CHAPTER 10

UNDERSTANDING THE ISSUES

1. If the U.S. dollar strengthens relative to a

FC, this means that the dollar commands

more FC. The direct exchange rate will

change in that 1 FC will be worth fewer

2. If the U.S. dollar is weakening against the

FC, then more dollars will be required to

settle FC purchases and exchange losses

will be experienced. These losses could be

hedged against through the use of a for-

ward contract to buy FC. Given a fixed for-

ward rate, the holder of the contract will

know exactly how many dollars it will take

to secure the necessary FC. As the value

of the payable to the foreign vendor in-

creases with resulting losses, the value of

3. A commitment to purchase inventory paya-

ble in FC is characterized by a fixed num-

ber of FC. However, the exchange rate for

the FC is subject to change; therefore, the

future transaction date. The losses on the

commitment could be offset by gains on the

hedging instruments. Furthermore, the firm

commitment account would then be used to

adjust the basis of the acquired inventory at

the date of the actual purchase transaction.

The basis adjustment would reduce the

cost of the inventory and allow for other-

wise increased profit margins.

4. The time value of an option is measured as

Ch. 10—Exercises 10–2

EXERCISES

EXERCISE 10-1

Balance sheet accounts—Debit (Credit): June 30 July 31

Inventory:

Down payment (50,000 euros × $1.350) ……………… $ 67,500 $ 67,500

EXERCISE 10-2

(1) January 1 $0.125 = FC 1

Rate Spot Direct FC 8 = $1

Rate Spot Indirect

(2) U.S. Dollars Foreign Currency (FC)

Value today (assumed amount) …………. $100 800 FC

Interest rate ……………………………………. 4% 5%

10–3 Ch. 10—Exercises

Exercise 10-2, Concluded

(3) This suggests that the domestic (U.S.) interest rates are higher than those of the foreign

country. Assume that one wants to buy foreign currency in the future; therefore, they retain

(4) When the U.S. dollar is weak relative to a FC, it takes more U.S. dollars to equal the FC.

(5) If the dollar strengthened relative to the FC, the amount of FC would increase, and the for-

ward rate would decrease.

EXERCISE 10-3

(1) The intrinsic value of the option is represented by the difference between the strike price

and the spot rate times the notional amount. The time value is equal to the value of the op-

tion less the intrinsic value. For the subject option, these values are as follows:

February 1 April 30 May 31

Strike price …………………………………. $ 2.05 $ 2.05 $ 2.05

Spot rate …………………………………….. $ 2.05 $ 2.08 $ 2.10

Notational amount ……………………….. 100,000 100,000 100,000

Exercise 10-3, Concluded

(2) Changes in the value of the forward contract are measured as the difference between the

value at the original forward rate versus the current forward rate. This difference in value is

then discounted back from the expiration date to the current date. For the subject forward

contract, the values are as follows:

February 1 April 30 May 31

Original forward value ………………………. $207,000 $207,000

Current forward value ………………………. $209,000 $210,000

(3) Given the hedge of an unrecognized commitment, changes in the value of the hedging

instrument would also be recognized as changes in the value of the commitment. When the

EXERCISE 10-4

(1) Apr. 15 No entry

May 1 Inventory ……………………………………………………………………. 343,500

$0.693.

June 30 Exchange Loss …………………………………………………………… 2,000

($0.687 – $0.691)]

Forward Contract ………………………………………………………… 995

Gain on Forward Contract ………………………………………… 995

To record change in value of forward contract

when forward rate is 1 FC = $0.695. Change in

Aug. 1 Forward Contract ………………………………………………………… 505

Gain on Forward Contract ………………………………………… 505

To record change in value of forward contract

when 1 FC = $0.696. Total change in forward

Foreign Currency ………………………………………………………… 348,000

Cash ……………………………………………………………………… 346,500

Exercise 10-4, Concluded

(2) Stark, Inc.

Partial Income Statement

For the Year Ended June 30

Exchange gain (loss) …………………………………………………………………………….. $(2,000)

Stark, Inc.

