297

CHAPTER 10

ACCOUNTING SYSTEMS FOR

MANUFACTURING OPERATIONS

CLASS DISCUSSION QUESTIONS

1. Managerial accounting differs from financial

accounting in the following ways:

(1) Financial accounting records and re-

ports transactions and events using

generally accepted accounting princi–

ples (GAAP), while managerial account-

ing is not restricted by specific rules.

That is, managerial accounting records

and reports whatever information is use–

ful to management for decision making.

pany or its segments.

2. For a company that produces desktop com-

puters, memory chips would be considered

a direct materials cost. For a cost to be con-

sidered a direct materials cost, the cost must

be an integral part of the finished product

and a significant portion of the total cost of

the product.

3. Product cost information is used by manag-

ers to (1) establish product prices, (2) con-

trol operations, and (3) develop financial

statements.

c. Process cost systems accumulate costs

for each department or process within a

factory.

5. Job order costing is used by firms that sell

custom goods and services to customers.

6. Materials should not be issued by the store-

keeper without a properly authorized materi-

als requisition. Both the storekeeper and the

recipient of the materials should initial the

materials requisition when the materials are

9. The use of a predetermined factory over-

head rate in job order cost accounting

assists management in pricing jobs. By

estimating the cost of direct materials and

direct labor based on past experience and

by applying the factory overhead rate, the

cost of a job can be estimated. The prede-

termined rate also permits the determination

of the cost of a job shortly after it is finished,

which enables management to adjust future

pricing policies to achieve the best combina-

298

b. Direct labor cost, direct labor hours, and

machine hours.

b. Underapplied

12. The simplest satisfactory procedure for

disposing of a relatively minor balance in the

factory overhead account is to transfer it to

Cost of Goods Sold.

13. Product costs are composed of three

elements of manufacturing costs: direct

materials cost, direct labor cost, and factory

overhead cost. These costs are treated as

assets until the product is sold. Product

consulting, advertising, or legal services.

Job cost sheets would accumulate all direct

be transferred to the cost of services on the

income statement.

15. a. The objective of JIT processing is to

produce products with high quality, low

cost, and instant availability.

b. JIT processing combines traditional

manufacturing functions into work cen-

ters where workers are cross-trained to

complete several functions. Also, ser-

vice activities such as repair and

299

EXERCISES

E10–1

a. Direct materials cost

e. Factory overhead cost

E10–2

a. Direct materials cost

f. Factory overhead cost

E10–3

a, b, d, f, g

E10–4

a. Period cost

b. Period cost

c. Period cost

d. Product cost

j. Product cost

k. Period cost

l. Period cost

m. Product cost

E10–5

a. period

b. plant depreciation

e. direct materials

f. process

300

E10–6

a. Materials requisitioned for use (both direct and indirect)

b. Factory labor used (both direct and indirect)

c. Application of factory overhead costs to jobs

E10–7

a.

Cost of goods sold:

Sales ……………………………………………………………………….. $375,000

Less gross profit ……………………………………………………… (120,000)

Cost of goods sold …………………………………………………… $255,000

b.

Direct materials cost:

Materials purchased …………………………………………………. $200,000

Less: Indirect materials ……………………………………………. $ 15,000

Materials inventory …………………………………………. 25,000 (40,000)

Direct materials cost ………………………………………………… $160,000

301

E10–8

a.

RECEIVED ISSUED BALANCE

Receiving

Report

Number

Quantit

y

Unit

Price

Materials

Requi-

sition

Number

Quantit

y

Amount

Date

Quantit

y

Amount

Unit

Price

Jul

y

1 250 $1,500 $6.00

309 400 $7.50 July 5 250 1,500 6.00

400 3,000 7.50

7401 480 $3,225* Jul

y

10 170 1,275 7.50

422 800 8.00 July 20 170 1,275 7.50

y

b. Ending wire cable balance:

