CASE 1.3

JUST FOR FEET, INC.

Synopsis

Harold Ruttenberg emigrated to the United States from South Africa in 1976. In his early thirties

at the time and the father of three small children, Ruttenberg wanted to escape the political and

In 1988, Ruttenberg sold his existing business and founded Just for Feet, Inc., a retail

“superstore” that sold principally athletic shoes. Over the next decade, Just for Feet opened more

than 300 retail outlets across the United States and became the second largest retailer of athletic

shoes in the nation. Ruttenberg took his company public in 1994. During the late 1990s, Just for

Feet’s common stock was one of the “hottest” securities on Wall Street, thanks to the company’s

impressive operating results, which included twenty-one straight quarterly increases in same-store

sales. Those operating results were even more impressive when one considers the fact that the

athletic shoe “sub–industry” was suffering from severe over-saturation during that time frame.

18 Case 1.3 Just for Feet, Inc.

Just For Feet, Inc.— Key Facts

1. In 1976, Harold Ruttenberg, a successful entrepreneur in South Africa, chose to emigrate to the

U.S. because of the economic and political turmoil in his home country.

3. In 1988, Ruttenberg founded Just for Feet, Inc., a retail company that marketed sports apparel,

principally athletic shoes, from large “superstores.”

4. From 1988 through 1998, Just for Feet’s revenues and profits grew dramatically; by 1998, the

5. In mid-1999, Just for Feet shocked the investing public by announcing that it would report its

7. A series of investigations by state and federal authorities revealed that Just for Feet’s impressive

operating results during the 1990s had been the product of a large-scale accounting fraud.

8. The three principal elements of the accounting fraud were improper accounting for vendor

10. The principal criticisms of Deloitte’s audits included the improper application of confirmation

11. Deloitte was fined $375,000 by the SEC for its deficient Just for Feet audits; the SEC suspended

the 1998 audit engagement partner for two years and the audit manager for one year.

12. At the same time that the SEC announced the sanctions imposed on Deloitte for its Just for Feet

Case 1.3 Just for Feet, Inc. 19

Instructional Objectives

1. To demonstrate the need for auditors to employ analytical procedures during the planning phase

of an audit to identify high-risk accounts.

3. To understand the nature and purpose of audit confirmations.

Suggestions for Use

This case can be integrated with the coverage of several different topics in an undergraduate or

graduate auditing course. Exhibits in this case present Just for Feet’s financial statements for the

final three years that it was fully operational, namely, fiscal 1996 through fiscal 1998. Instructors

can use those financial statements as the basis for a major analytical procedures assignment—see the

