CHAPTER 1

Accounting in Action

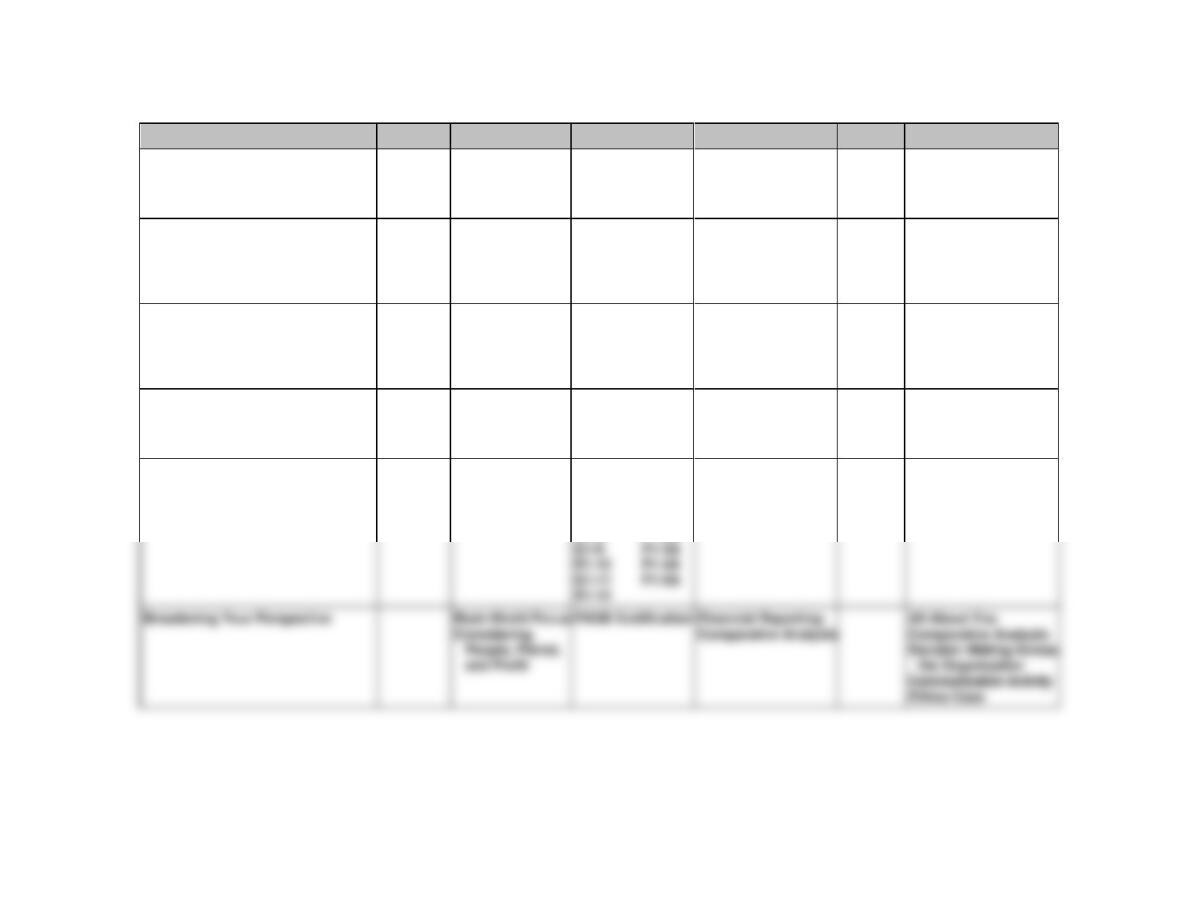

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Identify the activities and

users associated with

accounting.

1, 2, 3, 4, 5

1

1, 2

2. Explain the building blocks of

accounting: ethics, principles,

and assumptions.

6, 7, 8, 9, 10

2

3, 4

3. State the accounting

equation, and define its

components.

11, 12, 13, 22

1, 2, 3, 4, 5, 8

3, 5

5

1A, 2A 4A

4. Analyze the effects of

business transactions on the

accounting equation.

14, 15, 16, 18

6, 7, 9

4

6, 7, 8

1A, 2A, 4A,

5. Describe the four financial

statements and how they are

prepared.

17, 19, 20, 21

10, 11

5

9, 10, 11, 12,

2A, 3A, 4A,

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time Allotted

(min.)

1A

Analyze transactions and compute net income.

Moderate

40–50

2A

Analyze transactions and prepare income statement,

owner’s equity statement, and balance sheet.

Moderate

50–60

3A

Prepare income statement, owner’s equity statement, and

balance sheet.

Moderate

50–60

4A

Analyze transactions and prepare financial statements.

Moderate

40–50

owner’s equity statement.

WEYGANDT ACCOUNTING PRINCIPLES 12E

CHAPTER 1

ACCOUNTING IN ACTION

Number

LO

BT

Difficulty

Time (min.)

BE1

3

AP

Simple

2–4

BE2

3

AP

Simple

3–5

BE3

3

AP

Moderate

4–6

BE4

3

AP

Moderate

4–6

BE5

3

C

Simple

2–4

BE6

4

C

Simple

2–4

BE7

4

C

Simple

2–4

BE8

3

C

Simple

2–4

BE9

4

C

Simple

1–2

BE10

5

AP

Simple

3–5

BE11

5

C

Simple

2–4

DI1

1

K

Simple

2–4

DI2

2

K

Simple

2–4

DI3

3

AP

Simple

6–8

DI4

4

AP

Moderate

8–10

DI5

3, 5

AP

Moderate

10–12

EX1

1

C

Moderate

5–7

EX2

1

C

Simple

6–8

EX3

2

C

Moderate

6–8

EX4

2

C

Moderate

6–8

EX5

3

C

Simple

4–6

EX6

4

C

Simple

6–8

EX7

4

C

Simple

4–6

EX8

4

AP

Moderate

12–15

EX9

5

AP

Simple

12–15

EX10

5

AP

Moderate

8–10

EX11

5

AP

Moderate

6–8

EX12

5

AP

Simple

8–10

EX13

5

AN

Simple

8–10

EX14

5

AP

Simple

10–12

EX15

5

Simple

6–8

ACCOUNTING IN ACTION (Continued)

Number

LO

BT

Difficulty

Time (min.)

P1A

3, 4

AP

Moderate

40–50

AP

50–60

5

AP

50–60

P4A

3–5

AP

Moderate

40–50

AP

40–50

BYP1

5

AN

Simple

10–15

BYP2

5

AN, E

Simple

10–15

BYP3

BYP4

5

6

AN, E

C, AN

Simple

Simple

10–15

15–20

BYP5

4

Moderate

15–20

BYP6

5

Simple

12–15

BYP7

2

Simple

10–12

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End-of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Identify the activities and users

associated with accounting.

DI1-1

Q1-1

Q1-2

Q1-3

Q1-4

Q1-5

E1-1

E1-2

3. Explain the building blocks of

accounting: ethics, principles,

and assumptions.

Q1-7

Q1-8

Q1-9

Q1–10

DI1-1

Q1-6

E1-3

E1-4

3. State the accounting equation,

and define its components.

DI1-2

BE1-5

Q1–11

Q1–12

Q1–13

BE1-4

BE1-8

BE1-9

E1-5

BE1-1

BE1-2

BE1-3

DI1-5

P1–1A

P1–2A

P1–4A

4. Analyze the effects of business

transactions on the accounting

equation.

Q1–14

Q1–15

Q1–16

Q1–18

BE1-6

BE1-7

E1-6

E1-7

DI1-4

E1-8

P1–1A

P1–2A

P1–4A

P1–5A

5. Describe the four financial

statements and how they are

prepared.