320 at $8.00 ………………………………………………………. $2,560

c. Work in Process ($3,225 + $5,115) ………………………….. $8,340

d. Comparing quantities on hand as reported in the materials ledger with pre-

302

E10–9

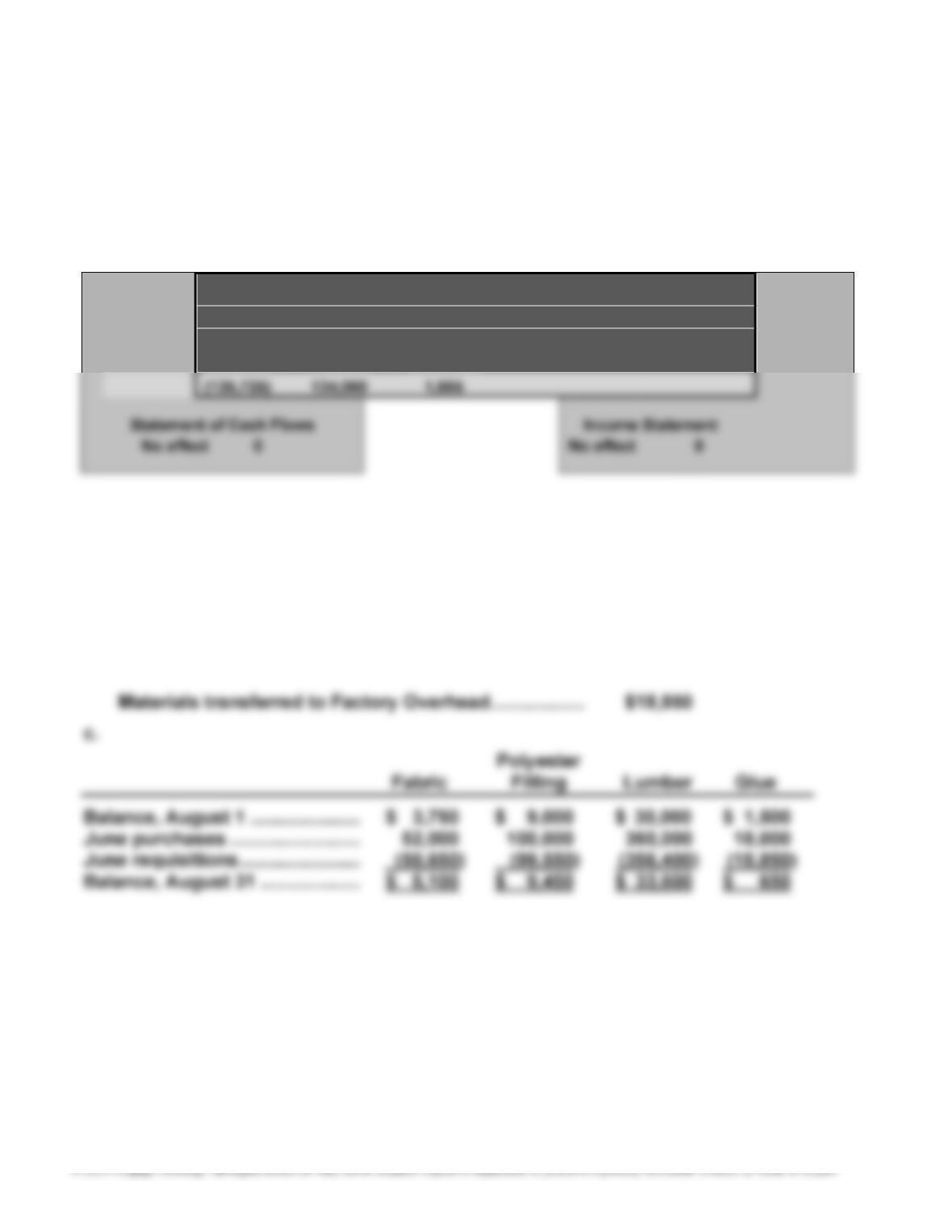

a. Materials transferred to Work in Process: $134,060*

Materials transferred to Factory Overhead: $1,665

*$134,060 = $56,425 + $38,810 + $14,275 + $24,550

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Work in Factor

y

Materials + Process + Overhead

E10–10

a. Materials purchases ……………………………………………… $530,000*

*$52,000 + $100,000 + $360,000 + $18,000

b. Materials transferred to Work in Process ……………….. $506,600*

*$50,650 + $99,550 + $356,400

303

E10–11

a. Factory labor costs transferred to Work in Process: $80,700*

*$80,700 = $5,000 + $11,150 + $9,440 + $18,060 + $20,200 + $13,250 + $3,600

Factory labor costs transferred to Factory Overhead: $14,000

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Work in Factory Wages

E10–12

a. Factory labor costs transferred to Work in Process: $2,900

Factory labor costs transferred to Factory Overhead: $260

Supporting Calculations:

Labor Costs (Hourly Rate × Hours)

Direct

Labor

Hourly (sum of Indirect

Rate Job 560A Job 560B Job 560C job costs) Labor

304

E10–13

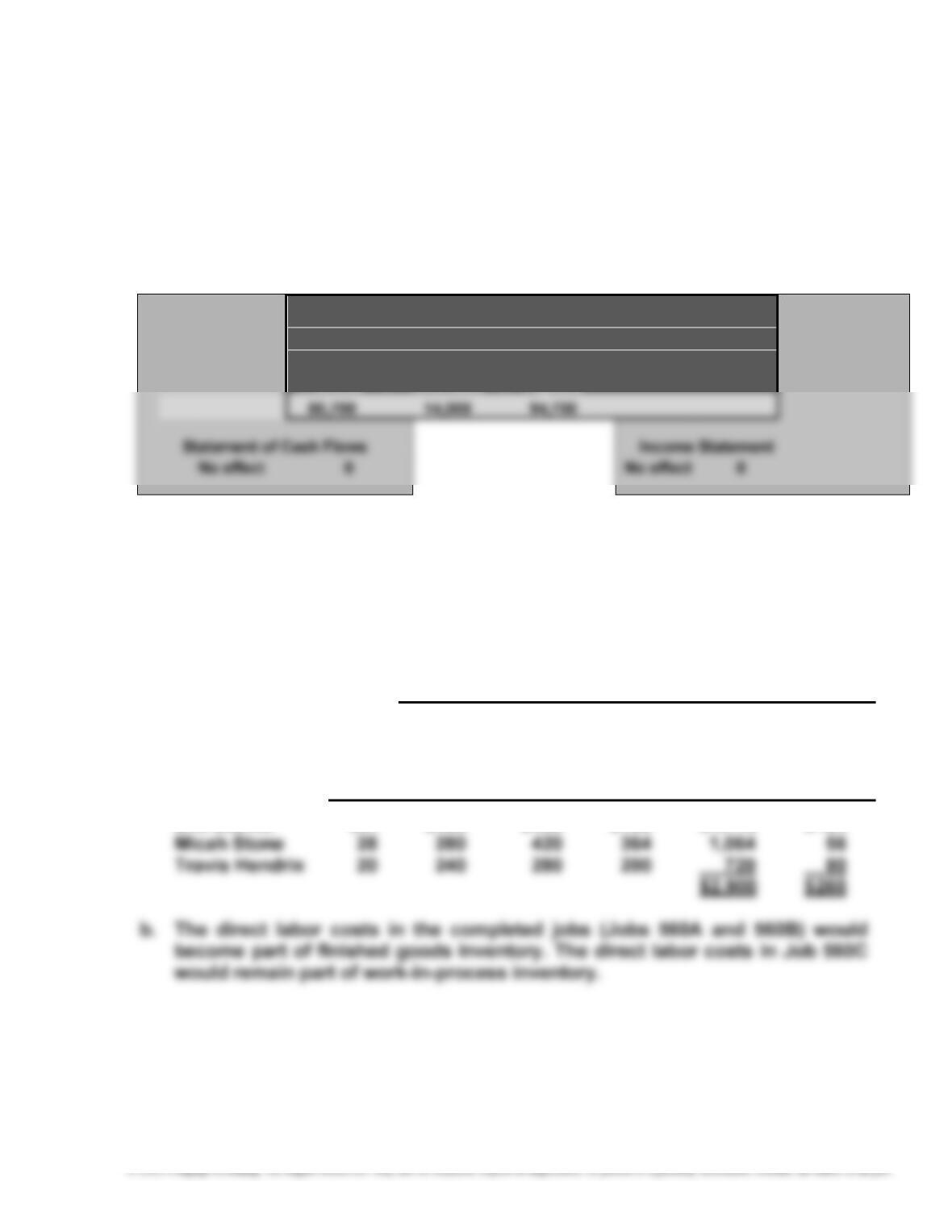

a. Factory labor costs transferred to Work in Process: $ 18,000*

Factory labor costs transferred to Factory Overhead: $1,750

*$6,400 + $3,900 + $4,800 + $2,900 = $18,000

c.

