CHAPTER 10

SOLUTIONS TO EXERCISES—SET B

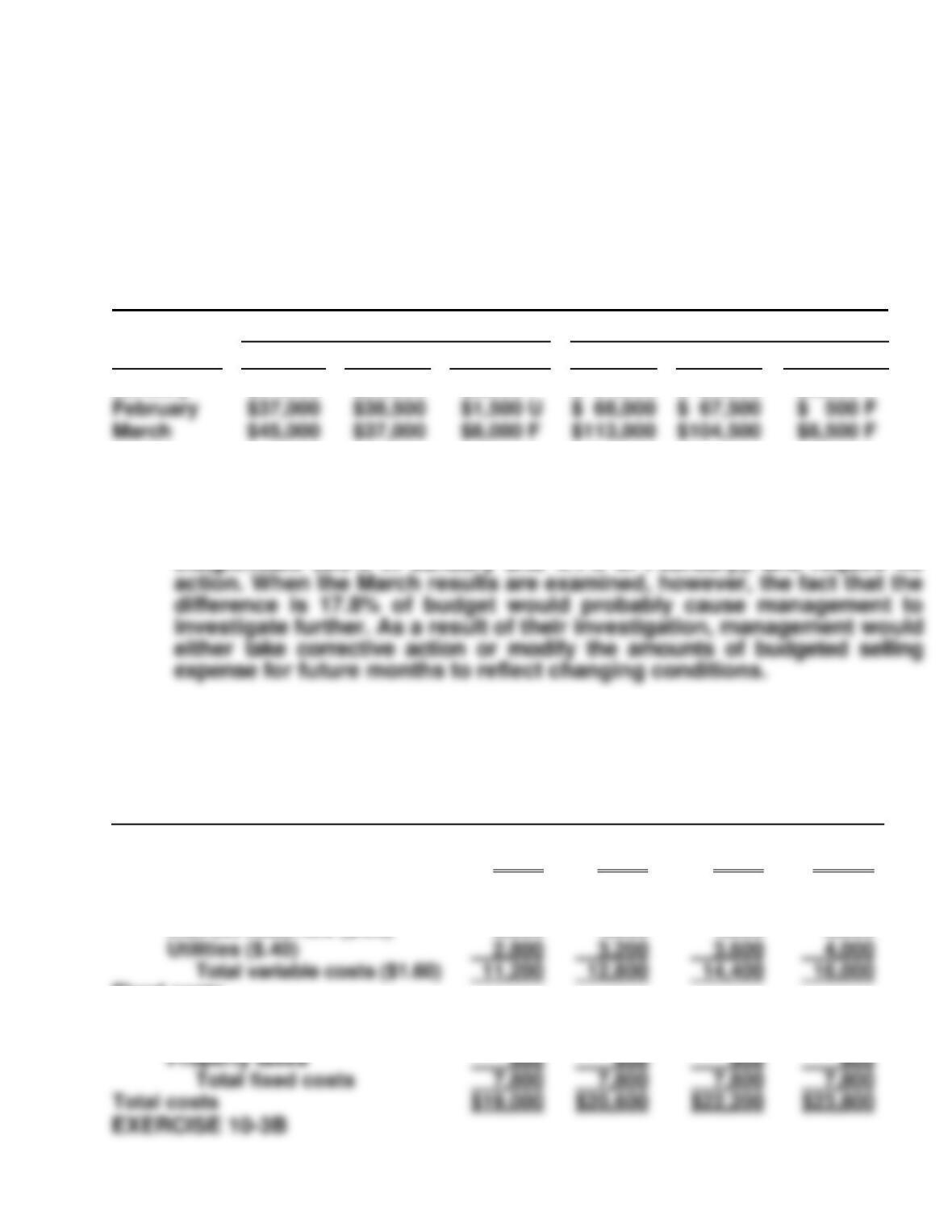

EXERCISE 10-1B

(a) MONICA COMPANY

Selling Expense Report

For March

By Month

Year–to–Date

Month

Budget

Actual

Difference

Budget

Actual

Difference

January

$31,000

$29,000

$2,000 F

$ 31,000

$ 29,000

$2,000 F

February

$38,500

$1,500 U

$ 68,000

$ 67,500

March

$37,000

$8,000 F

$104,500

$8,500 F

(b) The purpose of the Selling Expense Report is to help management

control selling expenses. The primary recipient is the sales manager.

(c) Most likely, when management scrutinized the results for January and

February, they would determine that the difference was fairly

insignificant (6.5% in January and 4.1% in February), and require no

EXERCISE 10-2B

CUBAN COMPANY

Monthly Flexible Manufacturing Overhead Budget

For the Year 2016

Activity level

Direct labor hours

Variable costs

Indirect labor ($.70)

Indirect materials ($.50)

Fixed costs

Supervision

Depreciation

7,000

$ 4,900

3,500

4,000

3,000

8,000

$ 5,600

4,000

4,000

3,000

9,000

$ 6,300

4,500

4,000

3,000

10,000

$ 7,000

5,000

4,000

3,000

(a) CUBAN COMPANY

Manufacturing Overhead Budget Report (Flexible)

For the Month Ended July 31, 2017

Difference

Direct labor hours (DLH)

Variable costs

Indirect labor ($.70)

Indirect materials ($.50)

Fixed costs

Supervision

Depreciation

Budget at

9,000 DLH

$ 6,300

4,500

4,000

3,000

Actual Costs

9,000 DLH

$ 6,100

4,300

4,000

3,000

Favorable F

Unfavorable U

$200 F

200 F

—

—

(b) CUBAN COMPANY

Manufacturing Overhead Budget Report (Flexible)

For the Month Ended July 31, 2017

Difference

Direct labor hours (DLH)

Variable costs

Indirect labor ($.70)

Indirect materials ($.50)

Fixed costs

Supervision

Budget at

8,500 DLH

$ 5,950

4,250

4,000

Actual Costs

8,500 DLH

$ 6,100

4,300

4,000

Favorable F

Unfavorable U

$150 U

50 U

—

(c) In case (a) the performance for the month was satisfactory. In case

(b) management may need to determine the causes of the unfavorable

EXERCISE 10-4B

PARADISE COMPANY

Monthly Flexible Selling Expense Budget

For the Year 2017

Activity level

Sales

Variable expenses

Sales commissions (6%)

Advertising (4%)

Fixed expenses

Sales salaries

Depreciation

$170,000

$ 10,200

6,800

35,000

7,000

$180,000

$ 10,800

7,200

35,000

7,000

$190,000

$ 11,400

7,600

35,000

7,000

$200,000

$ 12,000

8,000

35,000

7,000

EXERCISE 10-5B

(a) PARADISE COMPANY

Selling Expense Budget Report (Flexible)

For the Month Ended March 31, 2017

Difference

Sales

Variable expenses

Sales commissions

Advertising

Fixed expenses

Sales salaries

Depreciation

Budget

$170,000

$ 10,200

6,800

35,000

7,000

Actual

$170,000

$ 11,000

7,000

35,000

7,000

Favorable F

Unfavorable U

$ 800 U

200 U

0 U

0 U

EXERCISE 10-5B (Continued)

(b) PARADISE COMPANY

Selling Expense Budget Report (Flexible)

