Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 10

SOLUTIONS TO PROBLEMS: SET B

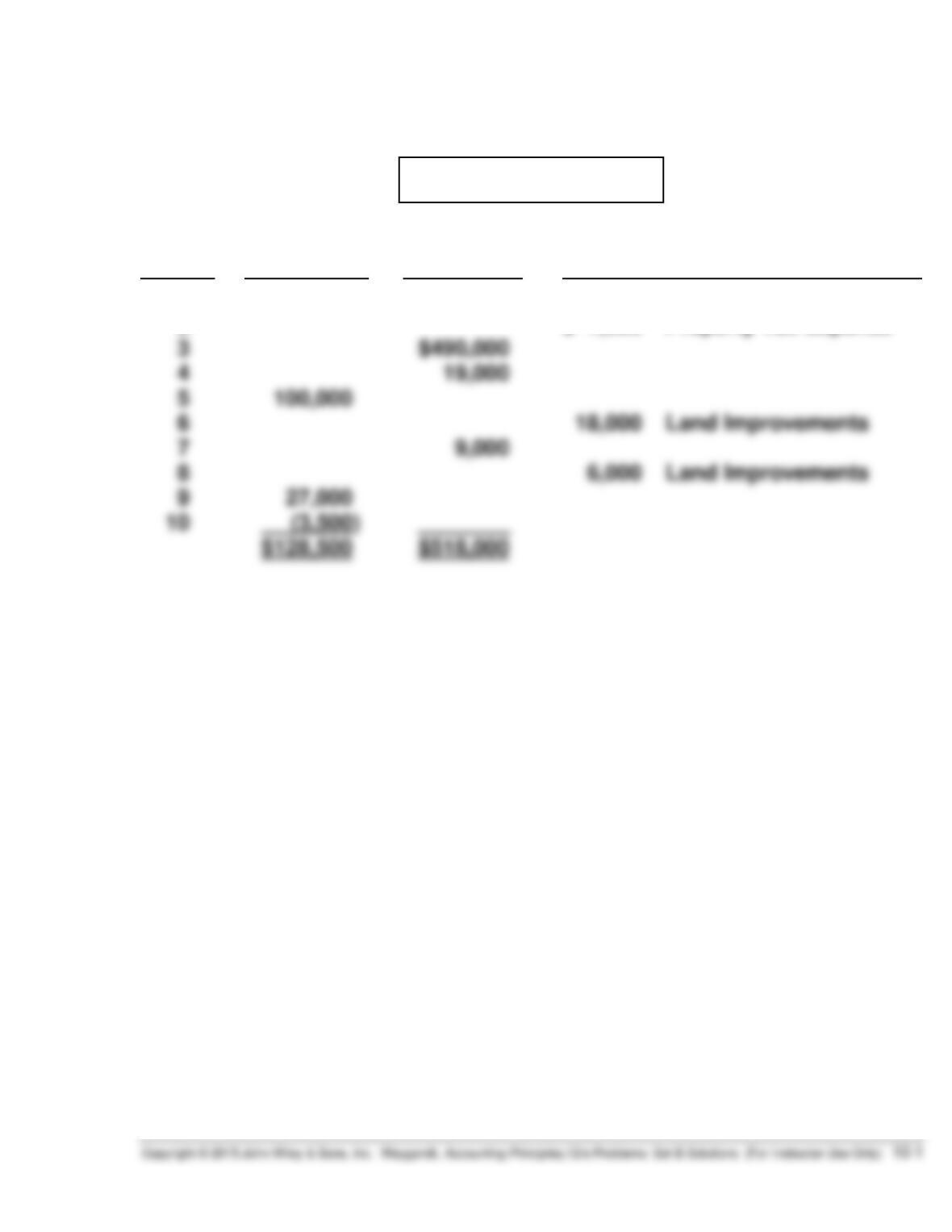

PROBLEM 10-1B

Item

Land

Buildings

Other Accounts

1

2

3

($ 5,000)

$490,000

$ 7,500 Property Tax Expense

PROBLEM 10-2B

(a)

