Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 10

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 10-1C

(a) Jan. 1 Cash ........................................................... 18,000

Notes Payable ................................... 18,000

5 Cash ........................................................... 18,480

Sales Revenue ($18,480 ÷ 105%) ..... 17,600

Sales Taxes Payable

($18,480 – $17,600) ........................ 880

(b) Jan. 31 Interest Expense ....................................... 105

Interest Payable

($18,000 X 7% X 1/12 = $105) ....... 105

PROBLEM 10-1C (Continued)

(c) Current liabilities

Notes payable ................................................................. $ 18,000

Accounts payable ........................................................... 52,000

Salaries and wages payable .......................................... 44,769

PROBLEM 10-2C

(a) Mar. 1 Equipment ................................................. 9,000

Notes Payable .................................... 9,000

31 Interest Expense

($9,000 X .06 X 1/12) .............................. 45

Interest Payable ................................. 45

31 Interest Expense

[($12,000 X .06 X 1/12) + $45 + $300] ......... 405

Interest Payable ................................. 405

PROBLEM 10-2C (Continued)

Interest Expense

3/31 45

4/30 345

PROBLEM 10-3C

(a) Jan. 1 Interest Payable ...................................... 84,000

Cash .................................................. 84,000

PROBLEM 10-4C

(a) 2016 Cash .......................................................... 600,000

April 1 Bonds Payable ................................. 600,000

(b) Dec. 31 Interest Expense ...................................... 36,000

Interest Payable

($600,000 X 8% X 9/12) ................. 36,000

PROBLEM 10-5C

(a) 2017

Jan. 1 Cash ($5,000,000 X 103%) ................. 5,150,000*

Bonds Payable ........................... 5,000,000

Premium on Bonds

Payable ................................... 150,000

PROBLEM 10-6C

(a)

