10–21

PROBLEM 10-35 (15 MINUTES)

Direct

Material

Initial

Mix

Unit

Cost

Standard

Material

Cost

Nyclyn ……………………………………………………………

12 kg

R$ 4.35

R$ 52.20

Salex ……………………………………………………………..

9.6 ltr

R$ 5.40

51.84

Protet …………………………………………………………….

R$ 7.20

PROBLEM 10-36 (45 MINUTES)

1. Type I fertilizer:

Price variance:

Actual quantity used x actual price

3,700 pounds x $ .53………………………………

$1,961

Actual quantity used x standard price

3,700 pounds x $ .50………………………………

Quantity variance:

Actual quantity used x standard price

$1,850

Standard quantity allowed x standard price

$ 350 Favorable

Purchase price variance:

Actual quantity purchased x actual price

$2,650

Actual quantity purchased x standard price

$ 150 Unfavorable

* 40 pounds x 55 clients x 2 applications/client

10–22

PROBLEM 10-36 (CONTINUED)

Type II fertilizer:

Price variance:

Actual quantity used x actual price

7,800 pounds x $ .40…………………………….

$3,120

Actual quantity used x standard price

7,800 pounds x $ .42…………………………….

$ 156 Favorable

Quantity variance:

Actual quantity used x standard price

$3,276

Standard quantity allowed x standard price

$ 420 Favorable

Purchase price variance:

Actual quantity purchased x actual price

$4,000

Actual quantity purchased x standard price

$ 200 Favorable

* 40 pounds x 55 clients x 4 applications/client

2. Direct-labor variances:

Rate variance:

Actual hours used x actual rate

$1,897.50

Actual hours used x standard rate

$ 412.50 Unfavorable

Chapter 10 – Standard Costing and Analysis of Direct Costs

PROBLEM 10-36 (CONTINUED)

Efficiency variance:

$1,485.00

$ 495.00 Favorable

* 2/3 hours x 55 clients x 6 applications

3. Actual cost of applications:

Type I fertilizer:

Actual quantity used x actual price (3,700 pounds x $ .53)….

$1,961.00

Type II fertilizer:

Actual quantity used x actual price (7,800 pounds x $ .40)….

Direct labor:

$6,978.50

10–24

PROBLEM 10-36 (CONTINUED)

4. (a) Yes, the service was a success. Overall costs were controlled, with each of

the three cost components (Type I fertilizer, Type II fertilizer, and direct labor)

producing a net favorable variance on usage, and an overall favorable

(b) In this case, several of the favorable variances may have come back to haunt

Wolfe. The favorable labor efficiency variance means that less time is being

5. This is a management judgment for Wolfe to make. If the service is continued, Wolfe

10–25

PROBLEM 10-37 (35 MINUTES)

1. a. Machine hours x 4 = standard direct-labor hours

2.

a. Standard

Direct-Labor

Cost*

b. 20% of the

Standard Direct-

Labor Cost*

January …………………………………………………….

$ 9,983

$1,997

February …………………………………………………..

6,050

1,210

March ……………………………………………………….

33,297

6,659

April …………………………………………………………

43,056

8,611

May …………………………………………………………..

9,651

1,930

June …………………………………………………………

13,994

2,799

July ………………………………………………………….

6,273

1,255

August ……………………………………………………..

5,791

1,158

September ………………………………………………..

5,791

1,158

October …………………………………………………….

4,343

10–26

PROBLEM 10-37 (CONTINUED)

