Chapter 10 – Standard Costing and Analysis of Direct Costs

10-1

CHAPTER 10

Standard Costing and Analysis of Direct Costs

ANSWERS TO REVIEW QUESTIONS

10-1 Any control system has three basic parts: a predetermined or standard performance

level, a measure of actual performance, and a comparison between standard and

10-3 One method of setting standards is the analysis of historical data. Historical cost

data provide an indicator of future costs. The methods for analyzing cost behavior

10-4 A perfection (or ideal) standard is the cost expected under perfect or ideal operating

conditions. A practical (or attainable) standard is the cost expected under normal

10-6 The standard quantity of material is the amount required to be included in the

10-7 An unfavorable direct-material price variance means that a higher price was paid for

Chapter 10 – Standard Costing and Analysis of Direct Costs

10-2

10-9 An unfavorable direct-material quantity variance means that a larger amount of

10–11 The direct-material purchase price variance is based on the quantity purchased (PQ).

Deviations between the actual and standard price, which are highlighted by the

10–12 An unfavorable direct-labor rate variance means that a higher labor rate was paid

than was anticipated when the standard was set. One possible cause is that labor

10–13 In some cases, the manager in the best position to influence the direct-labor rate

10–14 The interpretation of an unfavorable direct-labor efficiency variance is that more

Chapter 10 – Standard Costing and Analysis of Direct Costs

10-3

10–16 The issue of quantity purchased versus quantity used does not arise in the context

10–17 Several factors that managers often consider when determining the significance of a

10–18 Several ways in which standard-costing should be adapted in today’s manufacturing

environment are as follows:

(a) Reduced importance of labor standards and variances: As direct labor occupies

10-4

10–19 Under a standard-costing system, standard costs are used for product-costing

purposes as well as for control purposes. The costs entered into Work-in-Process

10–20 Advantages of a standard-costing system include the following:

(a) Standard costs provide a basis for sensible cost comparisons. Standard costs

enable the managerial accountant to compute the standard allowed cost, given

10-5

10-21 Seven criticisms of standard costing in an advanced manufacturing setting are the

following:

(a) Variances are too aggregate and too late to be useful.

Chapter 10 – Standard Costing and Analysis of Direct Costs

10-6

SOLUTIONS TO EXERCISES

EXERCISE 10-22 (15 MINUTES)

Direct-material price variance

=

AQ(AP – SP)

=

SP(AQ – SQ)

Direct-material purchase price variance

=

PQ(AP – SP)

†SQ = 4,000 pounds = 2,000 units 2 pounds per unit

Direct-labor rate variance

=

AH(AR – SR)

=

$1,935 Unfavorable

=

SR(AH – SH)

=

$8,100 Unfavorable

Chapter 10 – Standard Costing and Analysis of Direct Costs

10-7

EXERCISE 10-23 (30 MINUTES)

DIRECT-MATERIAL PRICE AND QUANTITY VARIANCES

ACTUAL MATERIAL COST

PROJ. MATERIAL COST

STANDARD MATERIAL COST

Actual

Quantity

Actual

Price

Actual

Quantity

Standard

Price

Standard

Quantity

Standard

Price

4,300

$7.40

4,300

$7.20

4,000

$7.20

10-8

EXERCISE 10-23 (CONTINUED)

DIRECT-MATERIAL PURCHASE PRICE VARIANCES

ACTUAL MATERIAL COST

OF PURCHASES

PROJ. MATERIAL COST

OF PURCHASES

Actual

Quantity

Actual

Price

Actual

Quantity

Standard

Price

6,500

$7.40

6,500

$7.20

DIRECT-LABOR RATE AND EFFICIENCY VARIANCES

ACTUAL LABOR COST

PROJ. LABOR COST

STANDARD LABOR COST

Actual

Hours

Actual

Rate

Actual

Hours

Standard

Rate

Standard

Hours

Standard

Rate

6,450

6,450

$18.00

Chapter 10 – Standard Costing and Analysis of Direct Costs

10-9

EXERCISE 10-24 (10 MINUTES)

Standard quantity:

Hardwood in finished product ………………………………………

7

board feet

Allowance for normal scrap …………………………………………

1.5

board feet

Total standard quantity required per box ………………………

8.5

board feet

Standard price:

Purchase price per board foot of hardwood ………………….

Transportation cost per board foot ………………………………

Total standard price per board foot ………………………………

Standard direct-material cost of a jewelry box:

Standard quantity ………………………………………………………..

8.5

board feet

Standard direct-material cost ……………………………………….

