Chapter 1 – A Framework for Financial Accounting

Problem 1-3B (concluded)

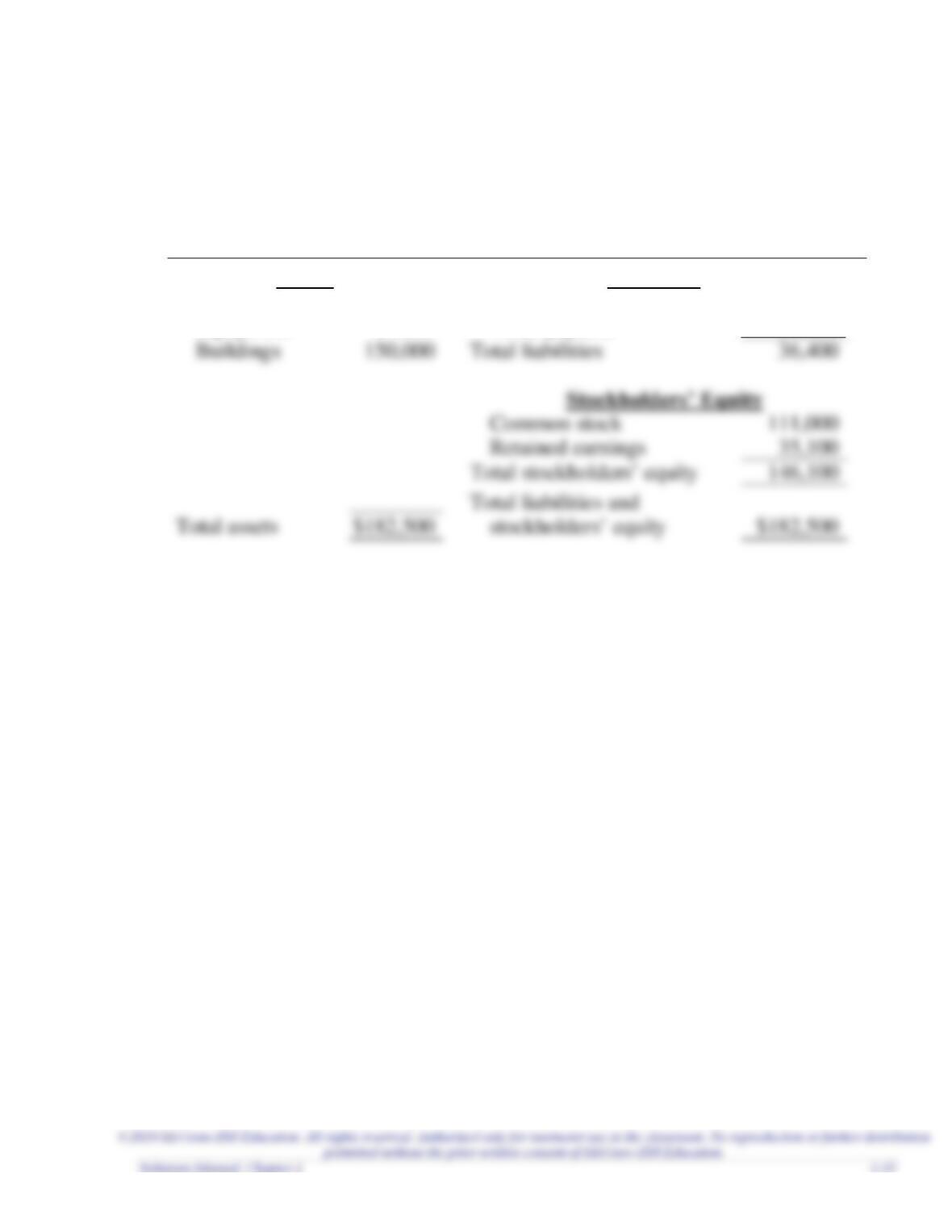

Gator Investments

Balance Sheet

Dec. 31, 2021

Assets

Liabilities

Cash

$ 5,500

Accounts payable

$ 6,400

Equipment

27,000

Notes payable

30,000

Buildings

Total liabilities

Common stock

Total assets

Chapter 1 – A Framework for Financial Accounting

1-36 Financial Accounting, 5e

Problem 1-4B (LO 1-3)

(Suggested order of calculation)

On the statement of stockholders’ equity,

$14,000 + (c) = $17,000

(c) = $3,000

From (g) and (h),

$4,000 + $17,000 (g) + $8,000 (h) = (i)

(i) = $29,000

From total liabilities and stockholders’ equity,

(f) = $29,000

Chapter 1 – A Framework for Financial Accounting

Problem 1-5B (LO 1-3)

Tar Heel Corporation

Income Statement

For the year ended December 31, 2021

Service revenues

$69,400

Expenses:

Net income

Tar Heel Corporation

Statement of Stockholders’ Equity

For the year ended December 31, 2021

Common

Stock

Retained

Earnings

Total

Stockholders’

Equity

Beginning balance

$21,000

$26,800

$47,800

Issuance of common stock

Add: Net income

Less: Dividends

Ending balance

$27,000

Problem 1-5B (concluded)

Tar Heel Corporation

Balance Sheet

December 31, 2021

Assets

Liabilities

Cash

$ 5,200

Accounts payable

$ 7,700

Accounts receivable

Salaries payable

Building

Total liabilities

Retained earnings

Chapter 1 – A Framework for Financial Accounting

Problem 1-6B (LO 1-7)

Assumption violated

1.