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Work in Factor

y

Process + Overhead

21,600 (21,600)

Statement of Cash Flows Income Statement

No effect 0 No effect 0

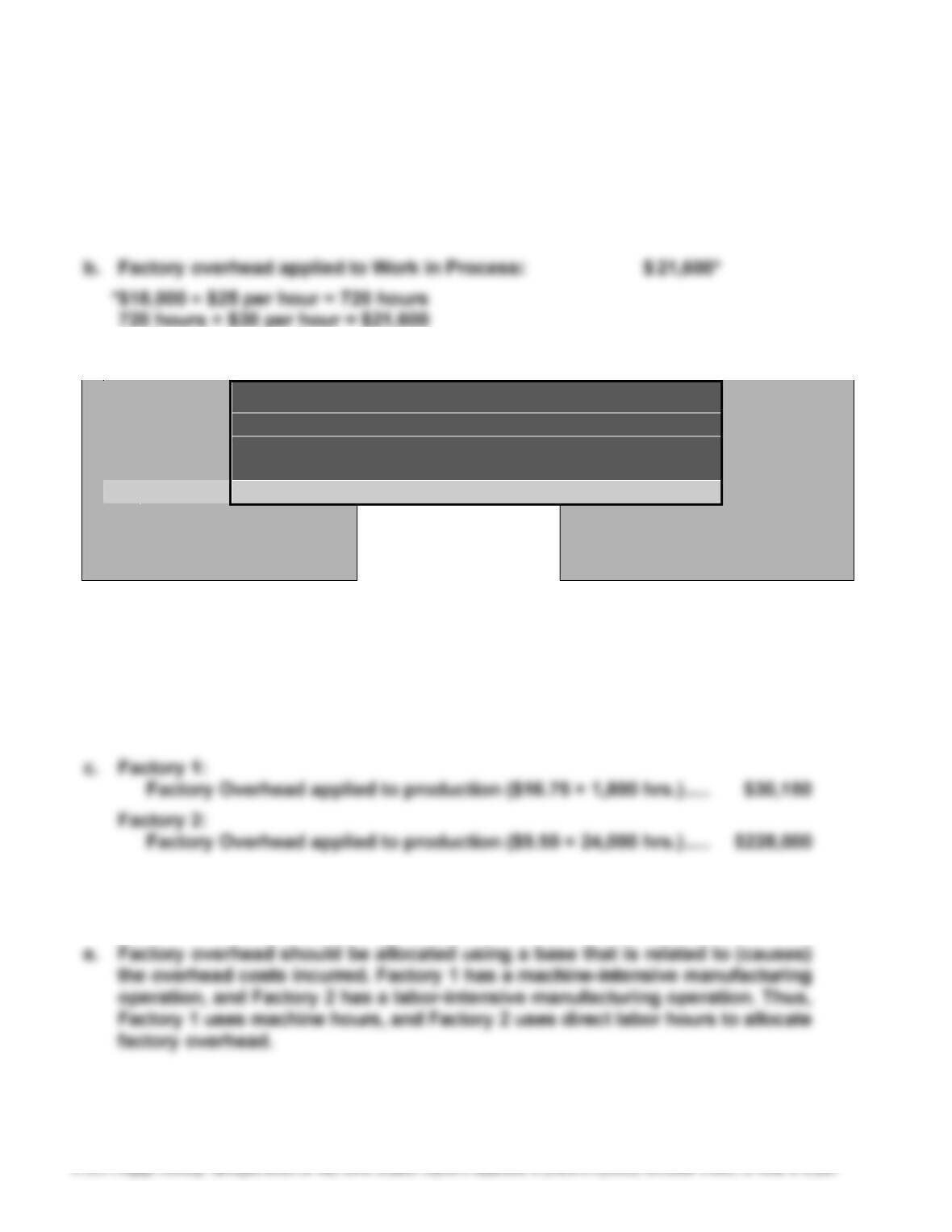

E10–14

a. Factory 1: $16.75 per machine hour = $375,200 ÷ 22,400 machine hours

b. Factory 2: $9.50 per direct labor hour = $2,660,000 ÷ 280,000 direct labor

hours

d. Factory 1: $(1,450) negative (overapplied) ($28,700 – $30,150)

Factory 2: $2,000 positive (underapplied) ($230,000 – $228,000)

305

E10–15

The estimated shop overhead is determined as follows:

Shop and repair equipment depreciation ………………………………….. $ 91,000

Shop supervisor salaries …………………………………………………………. 250,000

Shop property taxes ………………………………………………………………… 40,000

Shop supplies …………………………………………………………………………. 15,000

Total shop overhead …………………………………………………………… $396,000

E10–16

a. Estimated annual operating room overhead: $1,260,000

Estimated operating room activity base (number of operating room hours):

Hours per day …………………………………………………………… 12

Days per week ………………………………………………………….. × 7

Weeks per year (less repairs & maintenance weeks) …… × 50

Estimated annual operating room hours ……………………. 4,200

Predetermined surgical overhead rate:

306

E10–16, Concluded

c. Actual hours used in March …………………………………… 330

Predetermined surgical room overhead rate …………… × $300

Surgical room overhead applied, March …………………. $ 99,000

E10–17

a. Cost of jobs completed and transferred to

Finished Goods: $825,000*

*$180,000 + $225,000 + $140,000 + $280,000 = $825,000

b. Cost of unfinished jobs at October 31:

E10–18

a. Direct materials used and transferred to Work in Process: $13,200*

*$13,200 = $4,000 + $5,000 + $2,700 + $1,500

Indirect materials used and transferred to Factory Overhead: $2,000

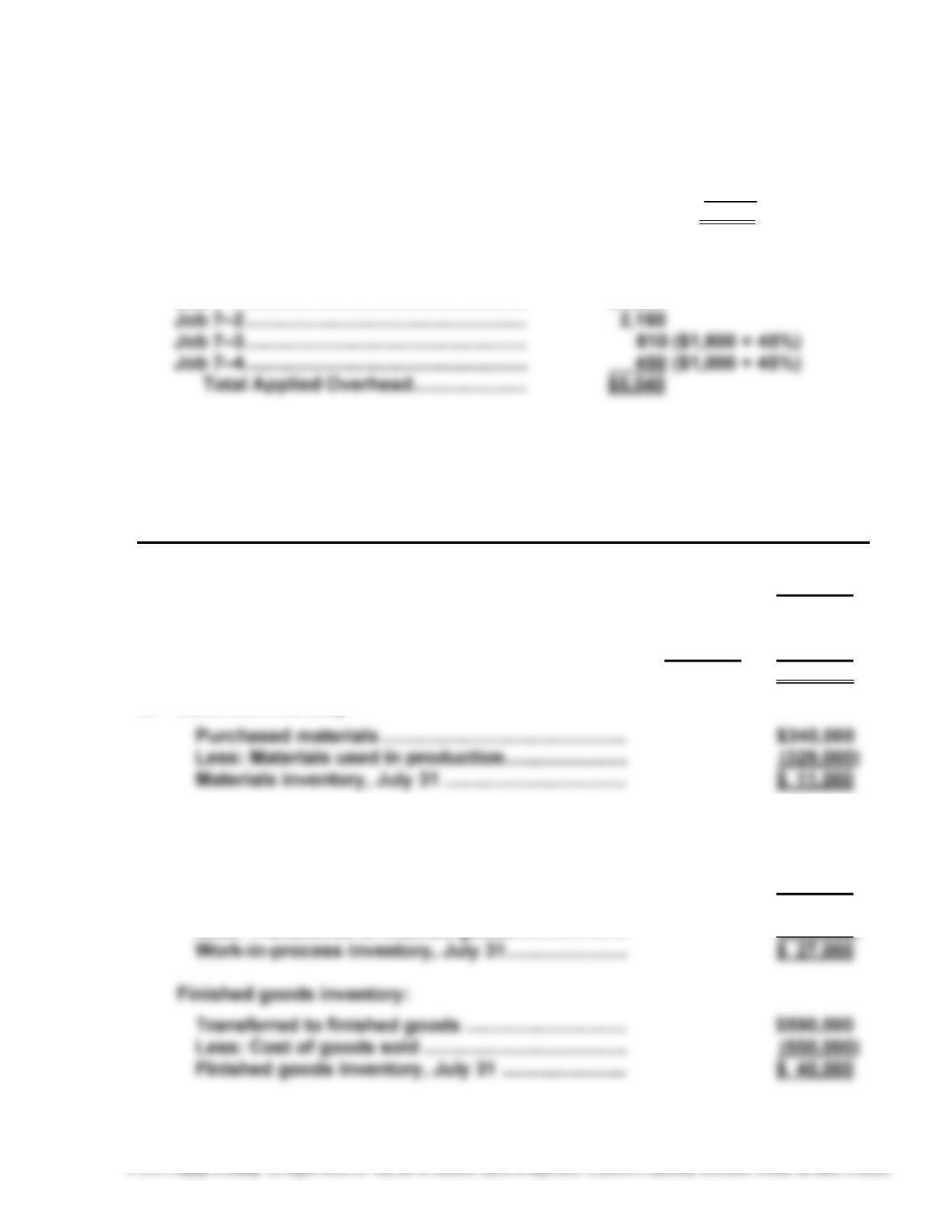

d. Cost of completed Jobs 7-01 and 7-02 ……………………. $21,180*

*$9,220 + $11,960

307

E10–18, Concluded

e. Actual factory overhead incurred …………………………… $5,150*

Factory overhead applied to jobs during July …………. (5,040)**

Underapplied factory overhead for July ………………….. $ 110

*$2,000 + $1,650 + $1,500 = $5,150

Applied Overhead**

Job 7–1 ……………………………………………… $1,620

E10–19

a. BRIDGER BIKES INC.

Income Statement

For the Month Ended July 31, 20Y6

Revenues …………………………………………………………………. $918,000

Cost of goods sold …………………………………………………… (550,000)

Gross profit ……………………………………………………………… $368,000

Selling expenses ………………………………………………………. $132,500

Administrative expenses …………………………………………… 80,000 (212,500)

Operating income …………………………………………………….. $155,500

b. Materials inventory:

Work-in-process inventory:

Materials used in production …………………………… $329,000

Direct labor …………………………………………………….. 160,000

Factory overhead (80% × $160,000) ………………….. 128,000

Additions to work in process …………………………… $617,000

308

E10–20