Suggested Solutions to Case Questions

20 Case 1.3 Just for Feet, Inc.

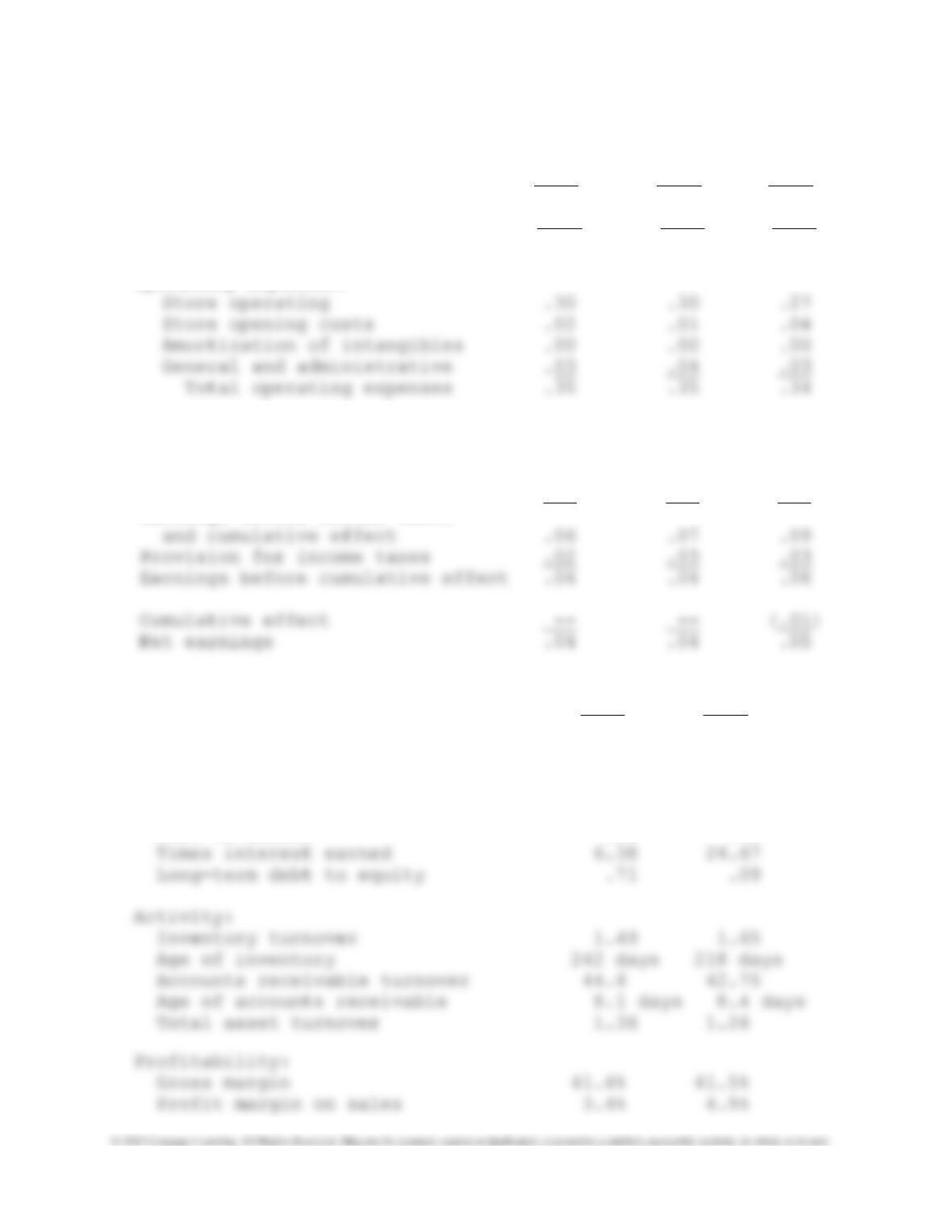

1. Common-sized balance sheets for Just for Feet’s 1996-1998 fiscal years: [Note: each fiscal year

ended on January 31 of the following year. For example, fiscal 1998 ended on January 31, 1999.]

1998 1997 1996

Current assets:

Cash .02 .19 .37

Short–term borrowings .00 .20 .27

Accounts payable .14 .12 .10

Accrued expenses .04 .02 .01

Income taxes payable .00 .00 .00

Current maturities of LT debt .01 .01 .01

Total current liabilities .19 .35 .39

Long–term debt and obligations .34 .05 .03

Total liabilities .53 .40 .42

Case 1.3 Just for Feet, Inc. 21

Common-sized income statements for Just for Feet:

1998 1997 1996

Net sales 1.00 1.00 1.00

Cost of sales .58 .58 .58

Gross profit .42 .42 .42

Operating expenses:

Operating income .07 .07 .08

Interest expense (.01) .00 .00

Interest income .00 .00 .01

Earnings before income taxes

Financial Ratios for Just for Feet:

1998 1997

Liquidity:

Current 3.39 2.00

Quick .37 .67

Solvency:

Debt to assets .53 .40

22 Case 1.3 Just for Feet, Inc.

Return on total assets 6.1% 5.5%

Return on equity 9.0% 8.8%

Equations:

Current ratio: current assets / current liabilities

Quick ratio: (current assets – inventory) / current liabilities

Debt to assets: total debt / total assets

Times interest earned: earnings before interest and taxes / interest charges

Long-term debt to equity: long term debt / shareholders’ equity

Selected industry norms as of 1998 (these norms were taken from a Dun & Bradstreet publication;

each industry norm is a mean for the given ratio):

Current ratio: 3.0

Quick ratio: .75

Debt to assets: .37

L-T debt to equity: .14

Following, in bullet form, are the key financial statement items and other issues that are “brought

to the surface” by the common-size financial statements, financial ratios, and other available

information regarding Just for Feet as of the end of fiscal 1998.