Partial Balance Sheet

As of June 30

Inventory …………………………. $343,500 Accounts payable …………….. $345,500

EXERCISE 10-5

(1) Gain (loss) on commitment through September 15: FCA FCB

Number of FC in commitment:

$549,600 ÷ $1.200 ………………………………… 458,000

Change in spot rate from commitment date to

transaction date:

$1.200 vs. $1.160 ………………………………….. $ 0.04

$0.685 vs. $0.692 ………………………………….. $ 0.007

Gain (loss) on commitment:

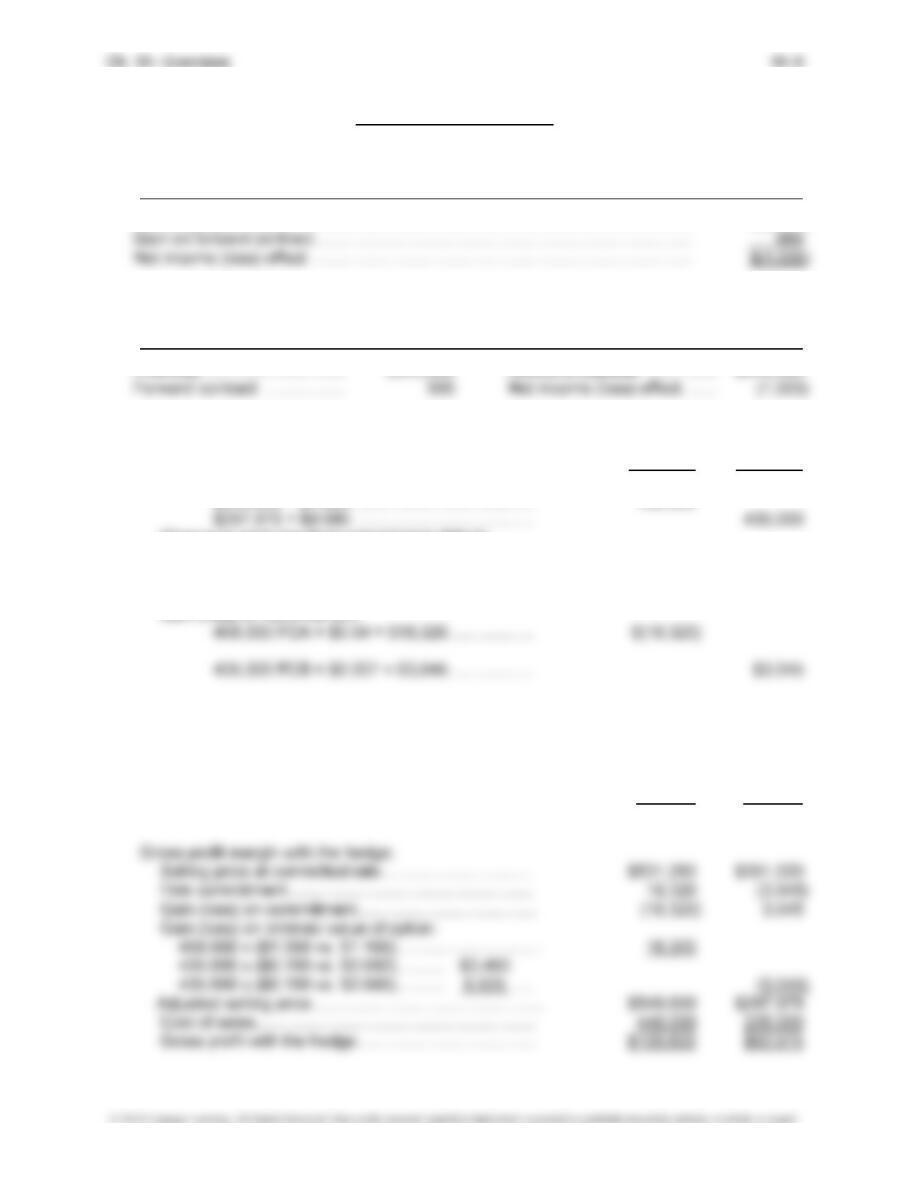

(2) Gross profit margin without the hedge:

Selling price at spot rate on date of sale:

458,000 x $1.16…………………………………………….. $531,280

435,000 x $0.692…………………………………………… $301,020

Cost of sales………………………………………………….… 440,000 235,000

Gross profit without the hedge…………………………….. $91,280 $66,020

10–7 Ch. 10—Exercises

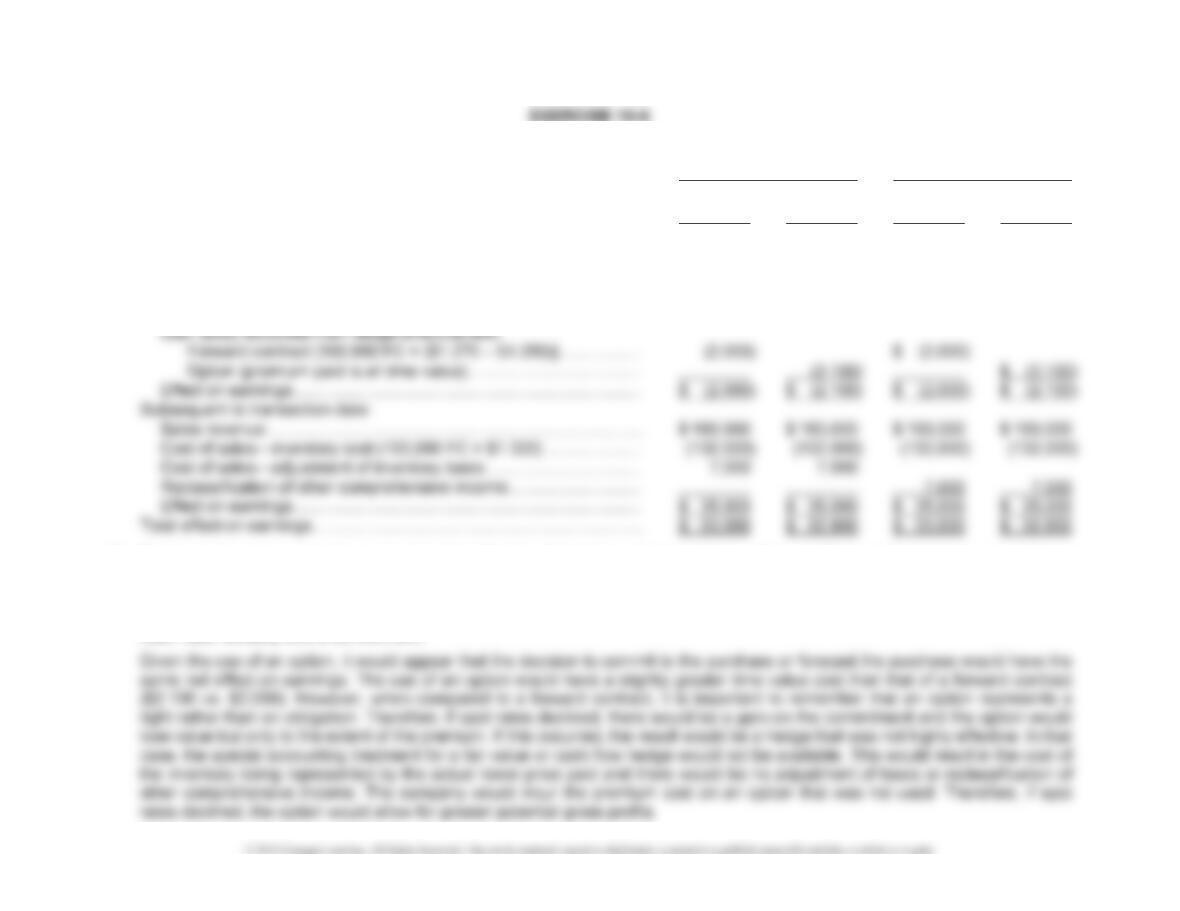

(1) Hedge of a Hedge of a

Commitment Using Forecasted Transaction

Forward Forward

Contract Option Contract Option

Prior to transaction date:

Gain (loss) on commitment [100,000 FC × ($1.250 – $1.320)] …….. $ (7,000) $ (7,000)

Gain (loss) on hedging instrument:

Forward contract [100,000 FC × ($1.320 – $1.250)] ……………… 7,000 —

Option [100,000 FC × ($1.320 spot – $1.250 strike)] …………….. 7,000 —

(2) Based on the above analysis, it would appear that the decision to commit to the purchase or forecast the purchase would have

the same net effect on earnings if a forward contract were used. Furthermore, this would be the case even if the rates moved in

the opposite direction as that assumed. Therefore, if a forward contract were used, Jackson’s decision should focus on other

factors. The legal form of a commitment is certainly much different from that of a forecasted transaction. Jackson would have

much less flexibility with a commitment.

Exercise 10-6, Concluded

In conclusion, it would appear that the best alternative would be to forecast the transaction and hedge the forecast with an

option.

Note: If spot rates were to decline below the original rate of 1 FC = $1.250 and fall to 1 FC = $1.180, the alternatives would

appear as follows:

Hedge of a Hedge of a

Commitment Using

Forecasted Transaction

Forward Forward

Contract Option Contract Option

Prior to transaction date:

Gain (loss) on commitment [100,000 FC × ($1.250 – $1.180)] …….. $ 7,000

Gain (loss) on hedging instrument:

Forward contract [100,000 FC × ($1.180 – $1.250)] ……………… (7,000)

Option (no intrinsic value – spot < strike) ……………………………..

Gain (loss) excluded from hedge effectiveness:

Forward contract [100,000 FC × ($1.270 – $1.250)] ……………… (2,000) $ (2,000)