a. Direct labor costs for April …………………………………… $ 434,000

b. Media purchases for April ……………………………………. $1,300,000

c. Overhead applied during April (40% × $1,300,000) … $ 520,000

E10–21

The CEO must not have been listening very closely at the conference. Just-in-

time is not primarily an inventory reduction method. Just-in-time is a process

improvement philosophy that focuses on reducing time, cost, poor quality, and

uncertainty from a process. Large inventories are merely a symptom of poorly

designed processes. Thus, the CEO’s statement is naive. The company must first

309

E10–22

This is an actual situation facing the U.S. apparel industry. Warren Featherbone

and other U.S.-based apparel manufacturers are discovering the strategic power

of just-in-time. Rather than competing with the offshore manufacturers on price,

these companies are providing smaller quantities with much faster delivery. The

retailer is able to order and receive goods in smaller, more frequent batch sizes.

As a result, the retailer is able to move with fashion trends more quickly. If, for

example, a particular style is proving popular, the domestic manufacturer can

E10–23

Piecework compensation is a characteristic of a traditional manufacturing philos-

ophy that is inconsistent with just-in-time. Under just-in-time, workers are viewed

not just as laborers but as valuable assets of the company. The company wants

workers to also bring their minds to the job. Thus, workers should be compen-

sated for contributing to process improvements, for training themselves to work

other jobs in the cell, and for managing themselves. This might involve an hourly

310

E10–24

a.

A B C D E F G

1 Patient Franklin Patient Krame

r

2 Activity

Activity

Usage ×

Activity

Rate

Activity

= Cost

Activity

Usage ×

Activity

Rate

Activity

= Cost

3 Room and

meals

1 days $225 per day $ 225 4 days $225 per day $ 900

b. Patient Kramer apparently had a more serious condition than did Patient

311

E10–25

a.

UMBRELLA INSURANCE COMPANY

Product Profitability Report

For the Year Ended December 31, 20Y2

Workers’

Auto Comp. Homeowners

Premium revenue …………………………….. $ 7,200,000 $ 6,500,000 $ 9,200,000

Less estimated claims ……………………… (5,040,000) (4,550,000) (6,440,000)