For the Month Ended March 31, 2017

Difference

Sales

Variable expenses

Sales commissions

Advertising

Fixed costs

Sales salaries

Depreciation

Budget

$180,000

$ 10,800

7,200

35,000

7,000

Actual

$180,000

$ 11,000

7,000

35,000

7,000

Favorable F

Unfavorable U

$200 U

200 F

0 U

0 U

(c) Flexible budgets are essential in evaluating a manager’s performance in

controlling variable expenses because the budget allowance varies

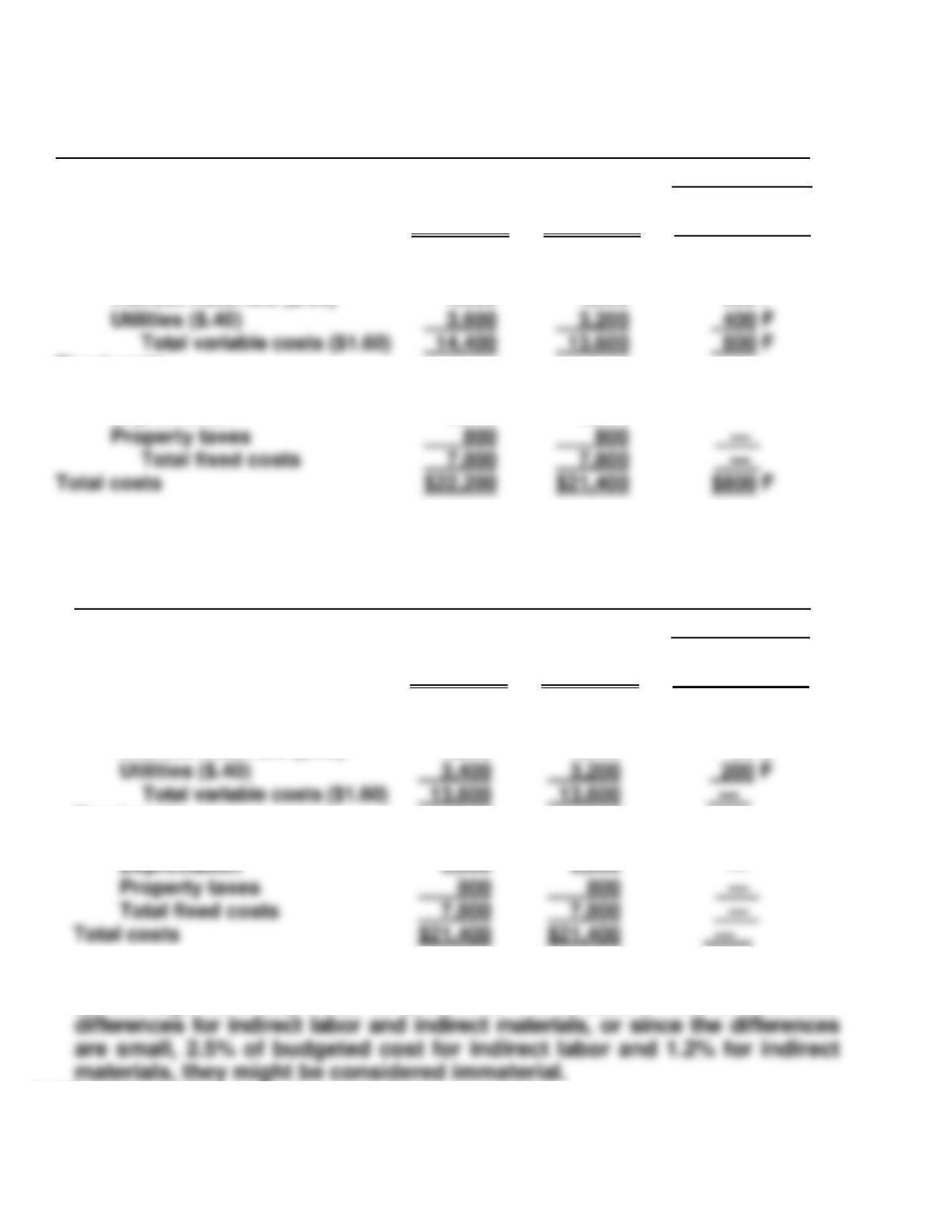

EXERCISE 10-6B

(a) SOPHIA COMPANY

Manufacturing Overhead Budget Report (Flexible)

For the Quarter Ended March 31, 2017

Difference

Budget

Actual

Favorable F

Unfavorable U

Variable costs

Indirect materials

Indirect labor

Fixed costs

Supervisory salaries

Depreciation

Property taxes and

insurance

$13,000

10,000

36,000

7,000

6,000

$16,000

9,700

36,000

7,000

5,900

$3,000 U

300 F

0 U

0 U

100 F

(b) SOPHIA COMPANY

Manufacturing Overhead Responsibility Report

For the Quarter Ended March 31, 2017

Difference

Controllable Costs

Budget

Actual

Favorable F

Unfavorable U

Indirect materials

Indirect labor

$13,000

10,000

$16,000

9,700

$3,000 U

300 F

*Includes variable and fixed costs

EXERCISE 10-7B

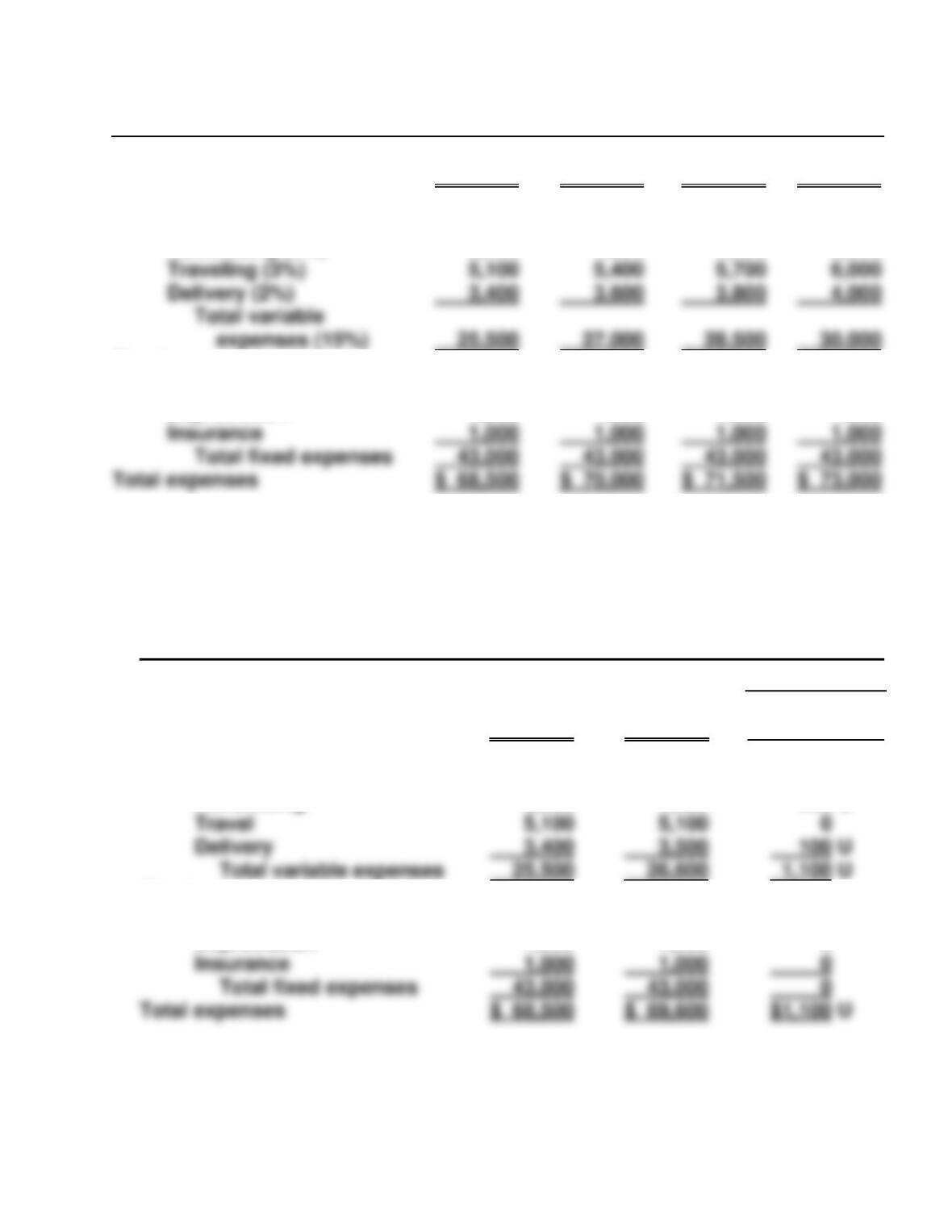

(a) HARMON COMPANY

Selling Expense Budget Report (Flexible)

Clothing Department

For the Month Ended October 31, 2017

Difference

Sales in units

Variable expenses

Sales commissions ($.25)

Advertising expense ($.10)

Fixed expenses

Rent

Sales salaries

Office salaries

Budget

10,000

$ 2,500

1,000

1,500

1,000

800

Actual

10,000

$ 2,700

900

1,500

1,000

800

Favorable F

Unfavorable U

$200 U

100 F

0

0

0

(b) Lance should not have been reprimanded. As shown in the flexible budget

EXERCISE 10-8B

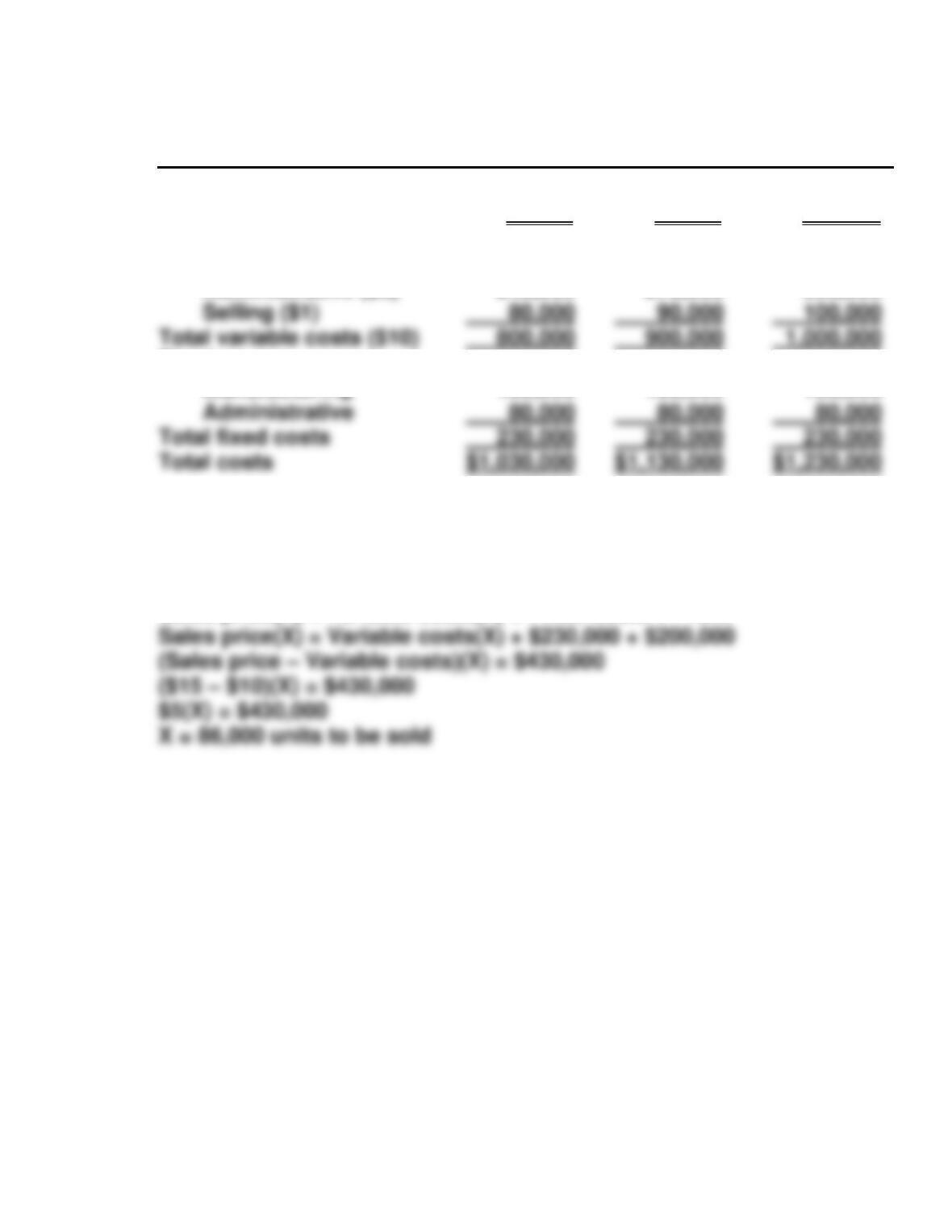

(a) REDSTONE INC.

Flexible Production Cost Budget

Activity level

Production levels 80,000 90,000 100,000

Variable costs:

Manufacturing ($6) $ 480,000 $ 540,000 $ 600,000

Administrative ($3) 240,000 270,000 300,000

Fixed costs:

Manufacturing 150,000 150,000 150,000

(b) $200,000 profit before taxes calculation in units:

Let (X) represent number of units

Sales price(X) = Variable costs(X) + Fixed costs + Profit

EXERCISE 10-9B

(a) MARKET GROOMERS

Flexible Budget

Activity level

Direct labor hours 500 600 700

Variable costs:

Grooming supplies ($5.00) $ 2,500 $ 3,000 $ 3,500

Direct labor ($10.00) 5,000 6,000 7,000

(b) A flexible budget presents expected costs at various levels of production

volume, not just one, so that comparisons can be made between actual

costs and budgeted costs at the same volume. This allows the person to

(c) $18,500 ÷ 500 = $37.00

(d) Cost formula is $10,000 + [$17.00(X)], where (X) = direct labor hours

Total cost = $10,000 + ($17.00 X 650) = $21,050.

EXERCISE 10-10B

(a) MEEKS PLUMBING COMPANY

Home Plumbing Services Segment

Responsibility Report

For the Quarter Ended March 31, 2017

Budget

Actual

Difference

Favorable F

Unfavorable U

Service revenue

$30,000

$31,500

$1,500 F

Variable costs:

Material and supplies

1,500

1,300

200 F

Wages

4,000

4,200

200 U

Controllable fixed costs:

Supervisory salaries

10,000

10,500

500 U

4,000

3,300

Total controllable fixed costs

500 F

Controllable margin

(b)

MEMO

TO: Karen Meeks

FROM: Student

SUBJECT: The Reporting Principles of Performance Reports

When evaluating the performance of a company’s segments, the performance reports

should:

1. Contain only data that are controllable by the segment’s manager.

2. Provide accurate and reliable budget data to measure performance.

EXERCISE 10-11B

Gas and oil

Total variable costs

8,200

8,900

Contribution margin

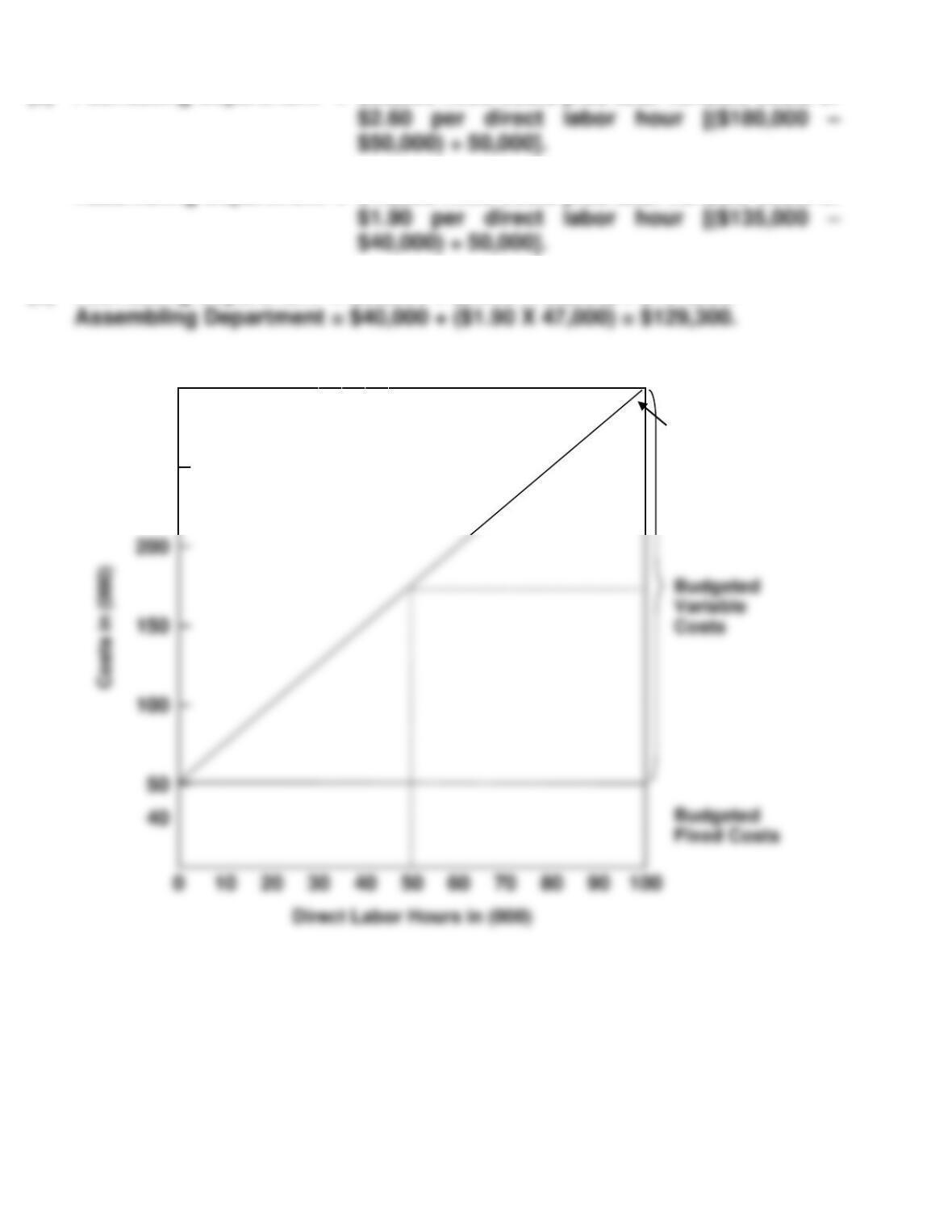

(a) Fabricating Department = $50,000 fixed costs plus total variable costs of

Assembling Department = $40,000 fixed costs plus total variable costs of

(b) Fabricating Department = $50,000 + ($2.60 X 53,000) = $187,800.

(c)

$300

200

100

Total

Budgeted

Cost Line

250

EXERCISE 10-12B

(a)

To Detroit Department Manager—Finishing Month: July

Controllable Costs:

Budget

Actual

Fav/Unfav

Direct Materials

$ 55,000

$ 51,700

$3,300 F

(b)

To Assembly Plant Manager—Detroit Month: July

Controllable Costs:

Budget

Actual

Fav/Unfav

Detroit Office

Departments:

$ 87,500

$ 90,000

$2,500 U

(c)

To Vice President—Production Month: July

Controllable Costs:

Budget

Actual

Fav/Unfav

V P Production

Assembly plants:

Atlanta

$ 160,000

421,000

$ 165,000

424,000

$5,000 U

3,000 U

EXERCISE 10-13B

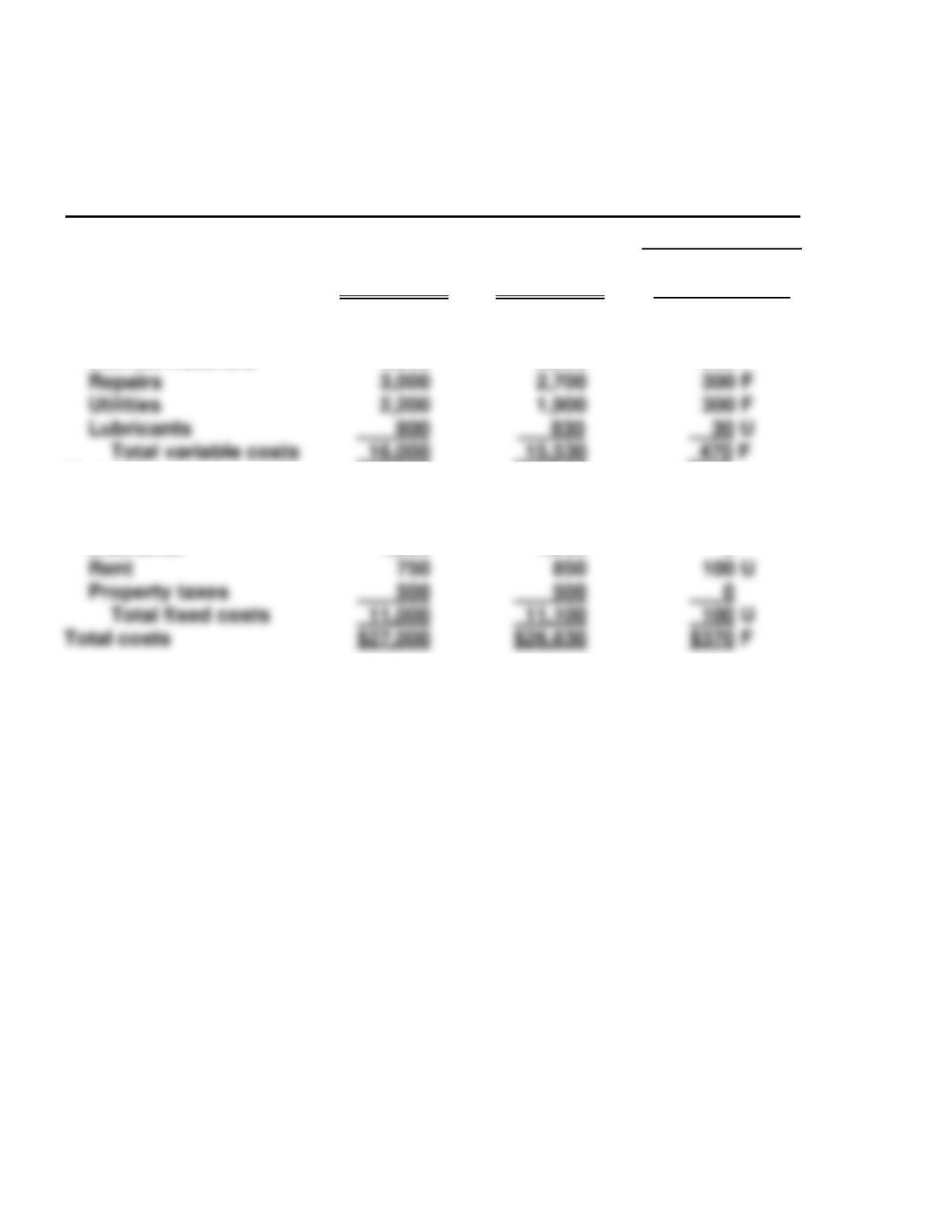

(a) STARLIGHT COMPANY

Mixing Department

Responsibility Report

For the Month Ended January 31, 2017

Controllable Cost

Budget

Actual

Difference

Indirect labor

Indirect materials

$11,100

7,500

$11,900

9,300

$ 800 UU

1,800 U

(b) Most likely, when management examined the responsibility report for

January, they would determine that the difference was insignificant for

indirect labor (7.2% of budget), lubricants (3%), and maintenance (0%)

EXERCISE 10-14B

(a) (1) Controllable margin ($260,000 – $100,000) $160,000

(2) Variable costs ($600,000 – $260,000) 340,000

EXERCISE 10-14B (Continued)

(b) BROGAN MANUFACTURING INC.

