EXERCISE 10-10

(a) Jan. 1 Cash ($600,000 1.03) ………………………. 618,000

(b) Long-term Liabilities

Bonds Payable, due 2027 ………………………… $600,000

EXERCISE 10–11

(a) Jan. 1 Cash ($500,000 .96) ……………………… 480,000

Discount on Bonds Payable …………….. 20,000

Bonds Payable …………………………. 500,000

EXERCISE 10-12

(a) The General Electric bonds were issued at a premium and the Boeing

bonds were issued at a discount.

EXERCISE 10-12 (Continued)

(b) The prices of the two bonds differed because bond price is based on the

market rate of interest not the stated rate of interest. Market interest

EXERCISE 10-13

2017

(a) Jan. 1 Cash ……………………………………………….. 350,000

Bonds Payable …………………………. 350,000

EXERCISE 10-14

(a) April 30 Bonds Payable ……………………………….. 140,000

Loss on Bond Redemption ……………… 14,900*

EXERCISE 10-14 (Continued)

(b) June 30 Bonds Payable ……………………………….. 170,000

Premium on Bonds Payable ……………. 14,000

EXERCISE 10-15

(a)

Account

Classification

Reason

Accounts payable

Current liability

Due within one year

Accrued pension liability

Long-term liability

Relates to pensions. Not due

within one year

Unearned rent revenue

Current liability

Due within one year

Bonds payable

Not due within one year

Income taxes payable

Current liability

Due within one year

Mortgage payable

Not due within one year

Operating leases

N/A

Not a balance sheet item—may

Notes payable

Long-term liability

Not due within one year

Salaries and wages payable

Current liability

Due within one year

Notes payable (due in 2018)

Current liability

Due within one year

EXERCISE 10-15 (Continued)

(b) SANCHEZ INC.

Balance Sheet (Partial)

December 31, 2017

(in thousands)

Current liabilities

Notes payable ……………………………………….

$2,563.6

Accounts payable …………………………………

4,263.9

Current portion of mortgage payable …….

1,992.2

Warranty liability …………………………………..

1,417.3

Unearned rent revenue ………………………….

1,058.1

Salaries and wages payable ………………….

Income taxes payable …………………………..

Total current liabilities ………………………

Long-term liabilities

Mortgage payable …………………………………

$6,746.7

Bonds payable ……………………………………..

1,961.2

Accrued pension liability ………………………

1,115.2

Notes payable ……………………………………….

Total long-term liabilities ………………….

Total liabilities …………………………………………….

EXERCISE 10-16

(a) 1. Working capital = $3,416.3 – $2,988.7 = $427.6

2. Current ratio = $3,416.3 ÷ $2,988.7 = 1.14:1

$473.2 = 14.71 times

(Times interest earned = (Net income + Interest expense + Income taxes) ÷

EXERCISE 10-16 (Continued)

(b) Debt to assets ratio, adjusted for off–balance–sheet lease obligations.

$16,191.0 + $8,800

= 64%

$30,224.9 + $8,800

EXERCISE 10-17

(a) Current ratio

EXERCISE 10-18

(a) Current ratio

2017 $6,244 ÷ $4,503 = 1.39:1

EXERCISE 10-19

(a) The company does not have to record these contingent liabilities

because they have determined that they are not likely to occur and the

impact would be immaterial in any event.