Year

Computation

Accumulated

Depreciation

12/31

MACHINE 1

2012

2013

2014

$100,000 X 10% = $10,000

$100,000 X 10% = $10,000

$100,000 X 10% = $10,000

$ 10,000

20,000

30,000

(b)

Year

Depreciation Computation

Expense

MACHINE 2

(1)

2013

$180,000 X 25% X 8/12 = $30,000

$30,000

PROBLEM 10-3B

(a) (1) Purchase price ................................................................. $ 58,000

Sales tax ........................................................................... 2,750

Shipping costs ................................................................. 100

Equipment .......................................................... 61,000

Cash ............................................................ 61,000

(2) Recorded cost .................................................................. $ 61,000

Less: Salvage value ........................................................ 5,000

(b) (1) Recorded cost .................................................................. $120,000

Less: Salvage value ........................................................ 10,000

(2)

Year

Book Value at

Beginning of

Year

DDB Rate

Annual

Depreciation

Expense

Accumulated

Depreciation

2015

2016

$120,000

60,000

*50%*

*50%*

$60,000

30,000

$60,000

90,000

PROBLEM 10-3B (Continued)

(3) Depreciation cost per unit = ($120,000 – $10,000)/25,000 units =

$4.40 per unit.

Annual Depreciation Expense

2015: $4.40 X 5,500 = $24,200

(c) The units-of-activity method reports the lowest amount of depreciation

expense the first year while the declining-balance method reports the

highest. In the fourth year, the declining-balance method reports the

lowest amount of depreciation expense while the straight-line method

reports the highest.

These facts occur because the declining-balance method is an accelerated

depreciation method in which the largest amount of depreciation is

PROBLEM 10-4B

Year

Depreciation

Expense

Accumulated

Depreciation

2013

2014

$45,000(a)

45,000

$ 45,000

90,000

(a)