Women’s Shoe Division

Responsibility Report

For the Month Ended June 30, 2017

Difference

Budget

Actual

Favorable F

Unfavorable U

Sales

Variable costs

$600,000

335,000

$600,000

340,000

$ 0 U

5,000 U

EXERCISE 10-15B

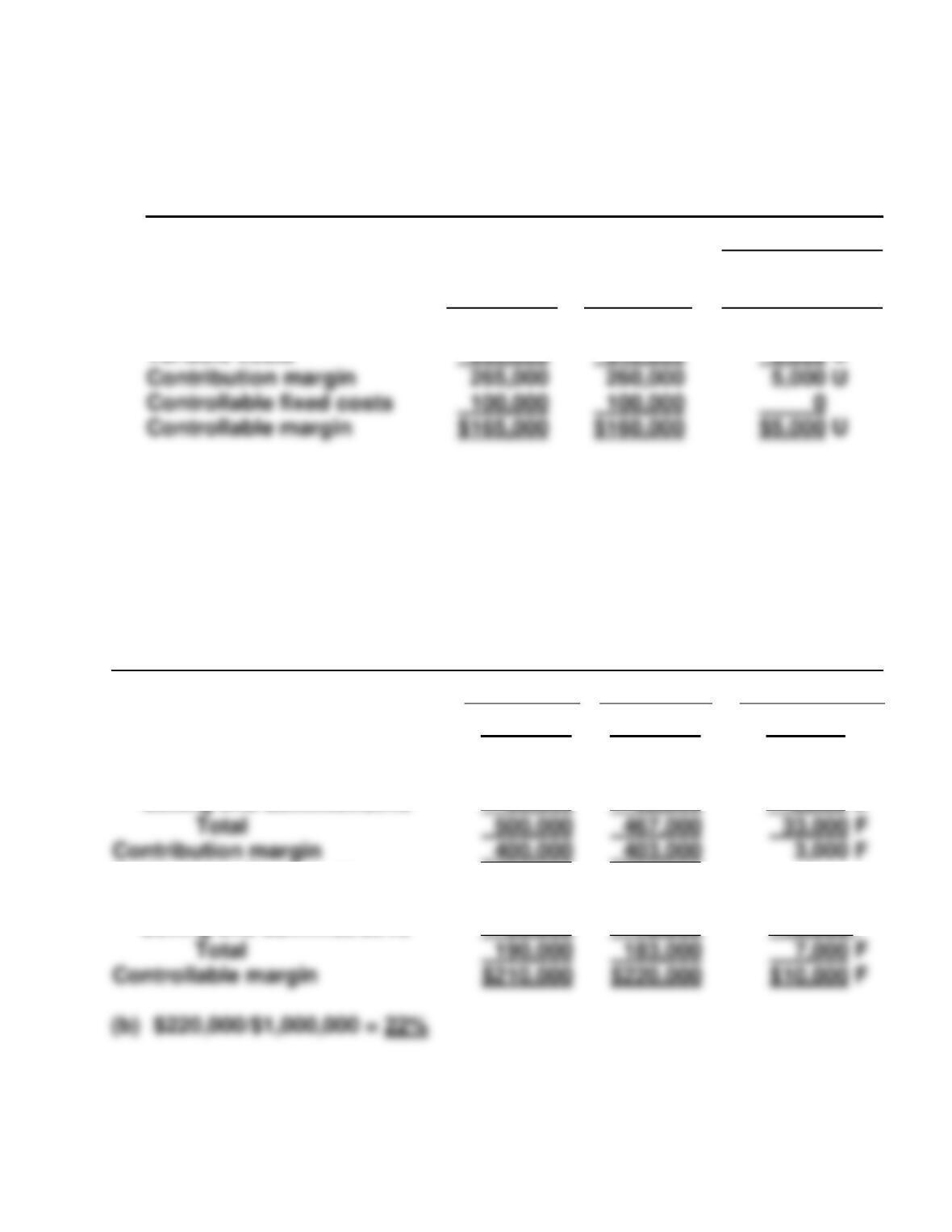

(a) SWENSON COMPANY

Sports Equipment Division

Responsibility Report

For the Year Ended December 31, 2017

Budget

Actual

Difference

Sales

$900,000

$870,000

$30,000 U

Variable costs

Cost of goods sold

440,000

405,000

35,000 F

Selling and administrative

60,000

62,000

2,000 U

Total

33,000 F

Contribution margin

403,000

3,000 F

Controllable fixed costs

Cost of goods sold

100,000

105,000

5,000 U

Selling and administrative

90,000

78,000

12,000 F

Total

7,000 F

Controllable margin

$210,000

$220,000

$10,000 F

EXERCISE 10-16B

(a) Controllable margin = ($3,200,000 – $2,500,000 – $400,000) = $300,000

(b) (1) Contribution margin percentage is 21.88%, or ($700,000 ÷ $3,200,000)