1. Clearly, inventory had to be a major focus of the fiscal 1998 audit. At January 31, 1999,

inventory was easily Just for Feet’s largest asset, accounting for almost 60% of the

Case 1.3 Just for Feet, Inc. 23

2. Cash is a financial statement item that is not particularly challenging to audit; however,

auditors must closely monitor a client’s cash and near–cash assets to assess the entity’s

liquidity. A client that has limited cash resources may pose a going-concern issue for its

auditors. Notice the dramatic decline in Just for Feet’s cash resources, both on an absolute

3. Related to the previous item was the sharp increase in Just for Feet’s long-term debt during

1998. Notice that the company’s long-term debt to equity ratio spiked from .09 at the end of

fiscal 1997 to .71 at the end of fiscal 1998. Although the company’s interest coverage ratio

4. Just for Feet’s financial data suggest that accounts payable may have merited more attention

than normal at the end of fiscal 1998. As a general rule, the growth rates of inventory and

5. A final issue that is raised by an analysis of Just for Feet’s 1996-1998 financial data is the

seemingly improbable consistency of certain of the company’s key financial ratios. In

particular, notice how stable the company’s gross margin (profit) percentage was over that

24 Case 1.3 Just for Feet, Inc.

2. (The second part of this question will be addressed first.) The audit risk model, as discussed in

AU Section 312, suggests that there is a direct relationship between control risk and audit risk. That

is, as the level of control risk posed by a client increases, ceteris paribus, there is a greater chance

that an auditor will issue a “clean” opinion when some other type of audit report is appropriate in the

3. This is a “sister” question to Question #2. Again, there is a direct correlation between inherent

risk and overall audit risk. As assessed inherent risk increases, ceteris paribus, overall audit risk

increases as well. To mitigate an increased level of inherent risk, auditors will typically increase the

rigor of their audit NET (nature, extent, and timing of their audit tests), thereby reducing detection

4. As a point of information, the phrase “audit risk factor” is apparently never explicitly defined in

the professional standards. A related phrase, “fraud risk factors” is defined in AU 316.31 as follows:

Case 1.3 Just for Feet, Inc. 25

—the high-risk business strategies applied by management

—the “significant” emphasis that management placed on achieving earnings goals

—management’s aggressive application of accounting standards

—management’s “excessive” interest in maintaining the company’s stock price at a high level

—“unique and highly complex” transactions engaged in by the company near year-end

—the domineering management style of Harold Ruttenberg

—the large increase in vendor allowance receivables from the end of 1997 to the end of 1998

As suggested previously, you might consider having your students complete Question #4 as a

group exercise. After each group has developed its “top five” list, collect those lists and make each

of them available to the entire class. Next, challenge individual groups to defend obvious “outliers”

and/or obvious omissions in their individual rankings.

Did the Deloitte auditors identify and respond appropriately to the audit risk factors just listed?

26 Case 1.3 Just for Feet, Inc.

5. There was a wide range of parties who stood to be affected by the decision of Thomas Shine

regarding whether or not to send a false confirmation to Deloitte & Touche. These parties included,

among others, Just for Feet’s stockholders and potential stockholders, Just for Feet’s lenders and

potential lenders, Just for Feet’s independent auditors, Shine’s own company and the stakeholders in

that organization, his family, and, of course, himself.

individuals should force themselves to “look” well into the future and consider how each decision

alternative, if chosen, may eventually affect their careers, their feelings of self-worth, and other

stakeholders.

An effective approach to addressing this question is to ask students to suggest different ways

that Thomas Shine could have responded to the ethical dilemma he faced. Then, you can engage