2017

2016

1. Current ratio

$59,223 ÷ $37,673

$75,806 ÷ $39,616

2. Free cash flow

$19,827 – $7,967

= $11,860

$16,593 – $4,694

= $11,899

3. Debt to assets ratio

$102,509 ÷ $165,276

= 62%

$137,171 ÷ $194,926

= 70%

(b) In terms of liquidity Krispy Kreme was less liquid in 2017 than 2016. Its

current ratio and free cash flow deteriorated. In contrast, its debt to

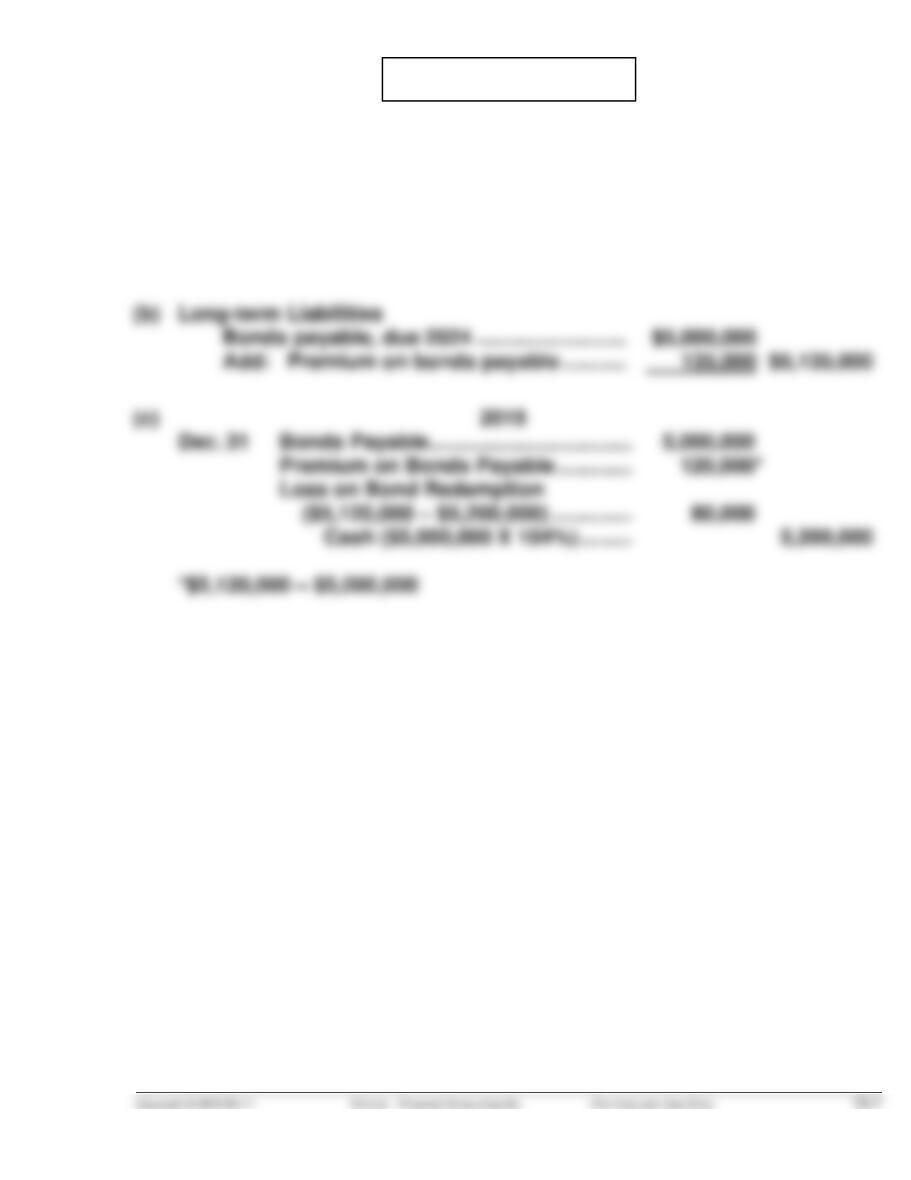

*PROBLEM 10-7C

2017

(a) Jan. 1 Interest Payable .............................. 216,000

Cash ......................................... 216,000

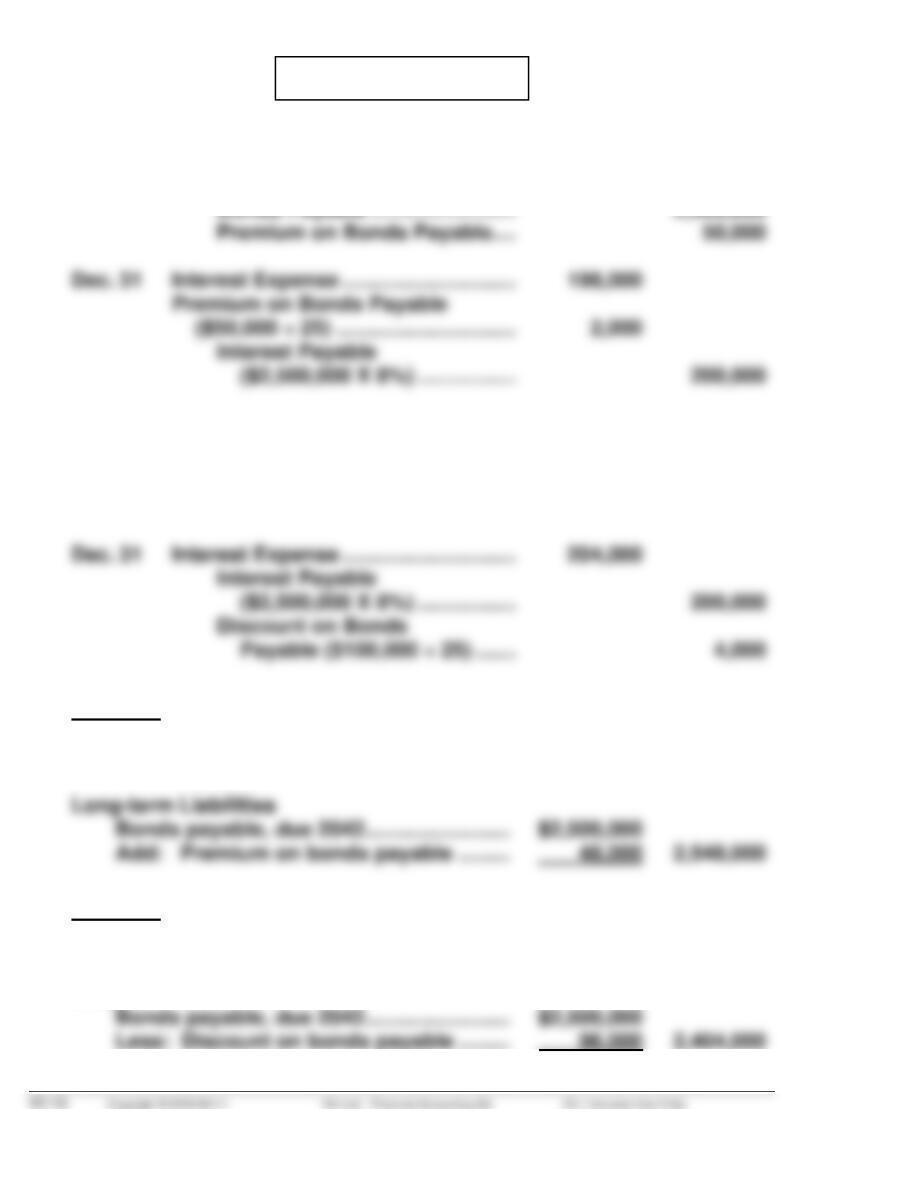

(b) Dec. 31 Interest Expense ............................. 188,000

Premium on Bonds Payable

(d) Dec. 31 Interest Expense ............................. 94,000**

Premium on Bonds Payable .......... 14,000**

*PROBLEM 10-8C

2017

(a) Jan. 1 Cash ($2,500,000 X 102%) ............... 2,550,000

2017

(b) Jan. 1 Cash ($2,500,000 X 96%) ................. 2,400,000

Discount on Bonds Payable ........... 100,000

Bonds Payable ......................... 2,500,000

(c) Premium

Current Liabilities

Interest payable ........................................ $ 200,000

Discount

Current Liabilities

Interest payable ........................................ $ 200,000