10–9 Ch. 10—Exercises

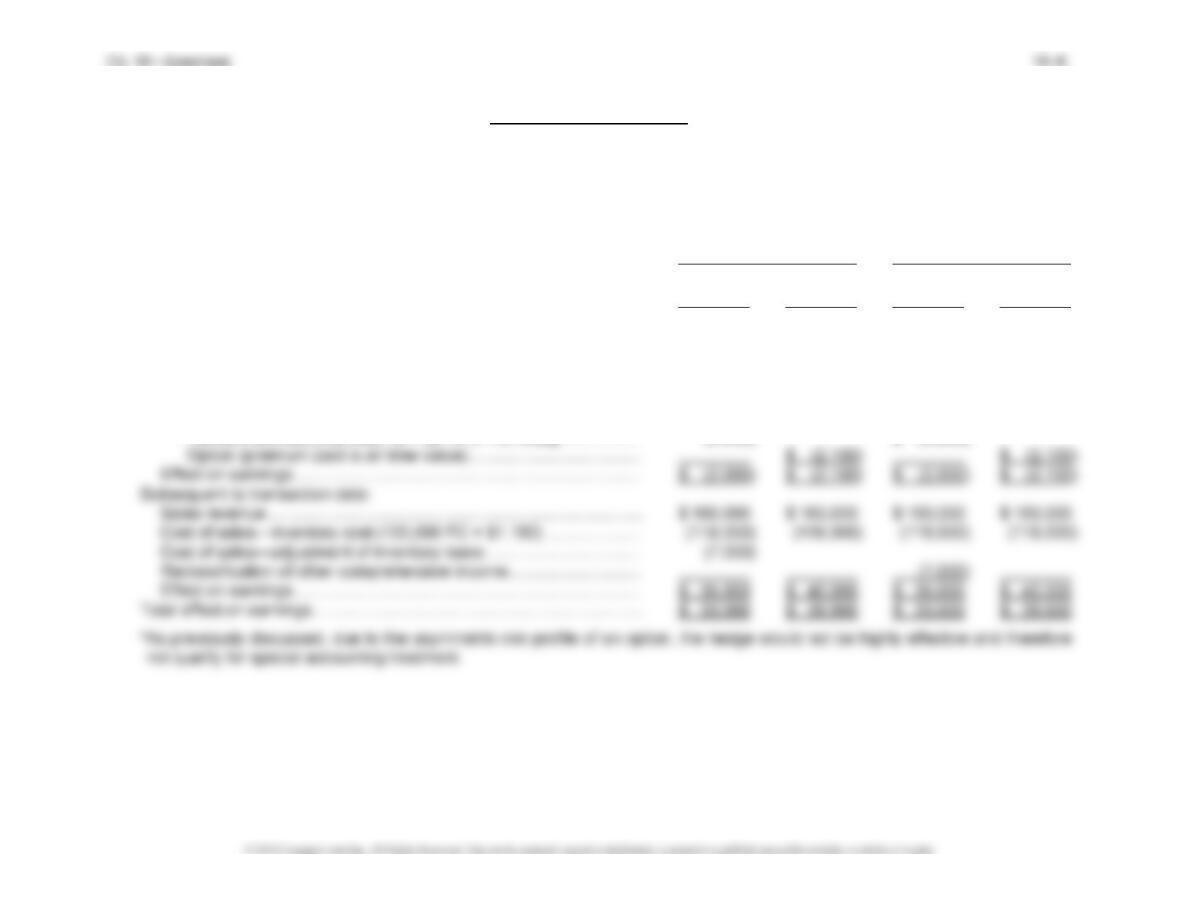

EXERCISE 10-7

Basis of Building Addition

Event or activity:

March 1 construction payment (200,000 FC × $1.50) ………………………. $ 300,000

Capitalized interest on 2-month note:

200,000 FC × 4.8% × 2/12 year × $1.48 …………………………………… 2,368

June 30 construction payment (300,000 FC × $1.55) ………………………. 465,000

Capitalized interest on 6-month note:

300,000 FC × 6.0% × 3/12 year × $1.58 …………………………………… 7,110

August 31 construction payment (400,000 FC × $1.60) …………………… 640,000

EXERCISE 10-8

Event A: Without the With the

Hedge

Hedge

Transaction exchange gain (loss)

[100,000 FC × ($1.100 – $1.150)] ………………………………………. $(5,000) $(5,000)

Forward contract gain (loss)

[100,000 FC × ($1.110 – $1.150)] ………………………………………. 4,000

Net income (loss) effect …………………………………………………………. $(5,000) $(1,000)

Event B: Without the With the

Hedge

Hedge

Gain on commitment

[(200,000 FC × ($1.172 – $1.150)] discounted 1 month ………… $ 4,378

Sales (200,000 FC × $1.170) ………………………………………………….. $ 234,000 234,000

PROBLEM 10-1

Transaction A:

Gain (Loss)

Exchange gain on exposed payable

[100,000 FC × ($1.140 – $1.150)] …………………………. $ 1,000

Transaction B:

Gain (Loss)

Gain on commitment

[100,000 FC × ($1.150 – $1.132)] …………………………. $ 1,800

Loss on forward contract

[100,000 FC × ($1.150 – $1.132)] …………………………. (1,800)

$(3,067)

Transaction D:

Change in time value* ………………………………………………. $ (200)

* On November 30, the intrinsic value is $500 and the time value is $700, versus December 31,

