314

P10–2

1. Schedule of manufacturing costs incurred during April:

Direct Direct Factory

Job Materials Labor Overhead Total

No. 401 $5,500 $ 6,650 $ 1,520 $13,670

No. 402 4,000 4,775 1,200 9,975

2. Schedule of jobs finished during April:

Direct Direct Factory

Job Materials Labor Overhead Total

No. 401 $ 5,500 $ 6,650 $1,520 $13,670

3. Schedule of jobs sold in April:

Job

No. 401 ……………………………………. $13,670

This schedule supports the cost of goods sold account for April.

315

P10–2, Concluded

4. Schedule of completed jobs on hand, April 30, 20Y4:

Direct Direct Factory

Job Materials Labor Overhead Total

Finished Goods, April 30

(Job 405) …………………….. $3,200 $4,000 $960 $8,160

5. Schedule of unfinished jobs:

Direct Direct Factory

Job Materials Labor Overhead Total

No. 404 …………………………… $ 7,100 $ 8,500 $2,240 $17,840

No. 406 …………………………… 1,850 2,200 560 4,610

6. Sales …………………………….. $47,750*

Cost of goods sold ………… (28,640)

Gross profit …………………… $19,110

316

P10–3

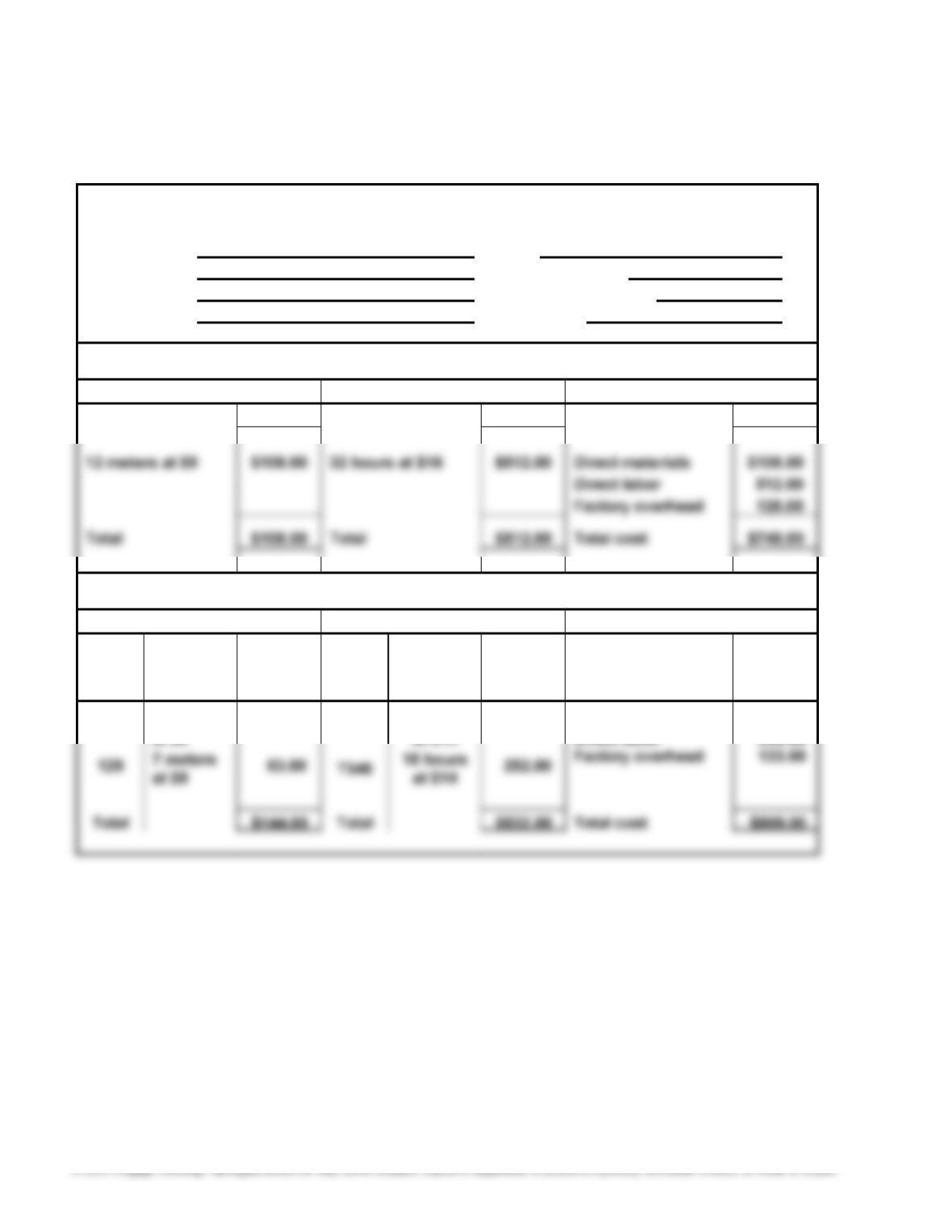

1. and 2.

JOB COST SHEET

Customer Millard Schmidt Date February 14, 20Y1

Address 315 White Oak Drive Date wanted March 15, 20Y1

Columbus, GA Date completed March 9, 20Y1

Item Reupholster couch and chair Job. No. 02-019

ESTIMATE

Direct Materials Direct Labor Summary

Amount Amount Amount

ACTUAL

Direct Materials Direct Labor Summary

Mat.

Req.

No.

Descrip-

tion

Amount

Time

Ticket

No.

Descrip-

tion

Amount

Item

Amount

122 9 meters

$ 81.00

T344 20 hours

$280.00 Direct materials

$144.00

317

1. Supporting calculations:

Job No.

Quan-

tity

May 1

Work in

Process

Direct

Materials

Direct

Labo

r

Factory

Overhead

Total

Cost

Unit

Cost

Units

Sold

Cost of

Goods

Sold

No. 0521 100 $1,500 $ 5,000 $ 15,000 $ 18,000 $ 39,500 $395.00 80 $ 31,600

No. 0522 200 4,000 8,500 26,000 31,200 69,700 $348.50 160 55,760

No. 0523 100 3,500 8,000 9,600 21,100 0 0

(A) $34,600. Materials applied to production in May plus indirect materials.

($32,100 + $2,500)

(B) $5,500. From table above and problem.

(C) $32,100. From table above.

(D) $96,000. From table above.

2. May 31 balances:

Materials $14,400 ($9,000 + $40,000 – $34,600)

Work in Process $33,000* [$21,100 (Job 0523) + $11,900 (Job 0526)]

Finished Goods $39,190** ($215,800 – $176,610)

Factory Overhead $1,200 underapplied [$(3,000) + $14,000 + $2,500

+ $102,900 – $115,200]

* or ($5,500 + $32,100 + $96,000 + $115,200 – $215,800)

** Units in Unit Total

Job No. Inventory Cost Cost

318

P10–5

1.

R-TUNES INC.

CYCLONE PANIC CD

Income Statement

For the Year Ended December 31, 20Y8

Sales …………………………………………………. $3,800,000

Cost of goods sold …………………………….. (807,500)

Gross profit ……………………………………….. $2,992,500

Selling expenses:

Promotional materials ……………………. $1,500,000

Supporting calculations:

Sales: 475,000 units × $8 = $3,800,000

Cost of goods sold: 475,000 units × $1.70 = $807,500

Manufacturing cost per unit (CD):

Direct materials:

Blank CD …………………………………………………. $ 0.40

Case ……………………………………………………….. 0.25

Song lyric insert ………………………………………. 0.18

Total direct materials ……………………………….. $ 0.83

2. Finished Goods balance, December 31, 20Y8:

(500,000 units – 475,000 units) × $1.70 = $42,500

Work in Process, December 31, 20Y8:

319

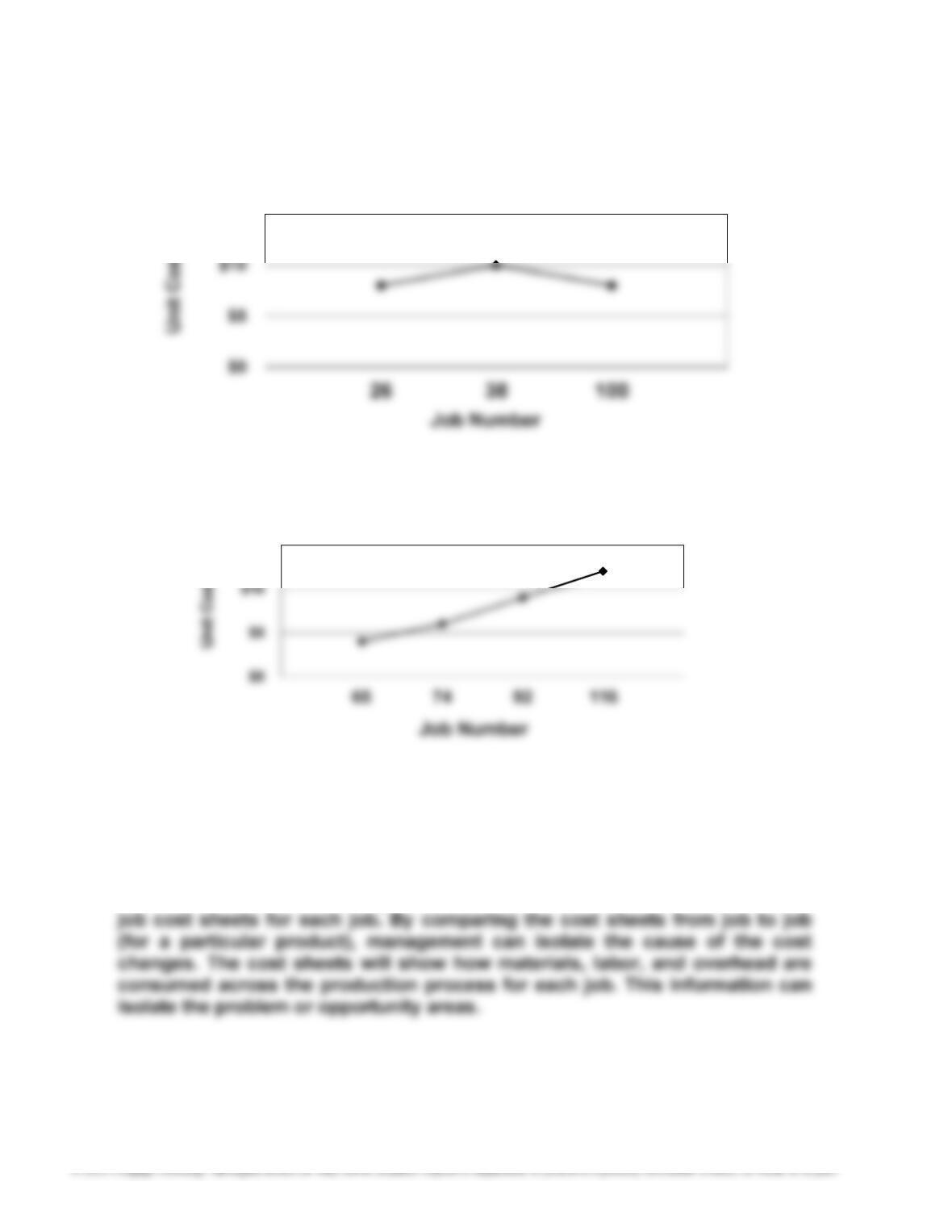

METRIC-BASED ANALYSIS

MBA 10–1

a.

Unit

Date Job No. Quantity Product Amount Cost

Jan. 13 1 180 Mercury $ 4,500 $25

Jan. 29 26 1,020 Venus 8,160 8

Feb. 3 38 1,330 Venus 13,300 10

Mar. 14 49 550 Mercury 12,100 22

Mercury Unit Costs

$20

$25

$30

320

MBA 10–1, Concluded

Venus Unit Costs

Pluto Unit Costs

As can be seen, the unit costs behave differently for each product. Pluto has

increasing unit costs during the year, Venus has fairly steady unit costs during

the year, and Mercury has decreasing unit costs during the year.

b. Management should determine why Pluto costs are increasing and why

Mercury costs are decreasing. This information can be determined from the

$15

$15

321

MBA 10–2

a. The first item to note is that the cost did not go up due to any increases in the

cost of labor or materials. Rather, the cost of the plaques increased because

Job 08-11 used more labor and materials per unit than did Job 05-1. Specifi-

b. An analysis of actual and expected labor hours for Job 05-1 and Job 08-11 is

as follows:

Job 05-1

Engraving:

Actual hours 40.0 hours

Job 08-11

Engraving:

Actual hours 50.0 hours

Expected hours (80 units × 30 min. per unit) ÷ 60 min. = 40.0 hours

Hours over expected 10.0 hours

322

MBA 10–3

The direct materials cost exceeded the estimate by $36 because 4 meters of

materials were spoiled. The direct labor cost exceeded the estimate by $20

even though the laborer was paid $2 less than expected per hour because an

MBA 10–4

Two or three trends seem apparent.

a. There appears to be a strong “Friday effect.” The unit cost on Friday increases

dramatically, then falls on Monday. Apparently, employees are not working as

efficiently because it is the end of the week.

