10

Fundamentals of Cost Management

Solutions to Review Questions

10–1.

Activity-based costing provides management with detailed costing information about

10–2.

Activity-based management can be implemented without an activity-based costing

10–3.

Value-added activities add value to the product or service whereas nonvalue-added

10–4.

Customers affect costs by the way they interact with the company and place demands

10–5.

10–6.

Resources supplied represent the capacity of the organization. They are the resources

10–7.

Capacity costs, generally included in the fixed overhead allocation, affect reported

product costs. Managers use reported costs to make decisions such as what price to

10–8.

The cost of excess capacity should be assigned to products or customers if the reason

10–9.

Quality affects cost in two major ways. Conformance costs are those that the firm incurs

in order to ensure the product or service meets required quality levels. Examples

10–10.

The four categories of a cost of quality system are:

1. Prevention: Costs to ensure good quality (product design, training).

Solutions to Critical Analysis and Discussion Questions

10–11.

Answers will vary.

10–12.

10–13.

10–14.

Answers will vary.

10–15.

10–16.

10–17.

10–18.

Two important factors managers need to consider are what competitors will do and how

10–19.

There is an opportunity cost associated with idle capacity. Knowing that capacity is not

10–20.

10–21.

Answers will vary. The answer depends on why excess demand exists and what

10–22.

Answers will vary but should include reasons why the elements are not important. For

instance, when purchasing a low-cost item, like paint to touch up minor scratches,

10–23.

Answers will vary. One example follows. The quality-based view would encourage

continuous improvement of the production process and might offer incentives (i.e. cash

Solutions to Exercises

10–24. (10 min.) Activity-Based Cost Management in a College.

10–25. (10 min.) Activity-Based Cost Management for a Hotel.

1. b. Improves efficiency. Having guests check in on-line means less work for the

10–26. (10 min.) Cost Hierarchy for a Not-for-Profit.

10–27. (20 min.) Driver Identification.

a. Number of calls to new commercial customers; records kept by sales reps.

10–28. (20 min.) Driver Identification.

10–29. (20 min.) Activity-Based Costing of Customers: Marvin’s Kitchen Supply.

a. Delivery cost based on order value:

Customer

Order

Value

Delivery Charge

(@10%)

City Diner …………………………………………

Le Chien Chaud ……………………………..

b. Delivery cost based on activity-based costing:

Cost driver rates:

Activity

Cost Driver

Cost ÷

Driver Volume =

Rate

Cost of delivery:

City Diner

Le Chien Chaud

Activity

Units of Cost

Driver

Cost

Units of Cost

Driver

Cost

Processing order ………………

52 orders

$780a

110 orders

$1,650

Loading truck ……………………

600 items

Delivering merchandise ……..

Processing invoice …………….

12 invoices

$8,580

10–30. (30 min.) Activity-Based Costing of Customers: Rock Solid Bank & Trust.

a.

Sales revenue ……………….

Costs:

Total costs…………………….

Operating profit ……………..

$2,625,000

b.

Customer A

Customer B

Deposit …………………………..

$6,000

$6,000

Sales revenue …………………

Interest on deposits ………….

Operating costs ……………….

10–30. (continued)

c.

Activity

Cost Driver

Cost

Driver Volume

Rate

Use ATM

Number of

uses

$1,500,000

÷

2,000,000

= $0.75 per use

Number of

visits

transaction

Number of

transactions

÷

transaction

Customer A

Customer B

Activity

Units of

Cost

Driver

Units of

Cost

Driver

Sales revenue …………………………………………….

$312.00

$312.00

Interest on deposit ………………………………………

30.00

30.00

$282.00

$282.00

Operating costs:

1,500

$489.75

Customer profit …………………………………………..

10–31. (15 min.) Activity-Based Costing of Customers: Rock Solid Bank & Trust.

10–32. (15 min.) Activity-Based Costing of Customers—Ethical Issues: Red’s

Lumber.

a. Red could use the information to offer “discounts” for weekday orders, which is

equivalent to a premium for weekend orders. Before Red makes any changes, he

10–33. (15 min.) Activity-Based Costing of Customers—Ethical Issues: Central

State College.

a. Possible allocation bases include number of students, student hours in the lab,

b. This is a difficult question and answers will vary. The dean views the training

10–34. (15 min.) Activity-Based Costing of Suppliers: Hult Games.

This can be answered using the format of Exhibit 10.9. First compute the cost of

a late delivery.

Number of cartons delivered late

(100,000 x 25% + 60,000 x 10%)

31,000

Cost of late deliveries …………………….

Cost of late delivery per carton ………. per ton

Average purchase price per carton …………..

Additional cost of late delivery per carton …..

Probability of late delivery ……………………….

Expected cost of late delivery per carton ……

Effective cost per carton ………………………….

10–35. (10 min.) Activity-Based Costing of Suppliers: Hult Games.

10–36. (20 min.) Activity-Based Costing of Suppliers: Kinnear Plastics.

The approach to this problem is to determine how much it costs to purchase a

ton of “good” plastic. The effective price is the quoted price divided by the

percentage of good tons that can be expected:

10–37. (10 min.) Activity-Based Costing of Suppliers: Kinnear Plastics.

