313

E10–26

Piecework compensation is a characteristic of a traditional manufacturing philos-

ophy that is inconsistent with just–in-time. Under just-in-time, workers are viewed

not just as laborers but as valuable assets of the company. The company wants

E10–27

a. The Japanese supply chain model is one based on long-term arrangements

and partnership. The Japanese automobile manufacturers want their suppliers

to be financially healthy because they rely on them for innovation. The Big

Three automakers, in contrast, are only concerned about getting the best

short-term price from their suppliers. The article seems to imply that the

longer-term benefits from partnership are being ignored by the Big Three. As a

result, they are willing to view their supplier relationships as temporary―until

E10–27, Concluded

c. Supply chain management is often beneficial to the customer. However, the

customer may have to trade off between short-term and longer-term benefits.

E10–28

Quickie’s team approaches are very different from using a manager to hire and

evaluate employees. First, the input of many individuals goes into the hiring

decision. In this way, the viewpoints of a variety of people are brought into the

315

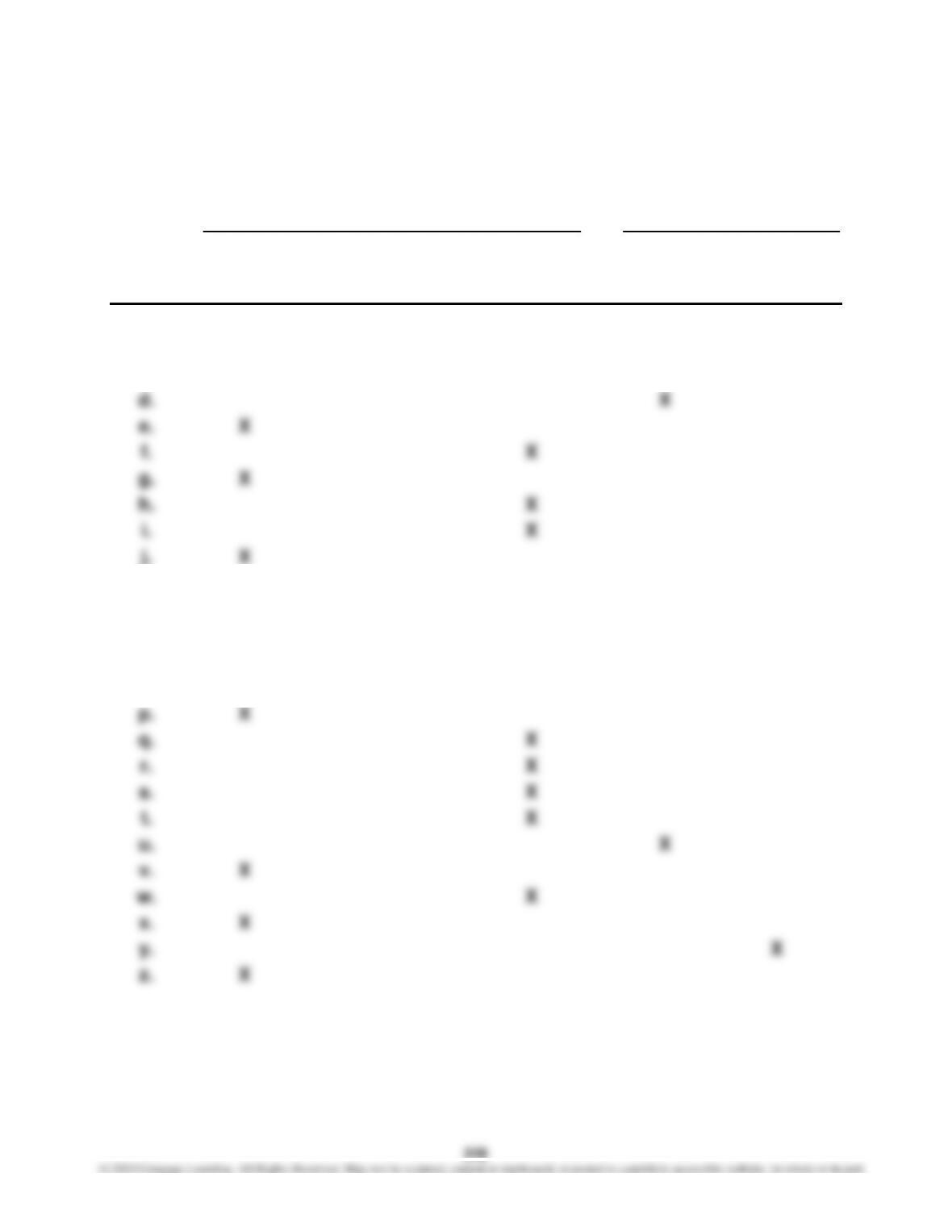

E10–29

a.

