CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

Prob. 15–2B (FIN MAN); Prob. 1–2B (MAN)

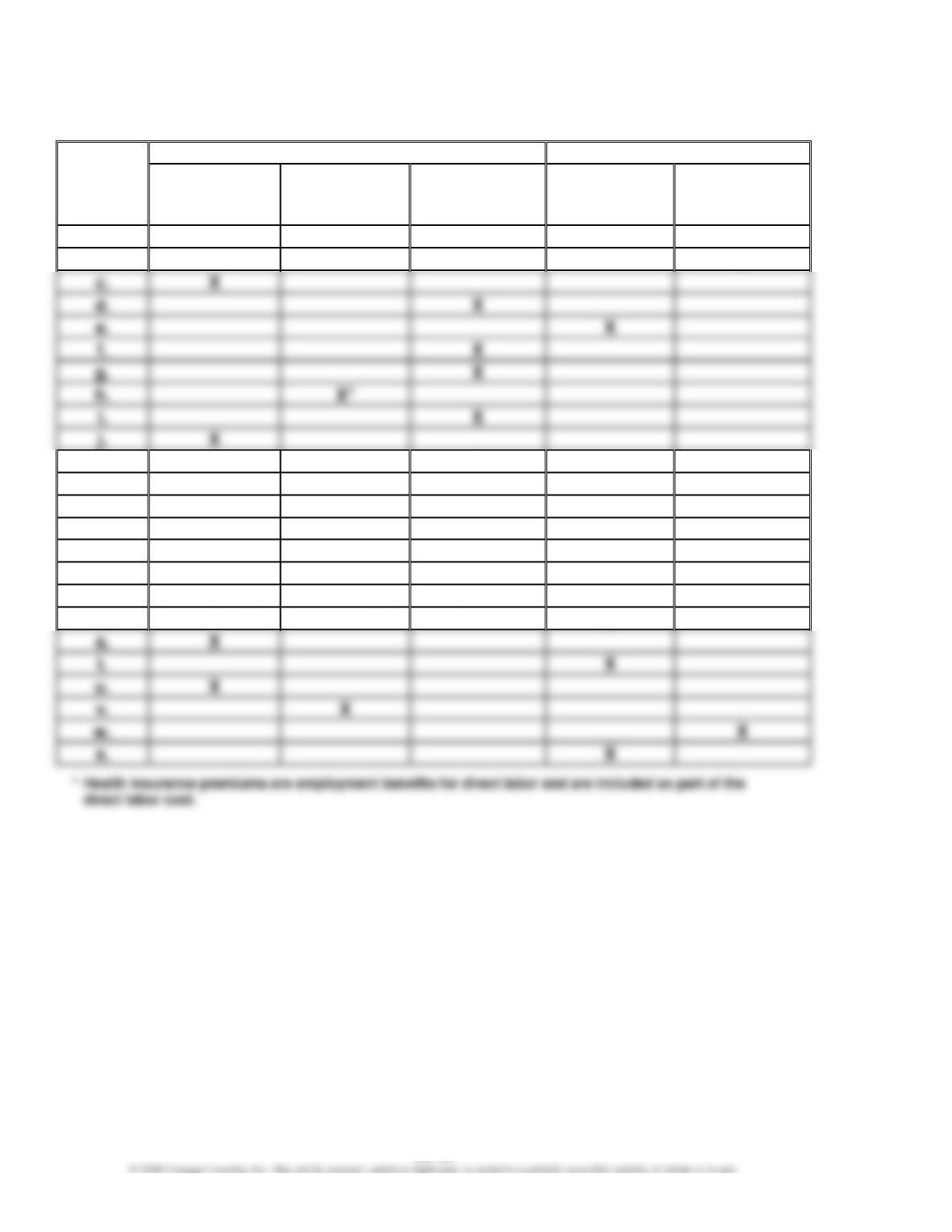

Cost

Product Costs

Period Costs

Direct

Materials

Cost

Direct

Labor

Cost

Factory

Overhead

Cost

Selling

Expense

Administrative

Expense

a.

X

b.

X

c.

d.

X

e.

X

X

g.

X

h.

i.

X

k.

X

l.

X

m.

X

n.

X

o.

X

p.

X

q.