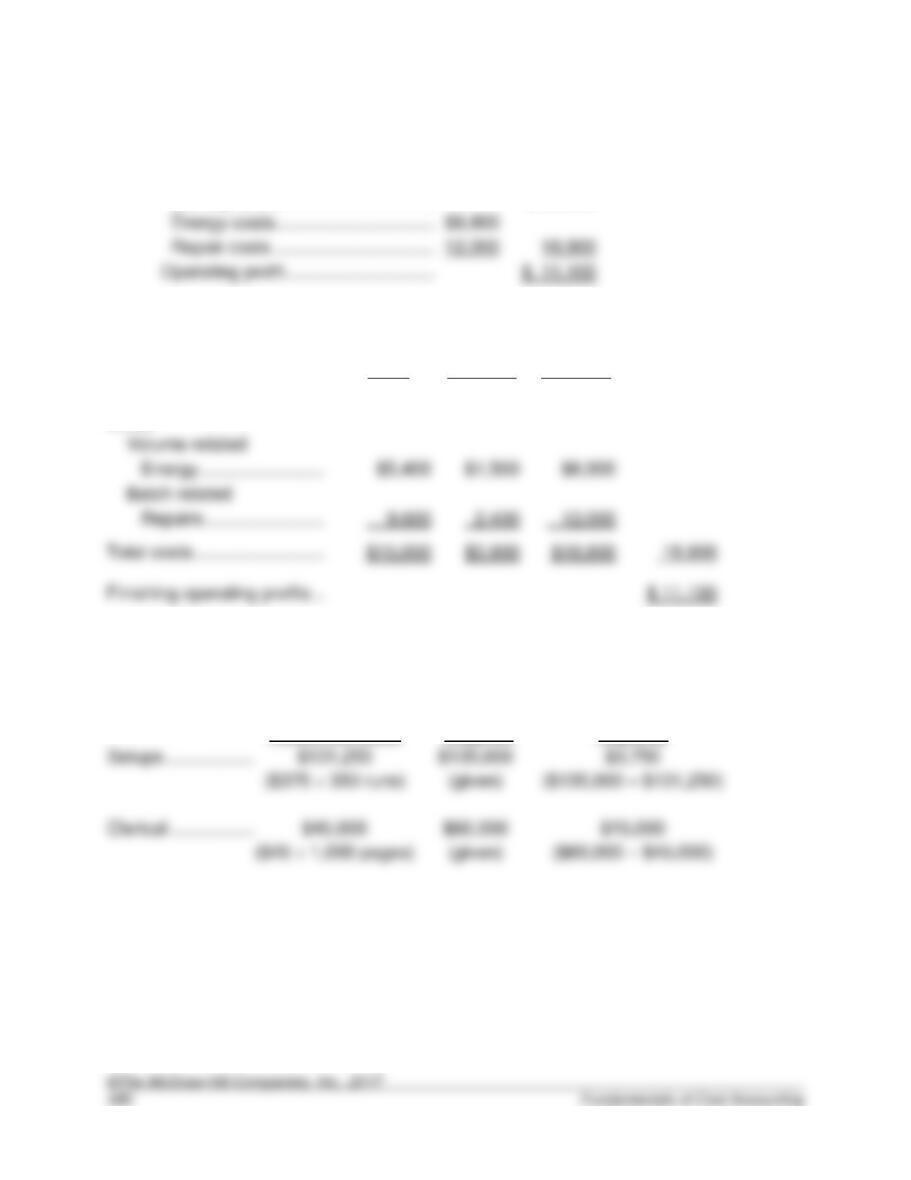

10–38. (15 min.) Resources Used versus Resources Supplied: Tri-State Mill.

Resources Used

Resources

Supplied

Unused Resource

Capacity

Energy ……………………………………………………….

Repairs ………………………………………………………

10–39. (10 min.) Resources Used versus Resources Supplied: Tri-State Mill.

a.

Finishing sales ……………………………..

$ 30,000

b.

Resources

Used

Unused

Resource

Capacity

Resources

Supplied

Finishing sales ……………….