Underwriting income ……………………….. $ 2,160,000 $ 1,950,000 $ 2,760,000

Administrative activities:*

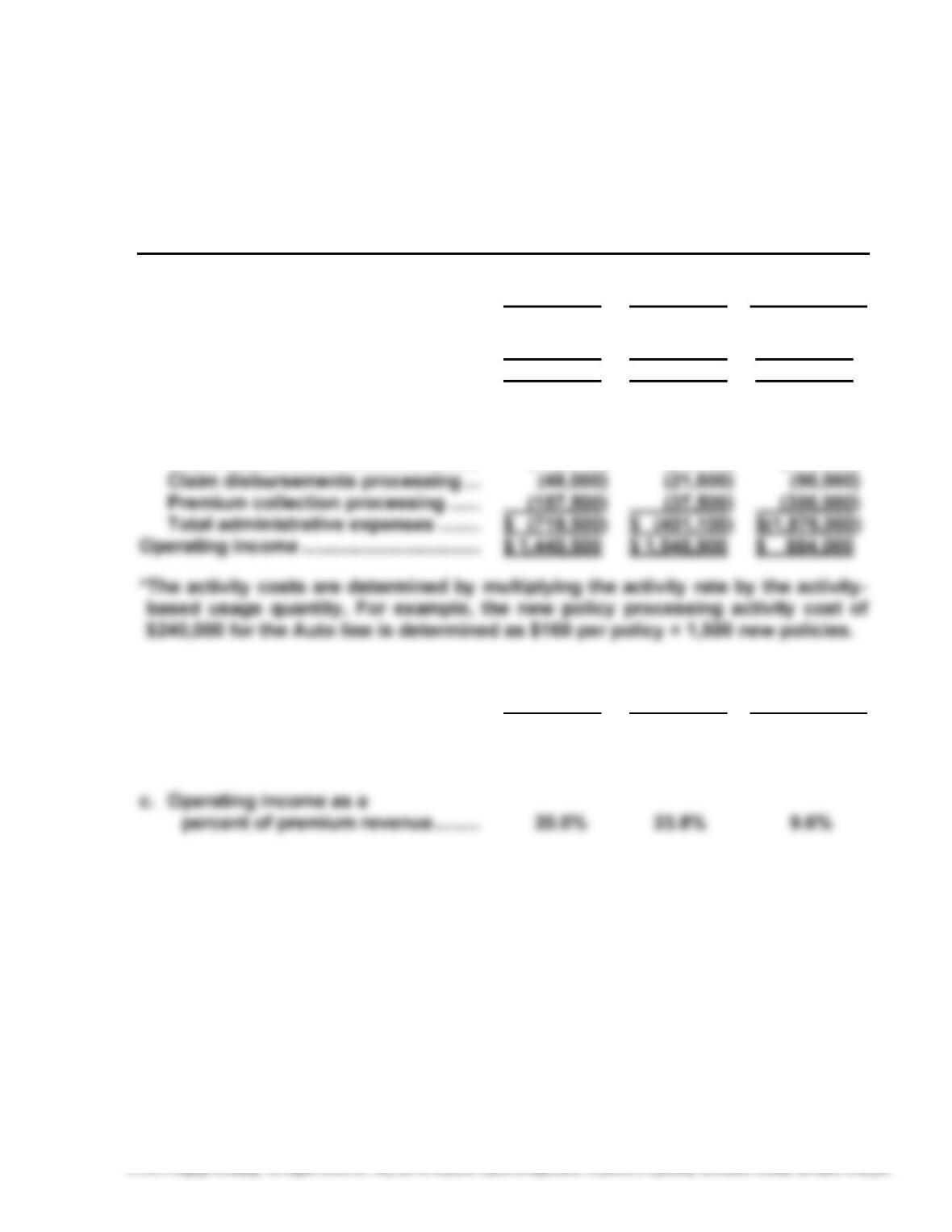

New policy processing ………………… $ (240,000) $ (232,000) $ (656,000)

Cancellation processing ……………… (84,000) (60,000) (480,000)

Claim audits ……………………………….. (160,000) (50,000) (350,000)

b. Workers’

Auto Comp. Homeowners

Underwriting income as a

percent of premium revenue ……… 30.0% 30.0% 30.0%

312

E10–25, Concluded

d. All three insurance lines have the same percentage of underwriting income to

premium revenue (30%). The differences among the insurance lines are in the

way they consume administrative activities. For example, the Homeowners

insurance line has the least profitability due to its high use of administrative

313

PROBLEMS

P10–1

Product Costs Period Costs

Direct Direct Factory

Materials Labor Overhead Selling Administrative

Cost Cost Cost Cost Expense Expense

a. X

b. X

c. X

k. X

l. X

m. X

n. X

o. X

p. X

q. X

r. X