Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

*PROBLEM 10-7A

2017

(a) Jan. 1 Interest Payable ................................. 96,000

Cash ............................................ 96,000

(b) Dec. 31 Interest Expense ................................ 98,400

2018

(c) Jan. 1 Bonds Payable ................................... 400,000

Loss on Bond Redemption ............... 11,600

Cash ($400,000 X 102%) ............ 408,000**

(d) Dec. 31 Interest Expense ................................ 82,000

Interest Payable ......................... 80,000**

Discount on Bonds Payable ..... 2,000**

(Amortization of discount = Remaining discount balance ÷ Remaining

*PROBLEM 10-8A

(a) Jan. 1 Cash ($2,000,000 X 102%) ............... 2,040,000

Bonds Payable ......................... 2,000,000

Premium on Bonds Payable .... 40,000

(b) Jan. 1 Cash ($2,000,000 X 97%) ................. 1,940,000

Discount on Bonds Payable ........... 60,000

Bonds Payable ......................... 2,000,000

(c) Premium

Current Liabilities

Interest payable ........................................ $ 140,000

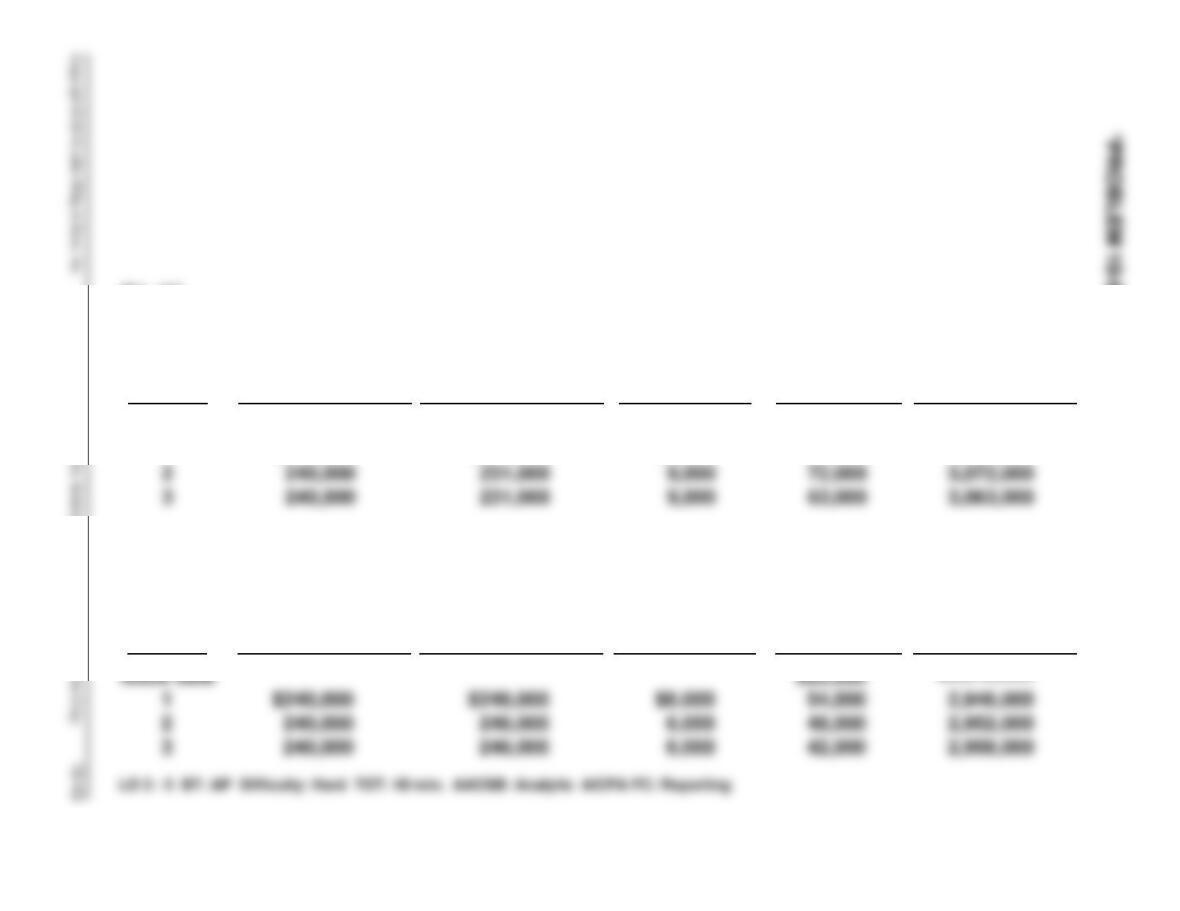

