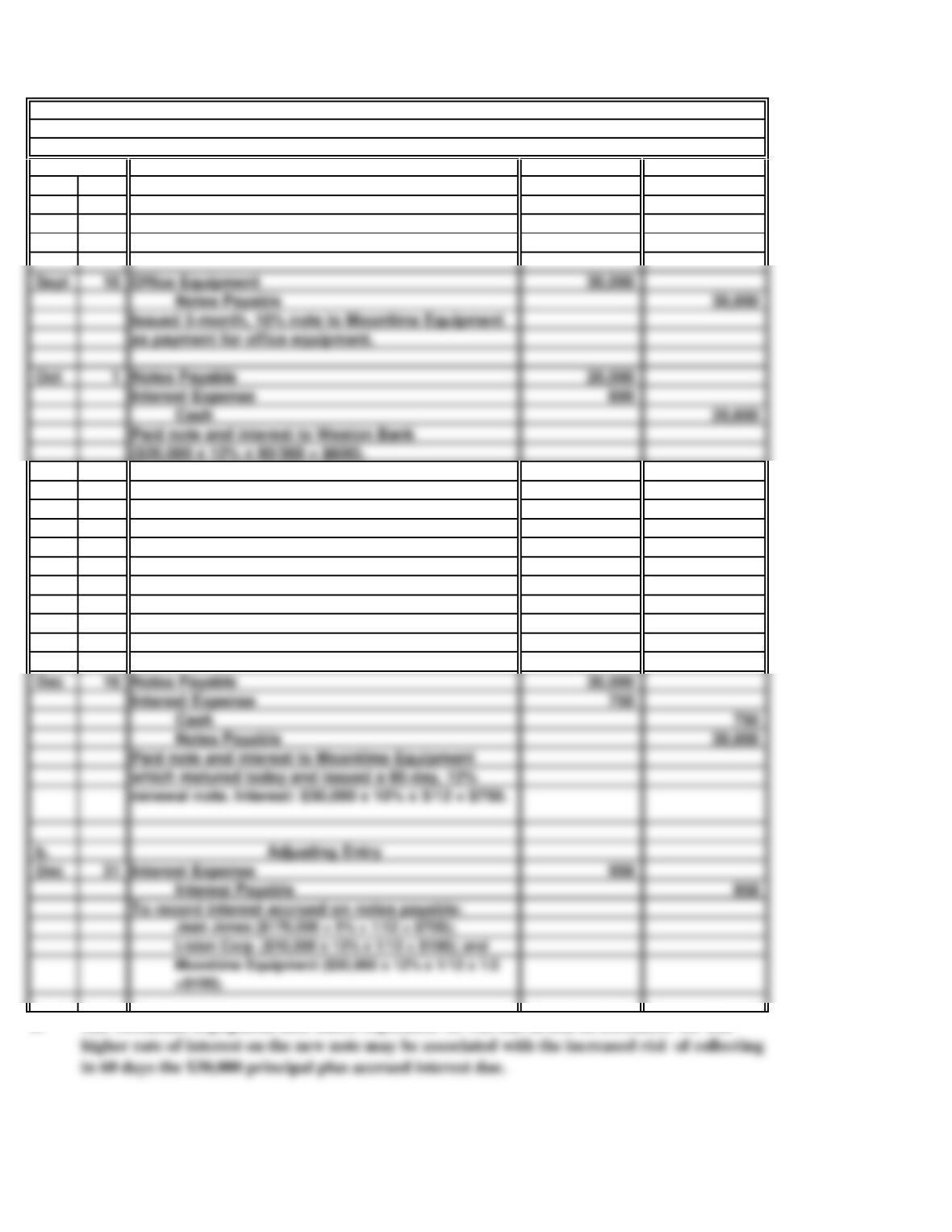

Aug 6 Cash 12,000

Sept 16 18,000

Notes Payable 18,000

Sept 20 12,000

180

Nov 1 Cash 250,000

Notes Payable 250,000

@ 15% per annum.

Paid note and interest to Maple Grove Bank

($12,000 x 12% x 45/360 = $180).

Obtained 90-day loan from Mike Swanson; interest

Dec 1 5,000

5,000

Dec 16 18,000

450

Notes Payable 18,000

Dec 31 6,428

6,428

Paid note and interest to Seawald Equipment

which matured today and issued a 30-day, 16%

Interest Expense

Interest Payable

To record interest accrued on notes payable:

Notes Payable

90-day, 14% note payable to Gathman Corporation.

Notes Payable

Interest Expense

To record purchase of merchandise and issue

Inventory

Notes Payable

Interest Expense

PROBLEM 10.3A

SWANSON CORPORATION

a.