PROBLEM 10-2

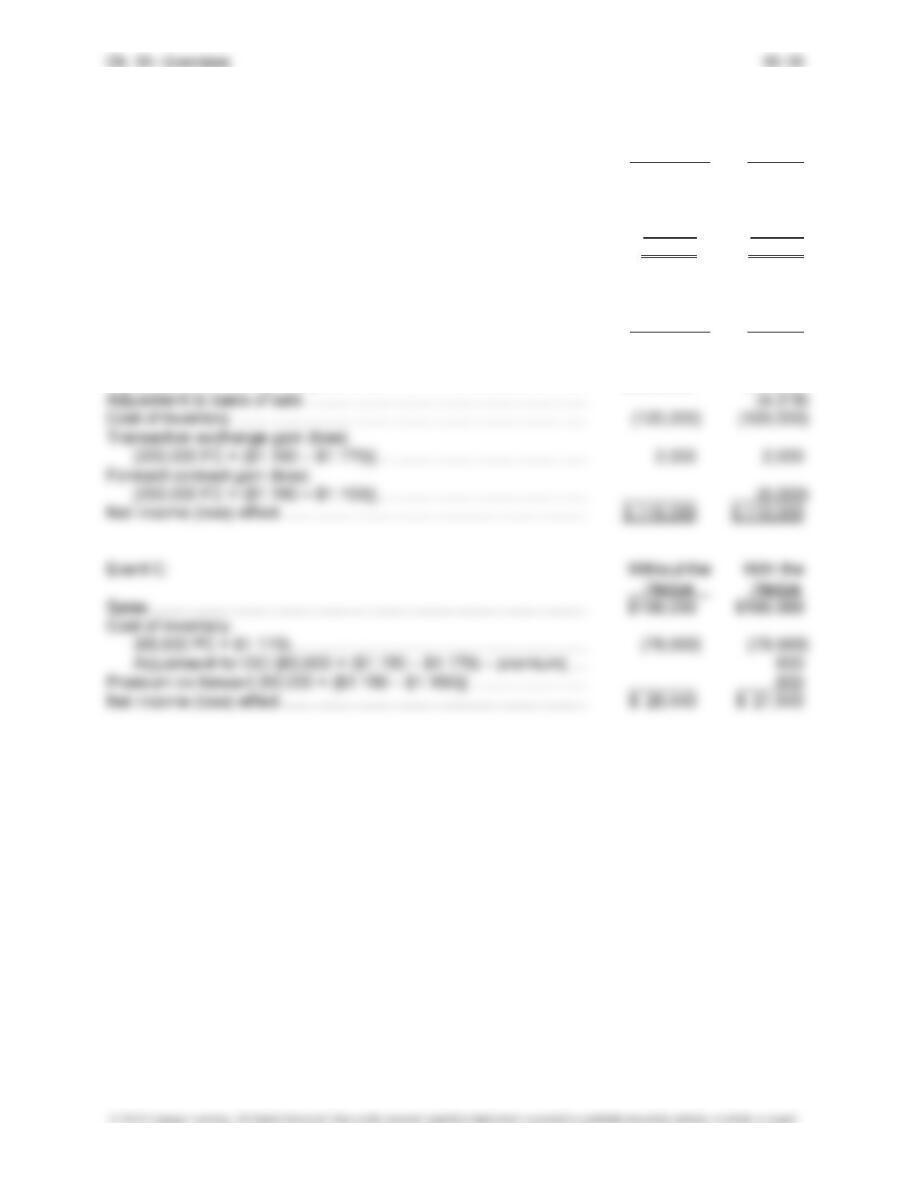

Balance sheet accounts—Debit (Credit): 2nd Quarter 3rd Quarter

Inventory of medical equipment ………………………………. $ 325,000 $ —

Firm commitment ………………………………………………….. (15,723)

Accounts receivable:

(800,000 FC × $0.470) ……………………………………… 376,000

Forward contract receivable……………………………………… 15,723 33,516

Note A:

June 1

June 30 August 15 September 30

Number of FC ………………………………….. 800,000 800,000 800,000 800,000

Spot rate—1 FC ……………………………….. $0.500 $0.485 $0.480 $0.470

Forward rate remaining time—1 FC = ….. $0.510 $0.490 $0.475 $0.468

Fair value of forward contract:

Present value of change:

n = 3.5, i = 0.50% …………………… $ 15,723

n = 0.5, i = 0.50% …………………… $ 33,516

Change in value from prior period: