14 Chapter 1 Introduction to Accounting and Business

OBJECTIVE 4

Describe and illustrate how business transactions can be recorded in terms of the resulting

change in the basic elements of the accounting equation.

SYNOPSIS

Using a sample company called NetSolutions, this objective demonstrates how business transactions

affect a company’s financial condition. Transactions, such as depositing cash, purchasing assets, selling

services, and paying bills, etc., affect the accounting equation. This shows students that through each

transaction the two sides of the accounting equation are always equal.

Key Terms and Definitions

• Account Payable – The liability created by a purchase on account.

• Account Receivable – A claim against the customer created by selling merchandise or services

on credit.

• Business Transaction – An economic event or condition that directly changes an entity’s

financial condition or directly affects its results of operations

• Expenses – Assets used up or services consumed in the process of generating revenues.

• Fees Earned – Revenue from providing services.

• Interest Revenue – Money received for interest.

• Prepaid Expenses – Items such as supplies that will be used in the business in the future.

• Rent Revenue – Money received for rent.

• Revenue – Increases in owner’s equity as a result of selling services or products to customers.

• Sales – The total amount charged customers for merchandise sold, including cash sales and sales

on account.

Relevant Example Exercises and Exhibits

• Example Exercise 1-3 – Transactions

• Exhibit 5 – Summary of Transactions for NetSolutions

• Exhibit 6 – Types of Transactions Affecting Owner’s Equity

SUGGESTED APPROACH

This objective illustrates recording business transactions within the framework of the accounting

equation. The text defines a business transaction as “an economic event or condition that directly changes

the entity’s financial condition or its results of operations.” Problem 1-1A or Problem 1-1B, as well as

TM 1-12, describe some of the economic events that are recorded as business transactions. This list can

assist your students in determining which events/conditions to record. For practice, ask students to list

transactions that they recently entered into with a business entity, such as purchasing gas for the car,

getting their hair cut, or purchasing their textbook from the bookstore.

The basics of recording transactions can be effectively illustrated by working a sample problem for the

students. Problem 1-1A or 1-1B provides several example transactions for a property rental management

business or an insurance agency, respectively. You can use either of these problems to demonstrate how

Chapter 1 Introduction to Accounting and Business 15

transactions are recorded. Any of the problems will work. Try to choose the problem opposite a

homework assignment. If you usually work A problems as homework problems, then work all

corresponding B problems in class. List the accounts that will be needed to record these transactions:

You will probably need to emphasize the following points as you demonstrate transactions:

1. The accounting equation must always stay in balance. Transactions may require additions to both

sides, subtractions from both sides of the equation, or an addition and a subtraction on the same side,

but the equation must always balance.

2. Revenue represents the receipt of assets (cash or accounts receivable) for goods sold or services

rendered. The receipt of assets from the owner is an investment by the owner.

3. Revenues are recognized when services are rendered, not when the cash is received.

4. Expenses are costs incurred in generating revenues. Purchases of assets, payments of liabilities, and

owner’s withdrawals are not recorded as expenses.

GROUP LEARNING ACTIVITY—Recording Business Transactions

Rather than working through all of the transactions in TM 1-13 for your students, consider working only

the first few. Divide the class into small groups (two to three students) and ask them to complete the

exercise in five to ten minutes. TM 1-14 provides the solution. Give your students the opportunity to

check their work and ask questions after they have completed their assignment.

OBJECTIVE 5

Describe the financial statements of a proprietorship and explain how they interrelate.

SYNOPSIS

This objective shows the income statement, statement of owner’s equity, balance sheet, and statement of

cash flows. Using the same NetSolutions example as the previous objective, the order, preparation, and

16 Chapter 1 Introduction to Accounting and Business

relationship between the four financial statements is demonstrated. Each statement is prepared for a

Key Terms and Definitions

• Account Form – The form of balance sheet that resembles the basic format of the accounting

equation, with assets on the left side and Liabilities and Owner’s Equity sections on the right

side.