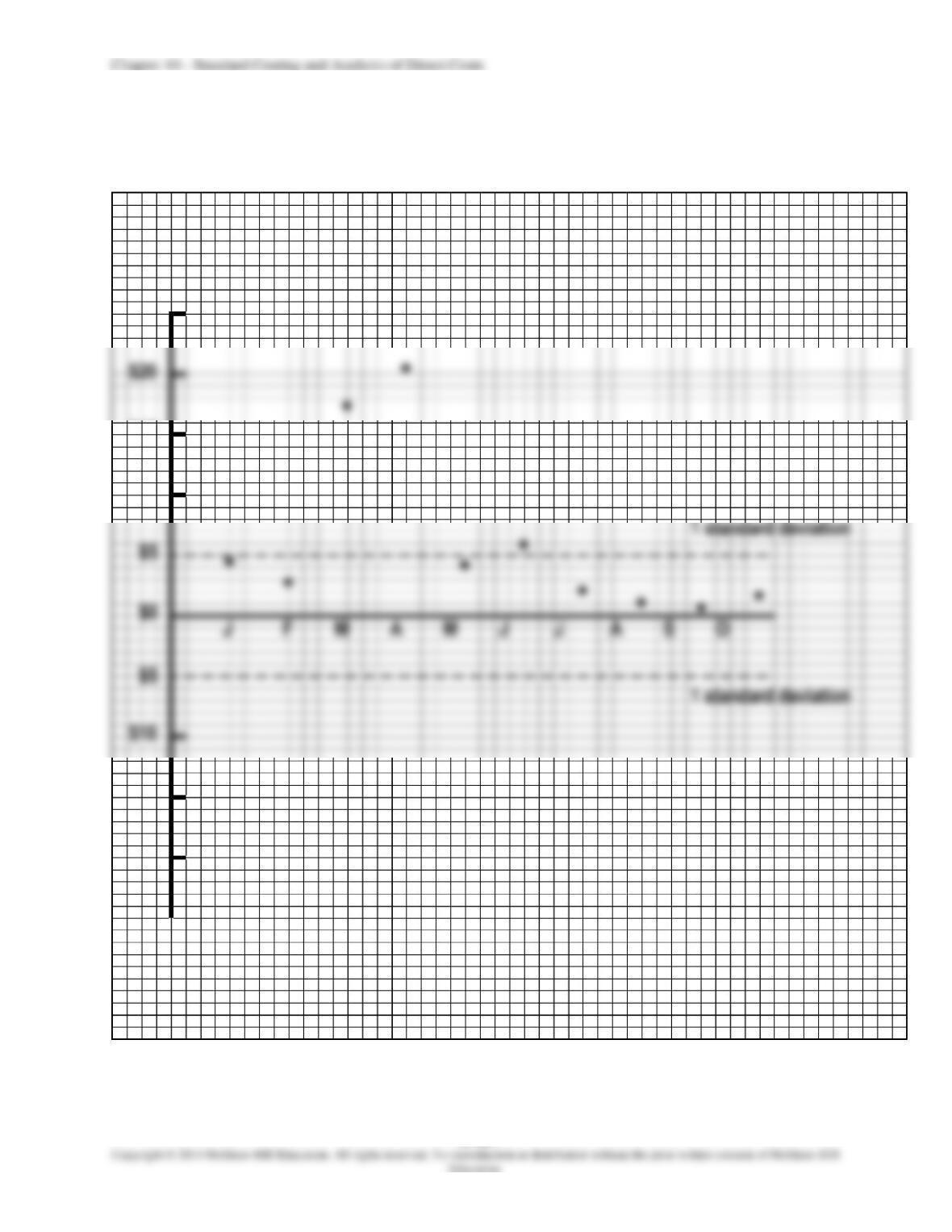

4. Statistical control chart for direct-labor efficiency variances:

$5

$0

$5

$10

$10

$15

$20

$25

$15

$20

$25

Favorable variances

(in thousands)

Unfavorable variances

(in thousands)

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–27

PROBLEM 10-37 (CONTINUED)

10–28

PROBLEM 10-38 (35 MINUTES)

1.

Schedule of standard production costs:

VALPORT VALVE COMPANY: SHREVEPORT PLANT

SCHEDULE OF STANDARD PRODUCTION COSTS: BASED ON 15,600 UNITS

FOR THE MONTH OF MARCH

Standard

Costs

Direct material ………………………………………………

15,600 units 3 lbs. $5.00

$ 234,000

Direct labor …………………………………………………..

877,500

2.

Variances:

a.

Direct-material price variance

=

(AQ

AP) – (AQ

SP)

=

b.

Direct-material quantity variance

=

(AQ

SP) – (SQ

SP)

=

$3,000 Favorable

c.

Direct-material purchase

=

$10,000 Unfavorable

d.

Direct-labor rate variance

=

(AH

=

$24,060 Favorable

10–29

PROBLEM 10-38 (CONTINUED)

e.

Direct-labor efficiency variance

=

(AH

SR) – (SH

SR)

=

$24,750 Unfavorable

PROBLEM 10-39 (30 MINUTES)

1. No. The variances are favorable and small, with each being less than 2% of

2. Direct-material variances:

Price variance*:

Actual quantity purchased/used x actual price

45,000 pounds x $7.70…………………………….

$346,500

Actual quantity purchased/used x standard price

$ 49,500 Favorable

Quantity variance:

Actual quantity used x standard price

45,000 pounds x $8.80……………………………

$396,000

Standard quantity allowed x standard price

39,900 pounds* x $8.80…………………………..

$ 44,880 Unfavorable

* 9,500 units x 4.2 pounds

Total direct-material variance:

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–30

PROBLEM 10-39 (CONTINUED)

Direct-labor variances:

Rate variance:

Actual hours used x actual rate

$339,625

Actual hours used x standard rate

$ 47,025 Unfavorable

Efficiency variance:

Actual hours used x standard rate

$292,600

Standard hours allowed x standard rate

$ 53,200 Favorable

* 9,500 units x 2.6 hours

Total direct-labor variance:

$47,025U + $53,200F = $6,175F

3. Yes. Although the combined variances are small, a more detailed analysis reveals

4. No, things are not going as smoothly as the vice president believes. With regard to

the new supplier, SolarPrime is paying less than expected for direct materials

10–31

PROBLEM 10-39 (CONTINUED)

5. Yes. Hoctor is the production supervisor. The prices paid for materials and the

quality of material acquired are normally the responsibility of the purchasing

PROBLEM 10-40 (30 MINUTES)

1.

Variances (U denotes unfavorable; F denotes favorable):

a.

Direct-labor rate variance for each labor class:

Labor

Class

Actual

Rate

Standard

Rate

Difference

in Rates

Actual

Hours

Rate

Variance

III

$25.80

$24.00

$1.80

1,100

$1,980 U

1,300

I

750

b.

Direct-labor efficiency variance for each labor class:

Labor

Class

Actual

Hours

Standard

Hours*

Difference

in Hours

Standard

Rate

Efficiency

Variance

III

1,100

1,000

100

$24.00

$2,400 U

1,300

300

21.00

6,300 U

1,000

15.00

(3,750) F

*Given April’s output of production.

10–32

PROBLEM 10-40 (CONTINUED)

2.

The advantages of not changing the labor rate would include (1) comparison of actual

operating results to a fixed base which was previously approved by management, and

PROBLEM 10-41 (30 MINUTES)

1.

a.

Responsibility for setting standards:

Materials:

Labor:

The development of standard prices for material is primarily the responsibility of

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–33

PROBLEM 10-41 (CONTINUED)

b.

The factors that should be considered in establishing material standards include

the following:

• Price studies, including expected general economic conditions, industry

prospects, demand for the materials, and market conditions.

2.

The basis for assignment of responsibility under a standard-costing system is

controllability. Judgments about whether departments or department managers are

10–34

PROBLEM 10-42 (40 MINUTES)

1. The standard cost per 10-gallon batch of strawberry jam is determined as follows:

Strawberries (7.5 qts.* $1.60) …………………………………….

$12.00

Sorting labor (3/60 hr. 6 qt. $18.00) …………………………

Packaging (40 qt.† $.76) …………………………………………….

Total standard cost per 10-gallon batch ………………………..

2.

Joe Adams’ behavior regarding the cost information is unethical because it

violates the following ethical standards (refer to the IMA Statement of Ethical

Professional Practice in the “Focus on Ethics” of Chapter 1):

3.

a.

In general, the purchasing manager is held responsible for unfavorable material

purchase price variances. Causes of these variances include the following:

PROBLEM 10-42 (CONTINUED)

b.

In general, the production manager is held responsible for unfavorable labor

efficiency variances. Causes of these variances include the following:

PROBLEM 10-43 (40 MINUTES)

1.

Variances to be investigated using rule of thumb:

Variance Type

Month

Amount

Percentage of

Standard Cost

Efficiency …………………….

August …………….

76,000 U ………………

7.60%

Efficiency …………………….

September ……….

74,000 U ………………

7.40%

Efficiency …………………….

October ……………

84,000 U ………………

8.40%

Efficiency …………………….

November ………..

120,000 U ………………

Efficiency …………………….

December ………..

104,000 U ………………

2.

The company’s direct-labor efficiency variances exhibit a consistent unfavorable

trend throughout the year. Beginning in January with an unfavorable variance of

3.

It is important to follow up on favorable variances. A consistent pattern of favorable

variances, a favorable trend, or a large favorable variance may indicate that

10–36

PROBLEM 10-43 (CONTINUED)