*PROBLEM 10-9A

(a) 1. 1/1/17 Cash ($3,000,000 X 103%) ....... 3,090,000

2. 1/1/17 Cash ($3,000,000 X 98%) ......... 2,940,000

Discount on Bonds

(b) See amortization tables on following page.

(c) 1. 12/31/17 Interest Expense ...................... 231,000

Premium on Bonds

2. 12/31/17 Interest Expense ...................... 246,000

Interest Payable ................ 240,000

Discount on Bonds

(d) 1. Long-term Liabilities:

Bonds Payable ..................................... $3,000,000

Plus: Unamortized Bond

(b), (1)

Annual

Interest

Periods

(A)

Interest to

Be Paid

(8% X $3,000,000)

(B)

Interest Expense

to Be Recorded

(A) – (C)

(C)

Premium

Amortization

($90,000 ÷ 10)

(D)

Unamortized

Premium

(D) – (C)

(E)

Bond

Carrying Value

[$3,000,000 + (D)]

Issue date

1

$240,000

$231,000

$9,000

$90,000

81,000

$3,090,000

3,081,000

(2)

Annual

Interest

Periods

(A)

Interest to

Be Paid

(8% X $3,000,000)

(B)

Interest Expense

to Be Recorded

(A) + (C)

(C)

Discount

Amortization

($60,000 ÷ 10)

(D)

Unamortized

Discount

(D) – (C)

(E)

Bond

Carrying Value

[$3,000,000 – (D)]