(b) For financial statement users it is important to understand the possible

implications that the contingent liabilities could have on the financial

*EXERCISE 10-20

2017

(a) Jan. 1 Cash ($500,000 X 103%) ………………….. 515,000

Bonds Payable ………………………… 500,000

(b) Dec. 31 Interest Expense …………………………….. 29,500

Premium on Bonds Payable

($15,000 X 1/30) ……………………………. 500

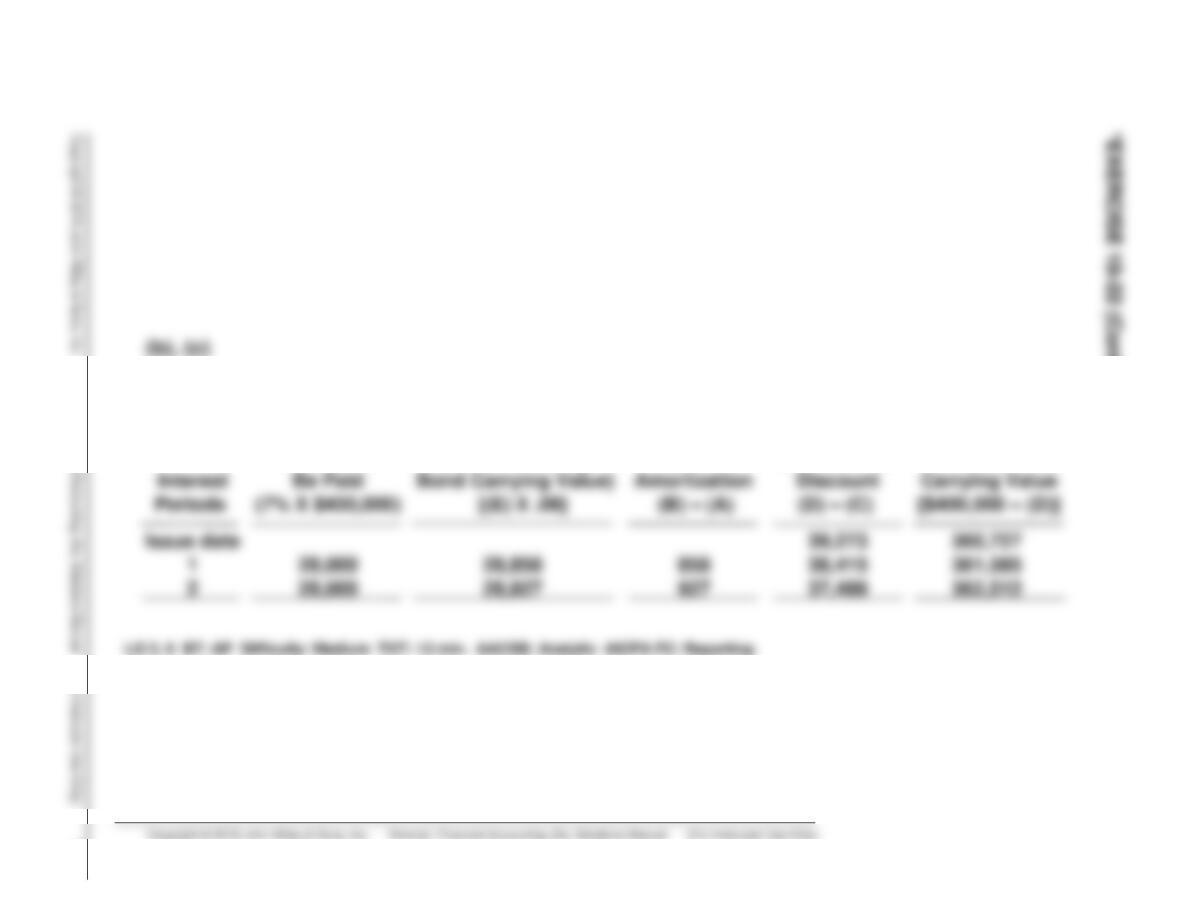

*EXERCISE 10-21

2016

(a) Dec. 31 Cash ……………………………………………… 288,000

Discount on Bonds Payable ……………. 12,000

Bonds Payable ………………………… 300,000

LO 3, 5 BT: AP Difficulty: Medium TOT: 8 min. AACSB: Analytic AICPA FC: Reporting