X

r.

X

s.

u.

X

v.

X

X

x.

CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

Prob. 15–3B (FIN MAN); Prob. 1–3B (MAN)

1. The most logical definition for the final cost object would be a hotel guest. Guests

2.

Cost

Direct

Indirect

a.

X

b.

X

X

d.

X

e.

X

X

g.

X

h.

X

X

X

k.

X

l.

X

m.

X

n.

X

o.

X

p.

X

q.

X

X

s.

X

X

u.

X

v.

X

X

CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

Prob. 15–4B (FIN MAN); Prob. 1–4B (MAN)

1. On Company

a. $30,800 ($282,800 + $65,800 – $317,800)

Off Company

a. $581,560 ($685,720* + $91,140 – $195,300)

b. $685,720 ($1,519,000 – $256,060 – $577,220)

* Note: The student must calculate part (b) prior to calculating part (a) because

the solution to part (b) is needed as an input to part (a).

2.

On Company

Statement of Cost of Goods Manufactured

For the Month Ended December 31

Work in process inventory, December 1

$ 119,000

Direct materials:

Materials inventory, December 1

$ 65,800

Purchases

282,800

Cost of materials available for use

$ 348,600

Materials inventory, December 31

(30,800)

Direct labor

387,800

Factory overhead

148,400

Total manufacturing costs incurred in December

854,000

Total manufacturing costs

$ 973,000

Work in process inventory, December 31

(172,200)

Cost of goods manufactured

$ 800,800

CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

Prob. 15–4B (FIN MAN); Prob. 1–4B (MAN) (Concluded)

3.

On

Company

Income

Statement

For the Month Ended December

31

Sales

$1,127,000

Cost of goods sold:

Finished goods inventory, December

1

$ 224,000

Cost of goods

Cost of finished goods available for sale

Gross profit

Operating expenses

Net

$ 182,000

CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

Prob. 15–5B (FIN MAN); Prob. 1–5B (MAN)

1.

Shanika

Company

Statement of Cost of Goods

Manufactured

For the Year Ended December 31,

20Y6

Work in process inventory, January 1, 20Y6

$109,200

Direct materials:

Materials inventory, January 1,

20Y6

$

77,350

Cost of materials available for use

Materials inventory, December 31, 20Y6

Direct labor

186,550

Factory overhead:

Indirect

labor

$

23,660

Depreciation expense—factory equipment

14,560

Heat, light, and power—factory

5,850

Property

taxes—factory

4,095

Rent expense—factory

6,825

62,660

Total manufacturing costs incurred in 20Y6

354,510

Total manufacturing costs

Work in process inventory, December 31,

Cost of goods manufactured

CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

Prob. 15–5B (FIN MAN); Prob. 1–5B (MAN) (Concluded)

2.

Shanika

Company

Income

Statement

For the Year Ended December 31,

20Y6

Sales

$ 864,500

Cost of goods sold:

Finished goods inventory, January 1,

20Y6

$ 113,750

Cost of goods

manufactured

367,510

Cost of finished goods available for sale

$ 481,260

Finished goods

inventory,

December 31,

20Y6

(100,100)

Cost of goods sold

(381,160)

Gross

profit

$

483,340

Operating

expenses:

Administrative

Office salaries expense

$ 113,750

Selling expenses:

Advertising

Sales salaries expense

Net income

$ 164,840

CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

MAKE A DECISION

MAD 15–1 (FIN MAN); MAD 1–1 (MAN)

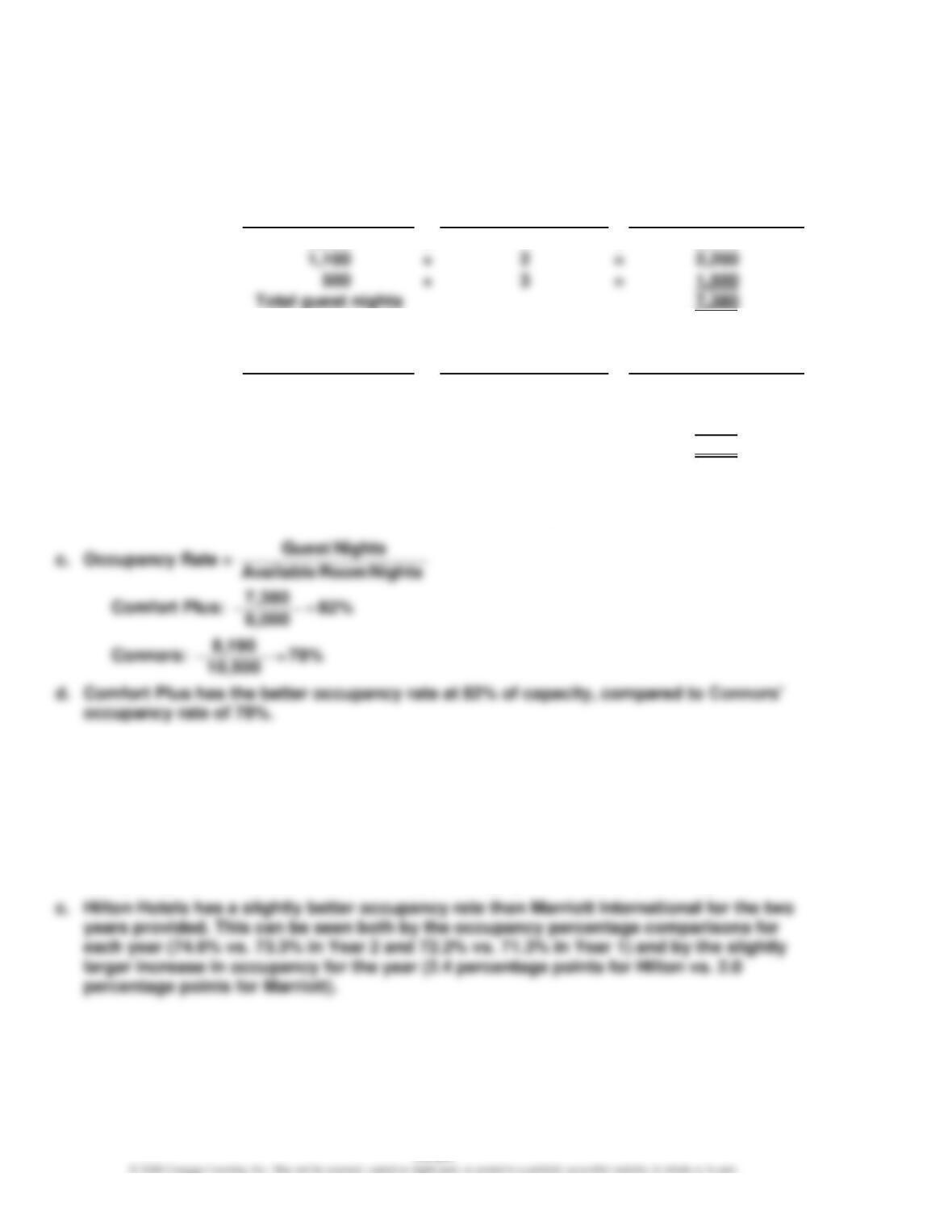

a.

Comfort Plus:

Number of Guests

Nights per Visit

Guest Nights

3,680

×

1

=

3,680

1,100

×

2

=

2,200

500

×

3

=

1,500

Total guest nights

7,380

Connors:

Number of Guests

Nights per Visit

Guest Nights

4,390

×

1

=

4,390

700

×

2

=

1,400

800

×

3

=

2,400

Total guest nights

8,190

b. Comfort Plus: 300 rooms × 30 days = 9,000 available room nights for April

Connors: 350 rooms × 30 days = 10,500 available room nights for April

MAD 15–2 (FIN MAN); MAD 1–2 (MAN)

a. The occupancy change is favorable for Hilton Hotels. The company improved occupancy

from 72.2% to 74.6%, or a 2.4 percentage point increase over the year.

b. The occupancy change is favorable for Marriott International. The company improved

occupancy from 71.3% to 73.3%, or a 2.0 percentage point increase over the year.

CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

MAD 15–2 (FIN MAN); MAD 1–2 (MAN) (Concluded)

d. An important question beyond occupancy is the price at which the rooms are sold. Price

will influence occupancy. For example, it is possible to increase occupancy by reducing

price. However, a reduced price may reduce revenue by more than the revenue increase

MAD 15–3 (FIN MAN); MAD 1–3 (MAN)

a.