$2,940,000

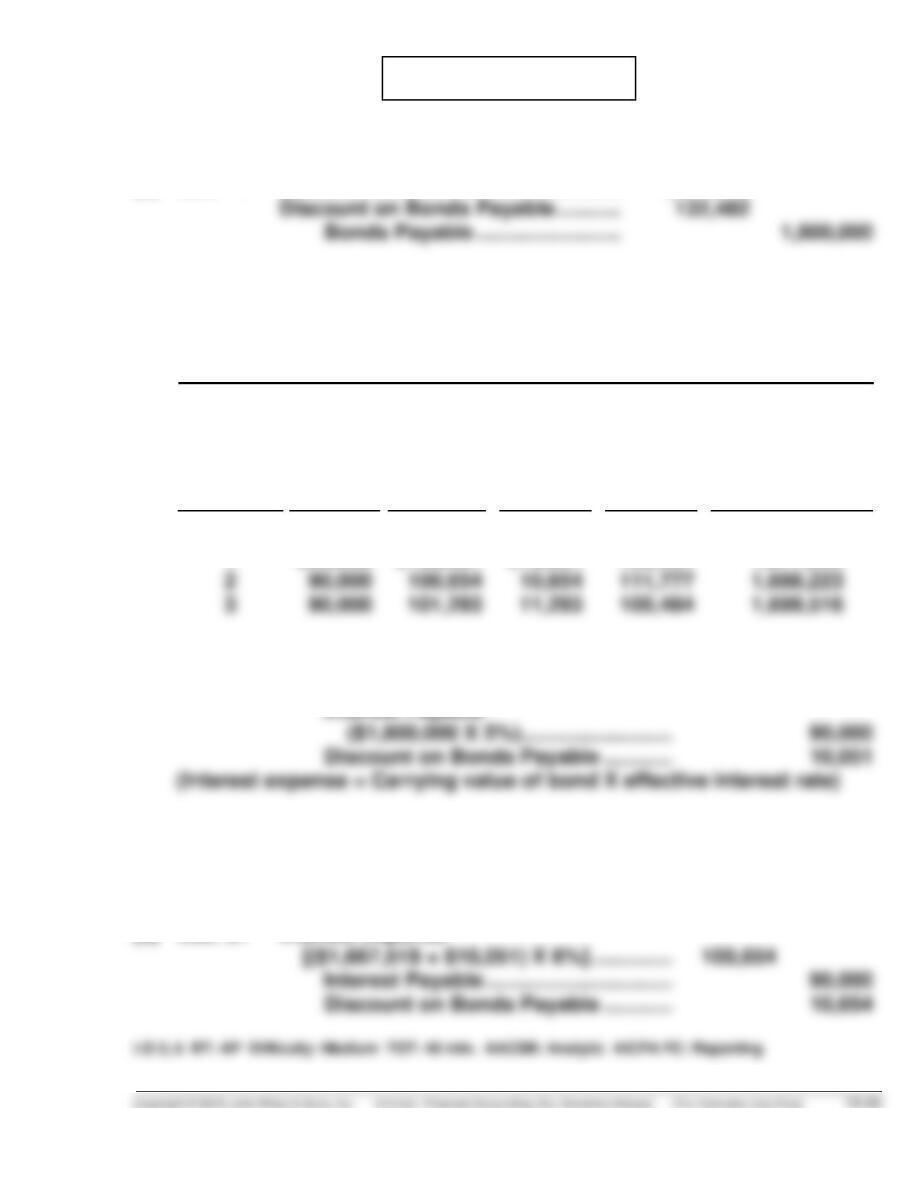

*PROBLEM 10-10A

2017

(a) Jan. 1 Cash .................................................. 1,667,518

(b) LACHTE CORP.

Bond Discount Amortization

Effective-Interest Method—Annual Interest Payments

5% Bonds Issued at 6%

Annual

Interest

Periods

(A)

Interest

to Be

Paid

(B)

Interest

Expense

to Be

Recorded

(C)

Discount

Amor-

tization

(B) – (A)

(D)

Unamor-

tized

Discount

(D) – (C)

(E)

Bond

Carrying

Value

($1,800,000 – D)

Issue date

1

$90,000

$100,051

$10,051

$132,482

122,431

$1,667,518

1,677,569

(c) Dec. 31 Interest Expense

($1,667,518 X 6%) ................................. 100,051

2018

(d) Jan. 1 Interest Payable ........................................ 90,000

Cash ................................................... 90,000

(e) Dec. 31 Interest Expense

*PROBLEM 10-11A

2017

(a) 1. Jan. 1 Cash ............................................ 2,147,202

Bonds Payable ................... 2,000,000

2. Dec. 31 Interest Expense

($2,147,202 X 6%) ................... 128,832

2018

3. Jan. 1 Interest Payable ......................... 140,000

4. Dec. 31 Interest Expense ........................ 128,162

[($2,147,202 – $11,168) X 6%]

(b) Bonds payable ..................................................... 2,000,000

(c) 1. Total bond interest expense—2018, $128,162.

2. The effective-interest method will result in more interest expense

reported than the straight-line method in 2018 when the bonds are

*PROBLEM 10-12A

(a)

Annual

Interest Period

(A)

Cash

Payment

(B)

Interest

Expense

(D) X 8%

(C)

Reduction

of Principal

(A) – (B)

(D)

Principal

Balance

(D) – (C)

Issue Date

1

$80,146

$25,600

$54,546

$320,000

265,454

(b) Dec. 31 Mortgage Payable ................................. 54,546

Interest Expense ................................... 25,600

Cash ............................................... 80,146

*PROBLEM 10-13A

(a)

Period

Cash

Payment

(A)

Interest

Expense

(B) = (D) X 7%

Principal

Reduction

(C) = (A) – (B)

Balance

(D) = (D) – (C)

July 1, 2016

$150,000

June 30, 2017

$ 36,584

$10,500

$ 26,084

123,916

June 30, 2018

36,584

8,674

27,910

96,006

*Rounded to make principal element equal to balance.

(See Illustration 10C-1)