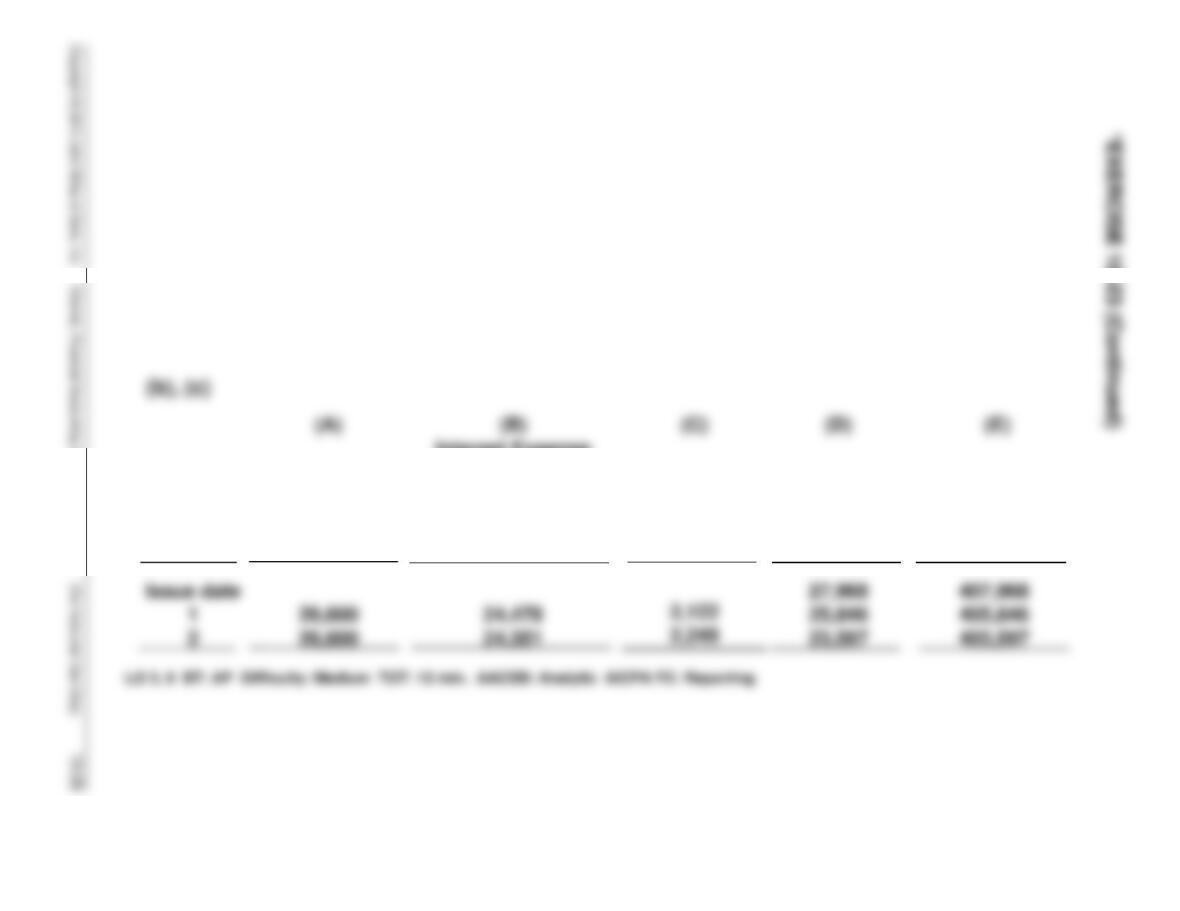

*EXERCISE 10-22

2017

(a) Jan. 1 Cash ……………………………………………….. 360,727

Discount on Bonds Payable …………….. 39,273

(A)

Interest to

(B)

Interest Expense

to Be Recorded

(8% X Preceding

(C)

Discount

(D)

Unamortized

(E)