(2) ($300,000 + $100,000) ÷ $5,000,000 = 8%

EXERCISE 10-17B

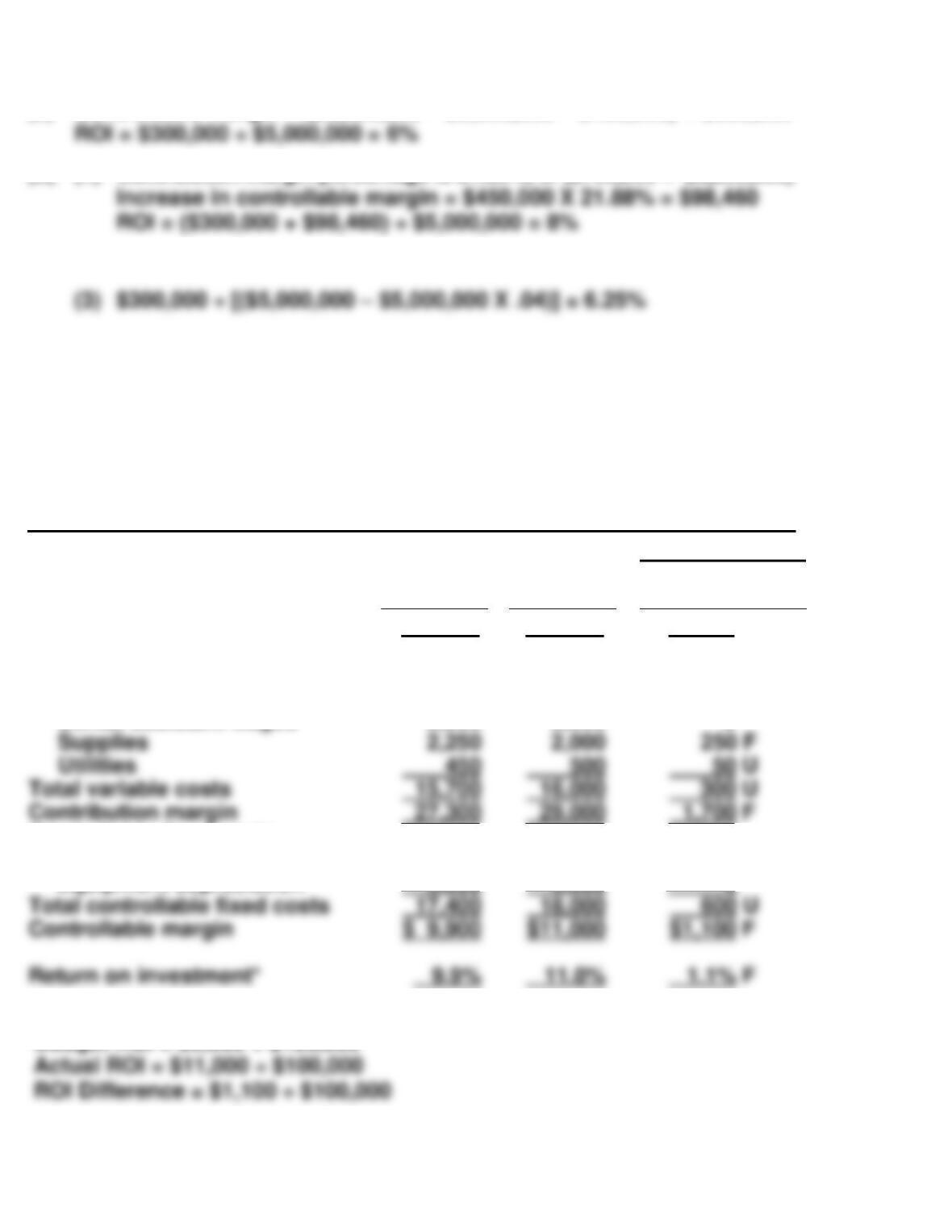

(a) MEND AND DONNER DENTAL CLINIC

Preventive Services

Responsibility Report

For the Month Ended May 31, 2017

Budget

Actual

Difference

Favorable F

Unfavorable U

Service revenue

$43,000

$45,000

$2,000 F

Variable costs

Filling materials

6,700

7,000

300 U

Novocain

3,800

4,000

200 U

Dental assistant wages

2,500

2,500

0

Supplies

2,250

2,000

250 F

Utilities

450

500

50 U

Total variable costs

300 U

Contribution margin

Controllable fixed costs

Dentist salary

11,400

12,000

600 U

Equipment depreciation

6,000

6,000

0

Controllable margin

$ 9,900

$11,000

$1,100 F

Return on investment*

1.1% F

*Average investment = ($102,400 + $97,600) ÷ 2 = $100,000

Budget ROI = $9,900 ÷ $100,000

EXERCISE 10-17B (Continued)

(b)

MEMO

TO: Drs. Richard Mend and Tommy Donner

FROM: Student

SUBJECT: Deficiencies in the Current Responsibility Reporting System

The current reporting system has the following deficiencies:

1. It does not clearly show both budgeted goals and actual performance.

2. It does not indicate the contribution margin generated by the center,

showing the amount available to go towards covering controllable

All of these deficiencies have been addressed in the recommended responsibility

report attached. As can be seen from that report, the Preventative Services

center is profitable. The service revenues generated in this center are adequate to

EXERCISE 10-18B

Jets:

ROI = Controllable margin ÷ Average operating assets

15% = Controllable margin ÷ $25,000,000

Contribution margin = Controllable margin + Controllable fixed costs

= $3,750,000 + $2,000,000

Hellicopters:

ROI

=

Controllable margin

÷

Average operating assets

10%

=

$95,000

÷

Average operating assets

Controllable marginin

=

Contribution margin

–

Controllable fixed costs

$95,000

=

$200,000

–

Controllable fixed costs

=

$105,000

Contribution margin

=

Service revenue – Variable costs

$200,000

=

$600,000 – Variable costs

=

$400,000

EXERCISE 10-18B (Continued)

Satellites:

Controllable margin

=

Contribution margin

–

Controllable fixed costs

Contribution margin

=

Service revenue

–

Variable costs

$820,000

EXERCISE 10-19B

(a) North Division: ROI = $210,000 ÷ $1,000,000 = 21%

(b) North Division:

Residual Income = $210,000 – (.16 X $1,000,000) = $50,000

West Division:

(c) (1) If ROI is used to measure performance, only the North Division (with

an 21% ROI) and the West Division (with a 18% ROI) would make the

additional investment that provides a 22% ROI. The South Division

*EXERCISE 10-20B

(b)

Controllable margin

–

(Minimum rate of return X Average operating assets)

=

Residual income

$250,000

–

(Minimum rate of return X $1,250,000)

=

$90,000

=

Minimum rate of return

=

(c)

Controllable margin

–

(Minimum rate of return X Average operating assets)

=

Residual income

Controllable margin

–

(18% X $1,500,000)

=

$150,000

Controllable margin

=

(d)

ROI

=

Controllable margin

÷

Average operating assets

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 10-1C

(a) DUNES COMPANY

Flexible Monthly Manufacturing Overhead Budget

Assembly Department

For the Year 2017

Activity level

Direct labor hours

Variable costs

Indirect labor ($.30)

Indirect materials ($.20)

Fixed costs

Supervision ($75,000/12)

Depreciation ($30,000/12)

Insurance ($12,000/12)

18,000

$ 5,400

3,600

6,250

2,500

1,000

20,000

$ 6,000

4,000

6,250

2,500

1,000

22,000

$ 6,600

4,400

6,250

2,500

1,000

24,000

$ 7,200

4,800

6,250

2,500

1,000

PROBLEM 10-1C (Continued)

(b) DUNES COMPANY

Manufacturing Overhead Budget Report (Flexible)

Assembly Department

For the Month Ended January 31, 2017

Difference

Direct labor hours (DLH)

Variable costs

Indirect labor

Indirect materials

Fixed costs

Supervision

Depreciation

Insurance

Budget at

20,000 DLH

$ 6,000

4,000

6,250

2,500

1,000

Actual Costs

20,000 DLH

$ 6,300

3,800

6,250

2,500

1,000

Favorable F

Unfavorable U

$300 U

200 F

0

0

0

(c) Control over both variable and fixed costs was good.