(b) July 2016 Cash ................................................... 150,000

Notes Payable .............................. 150,000

(c) 2018

Current liabilities

Notes payable ...................................................... $29,864

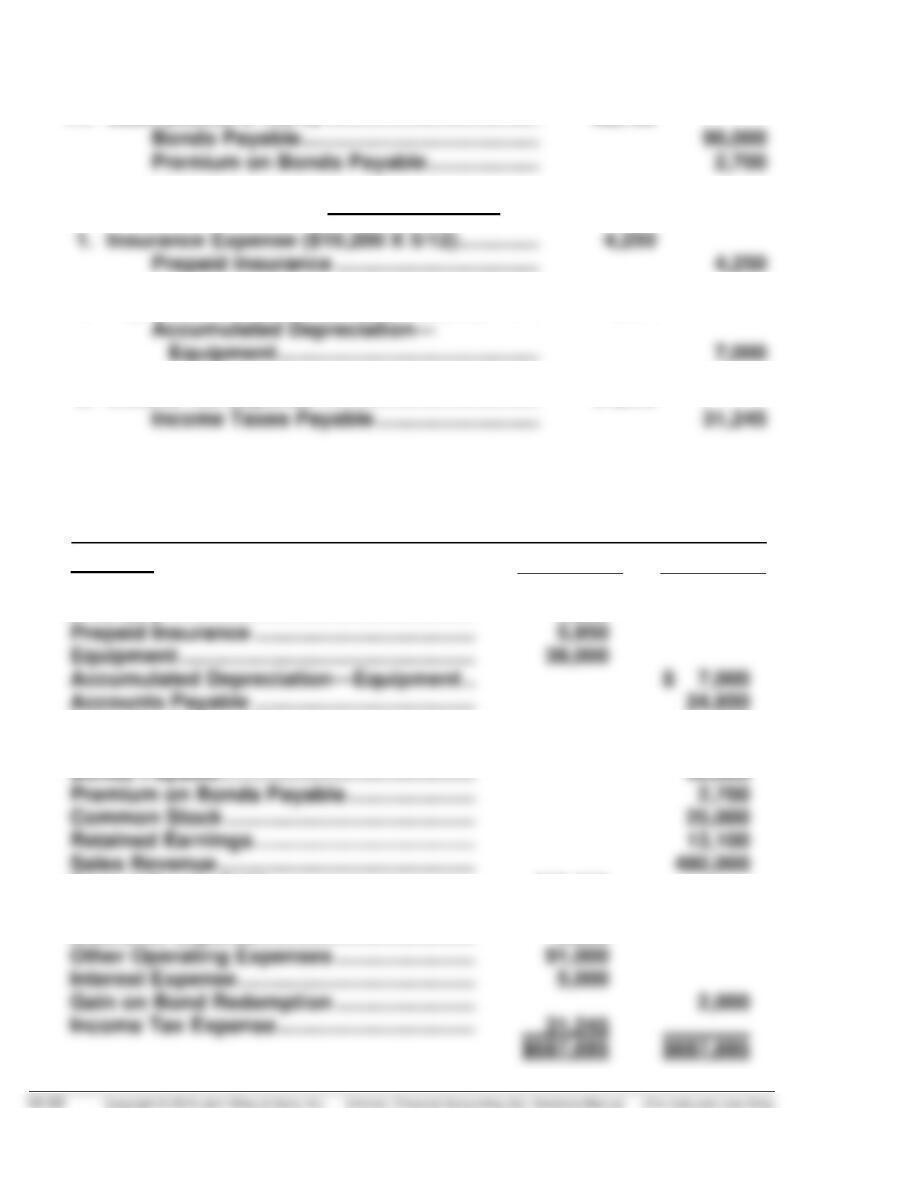

ACR 10 ACCOUNTING CYCLE REVIEW

(a)

1.

Interest Payable ..............................................

Cash .........................................................

2,500

2,500

3.

Cash .................................................................

Sales Revenue .........................................

508,800

480,000

5.

Interest Expense .............................................

Cash .........................................................

2,500

2,500

7.

Prepaid Insurance ..........................................

Cash .........................................................

10,200

10,200

9.

Other Operating Expenses ............................

Cash .........................................................

91,000

91,000

10.

Interest Expense .............................................

Cash .........................................................

2,500

2,500

ACR 10 (Continued)

11.

Cash (90,000 X 103%) .....................................

92,700

Adjusting Entries

2.

Depreciation Expense ($38,000 – $3,000) ÷ 5 ....

7,000

3.

Income Tax Expense ......................................

31,245

(b) AIMES CORPORATION

Trial Balance

12/31/2017

Account

Debit

Credit

Cash .............................................................

$227,800

Inventory .....................................................

6,850

Sales Taxes Payable ..................................

11,800

Income Taxes Payable ...............................

31,245

Cost of Goods Sold ....................................

265,000

Depreciation Expense ................................

7,000

Insurance Expense .....................................

9,850

ACR 10 (Continued)

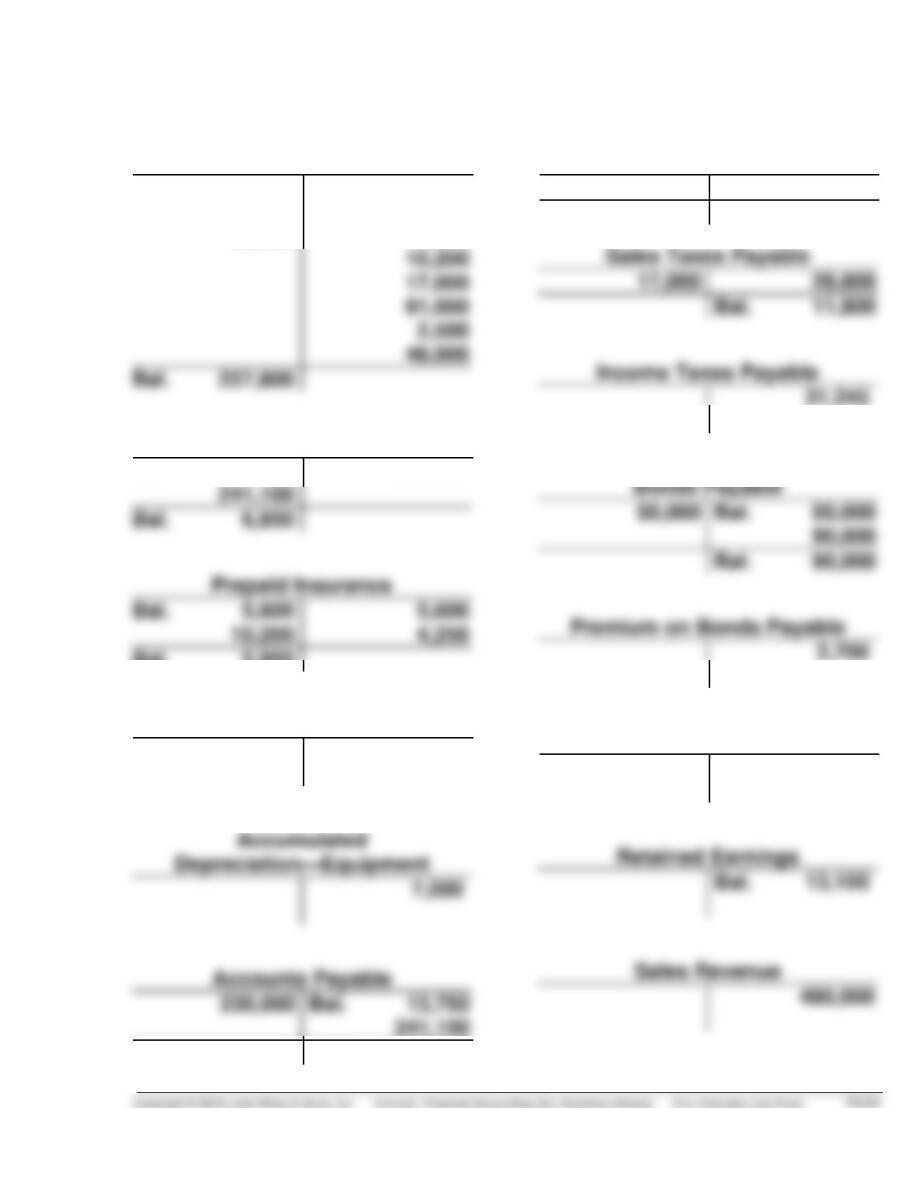

(a) and (b) Optional T accounts

Cash

Bal. 30,000

508,800

92,700

2,500

230,000

2,500

Inventory

Bal. 30,750

265,000

Bal. 5,950

Equipment

Bal. 38,000

Bal. 24,850

Interest Payable

2,500

Bal. 2,500

Bal. 0

Common Stock

Bal. 25,000

ACR 10 (Continued)

(a) and (b) (Continued)