$300,000 – $30,000

6 years

= $45,000

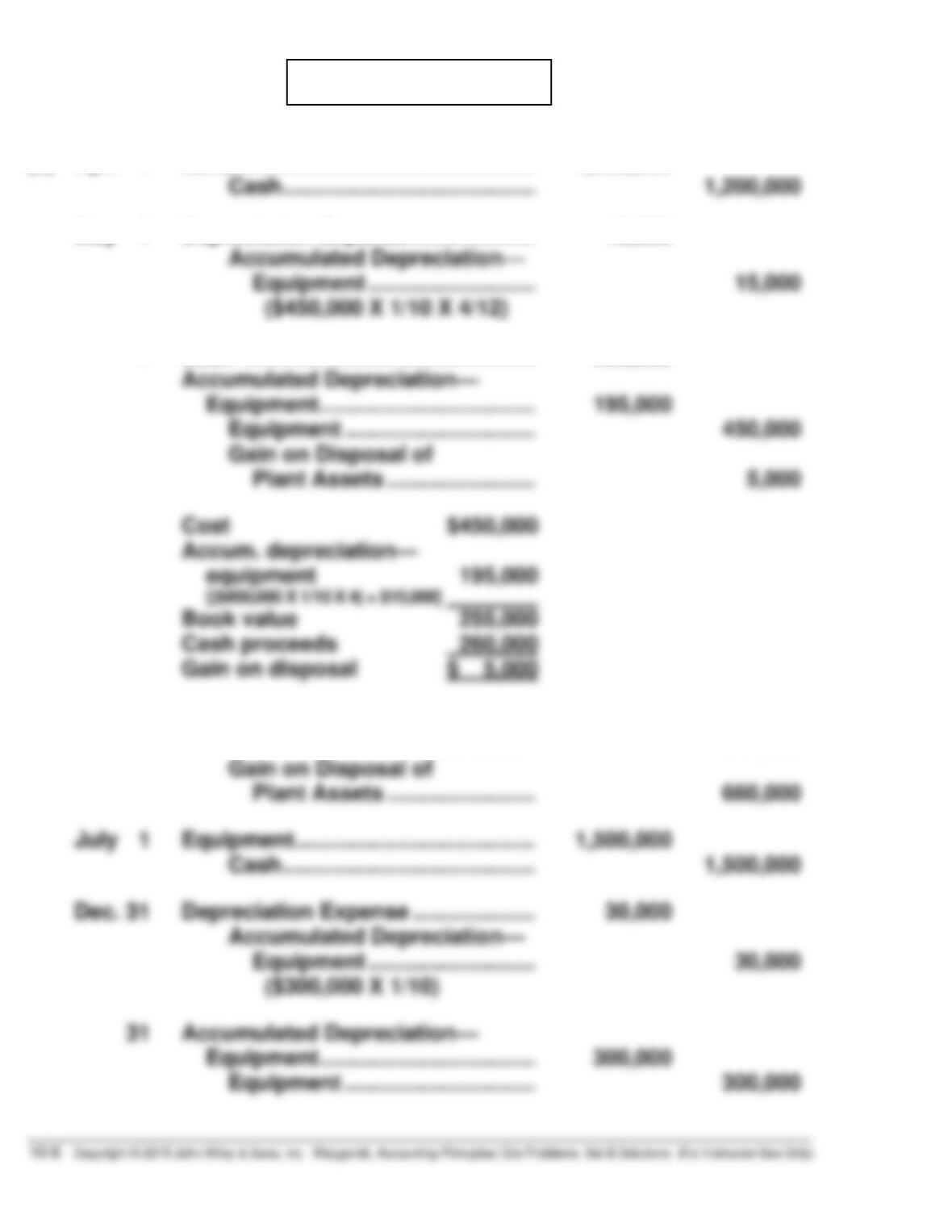

PROBLEM 10-5B

(a) Apr. 1 Land................................................. 1,200,000

Cash ......................................... 1,200,000

May 1 Depreciation Expense .................... 15,000

Accumulated Depreciation—

Equipment ........................... 15,000

($450,000 X 1/10 X 4/12)

