CHAPTER 10

SOLUTIONS TO PROBLEMS: SET B

PROBLEM 10-1B

(a) SPEIER COMPANY

Flexible Monthly Manufacturing Overhead Budget

Assembly Department

For the Year 2017

Activity level

Direct labor hours

Variable costs

Indirect labor ($.30)

Indirect materials ($.20)

Fixed costs

Supervision

Depreciation

Insurance

18,000

$ 5,400

3,600

6,300

2,500

1,000

20,000

$ 6,000

4,000

6,300

2,500

1,000

22,000

$ 6,600

4,400

6,300

2,500

1,000

24,000

$ 7,200

4,800

6,300

2,500

1,000

PROBLEM 10-1B (Continued)

(b) SPEIER COMPANY

Manufacturing Overhead Budget Report (Flexible)

Assembly Department

For the Month Ended January 31, 2017

Difference

Total costs

Direct labor hours (DLH)

Variable costs

Indirect labor ($0.30)

Indirect materials ($0.20)

Fixed costs

Supervision*

Depreciation

Budget at

20,000 DLH

$ 6,000

4,000

6,300

2,500

Actual Costs

20,000 DLH

$ 6,200

3,600

6,300

2,500

Favorable F

Unfavorable U

$200 U

400 F

0 U

0 U

(c) Control over both variable and fixed costs was good.

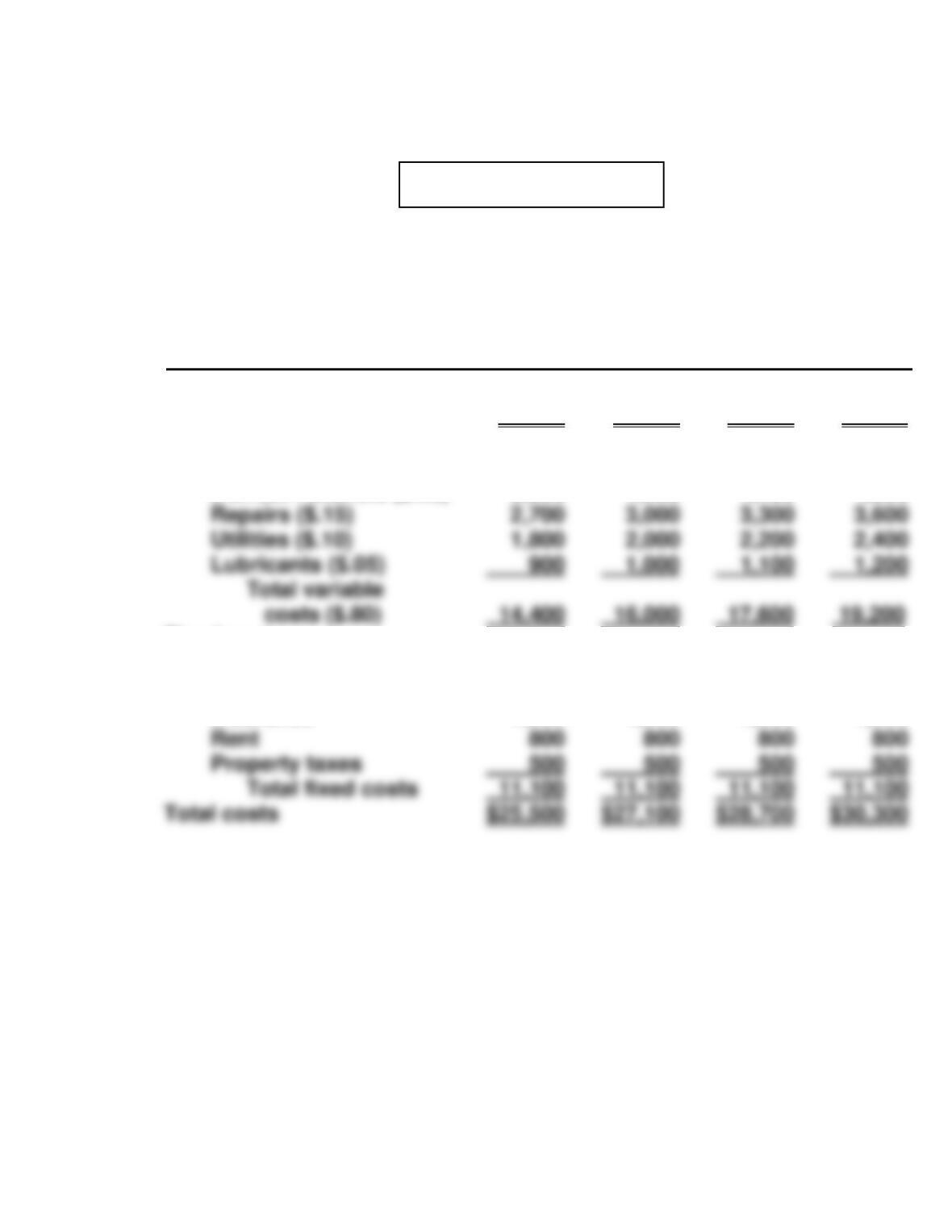

PROBLEM 10-2B

(a) GONZALEZ COMPANY

Flexible Monthly Manufacturing Overhead Budget

Assembly Department

For the Year 2017

Activity level

Direct labor hours

Variable costs

Indirect labor ($1.00)

Indirect materials ($.50)

Utilities ($.30)

Fixed costs

Supervision

Depreciation

22,500

$22,500

11,250

6,750

12,000

8,000

25,000

$25,000

12,500

7,500

12,000

8,000

27,500

$27,500

13,750

8,250

12,000

8,000

30,000

$30,000

15,000

9,000

12,000

8,000

PROBLEM 10-2B (Continued)

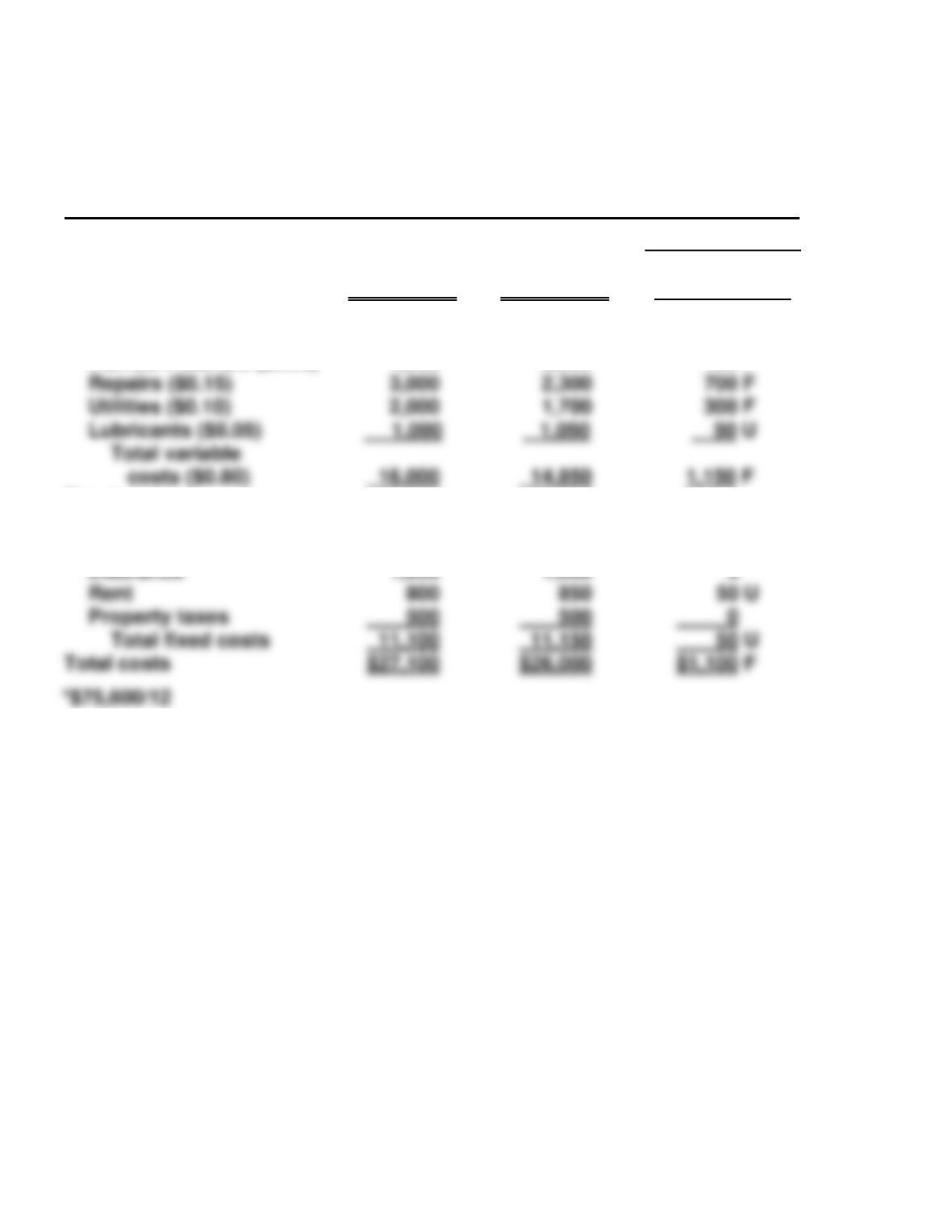

(b) GONZALEZ COMPANY

Assembly Department

Manufacturing Overhead Budget Report (Flexible)

For the Month Ended July 31, 2017

Difference

Total costs

Direct labor hours (DLH)

Variable costs

Indirect labor ($1.00)

Indirect materials ($0.50)

Fixed costs

Supervision

Depreciation

Budget at

27,500 DLH

$27,500

13,750

12,000

8,000

Actual Costs

27,500 DLH

$26,000

11,350

12,000

8,000

Favorable F

Unfavorable U

$1,500 F

2,400 F

0 F

0 F

(c) Based on the above budget report, control over costs was effective.

(d) The formula is fixed costs of $25,000 plus total variable costs of

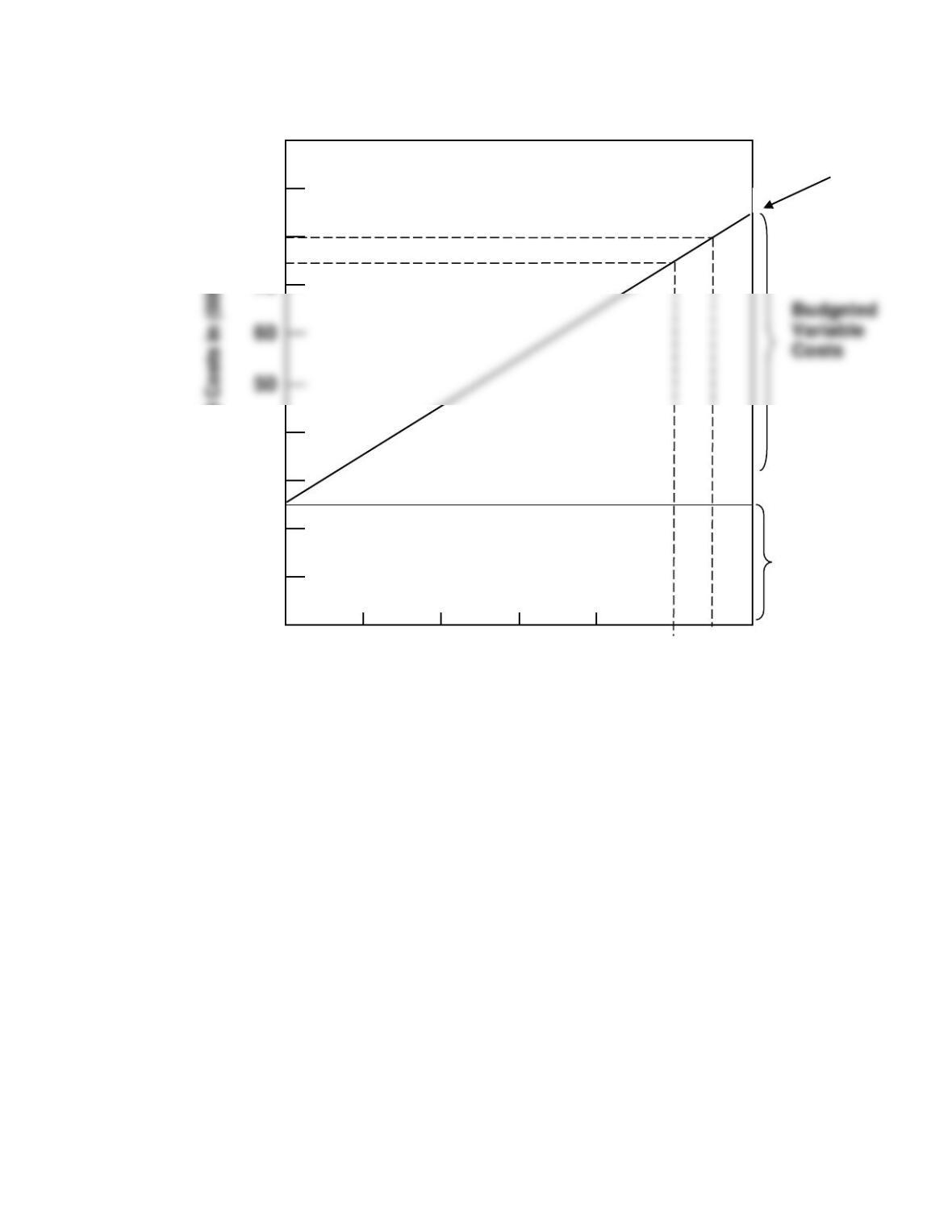

PROBLEM 10-2B (Continued)

(e)

$100

Total

Budgeted

Cost Line

Overhead Costs in (000)

90

80

70

40

30

20

Budgeted

Fixed Costs

10

0

5

10

15

20

25

30

Direct Labor Hours in (000)

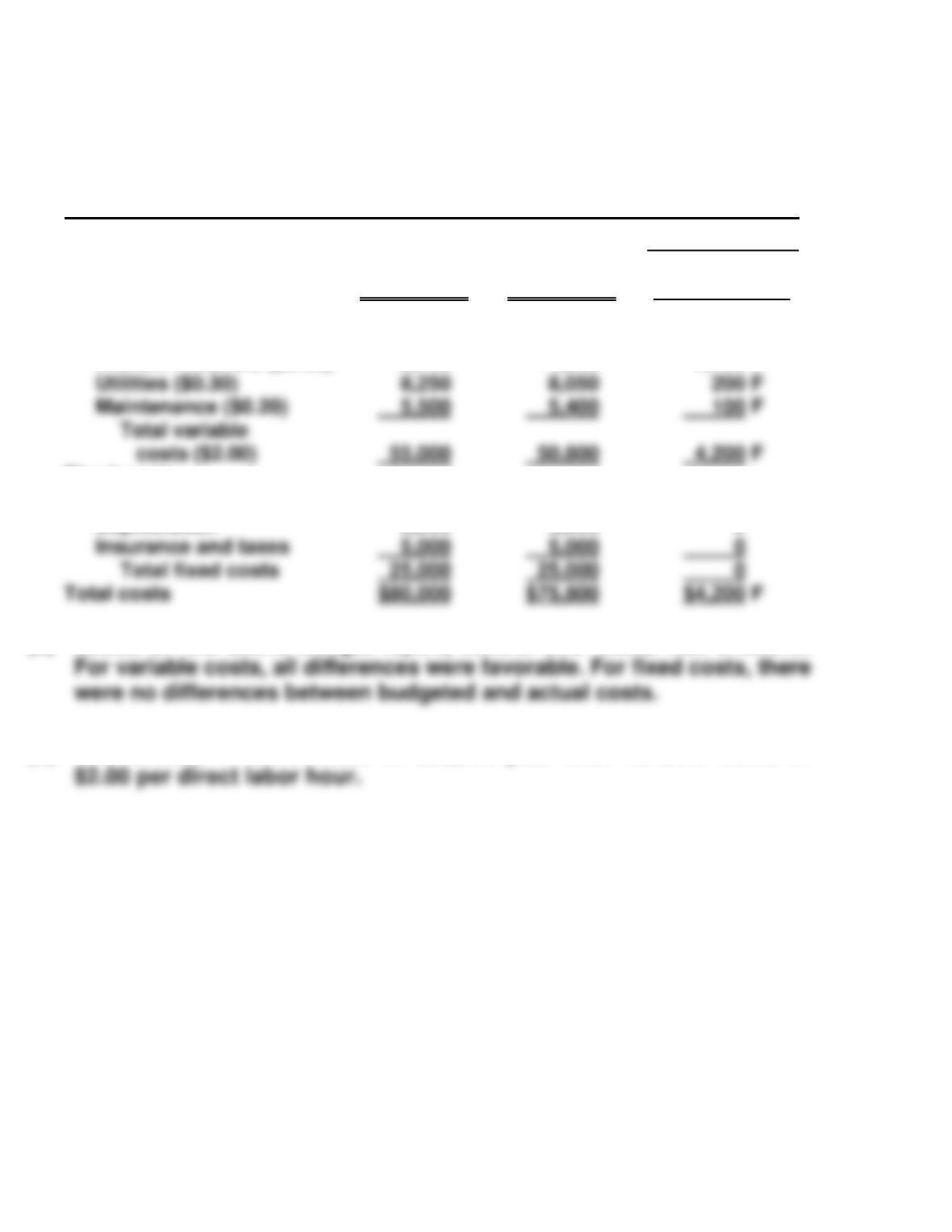

PROBLEM 10-3B

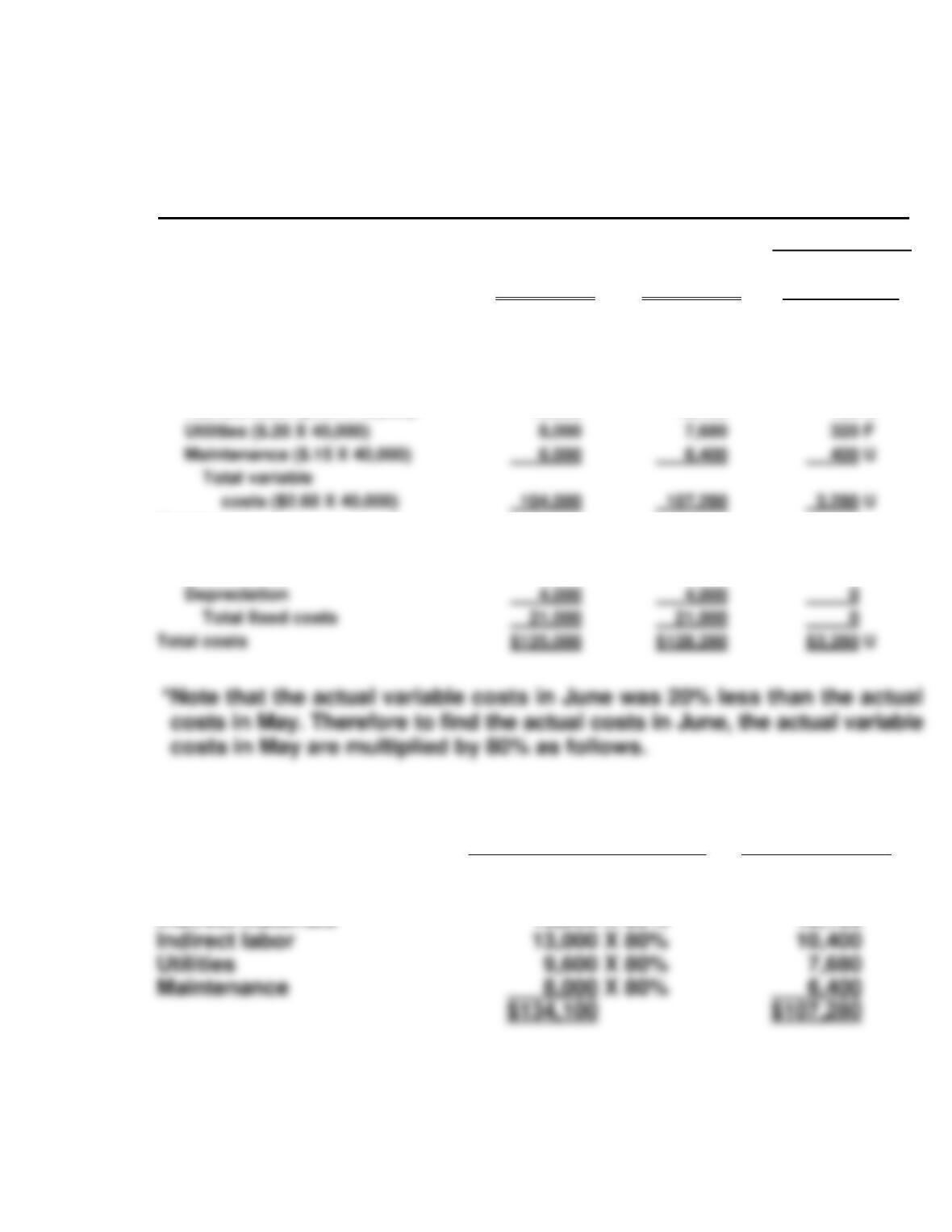

(a) The formula is fixed costs $21,000 plus total variable costs of $2.60 per

unit ($130,000 ÷ 50,000 units).

(b) HARDESTY COMPANY

Packaging Department

Budget Report (Flexible)

For the Month Ended May 31, 2017

Difference

Units

Variable costs*

Direct materials ($.80 X 55,000)

Direct labor ($.90 X 55,000)

Indirect materials ($.30 X 55,000)

Fixed costs

Rent

Supervision

Budget at

55,000 Units

$ 44,000

49,500

16,500

10,000

7,000

Actual Costs

55,000 Units

$ 41,000

47,300

15,200

10,000

7,000

Favorable F

Unfavorable U

$3,000 F

2,200 F

1,300 F

0 F

0 F

*Note that the per unit variable costs are computed by taking the budget

amount at 50,000 units and dividing it by 50,000. For example, direct

This report provides a better basis for evaluating performance because

the budget is based on the level of activity actually achieved.

PROBLEM 10-3B (Continued)

(c) HARDESTY COMPANY

Packaging Department

Budget Report (Flexible)

For the Month Ended June 30, 2017

Difference

Units

Variable costs

Direct materials ($.80 X 40,000)

Direct labor ($.90 X 40,000)

Indirect materials ($.30 X 40,000)

Indirect labor ($.25 X 40,000)

Fixed costs

Rent

Supervision

Budget at

40,000 Units

$ 32,000

36,000

12,000

10,000

10,000

7,000

Actual Costs

40,000 Units

$ 32,800*

37,840

12,160

10,400

10,000

7,000

Favorable F

Unfavorable U

$ 800 U

1,840 U

160 U

400 U

0 U

0 U

May

(actual)

June

(actual)

Direct materials

Direct labor

Indirect materials

$ 41,000 X 80%

47,300 X 80%

15,200 X 80%

=

$ 32,800

37,840

12,160

PROBLEM 10-4B

(a) GUZMAN INC.

Home Appliance Division

Responsibility Report

For the Year Ended December 31, 2017

Difference

Budget

Actual

Favorable F

Unfavorable U

Sales

Variable costs

Cost of goods sold

Controllable fixed costs

Cost of goods sold

$2,400,000

1,200,000

200,000

$2,310,000

1,258,000

192,000

$90,000 U

58,000 U

8,000 F

(b) The manager did not effectively control revenues and costs. Contribution

margin was $140,000 unfavorable and controllable margin was $135,000

unfavorable. Contribution margin was unfavorable primarily because

(c) Two costs are excluded from the report: (1) noncontrollable fixed costs

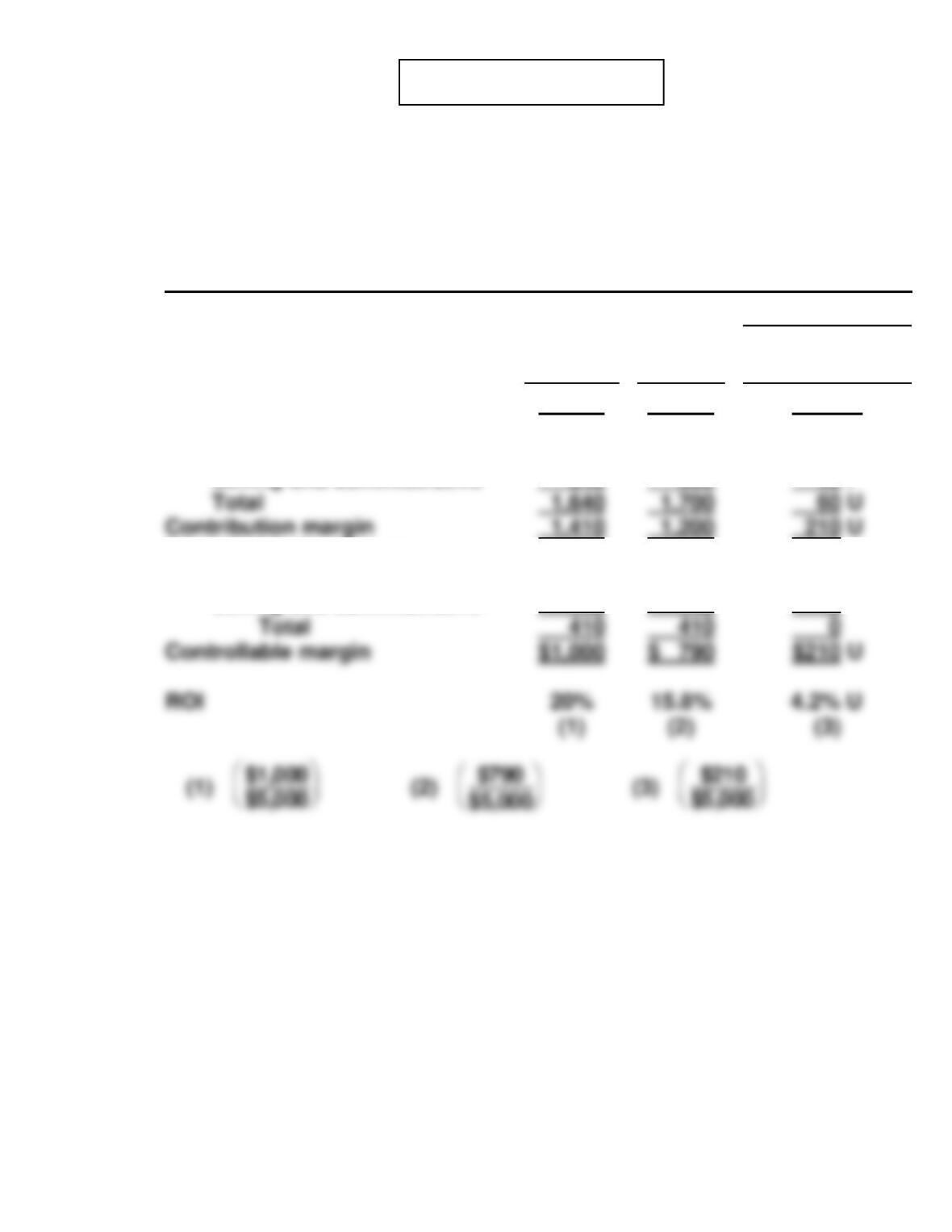

PROBLEM 10-5B

(a) STRAUSS COMPANY

Lawnmower Division

Responsibility Performance Report

For the Year Ended December 31, 2017

(in thousands of dollars)

Difference

Budget

Actual

Favorable F

Unfavorable U

Sales

Variable costs

Cost of goods sold

Selling and administrative

Controllable fixed costs

Cost of goods sold

Selling and administrative

$3,050

1,300

340

270

140

$2,900

1,400

300

270

140

$150 U

100 U

40 F

0 U

0 U

PROBLEM 10-5B (Continued)

(b) The performance of the manager of the Lawnmower Division was below

budget expectations for the year. The item that top management would

likely investigate first is the reason why sales were $150,000 below

(c) 1. [$790,000 + ($1,400,000 X 20%)] ÷ $5,000,000 = 21.4%.

PROBLEM 10-6B

(a) No. 1

To Cutting Department Manager—Phoenix Division Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

Indirect labor

Indirect materials

$ 90,000

61,000

$ 95,000

62,700

$ 5,000 U

1,700 U

No. 2

To Division Production Manager—Phoenix Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

Phoenix Division

Departments:

Cutting

$ 70,000

224,000

$ 73,100

241,300

$ 3,100 U

17,300 U

No. 3

To Vice-President—Production Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

V-P Production

Divisions:

Phoenix

$ 70,000

716,000

$ 72,000

754,400

$ 2,000 U

38,400 U

PROBLEM 10-6B (Continued)

No. 4

To President Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

President

Vice-Presidents:

Production

$ 91,300

2,251,000

$ 94,200

2,310,400

$ 2,900 U

59,400 U

(b) 1. Within the Phoenix division the rankings of the department managers

were: (1) Finishing, (2) Shaping, and (3) Cutting. If the rankings

3. Rankings in terms of dollars may be somewhat misleading in this

case because of the substantial difference between the production

*PROBLEM 10-7B

2. Residual Income = Controllable Margin – (Minimum Rate of

Return X Average Operating Assets)

(b) The management of Washington Enterprises would clearly have

accepted the investment opportunity it had in 2017 if residual income

had been used as the performance measure because an increase in