$ 30,000

Costs

Repairs ……………………

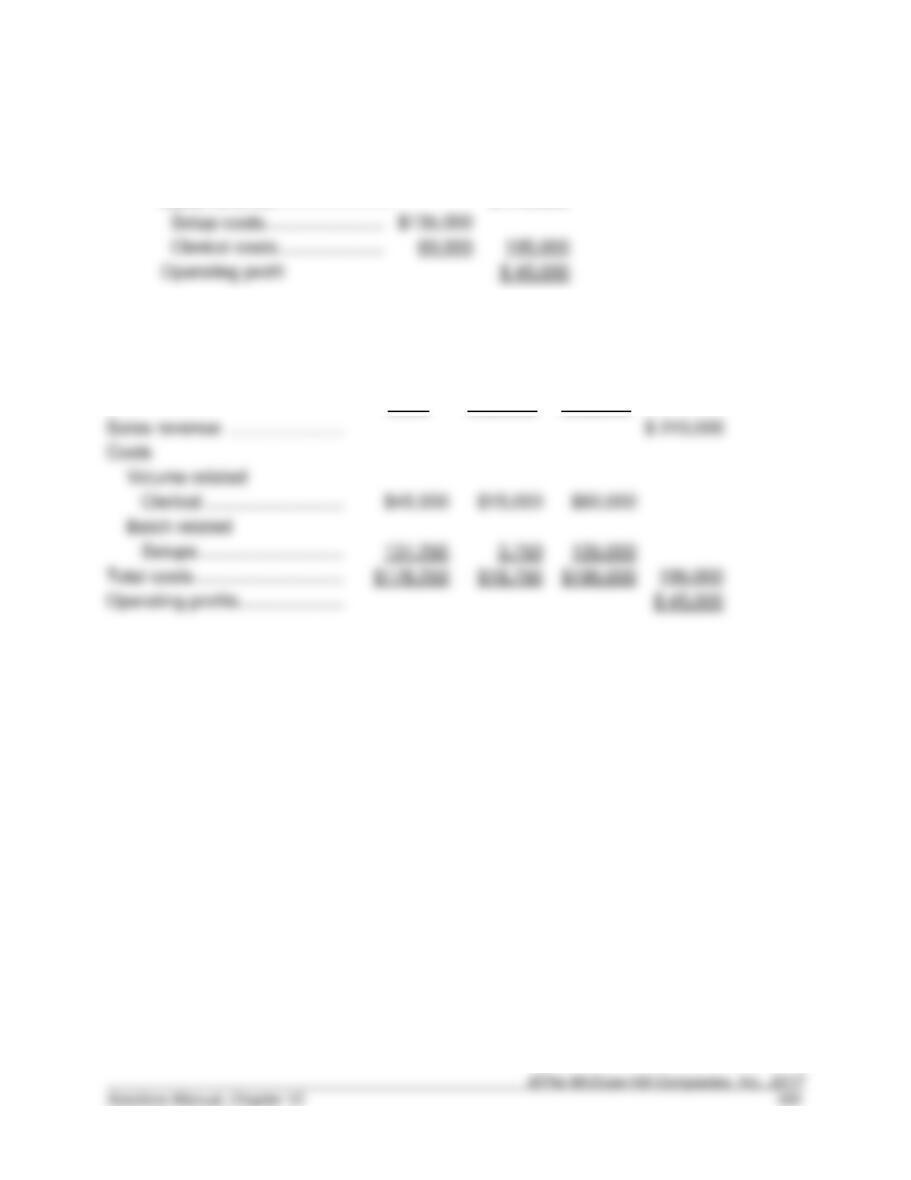

10–40. (15 min.) Resources Used versus Resources Supplied: Conlon

Enterprises.

Resources Used

Resources

Supplied

Unused Resource

Capacity

$60,000

10–41. (10 min.) Resources Used versus Resources Supplied: Conlon Enterprises.

a.

Sales revenue …………………….

$ 240,000

b.

Resources

Used

Unused

Resource

Capacity

Resources

Supplied

Sales revenue …………………..

Clerical ……………………….

$176,250

10–42. (40 min.) Resources Used versus Resources Supplied: Carbon Company.

a.

Resources

Supplieda

Unused Resource

Capacitya

Resources Used

÷ Cost Driver Volume

= Cost Driver Rate

= Cost Driver Rate

÷ Cost Driver Volume

Materials ……………………………………………………

$98,000

$2,000

$96,000

Purchasing …………………………………………………

÷ Cost Driver Volume

= Cost Driver Rate

$21,000

$1,800

÷ Cost Driver Volume

= Cost Driver Rate

÷ Cost Driver Volume

$19,200

÷ 80 orders

= $240 per order

10–43. (20 min.) Assigning Cost of Capacity: Mimi’s Fixtures.

a. Because the plant was purchased with excess capacity for future growth, current

production should not be charged with excess capacity. Therefore, the cost

c. If the minimum plant size was 30,000 tiles, then the capacity is for the customers’

benefit and the costing system should charge the cost of excess capacity to

10–44. (20 min.) Assigning Cost of Capacity: Curt’s Castings.

a. Because the plant was purchased for the benefit of Curt, current production

should not be charged with excess capacity. Therefore, the cost system should

report a cost of $8 per ton computed as follows:

10–45. (15 min.) Costs of Quality: Waterloo Company.

Customer complaints

EF

Materials inspection

Process inspection

Rework

Testing equipment

10–46. (20 min.) Costs of Quality: Domingo Corporation.

a. Prevention: Process inspection, quality training, preventive maintenance,

materials inspection.

b.

March

April

Prevention

$41,450 ÷ $490,000 …………………………………

8.5%

$29,180 ÷ $440,000 …………………………………

6.6%

Appraisal

$16,400 ÷ $490,000 …………………………………

$19,400 ÷ $440,000 …………………………………

Internal failure

$20,430 ÷ $440,000 …………………………………

External failure

$7,100 ÷ $490,000 …………………………………..

$8,200 ÷ $440,000 …………………………………..

10–47. (30 min.) Trading-Off Costs of Quality: Domingo Corporation.

Domingo Corporation

Cost of Quality Report

March

%

April

%

Sales revenue …………………………………………….

$490,000

$440,000

Prevention costs:

Process inspection …………………………………..

$ 1,650

$ 1,880

Quality training …………………………………………

19,800

13,000

Materials inspection ………………………………….

Total prevention costs ………………………………….

$ 41,450

$ 29,180

Appraisal costs:

Testing equipment …………………………..………

$ 7,000

Total appraisal costs ……………………………………

$ 16,400

$ 19,400

Internal failure costs:

Scrap ……………………………………………………..

$ 1,850

$ 1,930

Total internal failure costs …………………………….

$ 18,850

$ 20,430

External failure costs:

Warranty repairs ………………………………………

$ 4,800

Customer complaints ………………………………..

Total external failure costs: ………………………….

$ 8,200

Total Costs of Quality …………………………………..

10–48. (20 min.) Costs of Quality: Nuke-It-Now.

a. Prevention: Redesign process, training on equipment, preventative maintenance.

b.

Year 1

Year 2

Prevention

$393,000 ÷ $3,500,000 …………………………….

11.2%

Appraisal

$190,000 ÷ $3,500,000 …………………………….