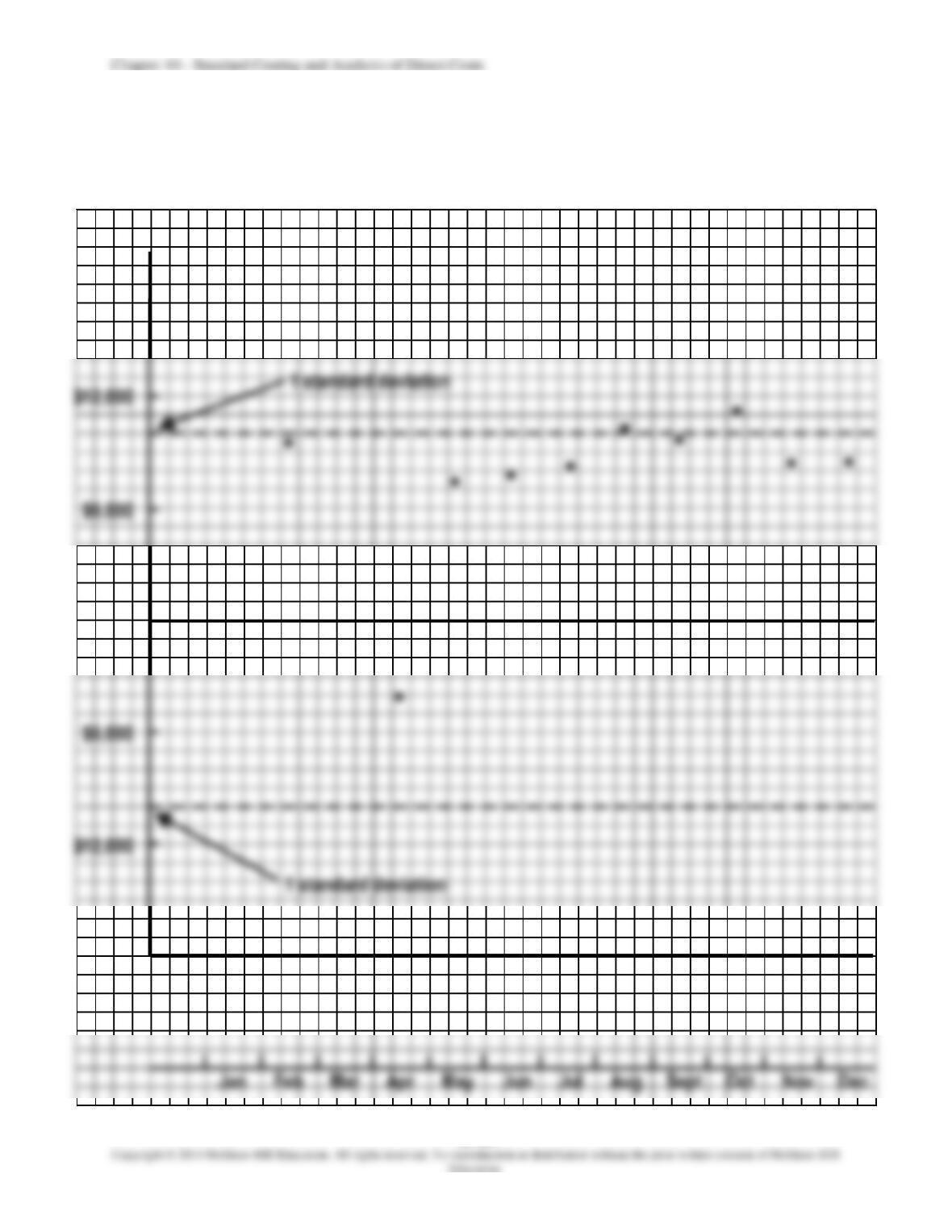

4. Statistical control chart: investigate August and October variances.

1 standard deviation

•

•

1 standard deviation

Time

Favorable variances

0

Unfavorable variances

•

•

10–37

PROBLEM 10-44 (35 MINUTES)

1.

At California Housewares’ Merced Division, the standard cost per cutting board is

calculated as follows:

Direct material:

Lumber (1.5 board ft.* $4.00 per board ft.) ……………

$6.00

Direct labor:

Prepare and cut (14.4†/60 hr. $8.00 per hr.) …………..

$1.92

2.

a.

The role of the purchasing manager in the development of standards includes

establishing the standard cost for material required by the bill of materials,

b.

The role of the industrial engineer in the development of standards includes

preparing the bill of materials that specifies the types and quantities of material

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–38

PROBLEM 10-44 (CONTINUED)

3.

a.

Standard costing allows for management by exception. Timely reporting of

variances allows management to take corrective action before costs get out of

hand. The breakdown of variances into various components helps management

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–39

PROBLEM 10-45 (25 MINUTES)

1.

(a)

Direct-material purchase price variance = PQ(AP – SP)

Product

Calculation

PQ(AP – SP)

Purchase

Price

Variance

Standard tent ………………

4,200 ($6.40* – $6) …………………………..

$1,680 U

Deluxe tent ………………….

1,600 ($7.90† – $8) …………………………..

(b)

Direct-material quantity variance = SP(AQ – SQ)

Product

Calculation

SP(AQ – SQ)

Quantity

Variance

Standard tent ……………..

$6 (2,500 – 2,400*) …………………………...

$600 U

Deluxe tent …………………

$8 (1,440 – 1,440†) …………………………...

Chapter 10 – Standard Costing and Analysis of Direct Costs

10–40

PROBLEM 10-45 (CONTINUED)

2.

Raw-Material Inventory ………………………………………..

38,000*

Direct-Material Purchase Price Variance ……………….

Accounts Payable ………………………………………

To record purchase of tent fabrics.

25,920*

Direct-Material Quantity Variance …………………………

Raw-Material Inventory ……………………………….

To record use of direct material.