Cost of Goods Sold

4,250

Bal. 9,850

Other Operating Expenses

91,000

Interest Expense

Gain on Bond Redemption

2,000

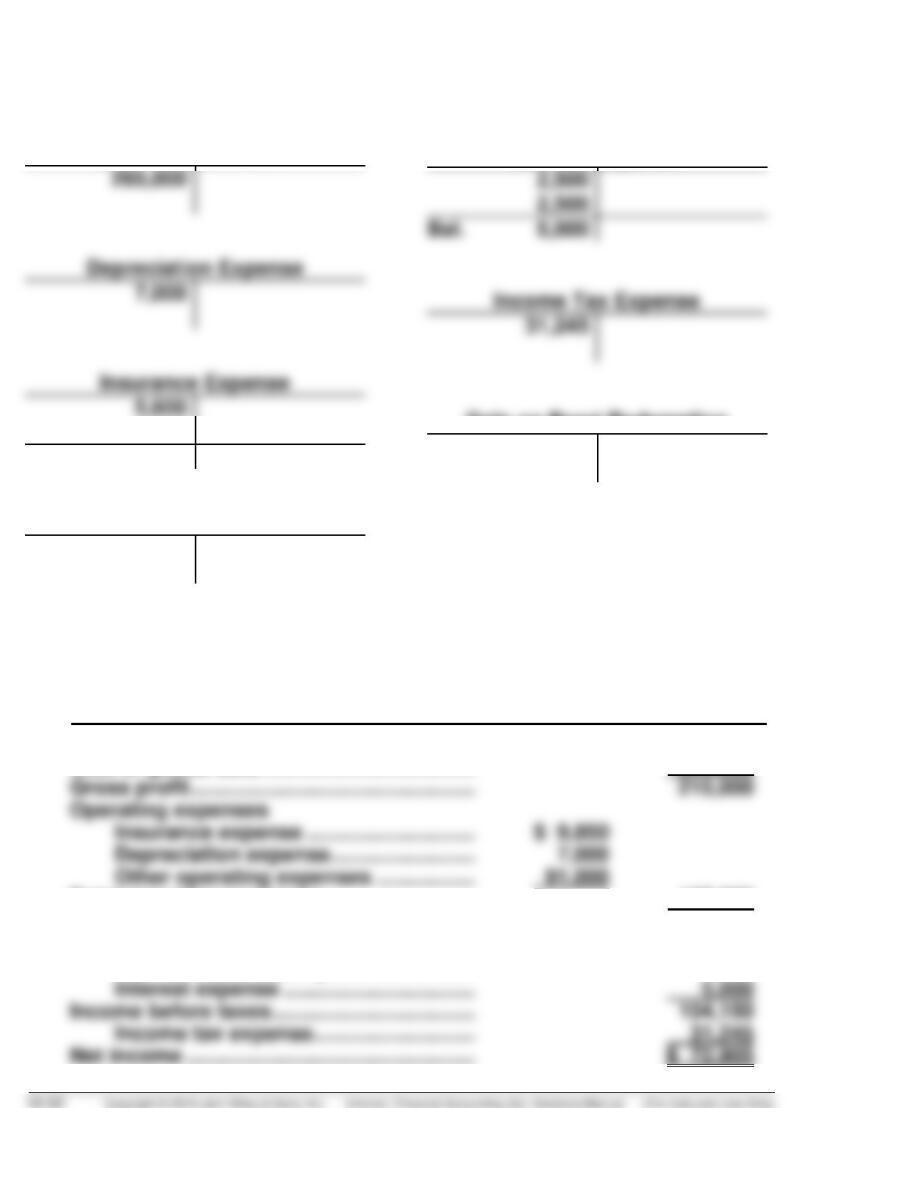

(c) AIMES CORPORATION

Income Statement

For the Year Ending 12/31/17

Sales revenue .............................................

$480,000

Cost of goods sold .....................................

265,000

Total operating expenses ..........................

107,850

Income from operations.............................

107,150

Other revenues and expenses

Gain on bond redemption ..................