Bond

*EXERCISE 10-23

2017

(a) Jan. 1 Cash ……………………………………………….. 407,968

(b) Dec. 31 Interest Expense ($407,968 X 6%) …….. 24,478

Premium on Bonds Payable …………….. 2,122

2018

(c) Jan. 1 Interest Payable ………………………………. 26,600

Interest

Periods

Interest to

Be Paid

(7% X $380,000)

Interest Expense

to Be Recorded

(6% X Preceding

Bond Carrying Value)

[(E) X .06]

Premium

Amortization

(A) – (B)

Unamortized

Premium

(D) – (C)

Bond

Carrying Value

[$380,000 + (D)]

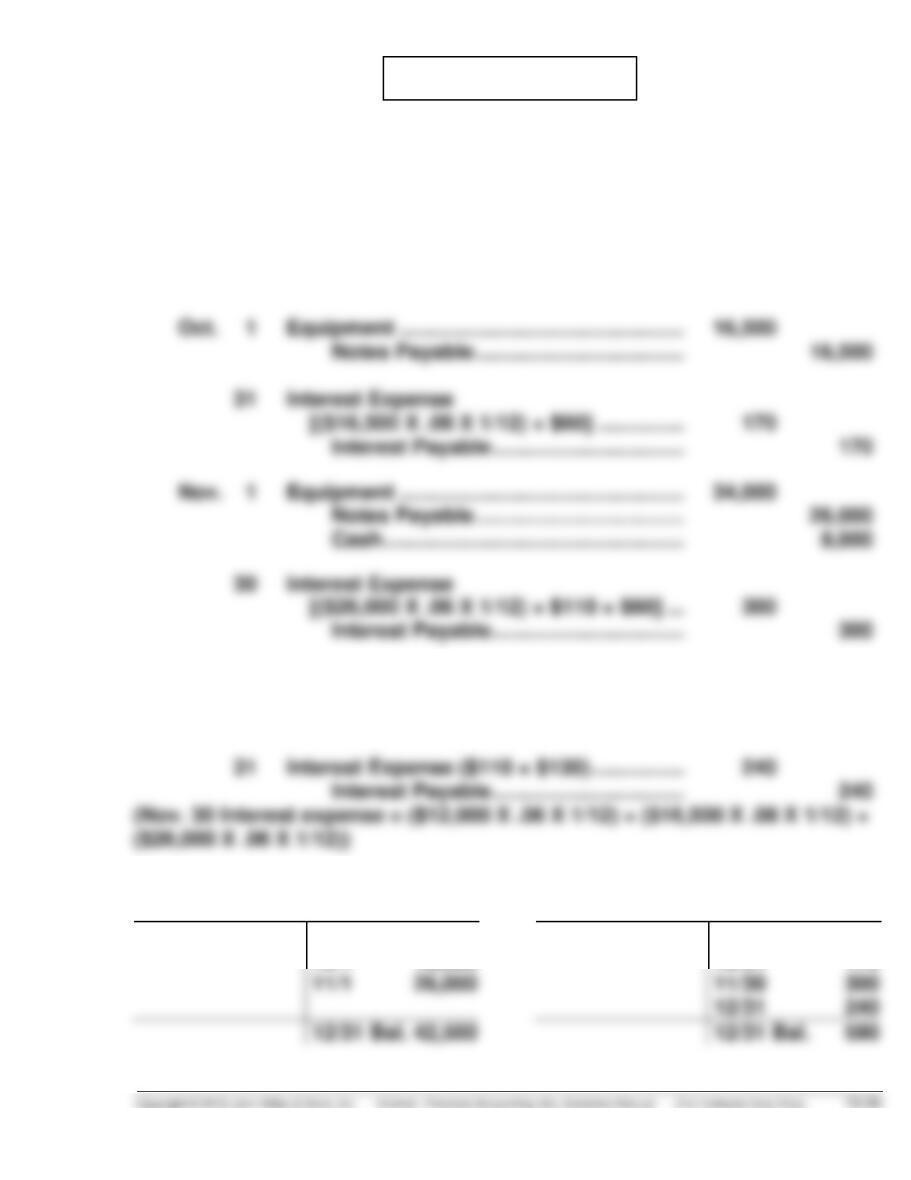

*EXERCISE 10-24

Issuance of Note

2017 Dec. 31 Cash …………………………………………. 300,000

First Installment Payment

Second Installment Payment

2019 Dec. 31 Interest Expense

[($300,000 – $20,000) X 10%] …… 28,000

(A) (B) (C) (D)