10–10

EXERCISE 10-25 (15 MINUTES)

1. Calculation of variances:

Direct-material price variance

=

AQ(AP – SP)

=

210,000($.62 – $.60)

=

SP(AQ – SQ)

=

$.60(210,000 – 200,000*)

=

$6,000 Unfavorable

=

PQ(AP – SP)

=

240,000($.62 – $.60)

=

AH(AR – SR)

=

13,000($12.20* – $12.00)

=

$2,600 Unfavorable

Direct-labor efficiency variance

=

SR(AH – SH)

=

$12.00(13,000 – 12,500*)

=

$6,000 Unfavorable

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–11

EXERCISE 10-26 (30 MINUTES)

DIRECT-MATERIAL PRICE AND QUANTITY VARIANCES

ACTUAL MATERIAL COST

PROJ. MATERIAL COST

STANDARD MATERIAL COST

Actual

Quantity

Actual

Price

Actual

Quantity

Standard

Price

Standard

Quantity

Standard

Price

210,000

$.62

210,000

$.60

200,000

$.60

DIRECT-MATERIAL PURCHASE PRICE VARIANCE

ACTUAL MATERIAL COST

PROJ. MATERIAL COST

Actual

Quantity

Actual

Price

Actual

Quantity

Standard

Price

240,000

$.62

240,000

$.60

10–12

EXERCISE 10-26 (CONTINUED)

DIRECT-LABOR RATE AND EFFICIENCY VARIANCES

ACTUAL LABOR COST

STANDARD LABOR COST

Actual

Hours

Actual

Rate

Actual

Hours

Standard

Rate

Standard

Hours

Standard

Rate

13,000

$12.20

13,000

$12.00

12,500

$12.00

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–13

EXERCISE 10-27 (30 MINUTES)

Answers will vary widely, depending on the company and the product. Typically, new

EXERCISE 10-28 (5 MINUTES)

Good output

=

(3/4) input = .75 input

10–14

EXERCISE 10-29 (30 MINUTES)

Direct

Material

Direct

Labor

Standard price or rate per unit of input ……………………….

$16 per lb

$20 per hre

Standard quantity per unit of output …………………………..

2.75 lbs per unitc

4 hrs per unitg

Actual quantity used per unit of output ………………………

Actual price or rate per unit of input …………………………..

$14 per lb

Actual output …………………………………………………………….

Standard input quantity allowed …………………………………

Direct-material purchase price variance ……………………..

$120,000 F

Direct-material quantity variance ……………………………….

$80,000 Ub

Direct-labor rate variance …………………………………………..

$ 70,000 Ud

Direct-labor efficiency variance ………………………………….

$200,000 F

Total direct-labor variance …………………………………………

$130,000 F

Explanatory notes:

a.

Direct-mat’l purchase price variance

=

PQ(AP – SP)

$120,000 F

=

PQ($14 – $16)

=

60,000 lbs

=

b.

Direct-material quantity variance

=

SP(AQ – SQ)

=

$16/lb x (60,000 lbs – 55,000 lbs)

=

$80,000 U

d.

=

rate variance + efficiency variance

$130,000 F

=

rate variance + $200,000 F

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–15

EXERCISE 10-29 (CONTINUED)

e.

AH = 20,000 units 3.5 hrs per unit

=

70,000 hrs

=

f.

Direct-labor efficiency variance

=

SR(AH – SH)