A

B

C

D

E

F

G

1

Patient Mims

Patient Slater

2

Activity

Activity

Usage ×

Activity

Rate

Activity

= Cost

Activity

Usage ×

Activity

Rate

Activity

= Cost

3

Room and

meals

2 days

$125/day

$ 250

4 days

$125/day

$ 500

4

Radiology

4 images

$180/image

720

7 images

$180/image

1,260

5

Pharmacy

6 orders

90

$15/order

6

Chemistry lab

2 tests

180

5 tests

$90/test

8

Total cost

$2,320

b. Patient Slater apparently had a more serious condition than did Patient Mims.

Patient Mims required less operating room hours, fewer tests and images,

and fewer days to recover than did Patient Slater. Thus, the activity cost to

Patient Mims is nearly one-third that of Patient Slater.

316

E10–30

a.

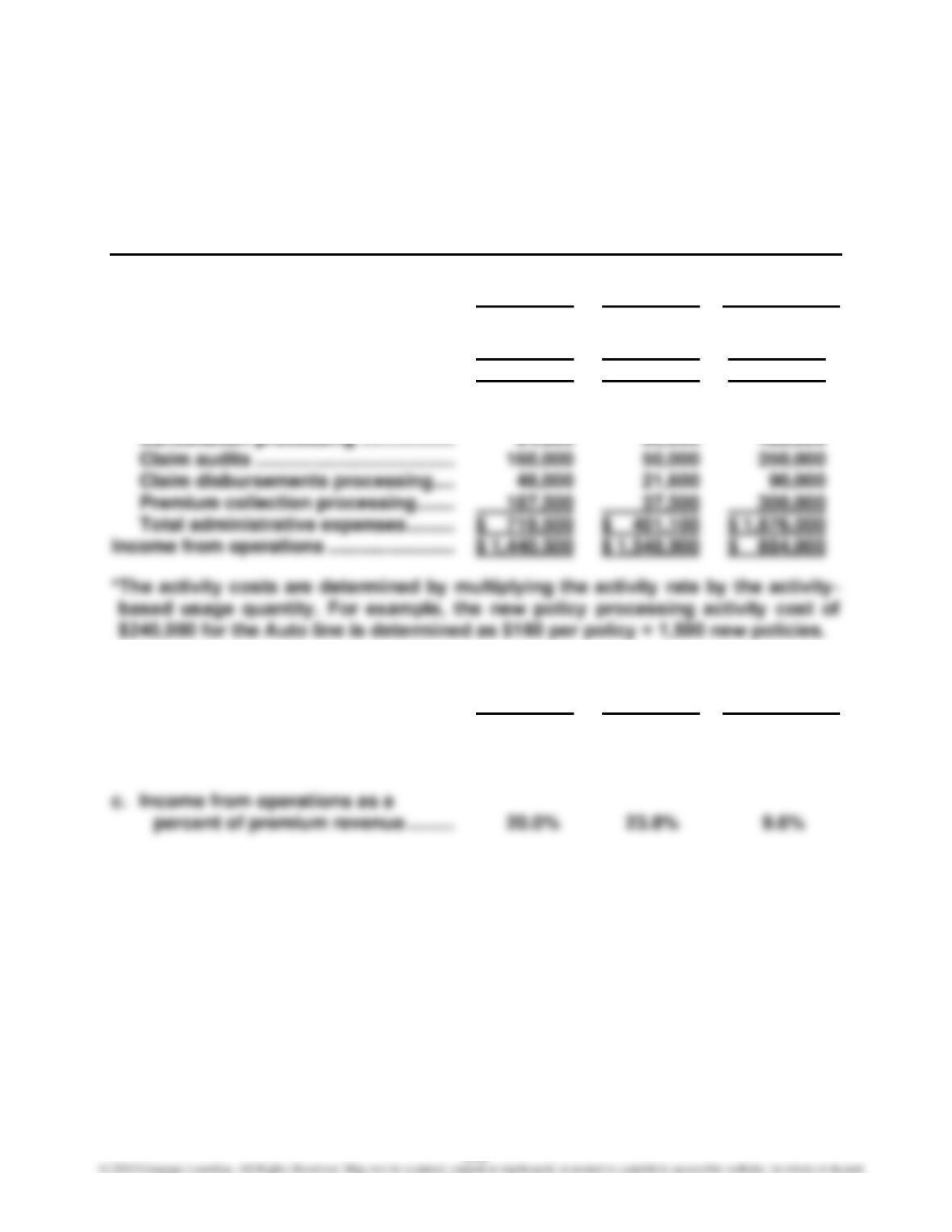

UMBRELLA INSURANCE COMPANY

Product Profitability Report

For the Year Ended December 31, 20Y2

Workers’