General Journal

20xx

Issued 3-month, 10% note to Seawald Equipment

Office Equipment

as payment for office equipment.

Grove Bank. Issued a 45-day promissory note.

25 Minutes, Medium

PROBLEM 10.4A

SPEEDY LUBE

a.

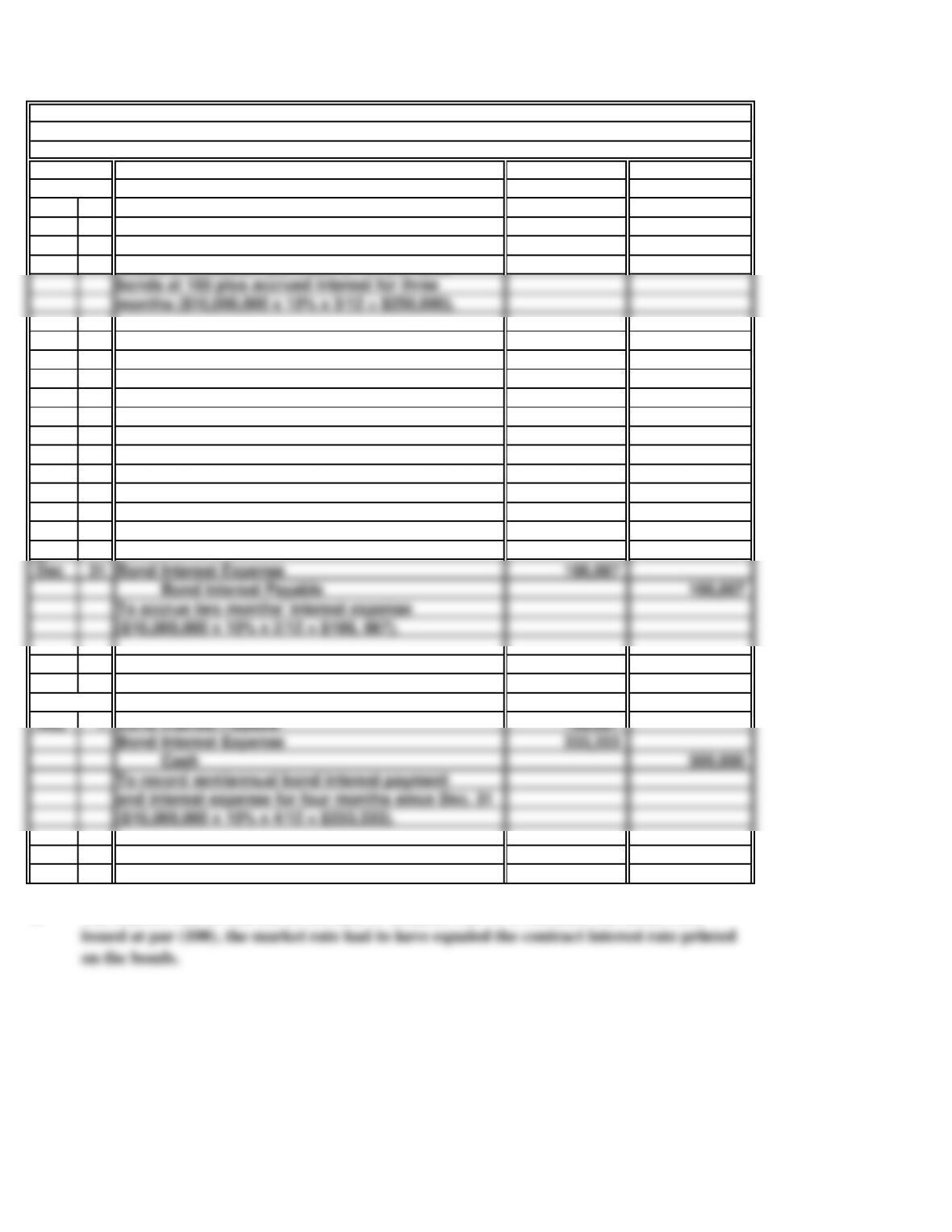

Oct 1 Interest Expense 10,800

310

c.

4

3

2

Reduction in

Monthly Interest Unpaid Unpaid

Payment Expense Balance Balance

1,080,000$

Oct. 1 11,110$ 10,800$ 310$ 1,079,690

d.

Mortgage Note Payable

Amortization Table

1

Issue date

Payable in 360 Monthly Installments of $11,110)

(12%, 30-Year Mortgage Note Payable for $1,080,000;

The amount of the monthly payments exceeds the amount of the monthly interest expense.