Annual Interest Reduction Principal

Interest Cash Expense of Principal Balance

Period Payment (D X 10%) (A) – (B) (D) – (C)

Issue date $300,000

12/31/18 $50,000 $30,000 $20,000 280,000

*EXERCISE 10-25

Annual

Interest

Period

(A)

Cash

Payment

(B)

Interest

Expense

(D) X 10%

(C)

Reduction

of Principal

(A) – (B)

(D)

Principal

Balance

(D) – (C)

1/1/2017

$50,000

1/1/2018

WAITE CORPORATION

Balance Sheet (Partial)

December 31, 2017

Current liabilities

Notes payable …………………………………………………………………….. $3,137

SOLUTIONS TO PROBLEMS

PROBLEM 10-1A

(a) Jan. 1 Cash ………………………………………………….. 18,000

Notes Payable …………………………….. 18,000

5 Cash ………………………………………………….. 6,254

Sales Revenue ($6,254 ÷ 1.06) ……… 5,900

Sales Taxes Payable

($6,254 – $5,900) ………………………. 354

(b) Jan. 31 Interest Expense ………………………………… 75

Interest Payable

($18,000 X 5% X 1/12) ……………….. 75

PROBLEM 10-1A (Continued)

(c) Current liabilities

Notes payable ……………………………………………………….. $ 18,000*

Accounts payable ………………………………………………….. 42,500*

PROBLEM 10-2A

(a) Sept. 1 Inventory ……………………………………………. 12,000

Notes Payable ……………………………… 12,000

30 Interest Expense

($12,000 X .06 X 1/12) ………………………. 60

Interest Payable …………………………... 60

Dec. 1 Notes Payable ……………………………………. 12,000

Interest Payable …………………………………. 180

Cash ……………………………………………. 12,180

(b)

Notes Payable

12/1 12,000

9/1 12,000

10/1 16,500

Interest Payable

12/1 180

9/30 60

10/31 170

PROBLEM 10-2A (Continued)

Interest Expense

9/30 60

10/31 170

PROBLEM 10-3A

(a) Jan. 1 Interest Payable …………………………... 40,000

Cash …………………………………….. 40,000**

PROBLEM 10-4A

2016

(a) Oct. 1 Cash …………………………………………… 700,000

Bonds Payable …………………….. 700,000

(b) Dec. 31 Interest Expense …………………………. 8,750

2017

(d) Oct. 1 Interest Expense

($700,000 X 5% X 9/12) ……………… 26,250

PROBLEM 10-5A

2017

(a) Jan. 1 Cash ($6,000,000 X 98%) ……………. 5,880,000

Discount on Bonds Payable ………. 120,000

(b) Long-term Liabilities

Bonds Payable, due 2032 …………………… $6,000,000

2019

(c) Jan. 1 Bonds Payable ………………………….. 6,000,000

Loss on Bond Redemption

($6,120,000 – $5,896,000) ……….. 224,000

PROBLEM 10-6A

(a)

2017

2016

1. Current ratio

= 1.03:1

= .92:1

2. Free cash flow

($2,457)

$1,500

3. Debt to assets ratio

$9,355 ÷ $14,308

= 65%

$9,831 ÷ $16,772

= 59%

4. Times interest

(b) The company’s position as measured through all ratios except the

(c) Southwest’s use of operating leases (vs. capital leases) would reduce its

solvency. If the leases were capital rather than operating, the balance sheet