• Balance Sheet – A list of the assets, liabilities, and owner’s equity as of a specific date,

usually at the close of the last day of a month or a year.

• Earnings – The amount by which revenues exceed expenses.

• Financial Statements – Financial reports that summarize the effects of events on a business.

Relevant Example Exercises and Exhibits

• Example Exercise 1-4 – Income Statement

• Example Exercise 1-5 – Statement of Owner’s Equity

• Example Exercise 1-6 – Balance Sheet

SUGGESTED APPROACH

This objective introduces the four financial statements of a proprietorship (in order of preparation: Income

Statement, Statement of Owner’s Equity, Balance Sheet, and Statement of Cash Flows) and explains how

they interrelate.

This objective also introduces the concept of “matching.” It is helpful to emphasize that matching is one

of the most important concepts in accounting. If revenues and expenses are not properly matched, then the

amount reported for net income is incorrect, making every statement thereafter incorrect.

1. The date portion of the heading varies among the financial statements. The Income Statement,

Statement of Owner’s Equity, and Statement of Cash Flows summarize transactions for a period of

time, while the Balance Sheet shows a “snapshot” of the business on a particular date.

Next, ask your students to build on the transactions recorded for Jim’s Lawn Care in the following Group

Learning Activity.

After covering the income statement, statement of owner’s equity, and balance sheet, you may want to

describe the statement of cash flows. Coverage of the cash flow statement also may be completely

GROUP LEARNING ACTIVITY—Preparing Financial Statements

Use Jim’s Lawn Care transactions solution (TM 1-14) to display on the overhead projector; divide the

class into small groups. Ask students to use the balances from your problem to prepare financial

statements for the month. TM 1-15 can be used to provide a template for the students to follow. TM 1-16

shows the completed income statement, statement of owner’s equity, and balance sheet for Jim’s Lawn

Care.

Handout 1 can be distributed here for the first time or re-assigned after a discussion about financial

statements to see how students will perform with a little accounting knowledge on their side.

Begin this exercise by asking the class to define the word “profit.” Next, divide the students into small

groups (two to five students). Ask them to read the upholstery shop exercise and determine the shop’s

18 Chapter 1 Introduction to Accounting and Business

profit. It is best to put the students at ease by announcing that, for today, there will be no “incorrect”

answers. Give the students 10 to 15 minutes to work. Ask for each group’s answer, and record it on the

board.

OBJECTIVE 6

Describe and illustrate the use of the ratio of liabilities to owner’s equity in evaluating a

company’s financial condition.

SYNOPSIS

Using the financial statements prepared in the previous objective, the use of the ratio of liabilities to

owner’s equity is examined. The total liabilities is divided by the total owner’s equity to calculate this

ratio. Since creditors have rights to a business’s assets before the owner, this ratio is important to both

owners and creditors. This ratio can affect how a business pays its creditors and foretells how well a

business will do in poor economic conditions. As this ratio increases, the creditors and the business

become more at risk.

Key Terms and Definitions

• Ratio of Liabilities to Owner’s (Stockholders’) Equity – A comprehensive leverage ratio that

measures the relationship of the claims of creditors to stockholders’ equity.

Relevant Example Exercises and Exhibits

• Example Exercise 1-8 – Ratio of Liabilities to Owner’s Equity

SUGGESTED APPROACH

This objective introduces the ratio of liabilities to owner’s equity. Explain that the ability of a business to

meet its financial obligations is a measure of the strength or weakness of its financial condition.

Remind students that the rights of creditors to a business’s assets come before the rights of the owners or

stockholders.

Chapter 1 Introduction to Accounting and Business 19

Handout 1-1

CLASSIC UPHOLSTERY SHOP

Tyler Smith had worked in an upholstery shop for 10 years. Last year, Tyler’s wages were $20,000.

Lately, Tyler had been unhappy with the shop’s owner. Convinced that he could run an upholstery shop

that did better work at a lower cost, Tyler decided to go into business for himself and opened CLASSIC

UPHOLSTERY SHOP.

To get the business going, Tyler decided to invest heavily in advertising. He spent $6,000 on advertising

aimed at consumers and another $2,000 on advertising aimed at getting work from interior decorators and

interior design stores. Tyler also purchased industrial sewing machines costing $4,000 and other tools and

equipment costing $3,000. He estimated that the sewing machines can be used for about five years before

maintenance costs will be too high and the machines will need to be replaced. The other tools and

equipment are not as durable and will have to be replaced in three years.

A review of Tyler’s checkbook shows he paid the following expenses (in addition to those mentioned

previously) during the first year of business:

Upholstery fabric $40,000

Other supplies 10,000

Tyler’s utility bill for the last month of the year has not arrived. He estimates that the bill will be

approximately $320.

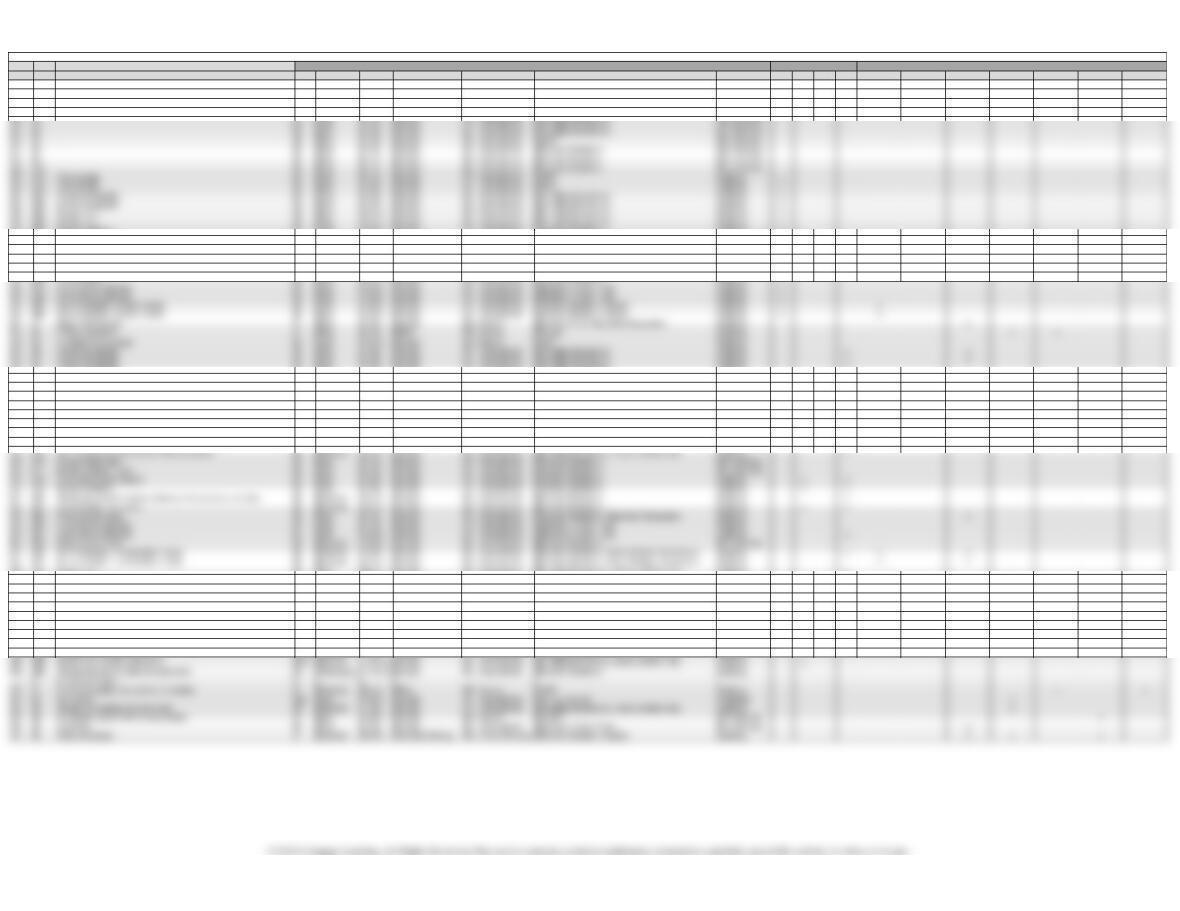

Type Item Description LO(s) Difficulty Time Est BUSPROG AICPA ACBSP – APC Bloom’s EE Excel GL SMH FAI Service Real World Writing Ethics Internet Group

DQ 1 1 Easy 5 min. Analytic BB – Industry Purpose Remembering

DQ 2 1 Easy 5 min. Analytic BB – Industry Purpose Remembering

DQ 3 1 Easy 5 min. Analytic BB – Industry Purpose Remembering

DQ 4 2 Easy 5 min. Analytic FN – Measurement Recording Transactions Remembering

PE 4A Income statement 5 Easy 10 min. Analytic FN – Measurement Financial Statements Applying x

PE 4B Income statement 5 Easy 10 min. Analytic FN – Measurement Financial Statements Applying x

PE 5A Statement of owner‘s equity 5 Easy 5 min. Analytic FN – Measurement Financial Statements Applying x

PE 5B Statement of owner‘s equity 5 Easy 5 min. Analytic FN – Measurement Financial Statements Applying x

PE 6A Balance sheet 5 Easy 10 min. Analytic FN – Measurement Financial Statements Applying x

PE 6B Balance sheet 5 Easy 10 min. Analytic FN – Measurement Financial Statements Applying x

EX 6 Accounting equation 3 Easy 5 min. Analytic FN – Measurement Recording Transactions Applying x

EX 7 Accounting equation 3, 4 Moderate 10 min. Analytic FN – Measurement Recording Transactions Applying x

EX 8 Asset, liability, owner’s equity items 3 Easy 5 min. Analytic FN – Measurement GAAP Remembering

EX 9 Effect of transactions on accounting equation 4 Easy 5 min. Analytic FN – Measurement Recording Transactions Applying

EX 10 Effect of transactions on accounting equation 4 Easy 5 min. Analytic FN – Measurement Recording Transactions Applying x

EX 11 Effect of transactions on owner’s equity 4 Easy 5 min. Analytic FN – Measurement Recording Transactions Applying

EX 12 Transactions 4 Easy 10 min. Analytic FN – Measurement Recording Transactions Applying

EX 13 Nature of transactions 4 Moderate 15 min. Analytic FN – Measurement Recording Transactions Applying x

EX 14 Net income and owner’s withdrawals 5 Easy 5 min. Analytic FN – Measurement Financial Statements Understanding x

PR 1A Transactions 4 Easy 30 min. Analytic FN – Measurement Recording Transactions, Financial Statements Applying x x

PR 2A Financial statements 5 Easy 30 min. Analytic FN – Measurement Financial Statements Applying x x

PR 3A Financial statements 5 Moderate 45 min. Analytic FN – Measurement Financial Statements Applying x

PR 4A Transactions; financial statements 4, 5 Moderate 1 hour Analytic FN – Measurement Recording Transactions, Financial Statements Applying

PR 5A Transactions; financial statements 4, 5 Moderate 1.5 hours Analytic FN – Measurement Recording Transactions, Financial Statements Applying x

PR 6A Missing amounts from financial statements 5 Challenging 1.5 hours Analytic FN – Measurement Financial Statements Applying

PR 1B Transactions 4 Easy 30 min. Analytic FN – Measurement Recording Transactions, Financial Statements Applying x x

PR 2B Financial statements 5 Easy 30 min. Analytic FN – Measurement Financial Statements Applying x x

PR 3B Financial statements 5 Moderate 45 min. Analytic FN – Measurement Financial Statements Applying x

PR 4B Transactions; financial statements 4, 5 Moderate 1 hour Analytic FN – Measurement Recording Transactions, Financial Statements Applying

HOMEWORK CHART WITH LEARNING OUTCOMES TAGGING

TAGGING

RESOURCES

FOCUS