Auto Comp. Homeowners

Premium revenue …………………………….. $ 7,200,000 $ 6,500,000 $ 9,200,000

Less estimated claims ……………………… 5,040,000 4,550,000 6,440,000

Underwriting income ………………………… $ 2,160,000 $ 1,950,000 $ 2,760,000

Administrative activities:*

New policy processing ………………… $ 240,000 $ 232,000 $ 656,000

b. Workers’

Auto Comp. Homeowners

Underwriting income as a

percent of premium revenue ……… 30.0% 30.0% 30.0%

E10–30, Concluded

d. All three insurance lines have the same percentage of underwriting income to

premium revenue (30%). The differences among the insurance lines are in the

way they consume administrative activities. For example, the Homeowners

PROBLEMS

P10–1

Product Costs Period Costs

Direct Direct Factory

Materials Labor Overhead Selling Administrative

Cost Cost Cost Cost Expense Expense

a. X

b. X

c. X

k. X

l. X

m. X

n. X

o. X

P10–2

1. Schedule of manufacturing costs incurred during June:

Direct Direct Factory

Job Materials Labor Overhead Total

No. 6001 $ 9,400 $ 8,800 $ 3,600 $ 21,800

2. Schedule of cost of jobs finished during June:

Direct Direct Factory

Job Materials Labor Overhead Total

No. 6001 $ 9,400 $ 8,800 $3,600 $ 21,800

3. Schedule of cost of jobs sold during June*:

Job

No. 6001 …………………………..……… $ 21,800

P10–2, Concluded

4. Schedule of completed jobs on hand, June 30, 20Y4*:

Direct Direct Factory

Job Materials Labor Overhead Total

Finished Goods, June 30

(Job 6005) ……………………. $16,400 $16,600 $6,600 $39,600

*This schedule supports the finished goods account as of June 30, 20Y4.

5. Schedule of unfinished jobs*:

Direct Direct Factory

Job Materials Labor Overhead Total

No. 6004 …………………………. $25,800 $21,840 $15,000 $62,640

6. Sales ……………………………… $110,000*

Cost of goods sold …………. 69,540

321

P10–3

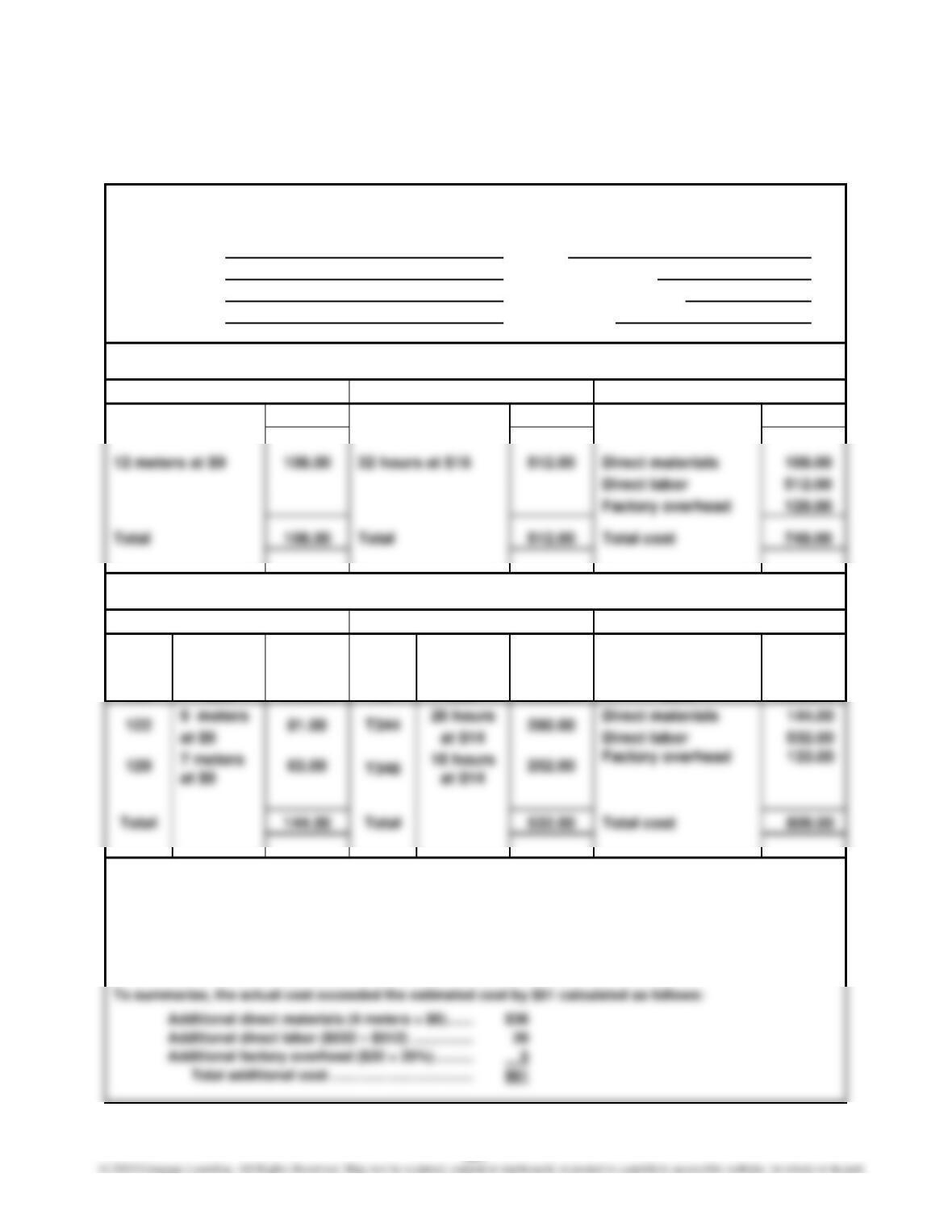

1. and 2.

JOB ORDER COST SHEET

Customer Millard Schmidt Date February 14, 20Y1

Address 315 White Oak Drive Date wanted March 15, 20Y1

Columbus, GA Date completed March 9, 20Y1

Item Reupholster couch and chair Job. No. 02–019

ESTIMATE

Direct Materials

Direct Labor

Summary

Amount

Amount

Amount

Direct materials

Direct labor

Factory overhead

ACTUAL

Direct Materials

Direct Labor

Summary

Mat.

Req.

No.

Descrip-

tion

Amount

Time

Ticket

No.

Descrip-

tion

Amount

Item

Amount

at $9

Total cost

Comments:

The direct materials cost exceeded the estimate by $36 because 4 meters of materials were spoiled. The di-

rect labor cost exceeded the estimate by $20 because an additional 6 hours of labor were used by an inexpe-

rienced employee that worked for $14 per hour. The increased labor cost also caused an additional $5 ($20 ×

25%) of factory overhead to be allocated to the job.

P10–4

1. Supporting calculations:

Job No.

Quan-

tity

May 1

Work in

Process

Direct

Materials

Direct

Labor

Factory

Overhead

Total

Cost

Unit

Cost

Units

Sold

Cost of

Goods

Sold

No. 0521

100

$1,500

$ 5,000

$ 15,000

$ 18,000

$ 39,500

$395.00

80

$ 31,600

No. 0522

200

4,000

8,500

26,000

31,200

69,700

$348.50

160

55,760

No. 0523

100

3,500

8,000

9,600

21,100

0

0

No. 0524

7,500

30,000

62,500

No. 0525

90

5,600

17,500

21,000

44,100

$490.00

36,750

No. 0526

70

4,500

5,400

11,900

0

0

A. $34,600. Materials applied to production in May + indirect materials.

($32,100 + $2,500)

B. $5,500. From table above and problem.

C. $32,100. From table above.

2. May 31 balances:

Materials $14,400 ($9,000 + $40,000 – $34,600)

Work in Process $33,000* [$21,100 (Job 0523) + $11,900 (Job 0526)]

Finished Goods $39,190** ($215,800 – $176,610)

323

P10–5

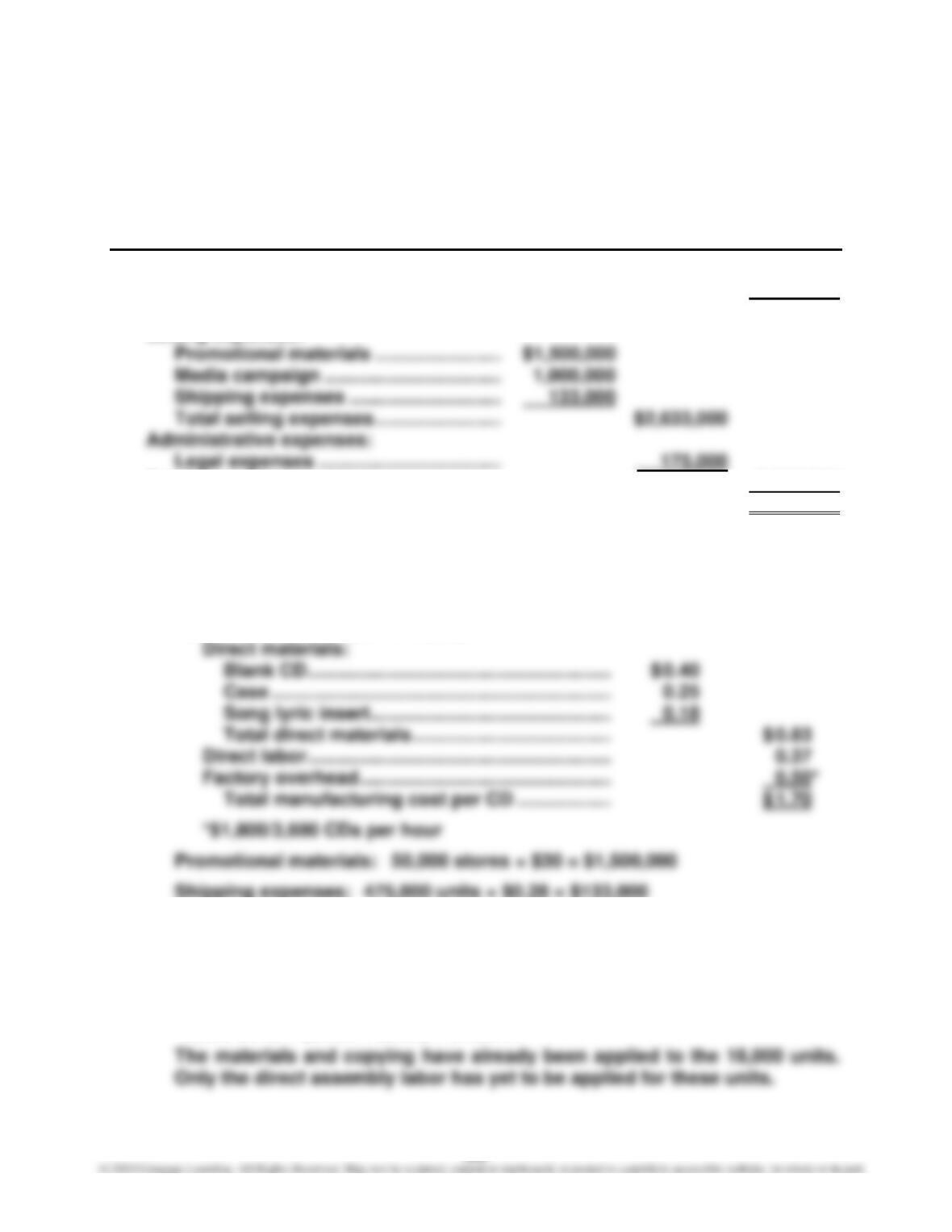

1.

R-TUNES INC.

Income Statement

For the Year Ended December 31, 20Y8

Sales …………………………..…………………….. $3,800,000

Cost of goods sold …………………………….. 807,500

Gross profit ……………………………………….. $2,992,500

Selling expenses:

Total operating expenses …………………… 2,808,000

Income from operations ……………………… $ 184,500

Supporting calculations:

Sales: 475,000 units × $8 = $3,800,000

Cost of goods sold: 475,000 units × $1.70 = $807,500

Manufacturing cost per unit (CD):

2. Finished Goods balance, December 31, 20Y8:

(500,000 units – 475,000 units) × $1.70 = $42,500

Work in Process, December 31, 20Y8:

18,000 units × ($0.83 + $0.50) = $23,940

324

CASES

Case 10–1

Although Beth may appear to have technically complied with company policy, her

computation of the cost of the lumber is unethical. The Statement of Ethical Con-

duct for Practitioners of Management Accounting and Financial Management

Case 10–2

The objectives of managerial accounting and financial accounting are different;

therefore, the vice president’s statement is very incomplete. In one sense, the

statement may be true at only very high levels in the organization. For example,

the division manager may be evaluated on the basis of financial accounting prof-

it. Thus, the divisional manager would be evaluated by central management in

nearly the same way that central management is evaluated by shareholders.

325

Case 10–3

1. Ashley’s bill has a number of points that should be considered. Some of the

points, with the appropriate argument, are identified below.

a. The trip back to the shop resulted in a $95 labor charge. Ashley should

argue that the whole hour should not be billed. The hour is the result of

b. The overtime premium should not have been charged to Ashley. What if

Ashley was the first appointment in the morning? If so, then there would

be no overtime premium. It’s only random misfortune that Ashley was

the last client of the day and therefore received the overtime premium.

Add to this the fact that the overtime would not have been necessary

without the trip back to the shop, and the conclusion is that Ashley

should not be directly charged for overtime. The overtime premium

should be part of Reboot’s overhead charged to all clients equally. Ash-

ley should be charged the overtime only if the decision for overtime was

caused by or required by Ashley.

Thus, the labor portion of the bill should only be $65 + $40 + $40 = $145.

There are other parts of the bill that should not be in dispute.

• The materials storage and handling charge is a normal charge of maintain-

ing a parts inventory for the benefit of clients that need parts.

326

Case 10–3, Concluded

2.

Cost Direct Materials Direct Labor Overhead

Circuit board X

Storage and handling X

Case 10–4

Two or three trends seem apparent. Starting with the most obvious:

a. There appears to be a strong “Friday effect.” The unit cost on Friday increas-

es dramatically, then falls on Monday. Apparently, the workforce is preparing

early for the weekend.

A number of further pieces of information should be requested.

a. First, it would be good to verify these trends with some other products. This

trend is probably not product-related but related generally to the day of the

week. This would mean that the trend should be apparent in the other prod-

ucts.

327

Case 10–4, Concluded

c. The Friday–Monday phenomenon is likely related to the workforce, but the

same cannot be said about the larger increasing trend over the four weeks. It

could be caused by any number of factors. A good first look would be to iso-

Case 10–5

1. The engineer is concerned that direct labor is not related to overhead con-

sumption because direct labor is a small part of the cost structure. Apparent-

ly, the company has replaced labor with expensive machine technology and

2. Since each direct labor hour now has $3,000 of factory overhead, small mis-

takes in the direct labor time estimates can have a large impact on the esti-

mated cost of a product. This is very critical. If the company underestimates

3. The engineer’s concern is valid. The company should consider replacing its

direct labor time activity base with one that more accurately reflects its pre-

sent resources. If the company is now highly automated, then machine hours

may be a much more reasonable activity base.

328

Case 10–6

Note to Instructors: Consider having the teams compete for the most examples.

Have half the class do the pizza restaurant and the other the copy shop, and

compare results.

Some examples that may be offered by the students are the following:

Copy and Graphics Shop

Direct Direct Selling

Cost Materials Labor Overhead Expense

Paper ……………………………………… X

Graphic designer wages ………….. X

Manager salary ……………………….. X

329

Case 10–6, Concluded

Pizza Restaurant

Direct Direct Selling

Cost Materials Labor Overhead Expense

Ingredients ……………………………. X

Cook wages ………………………….. X

Manager salary ……………………… X

Depreciation on equipment

and fixtures ……………………… X

Nondisposable plates, utensils,

cups …………………………..……. X

Repair costs …………………………. X

Property taxes ………………………. X

Store depreciation …………………. X

Cashier salary ……………………….. X

Beverage ………………………………. X

and overhead will not always be clear.

330

Case 10–7

Tyra Chastain’s claim that the inventory doesn’t cost the company anything is

likely not true. At the very minimum, inventory requires working capital to be

used. The financing cost associated with the working capital represents a cost to

high.

Gwen Willis should suggest that Tyra Chastain use just-in-time manufacturing

principles. The production process could be scheduled using pull techniques.

This would mean that the plant produces products only when there are orders.

Products would not be manufactured for inventory. In addition, the plant manager

should work to develop a reliable supply chain. One of the objectives of the sup-