Internal failure

$109,000 ÷ $3,500,000 …………………………….

External failure

$632,000 ÷ $3,500,000 …………………………….

10–49. (30 min.) Trading-off Costs of Quality: Nuke-It-Now.

Nuke-It-Now Corporation

Cost of Quality Report

Year 1

%

Year 2

%

Sales revenue …………………………………………….

$3,500,000

$3,800,000

Prevention:

Redesign process …………………………………….

$ 29,000

$ 37,000

Preventive maintenance …………………………...

Total prevention costs ………………………………….

$ 393,000

11.2%

$ 399,000

Appraisal:

Final inspection ………………………………………..

$ 190,000

$ 198,000

Internal failure:

Rework …………………………………………………..

Total internal failure costs …………………………….

$ 109,000

$ 139,000

External failure:

Warranty claims …………………………..…………..

$ 129,000

$ 176,000

Contract cancellations ………………………………

Total external failure costs …………………………...

$ 632,000

18.1

$ 506,000

10–50. (15 min.) Cost of Quality—Environmental Issues.

a. Criminal penalties for illegal dumping. (EF)

10–51. (15 min.) Cost of Quality—Financial Reporting Issues.

a. Extra work done by external auditors to complete the audit because new

Solutions to Problems

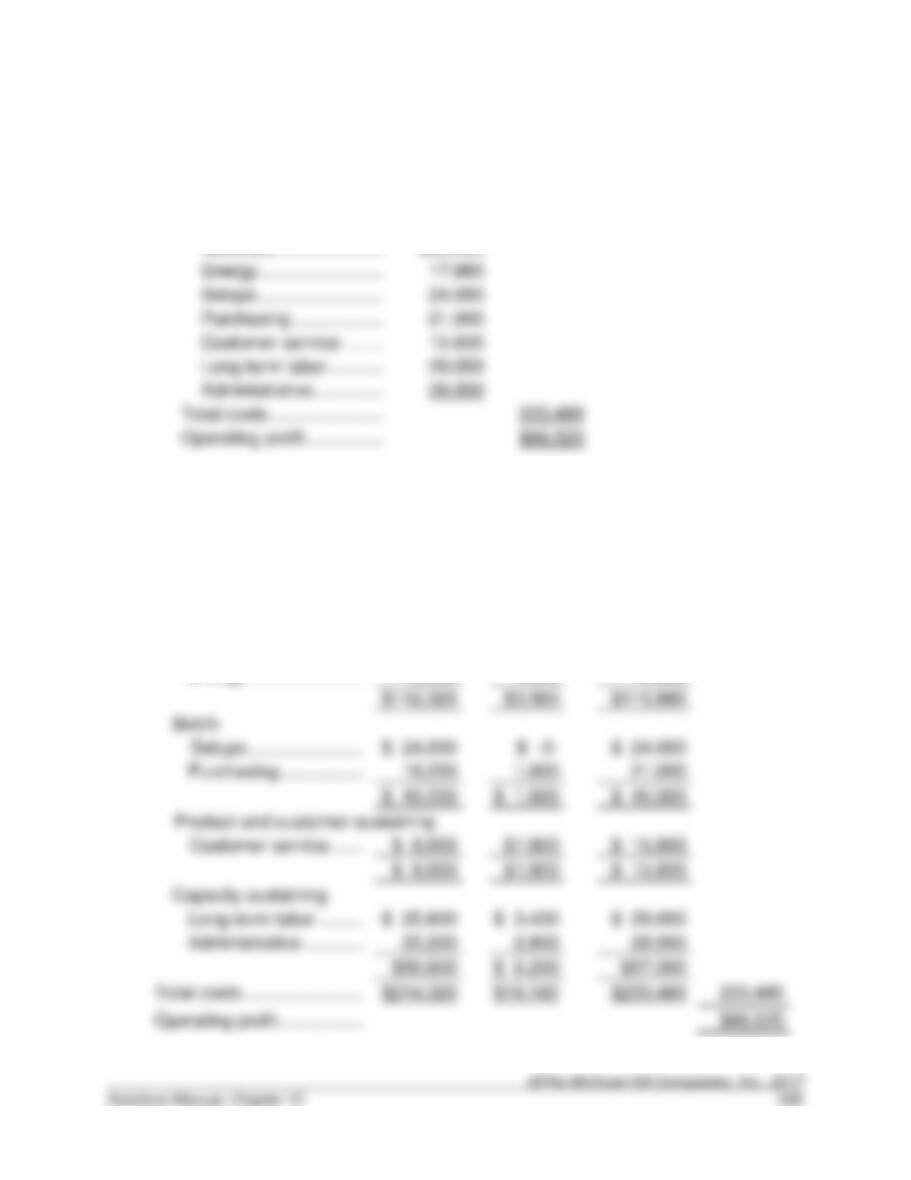

10–52. (50 min.) Activity-Based Reporting and Capacity: Carbon Company.

a.

Sales revenue ……………..

$300,000

Total costs …………………..

b.

Sales revenue

$300,000

Resources

Used

Unused

Resource

Capacity

Resources

Supplied

Costs

Unit

Materials ……………………………………………..

$96,000

$ 2,000

$98,000

Energy ………………………………………………..

16,320

1,560

17,880

$112,320

$3,560

$115,880

Batch

Setups ………………………………………………..

$ 24,000

$ 24,000

Purchasing …………………………………………..

$ 43,200

$ 45,000

Customer service ………………………………….

$ 15,600

$ 15,600

Capacity sustaining

Long-term labor ……………………………………

$ 25,600

Administrative ………………………………………

Operating profit …………………………………………..