=

80,000 hrs

=

4 hrs per unit

10–16

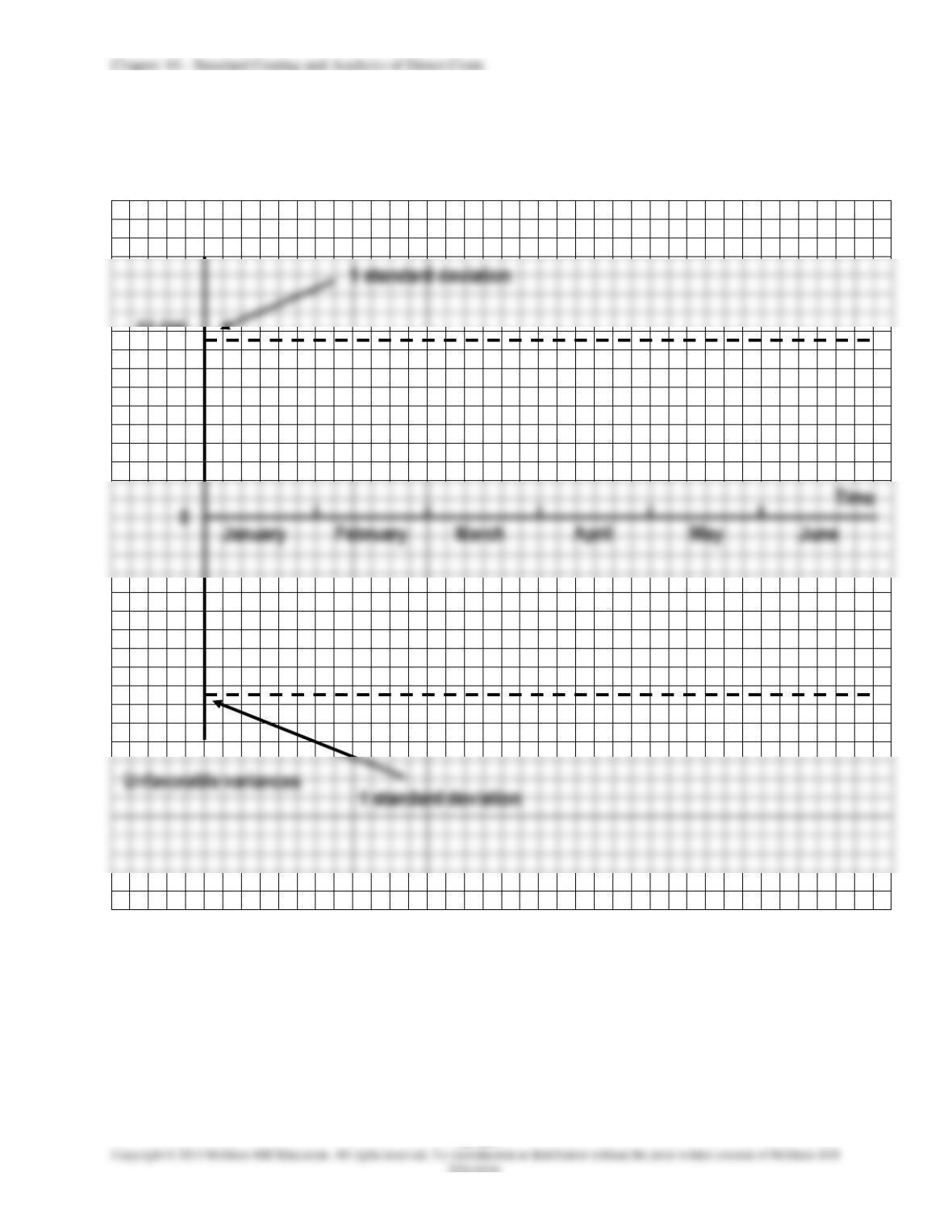

EXERCISE 10-30 (25 MINUTES)

1. Statistical control chart with variance data plotted:

Only the variances in May and June would be investigated, since they are the only ones

that exceed 1 standard deviation, $1,900.

Favorable variances

1 standard deviation

Time

$2,000

$1,000

$1,000

$2,000

•

•

•

•

•

•

10–17

EXERCISE 10-30 (CONTINUED)

2.

Rule of thumb:

Standard cost …………………………………………………………………………………..

$38,000

3.

would be cause for concern.

This is a judgment call, and there is no right or wrong answer. It would be reasonable

EXERCISE 10-31 (15 MINUTES)

1. Raw-Material Inventory ………………………………………..

144,000

Direct-Material Purchase Price Variance ………………

Accounts Payable ………………………………………..

148,800

2. Work-in-Process Inventory …………………………………..

120,000

Direct-Material Quantity Variance ………………………..

Raw-Material Inventory ………………………………..

126,000

3. Work-in-Process Inventory …………………………………..

150,000

Direct-Labor Rate Variance …………………………………

Direct-Labor Efficiency Variance …………………………

Wages Payable …………………………………………..

158,600

4. Cost of Goods Sold …………………………………………….

19,400

Direct-Material Purchase Price Variance ………

4,800

Direct-Material Quantity Variance ………………..

6,000

Direct-Labor Rate Variance ………………………….

2,600

Direct-Labor Efficiency Variance …………………

6,000

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–18

EXERCISE 10-32 (15 MINUTES)

Raw-Material Inventory

Direct-Material

Purchase Price Variance

126,000

4,800

Work-in-Process Inventory

Direct-Material

Quantity Variance

6,000

Accounts Payable

Direct-Labor

Rate Variance

148,800

2,600

Wages Payable

Direct-Labor

Efficiency Variance

158,600

6,000

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–19

SOLUTIONS TO PROBLEMS

PROBLEM 10-33 (25 MINUTES)

1.

Direct-material price variance

=

(AQ

AP) – (AQ

SP)

=

=

=

2.

Direct-material quantity variance

=

(AQ

SP) – (SQ

SP)

=

$25,650 – $27,000

=

$1,350 Favorable

3.

Direct-material purchase

price variance

=

(PQ

AP) – (PQ

SP)

=

=

$49,680 – $48,600

=

$1,080 Unfavorable

4.

Direct-labor rate variance

=

(AH

AR) – (AH

SR)

=

=

$38,430 – $37,800

=

$630 Unfavorable

5.

Direct-labor efficiency variance

=

(AH

SR) – (SH

SR)

=

=

$37,800 – $36,000

=

$1,800 Unfavorable

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–20

PROBLEM 10-34 (25 MINUTES)

1.

Direct-material price variance

=

(AQ

AP) – (AQ

SP)

=

=

$42,750 Unfavorable

2.

Direct-material quantity variance

=

(AQ x SP) – (SQ x SP)

=

$33,250 Favorable

3.

Direct-material purchase price

variance

=

(PQ

AP) – (PQ

SP)

=

=

$608,000 – $560,000

4.

Direct-labor rate variance

=

(AH

AR) – (AH

SR)

=

$4,400 Favorable

5.

Direct-labor efficiency variance

=

SR(AH – SH)

=

$4,000 Unfavorable