Number of

Guests

Average Length

of Visit (in

Nights)

Guest Nights (Number of

Guests × Average Length of

Visit)

Sunrise Suites

183,600

×

1.5

=

275,400

Nationwide Inns

228,000

×

1.2

=

273,600

Number of

for June

Sunrise Suites

×

Nationwide Inns

×

c. Occupancy Rate =

Guest Nights

Available RoomNights

Sunrise Suites:

275,400 85%

324,000 =

Nationwide Inns:

273,600 80%

342,000 =

CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

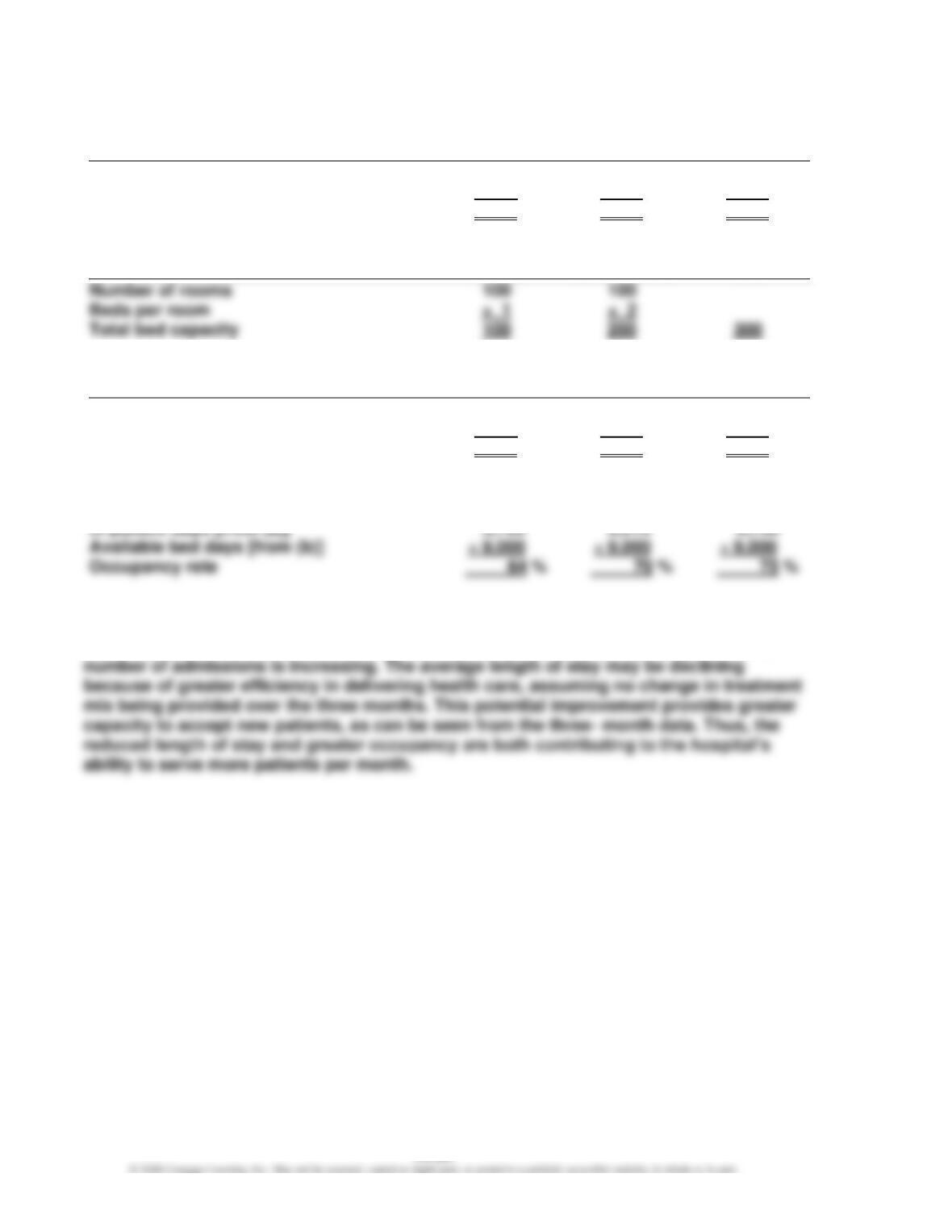

MAD 15–4 (FIN MAN); MAD 1–4 (MAN)

a.