10–52. (continued)

c. A traditional income statement shows management resources supplied, but gives

no indication of the resources used and unused resource capacity. Management

10–53. (50 min.) Activity-Based Reporting: Allcott Computer Services.

a.

Sales revenue ……………………………………

$1,350,000

Marketing ………………………………………

$120,000

Energy …………………………………………..

Administrative …………………………………

Total costs …………………………………………

Operating profit ………………………………….

b.

Sales revenue

$1,350,000

Resources

Used

Unused

Resource

Capacity

Resources

Supplied

Costs

Unit

Energy …………………………..…………………….

$80,000

$5,500

$ 85,500

Short-term labor ……………………………………

$ 395,500

$ 4,500

$ 42,000

$ 42,000

Marketing …………………………..………………..

$ 120,000

$ 17,000

$ 174,000

Capacity sustaining

Depreciation …………………………………………

$ 2,500

$ 89,500

Long-term labor …………………………………….

$ 21,500

Operating profit …………………………………………..

10–53. (continued)

c. A traditional income statement shows management resources supplied, but gives

no indication of the resources used and unused resource capacity. Management

10–54. (50 min.) Customer Profitability: SkiBlu, Ltd.

a.

Customer Costs

Gold

Silver

Number of customers ………

30,000

70,000

Number of customer representatives

30

7

Total gross margin ($660 x 30,000; $210 x 70,000)

customer representative)

margin)

Excess of gross margin over customer cost

10–55. (50 min.) Customer Profitability: Carmel Company.

a.

Customer Costs

Titanium

Platinum

Number of customers ……………………………………………

6,000

24,000

Number of customer representatives ………………………

30

12

Average gross margin per customers………………………

Total gross margin ($1,500 x 6,000; $200 x 24,000) ….

customer representative) ……………………………………….

margin) ……………………………………………………………….

Promotion costs (70% titanium; 30% platinum) …………

10–56. (30 min.) Activity-Based Costing of Suppliers: JFI Foods.

The effective price is the price to buy a “good” ton of feedstock. This can be

computed as the bid price divided by the yield (the ratio of good output to total

input).

Rex

Materials

Red Oak

Chemicals

Tons purchased ………………………..

Good output …………………………….

Yield (good output ÷ purchased) ….

Quoted price …………………………….

Effective cost per ton (a) ……………. (a)

10–57. (20 min.) Activity-Based Costing of Suppliers: JFI Foods.

a. $156.52. If Red Oak has an exclusive contract, the price per ton, adjusted for

10–58. (50 min.) Activity-Based Reporting: Leidenheimer Corporation.

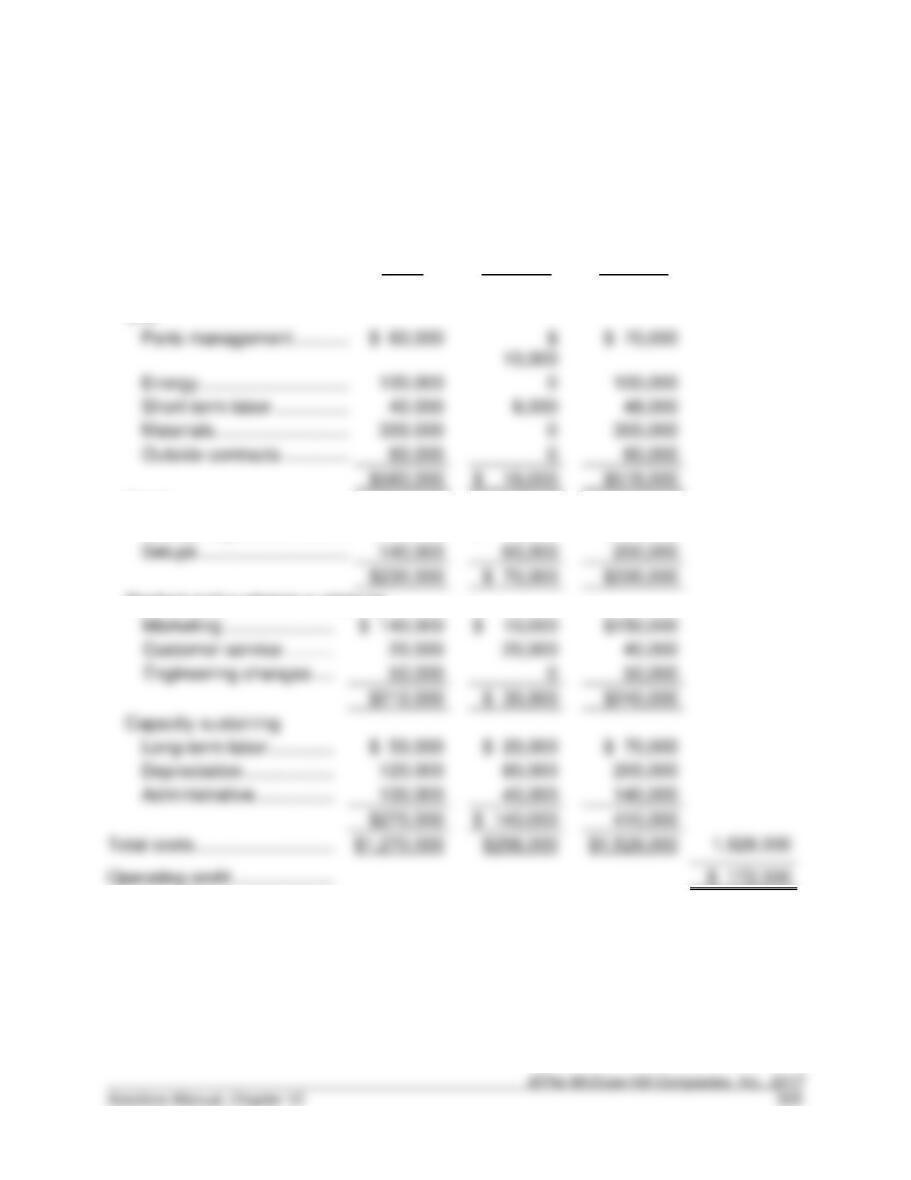

a.