Long-term Liabilities

*PROBLEM 10-9C

(a) 1. 12/31/16 Cash ($2,600,000 X 98%) ...... 2,548,000

2. 12/31/16 Cash ($2,600,000 X 104%) .... 2,704,000

Bonds Payable ............... 2,600,000

Premium on Bonds

Payable ....................... 104,000

2. 12/31/17 Interest Expense ................... 228,800

Premium on Bonds

Payable............................... 5,200

Cash ................................ 234,000

2. Long-term Liabilities:

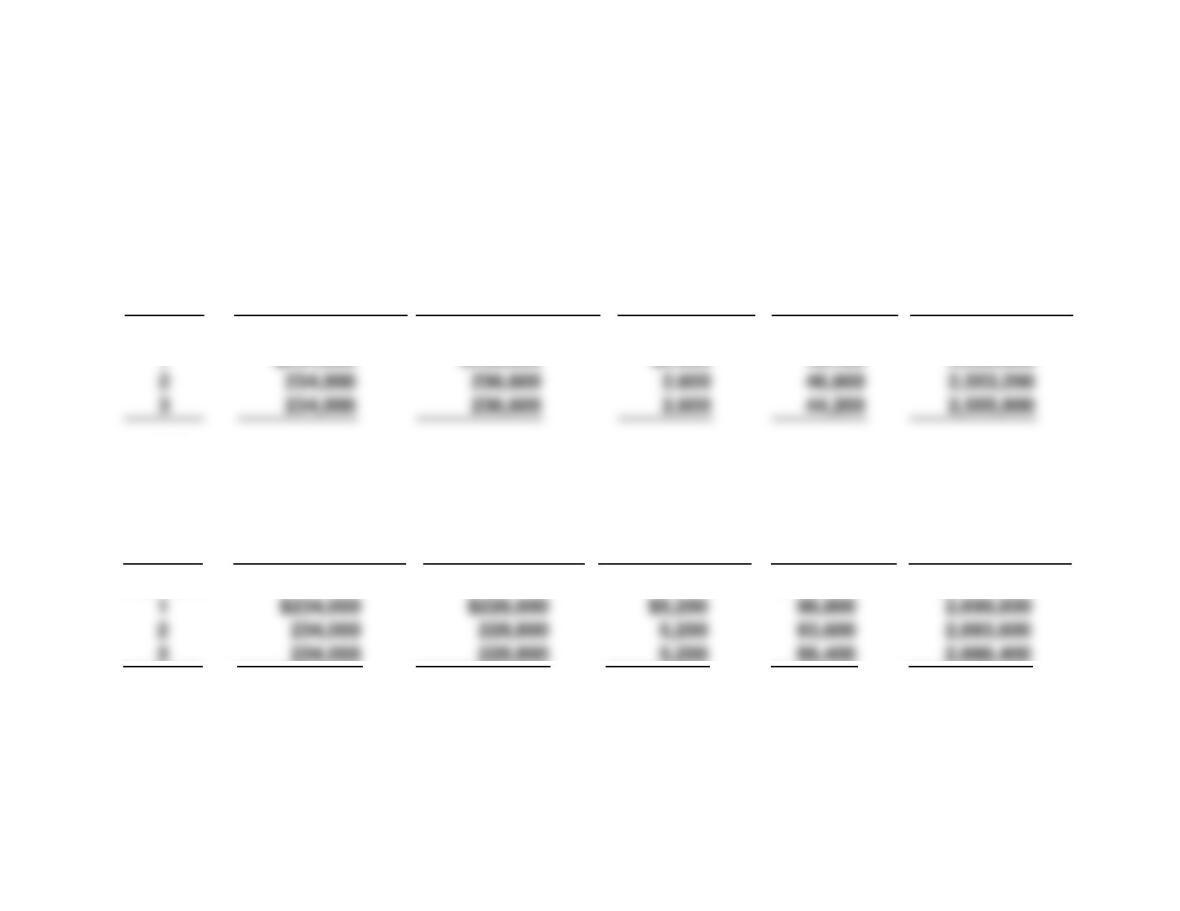

*PROBLEM 10-9C (Continued)

(b), (1)

Annual

Interest

Periods

(A)

Interest to

Be Paid

(9% X $2,600,000)

(B)

Interest Expense

to Be Recorded

(A) + (C)

(C)

Discount

Amortization

($52,000 ÷ 20)

(D)

Unamortized

Discount

(D) – (C)

(E)

Bond

Carrying Value

[$2,600,000 – (D)]

Issue date

1

$234,000

$236,600

$2,600

$52,000

49,400

$2,548,000

2,550,600

(2)

Annual

Interest

Periods

(A)

Interest to

Be Paid

(9% X $2,600,000)

(B)

Interest Expense

to Be Recorded

(A) – (C)

(C)

Premium

Amortization

($104,000 ÷ 20)

(D)

Unamortized

Premium

(D) – (C)

(E)

Bond

Carrying Value

[$2,600,000 + (D)]

Issue date

$104,000

$2,704,000

*PROBLEM 10-10C

2017