Q1–17

Q1–19

BE1-11

Q1–20

Q1–21

BE1-10

DI1-5

E1-8

E1–14

E1–15

E1–16

E1–17

P1–2A

E1–13

ANSWERS TO QUESTIONS

1. Yes, this is correct. Virtually every organization and person in our society uses accounting

information. Businesses, investors, creditors, government agencies, and not-for-profit organizations

must use accounting information to operate effectively.

2. Accounting is the process of identifying, recording, and communicating the economic events of

an organization to interested users of the information. The first step of the accounting process is

therefore to identify economic events that are relevant to a particular business. Once identified

3. (a) Internal users are those who plan, organize, and run the business and therefore are officers

and other decision makers.

4. (a) Investors (owners) use accounting information to make decisions to buy, hold, or sell owner–

ship shares of a company.

(b) Creditors use accounting information to evaluate the risks of granting credit or lending money.

6. Trenton Travel Agency should report the land at $90,000 on its December 31, 2017 balance

sheet. This is true not only at the time the land is purchased, but also over the time the land is

held. In determining which measurement principle to use (cost or fair value) companies weigh the

factual nature of cost figures versus the relevance of fair value. In general, companies use cost.

Only in situations where assets are actively traded do companies apply the fair value principle.

An important concept that accountants follow is the historical cost principle.

7. The monetary unit assumption requires that only transaction data that can be expressed in terms

of money be included in the accounting records. This assumption enables accounting to quantify

(measure) economic events.

Questions Chapter 1 (Continued)

10. One of the advantages Rachel Hipp would enjoy is that ownership of a corporation is represented

by transferable shares of stock. This would allow Rachel to raise money easily by selling

11. The basic accounting equation is Assets = Liabilities + Owner’s Equity.

12. (a) Assets are resources owned by a business. Liabilities are claims against assets. Put more

13. The liabilities are: (b) Accounts payable and (g) Salaries and wages payable.

14. Yes, a business can enter into a transaction in which only the left side of the accounting equation

is affected. An example would be a transaction where an increase in one asset is offset by

15. Business transactions are the economic events of the enterprise recorded by accountants

because they affect the basic accounting equation.

(a) The death of the owner of the company is not a business transaction as it does not affect

the basic accounting equation.

16. (a) Decrease assets and decrease owner’s equity.

(b) Increase assets and decrease assets.

(c) Increase assets and increase owner’s equity.

(d) Decrease assets and decrease liabilities.

18. No, this treatment is not proper. While the transaction does involve a receipt of cash, it does not

represent revenues. Revenues are the gross increase in owner’s equity resulting from business

activities entered into for the purpose of earning income. This transaction is simply an additional

investment made by the owner in the business.

Questions Chapter 1 (Continued)

19. Yes. Net income does appear on the income statement—it is the result of subtracting expenses

from revenues. In addition, net income appears in the owner’s equity statement—it is shown as

an addition to the beginning-of-period capital. Indirectly, the net income of a company is also

included in the balance sheet. It is included in the capital account which appears in the owner’s

equity section of the balance sheet.

20. (a) Ending capital balance …………………………………………………………………………. $198,000

Beginning capital balance …………………………………………………………………….. 168,000

Net income …………………………………………………………………………………………. $ 30,000

21. (a) Total revenues ($20,000 + $70,000) ………………………………………………………. $90,000

(b) Total expenses ($26,000 + $40,000) ………………………………………………………. $66,000

22. Apple’s accounting equation at September 28, 2013 was $207,000,000,000 = $83,451,000,000 +

$123,549,000,000.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 1-1

BRIEF EXERCISE 1-2

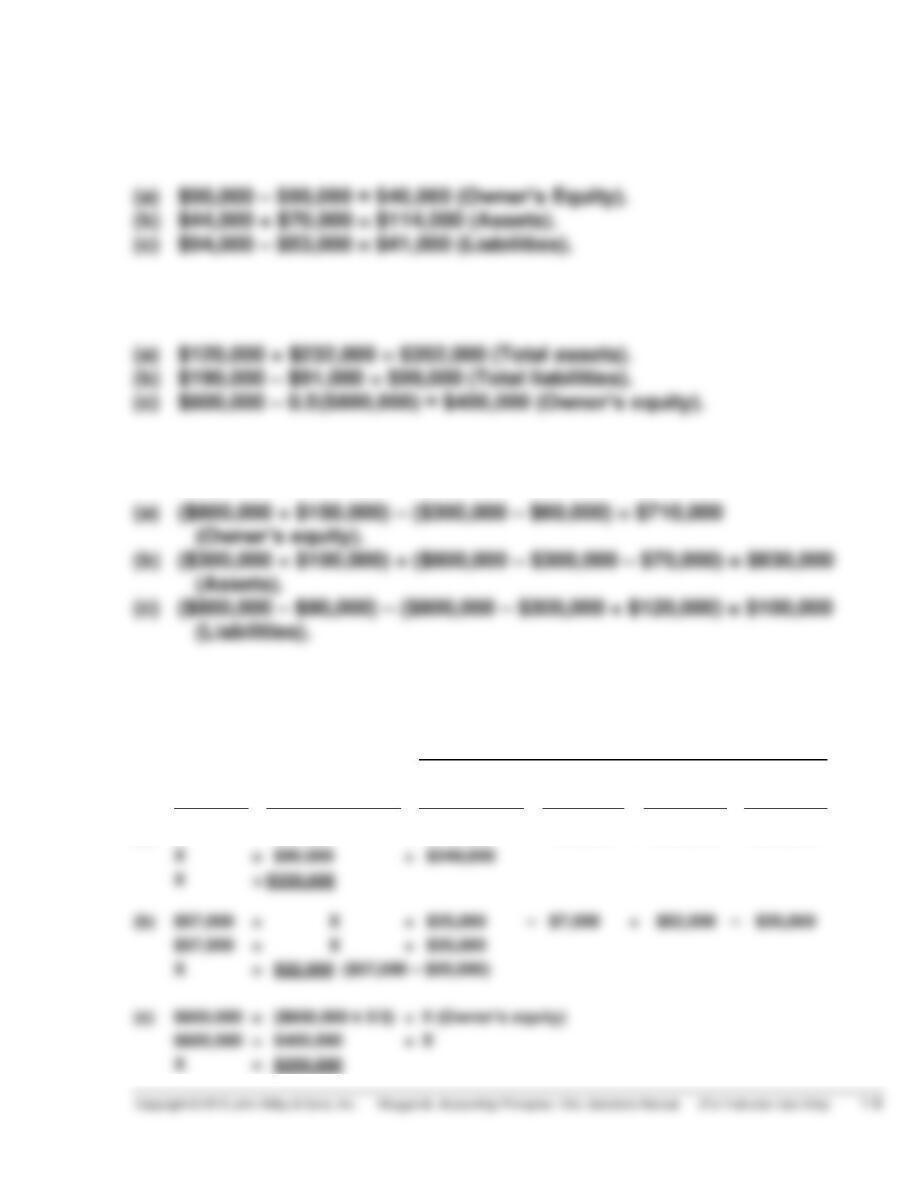

(a) $120,000 + $232,000 = $352,000 (Total assets).

BRIEF EXERCISE 1-3

(a) ($800,000 + $150,000) – ($300,000 – $60,000) = $710,000

(Owner’s equity).

BRIEF EXERCISE 1-4

Owner’s Equity

Assets

=

Liabilities

+

Owner’s

Capital

–

Owner’s

Drawings

+

Revenues

–

Expenses

(a)

X

=

$90,000

+

$150,000

–

$40,000

+

$450,000

–

$320,000

X

=

$90,000

+

$240,000

X

=

$330,000

(b)

$57,000

=

X

+

$25,000

–

$7,000

+

$52,000

–

$35,000

$57,000

=

+

$35,000

X

=

(c)

$600,000

=

($600,000 x 2/3)

+

X (Owner’s equity)

BRIEF EXERCISE 1-5

A (a) Accounts receivable A (d) Supplies

BRIEF EXERCISE 1-6

Assets

Liabilities

Owner’s Equity

(a)

+

+

NE

+

(c)

–

NE

BRIEF EXERCISE 1-7

Assets

Liabilities

Owner’s Equity

(a)

+

NE

+

(b)

–

NE

–

(c)

NE

NE

NE

BRIEF EXERCISE 1-8

E (a) Advertising expense D (e) Owner’s drawings

BRIEF EXERCISE 1-9

BRIEF EXERCISE 1-10

MENDOZA COMPANY

Balance Sheet

December 31, 2017

Assets

Cash ………………………………………………………………………………….. $ 49,000

Liabilities and Owner’s Equity

Liabilities

Accounts payable ………………………………………………………... $ 90,000

Owner’s equity

BRIEF EXERCISE 1-11

BS (a) Notes payable

IS (b) Advertising expense

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 1-1

1. False. The three steps in the accounting process are identification,

recording, and communication.

2. True.

DO IT! 1-2

1. False. Congress passed the Sarbanes-Oxley Act to reduce unethical

behavior and decrease the likelihood of future corporate scandals.

2. False. The standards of conduct by which actions are judged as right

DO IT! 1-3

1. Drawings is owner’s drawings (D); it decreases owner’s equity.

2. Rent Revenue is revenue (R); it increases owner’s equity.

DO IT! 1-4

Assets

=

Liabilities

+

Owner’s Equity

Cash

+

Accounts

Receivable

=

Accounts

Payable

+

Owner’s

Capital

–

Owner’s

Drawings

+

Revenues

–

Expenses

(1)

+$20,000

+$20,000

(2)

+$20,000

DO IT! 1-5

(a) The total assets are $49,000, comprised of Cash $6,500, Accounts

Receivable $13,500, and Equipment $29,000.

(b) Net income is $20,500, computed as follows:

Revenues

Service revenue………………………………………….. $53,500

Expenses

(c) The ending owner’s equity balance of Kirby Company is $21,000. By

rewriting the accounting equation, we can compute Owner’s Equity as

Assets minus Liabilities, as follows:

Total assets [as computed in (a)] ……………………….. $49,000

Less: Liabilities

Notes payable …………………………………………….. $25,000

SOLUTIONS TO EXERCISES

EXERCISE 1-1

C Analyzing and interpreting information.

R Classifying economic events.

C Explaining uses, meaning, and limitations of data.

EXERCISE 1-2

(a) Internal users

Marketing manager

Production supervisor

Store manager

Vice-president of finance

External users

Customers

Internal Revenue Service

Labor unions

Securities and Exchange Commission

Suppliers

(b) I Can we afford to give our employees a pay raise?

E Did the company earn a satisfactory income?

I Do we need to borrow in the near future?

EXERCISE 1-3

Angela Duffy, president of Duffy Company, instructed Jana Barth, the head

of the accounting department, to report the company’s land in its

accounting reports at its fair value of $170,000 instead of its cost of $100,000,

in an effort to make the company appear to be a better investment. The

historical cost principle requires that assets be recorded and reported at

their cost, because cost is faithfully representative and can be objectively

measured and verified. In this case, the historical cost principle should be

used and Land reported at $100,000, not $170,000.

The stakeholders include stockholders and creditors of Duffy Company,

potential stockholders and creditors, other users of Duffy’s accounting

reports, Angela Duffy, and Jana Barth. All users of Duffy’s accounting

reports could be harmed by relying on information that may be unreliable.

EXERCISE 1-4

1. Incorrect. The historical cost principle requires that assets (such as

buildings) be recorded and reported at their cost.

2. Correct. The monetary unit assumption requires that companies include

in the accounting records only transaction data that can be expressed

in terms of money.