Sales revenue …………………………………………….

$1,700,000

Quality inspections ………………………………………

100,000

Setups ……………………………………………………….

Marketing …………………………………………………..

150,000

Engineering changes …………………………………..

Total costs ………………………………………………….

10-58. (continued)

b.

Sales revenue

$1,700,000

Resources

Used

Unused

Resource

Capacity

Resources

Supplied

Costs

Unit

40,000

Materials ………………………………………………

60,000

$ 18,000

$578,000

Batch

Quality inspections ………………………………..

$ 90,000

$ 10,000

$100,000

60,000

Product and customer sustaining

Marketing …………………………………………….

Customer service ………………………………….

Engineering changes …………………………….

$210,000

$ 30,000

Capacity sustaining

Long-term labor …………………………………….

$ 50,000

$ 20,000

$ 70,000

80,000

40,000

$270,000

$ 140,000

Operating profit …………………………………………..

10-58. (continued)

c. A traditional income statement shows management resources supplied, but gives

no indication of the resources used and unused resource capacity. Management

has no way of knowing the amount of unused resource capacity or the cost of

10–59. (30 min.) Assigning Capacity Costs: Cathy and Tom’s Specialty Ice Cream

Company.

Cathy and Tom’s Specialty Ice Cream Company illustrates in a very simple way the

issues of cost system design when costing excess capacity. Although the problem

There are two possible approaches to costing the ice cream:

1. Cost at capacity:

Overhead rate =

($27,000 ÷ 18,000 gallons) =

$1.50/gallon

Product cost =

$2.50/gallon

2. Cost at demand:

Overhead rate =

($27,000 ÷ 13,500 gallons) =

$2.00/gallon

Product cost =

$3.00/gallon

How do you choose between the two? Why did Cathy and Tom buy a plant with a

capacity of 18,000 gallons? Possible reasons include:

$3.00/gallon

$4.00/gallon

$1.50/gallon

$2.50/gallon

10–60. (30 min.) Assigning Capacity Costs—Seasonality: Cathy and Tom’s

Specialty Ice Cream.

With seasonal demand fluctuations, the reason for the excess capacity is for the benefit

of the two customers (Cathy and Tom need all the capacity in the summer). The issue is

how to treat the excess capacity costs. The capacity costs in each season are $13,500

(= $27,000 ÷ 2 seasons). Two approaches to costing are:

1. Excess capacity costs assigned to season in which it is incurred, then to products

in that season. Thus,

2. Excess capacity costs assigned to the season requiring it, then to products

produced in that season. Thus,

Winter:

Overhead rate =

($13,500 50%) ÷ 4,500

gallons) =

$1.50/gallon

$2.50/gallon

$2.25/gallon

$3.25/gallon

10–61. (30 min.) Assigning Capacity Costs—Seasonality: Cathy and Tom’s

Specialty Ice Cream.

With seasonal demand fluctuations, the reason for the excess capacity is for the benefit

of the two customers (Cathy and Tom need all the capacity in the summer). The issue is

how to treat the excess capacity costs. The capacity costs in each season are $9,000 (=

$27,000 ÷ 3 seasons).

The capacity costs and capacity in each season is:

Capacity Costs

Winter

Fall/Spring

Summer

Total ………………………………………………………

$9,000

$9,000

$9,000

Unused………………………………………………….

(4,500)

(2,250)

–0–

Charge for unused ………………………………….

$4,500

$7,875

1.00

10–62. (30 min.) Assigning Capacity Costs: Mercia Chocolates.

Mercia Chocolates illustrates in a very simple way the issues of cost system design

There are two customers who demand a total of 60,000 packages, which is 80% of

plant capacity. The cost of the capacity (all assumed fixed) is $540,000.

There are two possible approaches to costing the chocolate:

How do you choose between the two? Why did Mercia buy a plant with a capacity of

90,000 packages? Possible reasons include:

(1) They hope to grow the market, i.e., for future expansion.

10–63. (30 min.) Assigning Capacity Costs—Seasonality: Mercia Chocolates.

With seasonal demand fluctuations, the reason for the excess capacity is for the benefit

1. Excess capacity costs assigned to season in which it is incurred, then to products

in that season. Thus,

Non-holiday:

Overhead rate =

$12.00/package

Holiday

Overhead rate =

$6.00/package

2. Excess capacity costs (= $540,000 x 33-1/3%, or $180,000) are assigned to the

season requiring it, then to products produced in that season. Thus,

Non-holiday:

Overhead rate =

($360,000 ÷ 30,000 packages) =

$12.00/package

Product cost =

$22.00/package

Holiday

Product cost =

$22.00/package

10–64. (30 min.) Quality Improvement: IPort Products.

a. There are two alternatives: continue with the current material or use the new

material. To determine the best alternative (considering only the financial

consequenses), compute profit under each alternative:

Current Material

New Material

Number of units sold ……………………………………………..