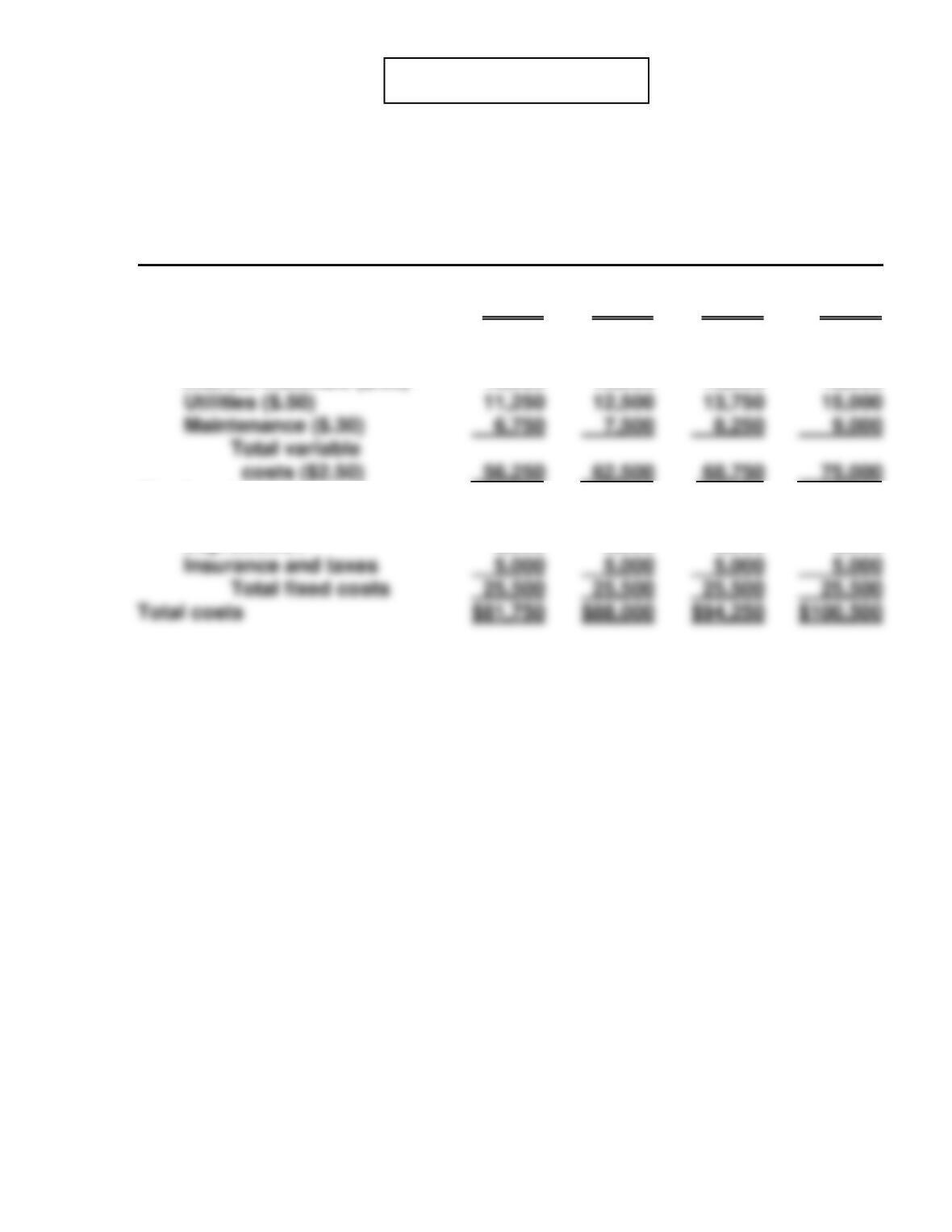

PROBLEM 10-2C

(a) WILLARD MANUFACTURING COMPANY

Flexible Monthly Manufacturing Overhead Budget

Assembly Department

For the Year 2017

Activity level

Direct labor hours

Variable costs

Indirect labor ($1.10)

Indirect materials ($.60)

Fixed costs

Supervision

Depreciation

22,500

$24,750

13,500

12,500

8,000

25,000

$27,500

15,000

12,500

8,000

27,500

$30,250

16,500

12,500

8,000

30,000

$ 33,000

18,000

12,500

8,000

PROBLEM 10-2C (Continued)

(b) WILLARD MANUFACTURING COMPANY

Assembly Department

Manufacturing Overhead Budget Report (Flexible)

For the Month Ended July 31, 2017

Difference

Direct labor hours (DLH)

Variable costs

Indirect labor

Indirect materials

Fixed costs

Supervision

Depreciation

Budget at

27,500 DLH

$30,250

16,500

12,500

8,000

Actual Costs

27,500 DLH

$29,000

14,000

12,500

8,000

Favorable F

Unfavorable U

$1,250 F

2,500 F

0 F

0 F

(c) Based on the above budget report, control over costs was effective. For

PROBLEM 10-2C (Continued)

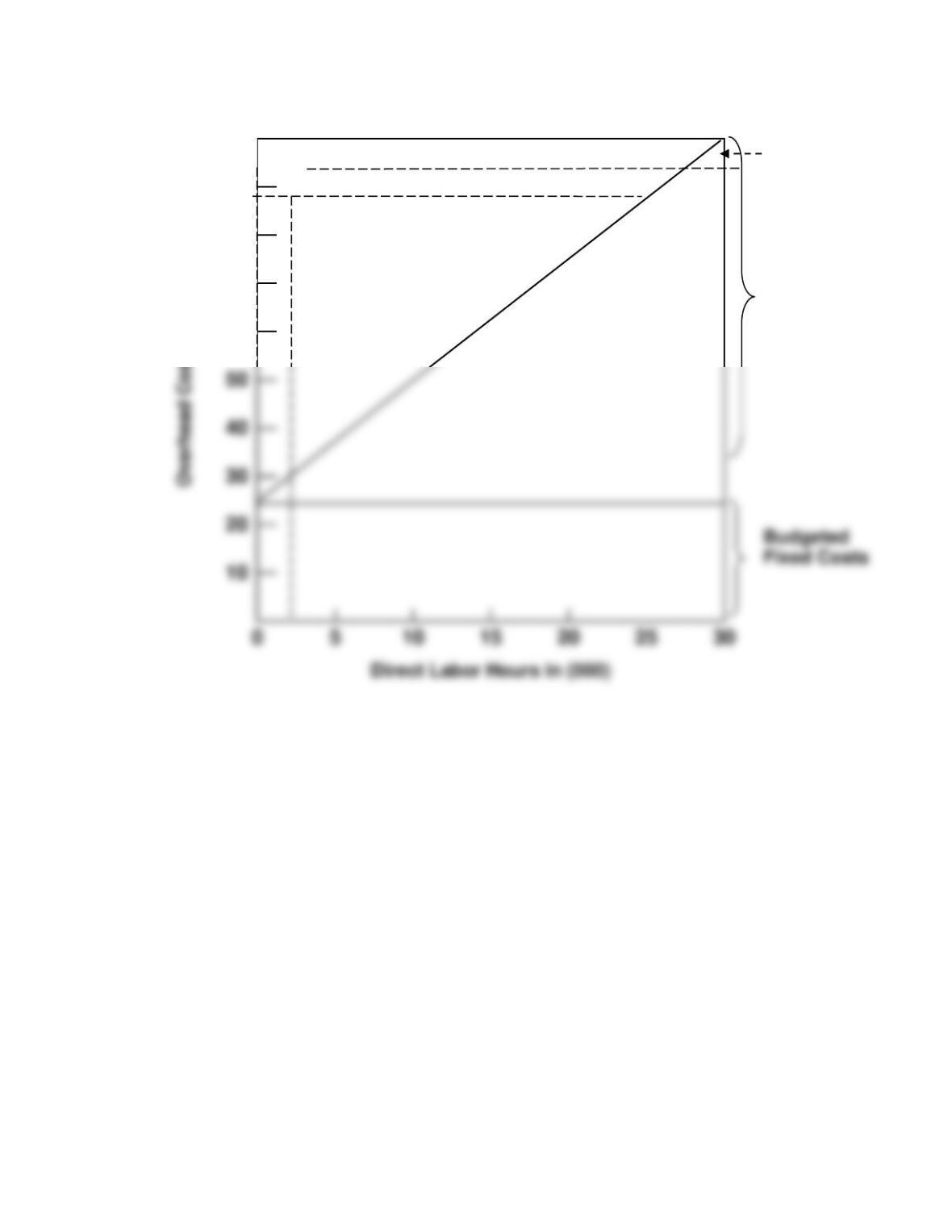

(e)