Periodicity

2.

Monetary unit

4.

Economic entity

Problem 1-7B (LO 1-7)

1.

h.

2.

g.

3.

f.

4.

a.

6.

e.

7.

i.

8.

b.

9.

c.

Chapter 1 – A Framework for Financial Accounting

1-40 Financial Accounting, 5e

ADDITIONAL PERSPECTIVES

Additional Perspective 1-1

Requirement 1

The three primary forms of business organizations include sole proprietorship, partnership, and

corporation. The major advantage of a corporation is limited liability. Stockholders of a corporation

Requirement 2

Typical financing activities include issuing common stock, borrowing, and repayment of borrowing.

Typical investing activities include the purchase of long-term assets such as land, buildings,

Requirement 3

Assets – cash, accounts receivable, supplies, and equipment.

Requirement 4

Income statement – revenues less expenses equal net income during an interval of time.

Statement of stockholders’ equity – changes in common stock and retained earnings during an

Chapter 1 – A Framework for Financial Accounting

Additional Perspective 1-2

AMERICAN EAGLE OUTFITTERS

($ in thousands)

Requirement 1

Total assets = $1,816,313

Total liabilities = $569,522

Requirement 4

Inflows

Outflows

Investing activities

There are none

Capital expenditures for

property and equipment

Financing activities

Net proceeds from stock

options exercised

Cash dividends paid

Requirement 5

The company’s auditor is Ernst & Young LLP.

The auditor states, “We have audited the accompanying consolidated balance sheets of

Chapter 1 – A Framework for Financial Accounting

1-42 Financial Accounting, 5e

Additional Perspective 1-3

BUCKLE

($ in thousands)

Requirement 1

Total assets = $538,116

Requirement 2

Consolidated Statements of Income

Requirement 3

Net sales = $913,380

Requirement 5

The company’s auditor is Deloitte & Touche LLP.

The auditor states, “We have audited the accompanying consolidated balance sheets of

The Buckle, Inc. and subsidiary (the “Company”) as of February 3, 2018 and January

28, 2017, and the related consolidated statements of income, comprehensive income,

Chapter 1 – A Framework for Financial Accounting

Additional Perspective 1-4

Requirement 1

The total assets of American Eagle are higher than the total assets of Buckle.

Requirement 2

The total liabilities of American Eagle are higher than the total liabilities of Buckle.

A higher amount of liabilities does not necessarily mean a higher chance of

Requirement 3

Ability to repay debt.

The ratio of total liabilities to total assets can be used as one measure of a company’s

Requirement 4

The net income of American Eagle is higher than the net income of Buckle. When

Requirement 5

Ability to generate profits.

Net income provides a measure of a company’s ability to generate profit for its

Chapter 1 – A Framework for Financial Accounting

1-44 Financial Accounting, 5e

Additional Perspective 1-5

1. Yes.

The role of an auditor is to express an independent, professional opinion of the extent

to which financial statements are prepared in compliance with Generally Accepted

Accounting Principles. An auditor’s ethics might be challenged because of the need to

2. No.

Auditors are not employees of the company. They are hired by a company as an

3. Yes.

Although ultimate responsibility for fair presentation of financial statements lies with

management, the auditor’s opinion lends additional credibility to those financial

4. No.

Even though the auditor faces this ethical dilemma, they serve an important role in the

reporting of financial information to help investors and creditors make decisions.

Chapter 1 – A Framework for Financial Accounting

Additional Perspective 1-6

Requirement 1

The mission of the U.S. Securities and Exchange Commission is to protect investors,

maintain fair, orderly, and efficient markets, and facilitate capital formation.

The SEC was created to restore investor confidence in our capital markets by

providing investors and the markets with more reliable information and clear rules of

honest dealing.

Chapter 1 – A Framework for Financial Accounting

1-46 Financial Accounting, 5e

Additional Perspective 1-6 (continued)

Requirement 2

The four main financial statements discussed by the SEC are: (1) balance sheets;

(2) income statements; (3) cash flow statements; and (4) statements of shareholders’

equity.

A balance sheet provides detailed information about a company’s assets, liabilities and

shareholders’ equity.

The statement of shareholders’ equity shows changes in the interests of the company’s

shareholders over time.

The disclosure notes provide additional information beyond that reported in the

financial statements. This information includes items such as significant accounting

Chapter 1 – A Framework for Financial Accounting

Additional Perspective 1-6 (concluded)

Requirement 3

The mission of the FASB is to establish and improve standards of financial accounting

and reporting for the guidance and education of the public, including issuers, auditors,

and users of financial information.

Requirement 4

(a) Yes; Nike properly prepared the four financial statements.

Chapter 1 – A Framework for Financial Accounting

1-48 Financial Accounting, 5e

Additional Perspective 1-7

The functions of financial accounting are to measure business activities of a company

and to communicate information about those activities to investors and creditors and

other outside users for decision-making purposes.

The four financial statements include:

1. Income statement, which shows revenues and expenses during the reporting period.

2. Statement of stockholders’ equity, which shows the change in stockholders’ equity

during the reporting period.