2,000

ACR 10 (Continued)

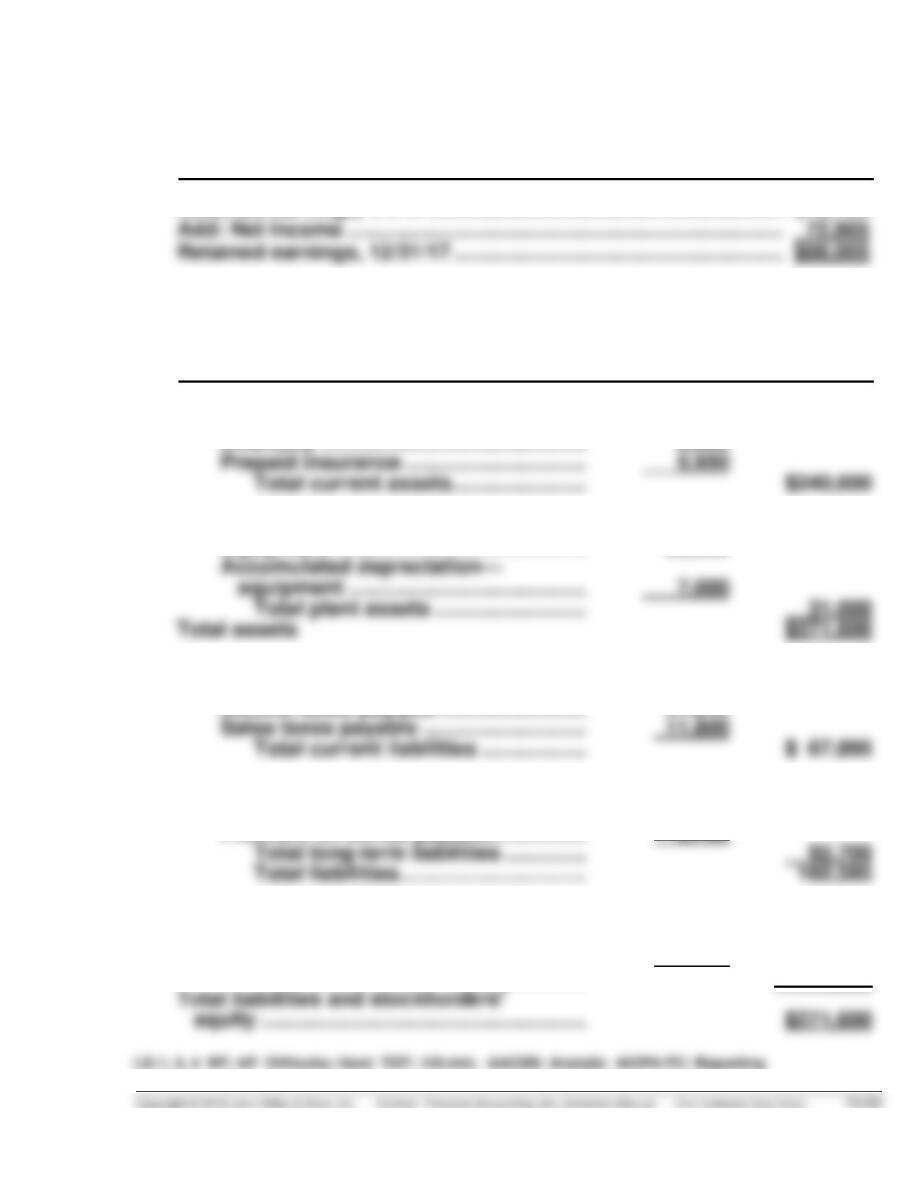

AIMES CORPORATION

Retained Earnings Statement

For the Year Ending 12/31/17

Retained earnings, 1/1/17 .............................................................

$13,100

AIMES CORPORATION

Balance Sheet

12/31/2017

Current Assets

Cash ......................................................

$227,800

Property, Plant, and Equipment

Equipment ............................................

38,000

Current Liabilities

Accounts payable ................................

$24,850

Income taxes payable .........................

31,245

Long-term liabilities

Bonds payable .....................................

90,000

Premium on bonds payable ................

2,700

Stockholders’ Equity

Common stock ....................................

25,000

Retained earnings ...............................

86,005

Total stockholders’ equity ............

111,005

CT 10-1 FINANCIAL REPORTING PROBLEM

(a) Total current liabilities at September 27, 2014, $63,448 millions. Apple's

total current liabilities increased by $19,790 millions ($63,448 – $43,658)

relative to the prior year.