(a) Jan. 1 Cash .................................................. 1,077,217

(b) PEDRAZA CORPORATION

Bond Premium Amortization

Effective-Interest Method—Annual Interest Payments

6% Bonds Issued at 5%

Annual

Interest

Periods

(A)

Interest

to Be

Paid

(B)

Interest

Expense

(C)

Premium

Amor-

tization

(A) – (B)

(D)

Unamor-

tized

Premium

(D) – (C)

(E)

Bond

Carrying

Value

($1,000,000 + D)

Issue date

1

$60,000

$53,861

$6,139

$77,217

71,078

$1,077,217

1,071,078

(c) Dec. 31 Interest Expense

($1,077,217 X 5%) .................................. 53,861

Premium on Bonds Payable .................... 6,139

(d) 2018

Jan. 1 Interest Payable ........................................ 60,000

Cash ................................................... 60,000

(e) Dec. 31 Interest Expense

[($1,077,217 – $6,139) X 5%] ................ 53,554

*PROBLEM 10-11C

(a) 1. 2017

Jan. 1 Cash .......................................... 3,391,514

2. Dec. 31 Interest Expense

($3,391,514 X 10%) ............... 339,151

3. 2018

4. Dec. 31 Interest Expense ...................... 341,067

[($3,391,514 + $19,151) X 10%]

(b) Bonds Payable .................................................. $4,000,000*

(c) 1. Total bond interest expense—2018, $341,067.