At December 31, 2018, two amounts relating to this mortgage loan will appear as

current liabilities in the borrower’s balance sheet. First, as payments are due on the

Sept. 1, 2018

Period

Date

Interest

Payment

b.

General Journal

2018

To record monthly payment on mortgage.

Mortgage Note Payable

To record monthly mortgage payment.

15 Minutes, Easy

Aug 1 Cash 10,250,000

Bonds Payable 10,000,000

Bond Interest Payable 250,000

b.

Nov 1 250,000

250,000

Cash 500,000

c.

Dec 31 166,667

Bond Interest Payable 166,667

Bond Interest Expense

To accrue two months’ interest expense

($10,000,000 x 10% x 2/12 = $166, 667).

d.

May 1 166,667

333,333

Cash 500,000

Bond Interest Payable

To record semiannual bond interest payment

($10,000,000 x 10% x 4/12 = $333,333).

Bond Interest Expense

and interest expense for four months since Dec. 31

e.

a.

Issued $10,000,000 face value of 10%, 20-year

PROBLEM 10.5A

General Journal

2018

GREEN MOUNTAIN POWER COMPANY

Bond Interest Payable

$500,000).

The market rate of interest on the date of issuance was 10%. Because the bonds were

Bond Interest Expense

Paid semiannual interest ($10,000,000 x 10% x 1/2 =

2019

months ($10,000,000 x 10% x 3/12 = $250,000).

bonds at 100 plus accrued interest for three

35 Minutes, Strong

Dec 31 Bond Interest Expense 2,693,334

26,667

Bond Interest

2,666,667

Mar 1 2,666,667

1,346,667

13,334

Cash 4,000,000

(2)

Dec 31 2,653,334

13,333

Bond Interest

2,653,334$

Bond interest expense for four months

Accrual of interest on bonds for four months:

Contract interest ($80,000,000 x 10% x 4/12)

Mar 1 2,666,667

Cash 4,000,000

* Actual amount differs slightly due to rounding errors.

months, as computed in preceding entry).*

Semiannual bond interest payment and interest

Premium on Bonds Payable

expense for two months (1/2 of interest for four

1,326,667

2018

2019

Bond Interest Expense

interest expense for two months (1/2 of interest for

four months, as computed in preceding entry). *

Bond Interest Payable

Premium on Bonds Payable

Bonds issued at 101:

Bonds Interest Expense

To record semiannual bond interest payment and

Discount on Bonds Payable

(1)

Bonds issued at 98:

Bond Interest Expense

2019

2018

Discount on Bonds Payable

Bond Interest Payable

PROBLEM 10.6A

a.

General Journal

EVANSVILLE LUMBER COMPANY

To record accrual of bond interest expense for

Bond interest expense for four months

four months in 2018:

b.

Net bond liability at Dec. 31, 2019: Bonds Bonds

Issued Issued

at 98 at 101

*

Premium amortized at Dec. 31, 2019:

Amount amortized in 2019 ($1,600,000 ÷ 20 years) …………………………………..

Amount amortized in 2019 ($800,000 ÷ 20 years) ……………………………………

c.

PROBLEM 10.6A

EVANSVILLE LUMBER COMPANY (concluded)

The effective rate of interest would be higher under assumption 1. The less that investors

Discount amortized at Dec. 31, 2019:

* Less: Discount on bonds payable ($1,600,000-$106,667) (1,493,333)

Net bond liability at Dec. 31, 2019:

45 Minutes, Strong

a.

Liabilities: (in thousands)

Accounts payable 65,600$

11,347

Accrued interest payable 7,333

100,000$

250,000$

260 249,740

Deferred income taxes

Add: Premium on bonds payable

Capital lease obligation (less current portion)

11% Bonds payable, due June 1, 2028

c. (1) Computation of debt ratio:

Total liabilities (above) 1,088,620$

Total assets (given) 2,093,500$

Debt ratio ($1,088,620 ÷ $2,093,500) 52%

(2) Computation of interest coverage ratio:

Annual interest expense ($61,000 + $17,000) 78,000$

Part b appears on the following page.

6-3/4% Bonds payable, due February 1, 2019

8-1/2% Bonds payable, due June 1, 2019

Less: Discount on bonds payable

Current liabilities:

Accrued expenses payable (other than interest)

Long-term liabilities:

PROBLEM 10.7A

MURFREESBORO TELEPHONE CORPORATION

December 31, 2018

Partial Balance Sheet

CORPORATION (MTC)

MURFREESBORO TELEPHONE

b. (1)

(3)

(4)

(5)

(6)

d.