CT 10-2 COMPARATIVE ANALYSIS PROBLEM

(a)

Columbia Sportswear

VF Corporation

(b)

Columbia Sportswear

VF Corporation

(1)

Debt to assets

$436,975

$1,792,209

= 24.4%

$4,349,258

$9,980,190

* = 43.6%

The higher the percentage of debt to assets, the greater the risk that a

company may be unable to meet its maturing obligations. Columbia

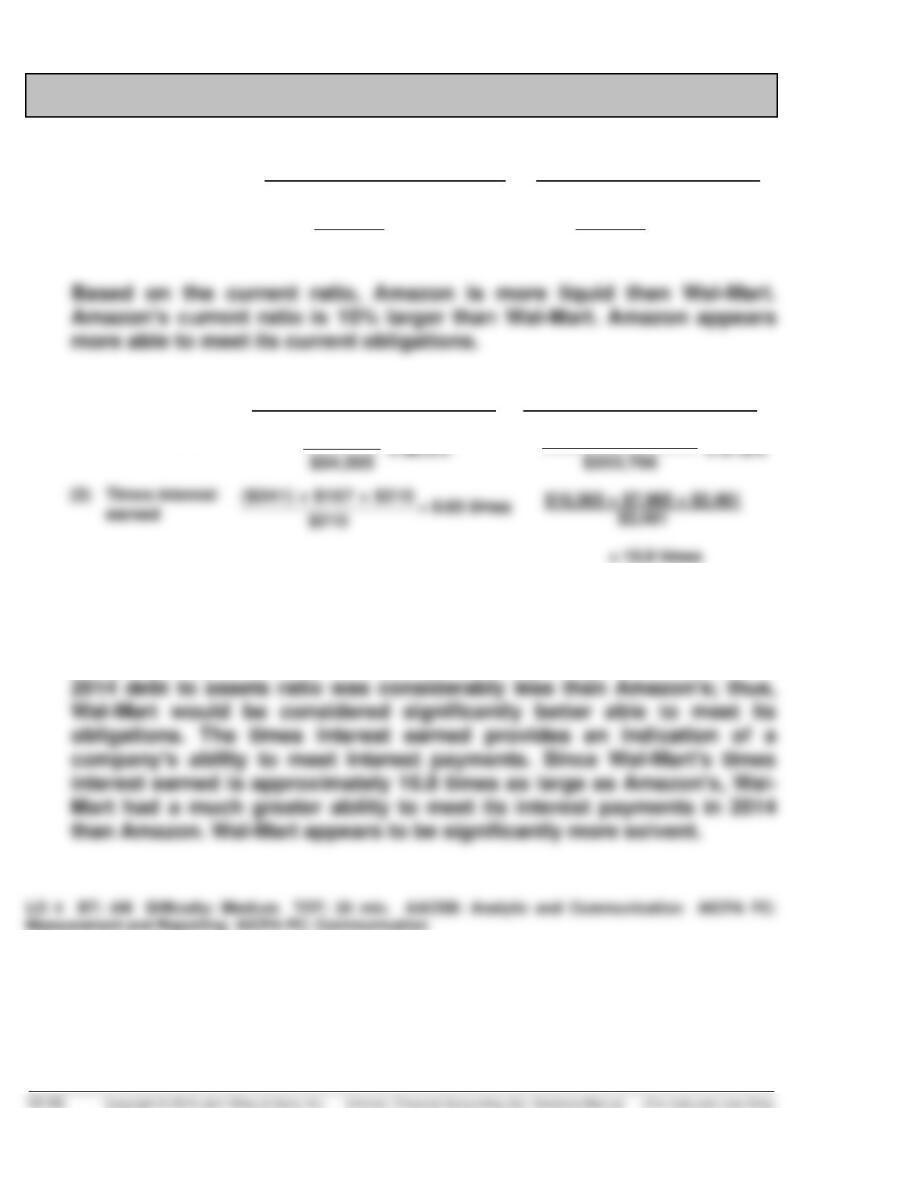

CT 10-3 COMPARATIVE ANALYSIS PROBLEM

(a)

Amazon .com

Wal-Mart

(1)

Current ratio

$31,327

$28,089

= 1.12:1

$63,278

$65,272

= 0.97:1

(b)

Amazon .com

Wal-Mart

(1)

Debt to assets

$43,764 *

$203,706 $85,937

-

*$28,089 + $8,265 + $7,410

The higher the percentage of debt to assets, the greater the risk that a

company may be unable to meet its maturing obligations. Wal-Mart’s