June 1 Cash ................................................ 1,000,000

Land ......................................... 340,000

Gain on Disposal of

Plant Assets ........................ 660,000

July 1 Equipment ....................................... 1,500,000

Cash ......................................... 1,500,000

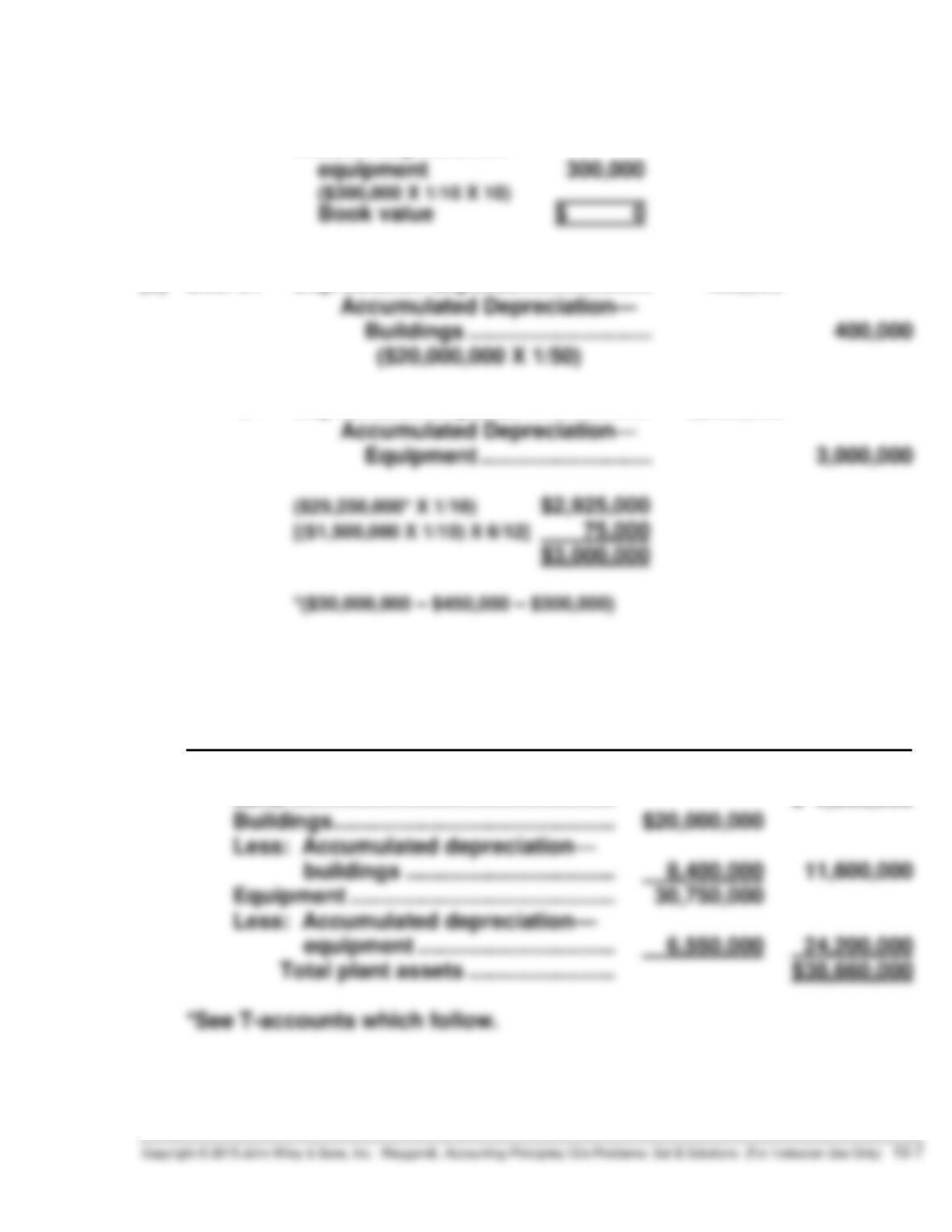

PROBLEM 10-5B (Continued)

Cost $300,000

Accum. depreciation—

(b) Dec. 31 Depreciation Expense ..................... 400,000

Accumulated Depreciation—

Buildings .............................. 400,000

($20,000,000 X 1/50)

31 Depreciation Expense ..................... 3,000,000

Accumulated Depreciation—

(c) TORREALBA COMPANY

Partial Balance Sheet

December 31, 2016

Plant Assets*

Land ..................................................... $ 2,860,000

Buildings .............................................. $20,000,000

Less: Accumulated depreciation—

buildings .................................. 8,400,000 11,600,000

PROBLEM 10-5B (Continued)

Land

Bal. 2,000,000

June 1 340,000

Buildings

Bal. 20,000,000

Bal. 20,000,000

Accumulated Depreciation—Buildings

Bal. 8,000,000

Equipment

Bal. 30,000,000

May 1 450,000

Accumulated Depreciation—Equipment

May 1 195,000

Dec. 31 300,000

Bal. 4,000,000

May 1 15,000

PROBLEM 10-6B

(a) Accumulated Depreciation—Equipment .................. 26,000

Loss on Disposal of Plant Assets ............................ 19,000

Equipment .......................................................... 45,000

PROBLEM 10-7B

(a) Jan. 2 Patents .................................................. 36,000

Cash ............................................... 36,000

Jan.– Research and Development

June Expense ............................................ 230,000

Cash ............................................... 230,000

(b) Dec. 31 Amortization Expense .......................... 14,000

Patents ........................................... 14,000

[($100,000 X 1/10) + ($36,000 X 1/9)]

(c) Intangible Assets

Patents ($136,000 cost – $24,000 amortization) (1) ............. $112,000

Copyrights ($360,000 cost – $31,500 amortization) (2) ....... 328,500

Total intangible assets ................................................... $440,500

(d) The intangible assets of the company consist of two patents and two

copyrights. One patent with a total cost of $136,000 is being amortized

in two segments ($100,000 over 10 years and $36,000 over 9 years); the

PROBLEM 10-8B

1. Research and Development Expense ...................... 110,000

Patents ................................................................ 110,000

PROBLEM 10-9B

(a)

Auer Corp.

Marte Corp.

Asset turnover

$1,050,000

$1,000,000

= 1.05 times

$945,000

$1,050,000

= .90 times