$100

Total

Budgeted

Cost Line

90

80

70

Budgeted

Variable

Costs

60

40

30

20

10

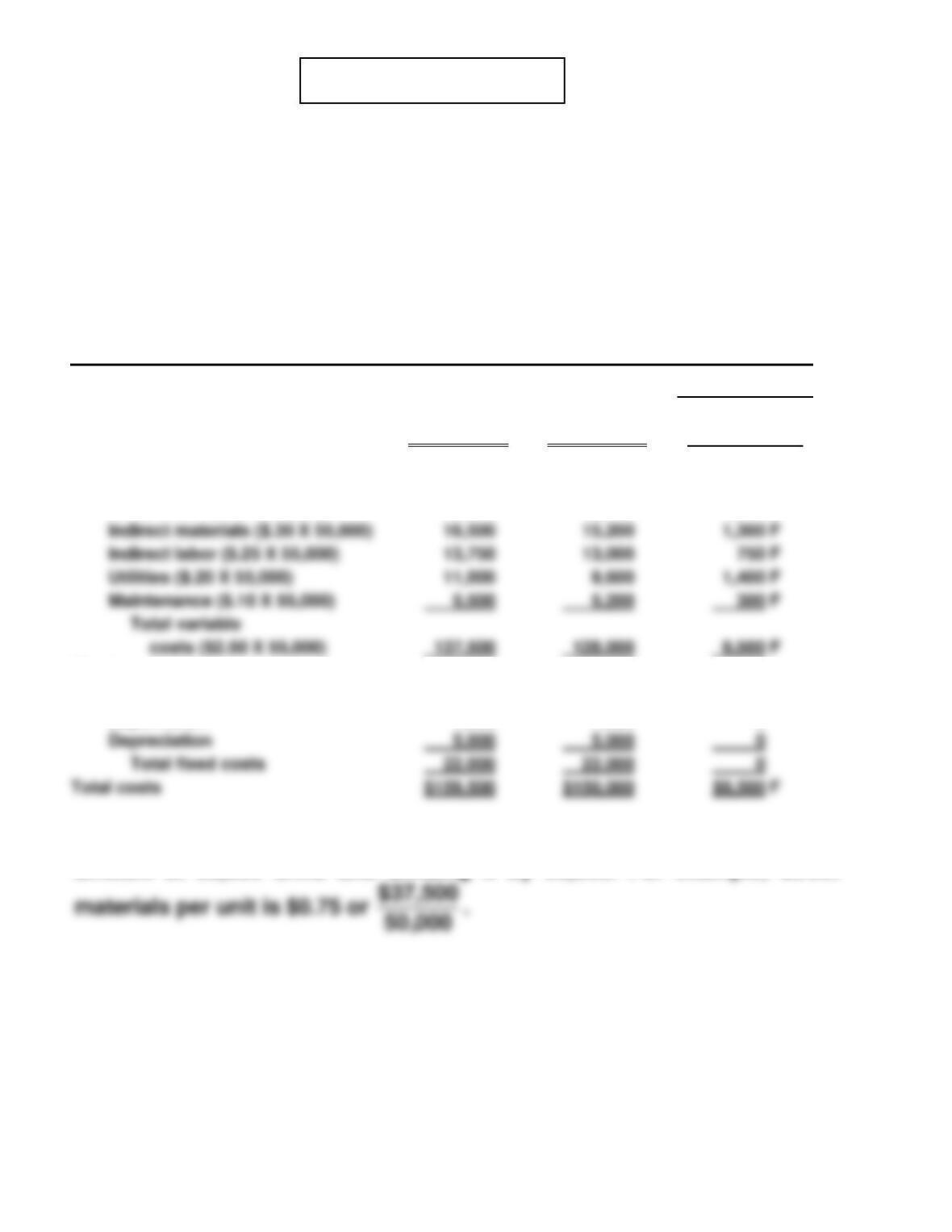

PROBLEM 10-3C

(a) The formula is fixed costs $22,000 plus total variable costs of $2.50 per

unit ($125,000 ÷ 50,000 units).

(b) ANSON COMPANY

Packaging Department

Budget Report (Flexible)

For the Month Ended May 31, 2017

Difference

Units

Variable costs*

Direct materials ($.75 X 55,000)

Direct labor ($.90 X 55,000)

Fixed costs

Rent

Supervision

Budget at

55,000 Units

$ 41,250

49,500

10,000

7,000

Actual Costs

55,000 Units

$ 38,000

47,000

10,000

7,000

Favorable F

Unfavorable U

$3,250 F

2,500 F

0 F

0 F

*Note that the per unit variable costs are computed by taking the budget

amount at 50,000 units and dividing it by 50,000. For example, direct

This report provides a better basis for evaluating performance because

the budget is based on the level of activity actually achieved.

PROBLEM 10-3C (Continued)

(c) ANSON COMPANY

Packaging Department

Budget Report (Flexible)

For the Month Ended June 30, 2017

Difference

Units

Variable costs

Direct materials ($.75 X 40,000)

Direct labor ($.90 X 40,000)

Indirect materials ($.30 X 40,000)

Fixed costs

Rent

Supervision

Budget at

40,000 Units

$ 30,000

36,000

12,000

10,000

7,000

Actual Costs

40,000 Units

$ 30,400*

37,600

12,160

10,000

7,000

Favorable F

Unfavorable U

$ 400 U

1,600 U

160 U

0 U

0 U

*Note that the actual variable costs in June was 20% less than the actual

costs in May. Therefore to find the actual costs in June, the actual variable

May

(actual)

June

(actual)

Direct materials

Direct labor

$ 38,000 X 80%

47,000 X 80%

=

$ 30,400

37,600

PROBLEM 10-4C

(a) ARLEN MANUFACTURING INC.

Electronics Division

Responsibility Report

For the Year Ended December 31, 2017

Difference

Budget

Actual

Favorable F

Unfavorable U

Sales

Variable costs

Cost of goods sold

Controllable fixed costs

Cost of goods sold

Selling and administrative

$2,400,000

1,200,000

200,000

60,000

$2,200,000

1,260,000

191,000

63,000

$200,000 U

60,000 U

9,000 F

3,000 U

(b) The manager did not effectively control revenues and costs. Contribution

margin was $252,000 unfavorable and controllable margin was $246,000

unfavorable. Contribution margin was unfavorable primarily because

sales were $200,000 under budget and variable cost of goods sold was

(c) Two costs are excluded from the report: (1) noncontrollable fixed costs

and (2) indirect fixed costs. The reason is that neither cost is controllable by

the Electronics Division Manager.

PROBLEM 10-5C

(a) MARX MANUFACTURING COMPANY

Weedeater Division

Responsibility Performance Report

For the Year Ended December 31, 2016

(in thousands of dollars)

Difference

Budget

Actual

Favorable F

Unfavorable U

Sales

Variable costs

Cost of goods sold

Selling and administrative

Total

$3,020

1,310

350

1,660

$2,900

1,400

290

1,690

$120 U

90 U

60 F

30 U

ROI

3% U

PROBLEM 10-5C (Continued)

(b) The performance of the manager of the Weedeater Division was below

budget expectations for the year. The item that top management should

likely investigate first is the reason why sales were $120,000 below

(c) (1) [$800,000 + ($1,400,000 X 15%)] ÷ $5,000,000 = 20.2%.

PROBLEM 10-6C

(a) No. 1

To Cutting Department Manager—New York Division Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

Indirect labor

Indirect materials

$ 90,000

61,000

$ 95,000

62,500

$ 5,000 U

1,500 U

No. 2

To Division Production Manager—New York Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

New York Division

Departments:

Cutting

$ 70,000

224,000

$ 73,100

240,100

$ 3,100 U

16,100 U

No. 3

To Vice-President—Production Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

V-P Production

Divisions:

New York

$ 70,000

717,000

$ 73,000

752,200

$ 3,000 U

35,200 U

PROBLEM 10-6C (Continued)

No. 4

To President Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

President

Vice-Presidents:

Production

$ 91,300

2,252,000

$ 96,200

2,307,200

$ 4,900 U

55,200 U

(b) (1) Within the New York division the rankings of the department managers

were: (1) Finishing, (2) Shaping, and (3) Cutting. If the rankings were

(2) At the division manager level, the rankings were: (1) San Francisco, (2)

Tulsa, and (3) New York.

(3) Rankings in terms of dollars may be somewhat misleading in this

case because of the substantial difference between the production

*PROBLEM 10-7C

(a) (1) ROI = Controllable Margin ÷ Average Operating Assets

(2) Residual Income = Controllable Margin – (Minimum Rate of Return X

Average Operating Assets)

(b) The management of Custom Enterprises would clearly have accepted the

investment opportunity it had in 2017 if residual income had been used

as the performance measure because an increase in residual income

results from a project whose ROI is greater than the minimum rate of

return.

If management of the division had used ROI as the performance