127,500

142,500

Price per unit ………………………………………………………..

$20

$20

Sales revenue ………………………………………………………

Variable cutting manufacturing costs (150,000 units):

Fixed manufacturing costs (cutting)…………………………..

Variable sewing costs (@$3) …………………………………..

382,500

427,500

Fixed sewing costs ………………………………………………..

Inspection and testing ……………………………………………

Additional revenue ……………………………………….

($20 x 15,000 units)

Inspection savings ……………………………………….

Less additional material cost in cutting ……………

($2.25 x 150,000)

Less additional variable cost in sewing …………..

($3 x 15,000)

10–65. (30 min.) Quality Improvement: Metallic, Inc.

a. There are two alternatives: continue with the current material or use the new

material. To determine the best alternative (considering only the financial

consequenses), compute profit under each alternative:

Current Material

New Material

Number of units sold ……………………………………………..

8,500

9,500

Price per unit ………………………………………………………..

$500

$500

Sales revenue ………………………………………………………

Variable bending manufacturing costs (10,000 units):

Fixed manufacturing costs (cutting)…………………………..

Variable welding costs (@$75) ………………………………..

Fixed welding costs ……………………………………………….

Inspection and testing ……………………………………………

Alternatively, we can do a differential analysis:

Additional revenue ……………………………………..

($500 x 1,000 units)

$500,000

Inspection savings ……………………………………..

$520,000

Less additional material cost in bending ………..

Less additional variable cost in welding ………..

Solutions to Integrative Cases

10–66. (50 Min) Cost Hierarchies, Cost of Customers, and Pricing: WSM

Corporation.

a.

($000)

Sales revenue ………………

(40 Passengers

x 1,400 flights x $225)

$12,600

Costs:

10–66. (continued)

b.

We can first consider the incremental revenues and costs that would result:

Increase in revenues: (5% x 40 passengers x 1,400 flights x $225) = $630,000

Based on a purely financial analysis, we might recommend that WSM not adopt the

Internet sales alternative. However, there are other considerations that may make this

alternative attractive. For example, some issues that would need to be considered

include:

c.

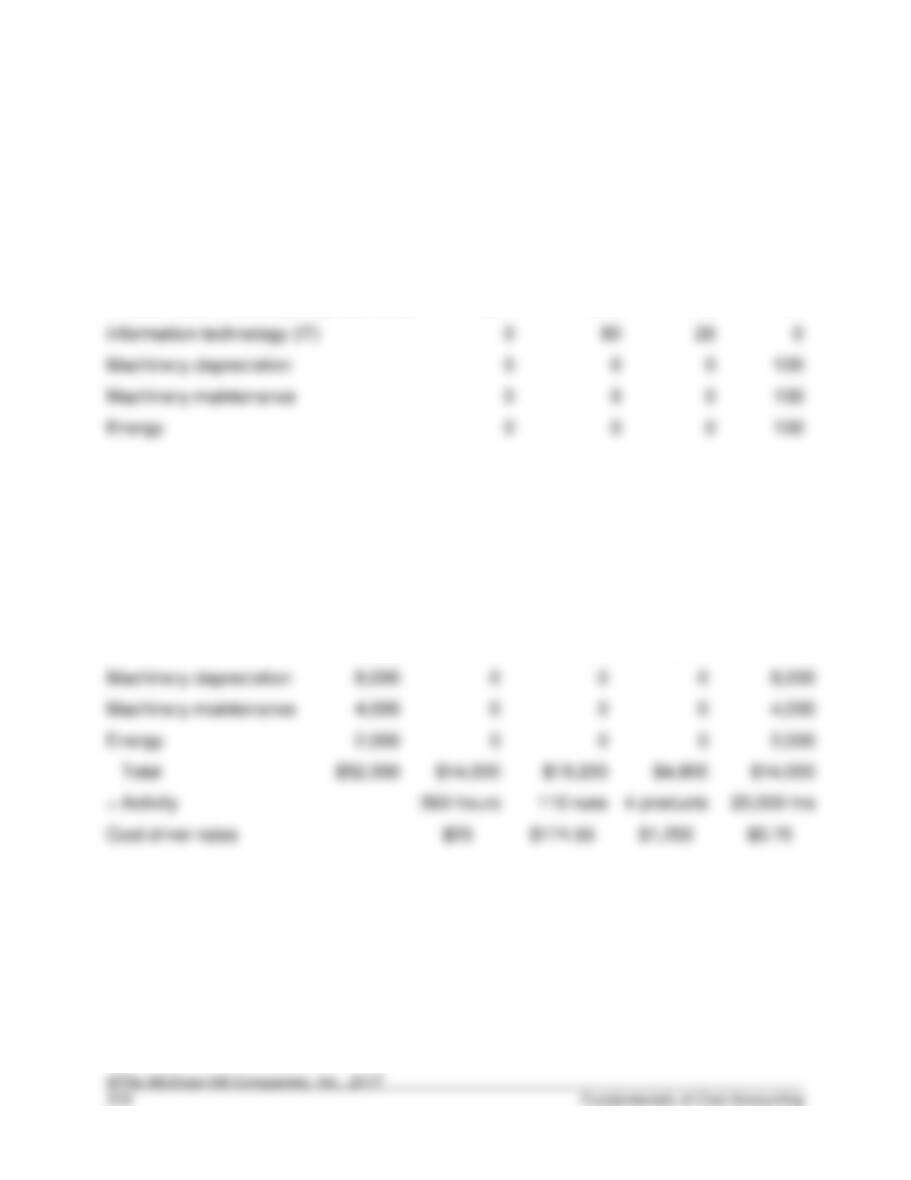

10–67. (50 Min) Unused Capacity: The Grape Cola Caper.

(Refer to the solution for 9-53.)

a. Percentage utilization of resource by activities:

Activity

Setups

Production

Runs

Products

Machine

Time

Indirect labor (including fringe benefits)

50%

40%

10%

0%

Information technology (IT)

Machinery maintenance

0

Energy

0

Costs assigned to activiities:

Activity

Cost

Setups

Production

Runs

Products

Machine

Time

Indirect labor

$28,000

$14,000

$11,200

$2,800

$ 0

IT

10,000

0

8,000

2,000

0

Machinery depreciation

8,000

0

0

0

8,000

Machinery maintenance

4,000

0

0

0

4,000

Energy

2,000

0

0

÷ Activity

20,000 hrs

Cost driver rates

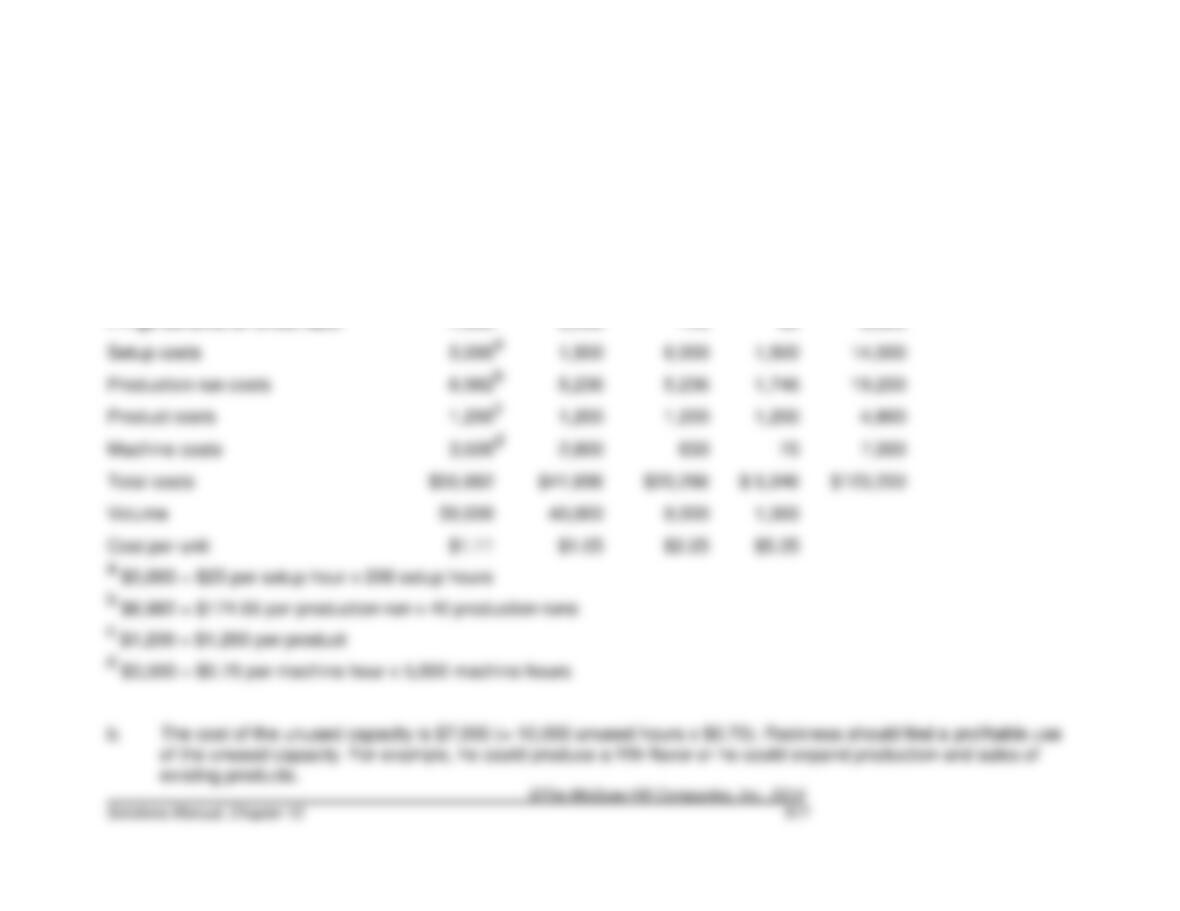

10–67. (continued)

The only change is the cost driver rate for machine time:

Unit Costs on Cola Bottling Line

Diet

Regular

Cherry

Grape

Total

Materials

$ 25,000

$ 20,000

$ 4,680

$ 550

$ 50,230

Direct labor

10,000

8,000

1,800

200

20,000

Fringe benefits on direct labor

4,000

3,200

720

80

8,000

Setup costs

Production run costs

Product costs

Machine costs

Total costs

$55,682

Volume

1,000

Cost per unit

$5.35

10–67. (continued)

c.

First, compute the costs per unit of Diet Cola, except for the machine costs:

Diet cola costs:

Materials

$ 25,000

Direct labor

10,000

Fringe benefits on direct labor

4,000

Setup costs

Production run costs

Product costs

Diet cola volume (units)

Unit costs before machine

$1.04364

(= $52,182 ÷ 50,000 units)

(= $14,000 ÷ 200,000 units)

Vanilla total costs for 100,000 units

$111,364