EXERCISE 1-5

Asset

Liability

Owner’s Equity

Cash

Accounts payable

Owner’s capital

Equipment

Notes payable

EXERCISE 1-6

1. Increase in assets and increase in owner’s equity.

2. Decrease in assets and decrease in owner’s equity.

3. Increase in assets and increase in liabilities.

4. Increase in assets and increase in owner’s equity.

EXERCISE 1-7

1. (c) 5. (d)

EXERCISE 1-8

(a) 1. Owner invested $15,000 cash in the business.

2. Purchased equipment for $5,000, paying $2,000 in cash and the

balance of $3,000 on account.

EXERCISE 1-8 (Continued)

6. Owner withdrew $2,000 cash for personal use.

7. Paid $650 cash for rent.

8. Collected $450 cash from customers on account.

9. Paid salaries and wages of $4,800.

10. Incurred $400 of utilities expense on account.

(b) Investment ……………………………………………………………………. $15,000

Service revenue ……………………………………………………………. 8,500

Drawings ……………………………………………………………………… (2,000)

Rent expense ……………………………………………………………….. (650)

Salaries and wages expense …………………………………………. (4,800)

Utilities expense …………………………………………………………… (400)

Increase in owner’s equity …………………………………………….. $15,650

EXERCISE 1-9

ARTHUR COOPER & CO.

Income Statement

For the Month Ended August 31, 2017

Revenues

Service revenue ………………………………………………… $8,500

Expenses

EXERCISE 1-9 (Continued)

ARTHUR COOPER & CO.

Owner’s Equity Statement

For the Month Ended August 31, 2017

Owner’s capital, August 1 …………………………………….. $ 0

Add: Investments ………………………………………………. $15,000

Net income ………………………………………………… 2,650 17,650

17,650

Less: Drawings …………………………………………………… 2,000

Owner’s capital, August 31 …………………………………… $15,650

ARTHUR COOPER & CO.

Balance Sheet

August 31, 2017

Assets

Cash ………………………………………………………………………………….. $ 8,350

Accounts receivable ……………………………………………………………. 3,450

Liabilities and Owner’s Equity

Liabilities

Accounts payable ………………………………………………………… $ 1,900

Owner’s equity

Owner’s capital ……………………………………………………………. 15,650

Total liabilities and owner’s equity …………………………. $17,550

EXERCISE 1-10

EXERCISE 1-10 (Continued)

(b) Owner’s equity—12/31/17 ($460,000 – $300,000) …………… $160,000

Owner’s equity—1/1/17—see (a) ………………………………….. 150,000

Increase in owner’s equity ………………………………………….. 10,000

Less: Additional investment ………………………………………. 45,000

Net loss for 2017 ………………………………………………………… $ (35,000)

EXERCISE 1-11

(a) Total assets (beginning of year) ………………………………….. $110,000

Total liabilities (beginning of year) ………………………………. 85,000

Total owner’s equity (beginning of year) ……………………… $ 25,000

(b) Total owner’s equity (end of year) ……………………………….. $ 40,000

Total owner’s equity (beginning of year) ……………………… 25,000

Increase in owner’s equity ………………………………………….. $ 15,000

EXERCISE 1-11 (Continued)

(d) Total owner’s equity (end of year) ……………………………….. $130,000

Total owner’s equity (beginning of year) ……………………… 80,000

Increase in owner’s equity ………………………………………….. $ 50,000

EXERCISE 1-12

ARMANDA CO.

Income Statement

For the Year Ended December 31, 2017

Revenues

Service revenue ……………………………………………. $63,600

Expenses

Salaries and wages expense ………………………….. $29,500

Rent expense ……………………………………………….. 10,400

Utilities expense …………………………………………… 3,100

ARMANDA CO.

Owner’s Equity Statement

For the Year Ended December 31, 2017

Owner’s capital, January 1 ……………………………………………………. $48,000