PROBLEM 10.7A

MURFREESBORO

TELEPHONE CORPORATION

(concluded)

In summary, the fact that MTC is a profitable telephone company with a reasonable debt

As the 6 3/4% bond issue is being refinanced on a long-term basis (that is, paid from the

The portion of the capital lease obligation that will be repaid within one year ($4,621) is

in the periods in which these costs are incurred.

The $18,000 portion of the unfunded liability for postretirement benefits that will be

Income taxes payable relate to the current year’s income tax return and, therefore, are

Based solely upon its debt ratio and interest coverage ratio, Murfreesboro Telephone

Corporation appears to be a good credit risk. One must consider, however, that MTC is a

(2)

The 8 1/2% bonds will be repaid from a bond sinking fund rather than from current

20 Minutes, Strong

a.

Liabilities:

Unearned revenues 300,000$

100,000

900,000$

Deferred income taxes**

Notes payable*

b.

●

●

●

The following items listed by the company have been excluded from current and long-term

liabilities for the reasons indicated:

Interest expense that will arise in the future from existing obligations is not yet a liability.

PROBLEM 10.8A

PETERSEN CORPORATION

Bonds payable

Current liabilities:

Income taxes payable

Long-term liabilities:

Notes payable (current portion) 12,000

25 Minutes, Easy

Current Long-Term Owners’

Transaction Revenue – Expenses = Net Income Assets = Liabilities + Liabilities + Equity

a. NE I D NE INE D

b. NE NE NE NE I D NE

c. NE I D D I NE D

SOLUTIONS TO PROBLEMS SET B

PROBLEM 10.1B

PHILMAR, INC.

Income Statement

Balance Sheet

30 Minutes, Medium

a.

Liabilities:

Income taxes payable 15,000$

26,000

b.

(1)

(2)

(3)

As the accrued interest is payable within one month, it is a current liability.

(4)

The pending lawsuit is a loss contingency. As no reasonable estimate can be made of

Comments on information in the numbered paragraphs:

The $17,000 principal amount of the mortgage note payable scheduled for

Current liabilities:

Accrued expenses and payroll taxes

PROBLEM 10.2B

GEORGIA PEACH

December 31, 2018

Partial Balance Sheet

GEORGIA PEACH

Mortgage note payable-current ( $750,000 – $ 733,000) 17,000

Long-term liabilities:

25 Minutes, Medium

Jul 1 Cash 20,000

Notes Payable 20,000

Dec 1 Cash 170,000

Notes Payable 170,000

Dec 1 10,000

10,000

Dec 16 30,000

Notes Payable 30,000

b.

Dec 31 958

which matured today and issued a 60-day, 12%

Interest Payable

To record interest accrued on notes payable:

Notes Payable

Interest Expense

Interest Expense

Paid note and interest to Moontime Equipment

c.

Inventory

Notes Payable

The Moontime Equipment note dated September 16 was due in full on December 16. The

PROBLEM 10.3B

SWANLEE CORPORATION

a.

General Journal

20xx

Bank. Issued a 90-day promissory note.

@ 5% per annum.

Borrowed $20,000 @ 12% per annum from Weston

To record purchase of merchandise and issue

90-day, 12% note payable to Listen Corporation.

Obtained 120-day loan from Jean Jones; interest

Sept 16 30,000

Notes Payable 30,000

Oct 1 20,000

Issued 3-month, 10% note to Moontime Equipment

as payment for office equipment.

Office Equipment

Notes Payable

Interest Expense

Paid note and interest to Weston Bank

($20,000 x 12% x 90/360 = $600).

25 Minutes, Medium

JENCO

a.

Nov 1 Interest Expense 1,000

1,633

c.

Reduction in

Monthly Interest Unpaid Unpaid

Payment Expense Balance Balance

100,000$

Nov. 1 2,633$ 1,000$ 1,633$ 98,367

Dec. 1 2,633 984 1,649 96,718

Jan. 1, 2019 2,633 967 1,666 95,052

Feb. 1 2,633 951 1,682 93,370

2

3

4

d.

The amount of the monthly payments exceeds the amount of the monthly interest

expense. Therefore, a portion of each payment reduces the unpaid balance of the loan.

At December 31, 2018, two amounts relating to this mortgage loan will appear as

1

Period

Date

Issue date

Oct. 1, 2018

(12%, 4-Year Mortgage Note Payable for $100,000;

Payable in 48 Monthly Installments of $2,633)

Interest

Payment

Amortization Table

PROBLEM 10.4B

b.

General Journal

2018

Note Payable

Note Payable

To record monthly payment on note payable to

Vicksburg State Bank.

To record monthly payment on note payable to