2. The effective-interest method will result in less interest expense

reported than the straight-line method in 2018 when the bonds

*PROBLEM 10-11C (Continued)

3. Annual interest payments

($4,000,000 X 8%) = $320,000; $320,000 X 15 ........ $4,800,000

*PROBLEM 10-12C

(a)

Quarterly

Interest Period

(A)

Cash

Payment

(B)

Interest

Expense

(D) X 1.5%

(C)

Reduction

of Principal

(A) – (B)

(D)

Principal

Balance

(D) – (C)

Issue Date

1

$23,298

$6,000

$17,298

$400,000

382,702

(c) Current liabilities

Mortgage payable ......................................................... $ 71,825*

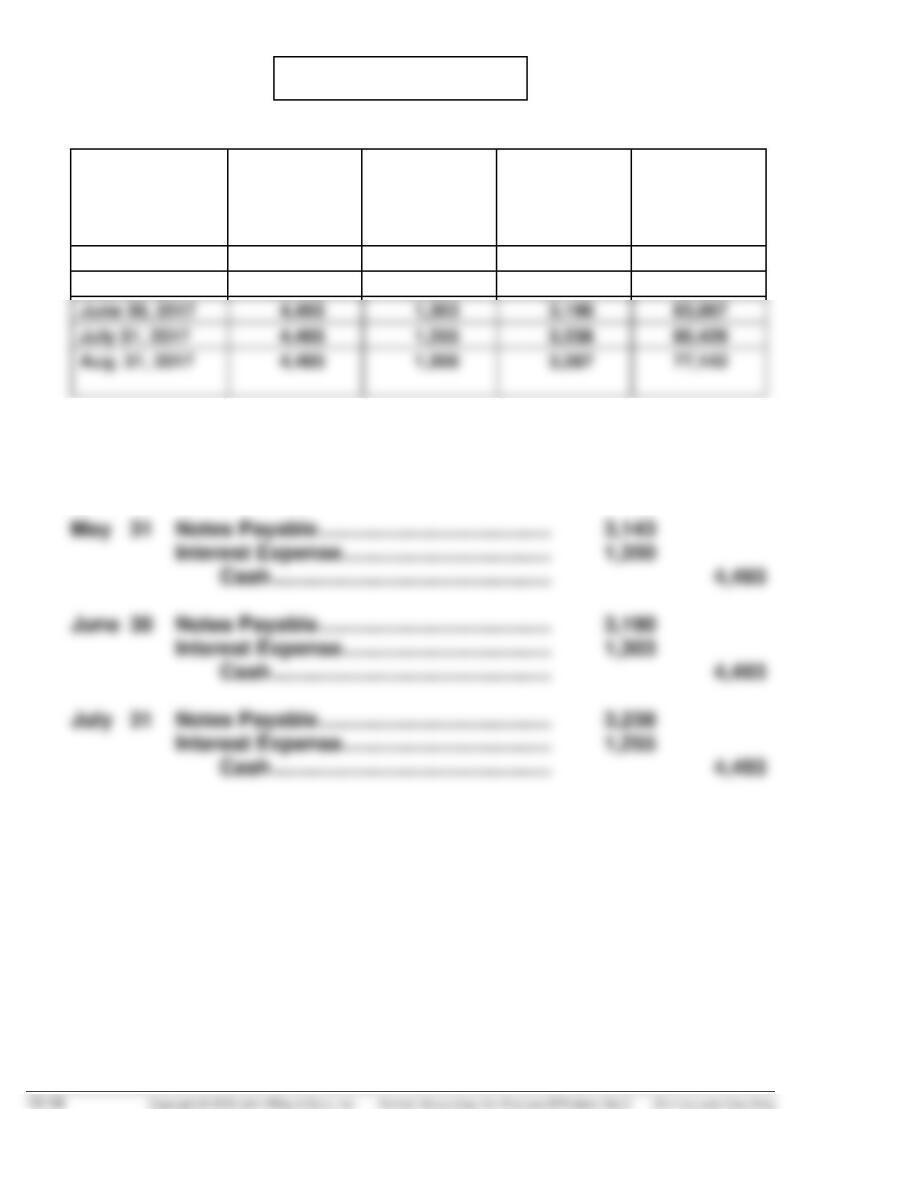

*PROBLEM 10-13C

(a)

Period

Cash

Payment

(A)

Interest

Expense

(B) = (D) X

1.5%

Principal

Reduction

(C) = (A) – (B)

Balance

(D) = (D) – (C)

May 1, 2017

$90,000

May 31, 2017

$4,493

$1,350

$3,143

86,857

(b) May 1 Cash ....................................................... 90,000

Notes Payable ................................ 90,000