A number of further pieces of information should be requested.

a. It would be good to verify these trends with some other products. This trend

is probably not product-related but related generally to the day of the week.

This would mean the trend should be apparent in the other products.

323

MBA 10–4, Concluded

c. The Friday–Monday phenomenon is likely related to the workforce, but the

same cannot be said about the larger increasing trend over the four weeks. It

could be caused by any number of factors. A good first look would be to iso-

late materials costs to see if these are contributors. How much of the effect is

324

CASES

Case 10–1

Although Beth may appear to have technically complied with company policy, her

computation of the cost of the lumber is unethical. The Statement of Ethical Con-

duct for Practitioners of Management Accounting and Financial Management

requires that Beth avoid all actual or apparent conflict-of-interest situations.

Case 10–2

The objectives of managerial accounting and financial accounting are different;

therefore, the vice president’s statement is incomplete. In one sense, the state-

ment may be true at only high levels in the organization. For example, the division

manager may be evaluated on the basis of financial accounting profit. Thus, the

divisional manager would be evaluated by central management in nearly the

same way that central management is evaluated by shareholders.

325

Case 10–3

1. Ashley’s bill has a number of points that should be considered. Some of the

points, with the appropriate argument, are identified below.

a. The trip back to the shop resulted in a $95 labor charge. Ashley should

argue that the whole hour should not be billed. The hour is the result of

stocking out of a circuit board on the truck. The circuit board should

have been with the repair person. There was a board for the previous

customer. However, since only one was stocked, the repair person had

to go back to the shop. The trip back to the shop was nonproductive time

that should not have been directly charged to Ashley but should be part

of Reboot’s overhead cost to all customers. In other words, Ashley

should not be responsible for this mistake.

Thus, the labor portion of the bill should only be $65 + $40 + $40 = $145.

There are other parts of the bill that should not be in dispute.

The materials storage and handling charge is a normal charge of maintain-

326

Case 10–3, Concluded

2.

Cost Direct Materials Direct Labor Overhead

Circuit board X

Storage and handling X

Straight-time labor X

Fringe benefits* X

Case 10–4

1. The engineer is concerned that direct labor is not related to overhead con-

sumption because direct labor is a small part of the cost structure. Apparent-

ly, the company has replaced labor with expensive machine technology and

2. Since each direct labor hour now has $3,000 of factory overhead attached to

it, small mistakes in the direct labor time estimates can have a large impact

on the estimated cost of a product. If the company underestimates the direct

3. The engineer’s concern is valid. The company should consider replacing its

direct labor time activity base with one that more accurately reflects its present

resources. If the company is now highly automated, then machine hours may

be a much more reasonable activity base for applying overhead to jobs.

327

Case 10–5

Note to Instructors: Consider having the teams compete for the most examples.

Have half the class do the take-out pizza restaurant and the other the copy shop,

and compare results.

Some examples that may be offered by the students are the following:

Copy and Graphics Shop

Direct Direct Selling

Cost Materials Labor Overhead Expense

Paper ………………………………………. X

Graphic designer wages ………….. X

Manager salary ………………………… X

Lease cost of copy machine …….. X

Coupon costs ………………………….. X

Advertising ……………………………… X

Packaging (bags and boxes)…….. X

328

Case 10–5, Concluded

Take-Out Pizza Restaurant

Direct Direct Selling

Cost Materials Labor Overhead Expense

Ingredients …………………………… X

Cook wages ………………………….. X

Manager salary …………………….. X

Depreciation on equipment

and fixtures ……………………… X

Repair costs ………………………… X

Property taxes ………………………. X

Store depreciation ………………… X

Cashier salary ………………………. X

Beverage ……………………………… X

Building heat and A/C …………… X

Salad ingredients ………………….. X

329

Case 10–6

Tyra Chastain’s claim that the inventory doesn’t cost the company anything is

likely not true. At the very minimum, inventory requires working capital to be

used. The financing cost associated with the working capital represents a cost to

Gwen Willis should suggest that Tyra Chastain use just-in-time manufacturing

principles. The production process could be scheduled using pull techniques.

This would mean the plant produces products only when there are orders.

Products would not be manufactured for inventory. In addition, the plant manager

should work to develop a reliable supply chain. One of the objectives of the supply

chain management would be to improve supplier shipment reliability, so that