April

May

June

Admitted patients

1,440

1,860

2,250

Average length of stay per patient

× 4.0

× 3.5

× 3.0

In-patient days

5,760

6,510

6,750

b.

Available beds:

Private

Semi-Private

Total

Number of rooms

Beds per room

Total bed capacity

Available bed days:

April

May

June

Bed capacity

300

300

300

Days per month

× 30

× 31

× 30

Available bed days

9,000

9,300

9,000

c.

Occupancy rate:

April

May

June

In-patient days [from (a)]

5,760

6,510

Available bed days [from (b)]

÷ 9,000

÷ 9,000

÷ 9,000

Occupancy rate

d. The occupancy rate increased from April to May and again from May to June. This

suggests the hospital bed capacity is being utilized more efficiently over time. A closer

examination of the data reveals that the average length of stay is declining, while the

CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

MAD 15–5 (FIN MAN); MAD 1–5 (MAN)

a.

Available seat capacity for each flight number for June:

Number of seats per flight

Number of flights in June (one per day)

180

× 30

Total seat capacity per flight number (June)

5,400

b.

Flight

Number

Number of

Seats Sold

Available Seat

Capacity [from (a)]

Passenger

Load*

* Number of seats sold ÷ Available seat capacity

c. The passenger load information indicates that Flight 57 flies very near to capacity, but

Flights 85 and 94 fly at less than half of capacity. This suggests the management of

CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

TAKE IT FURTHER

TIF 15–1 (FIN MAN); TIF 1–1 (MAN)

Brian has behaved unethically and violated several of the IMA’s principles of ethical

conduct. By determining the price of the lumber that he is buying, Brian has created a

conflict-of-interest situation that violates the principle of objectivity. For professionals to be

TIF 15–2 (FIN MAN); TIF 1–2 (MAN)

Answers may vary slightly by restaurant chosen. A suggested answer for a pizza restaurant

follows:

Cost

Direct

Materials

Direct

Labor

Overhead

Selling

Expenses

Ingredients ………………………………………….

X

Cook wages ………………………………………..

X

Manager salary ……………………………………

X

X

Coupon costs ……………………………………..

X

Advertising ………………………………………… .

X

X

Disposable plates, utensils, cups………….

X

Nondisposable plates, utensils, cups ……

X

Repair costs ………………………………………..

X

Property taxes …………………………………….

X

Store depreciation ……………………………….

X

Cashier salary ……………………………………..

X

Beverages …………………………………………..

X

Building heat and A/C ………………………….

X

Salad ingredients …………………………………

X

Delivery person wages …………………………

X

Power costs for ovens …………………………

X

In service businesses, the distinction between direct labor and overhead will not always be

clear.

CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

TIF 15–3 (FIN MAN); TIF 1–3 (MAN)

Memo

To: Todd Johnson

From: A+ Student

Re: Financial vs. Managerial Accounting Information

The objectives of financial and managerial accounting are quite different, and your

statement does not fully consider these differences. In one sense, your statement may be

appropriate at high levels in the organization. For example, it is appropriate to evaluate a

division manager who is responsible for the overall performance of a division using the

The stockholders’ interest in profit is related to increasing shareholder value. Managers

must increase long-term shareholder value by engaging in strategies that enhance people,

CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

TIF 15–4 (FIN MAN); TIF 1–4 (MAN)

a. The vice president of the Information Systems Division can use managerial accounting

b. The hospital administrator can use managerial accounting information in a number of

ways. One way is for cost planning and control. The administrator could use managerial

information to keep costs commensurate with services provided and to plan for staffing

c. The CEO of the food company will use managerial accounting information to support the

control of the three divisions. Each of the three divisions will be subject to a number of

d. The copy shop manager needs fairly simple managerial accounting information. At the

most basic level, the copy shop manager needs to know the costs of performing various

copy tasks, such as one-sided copy, two-sided copy, collating, and binding. These

CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

TIF 15–5 (FIN MAN); TIF 1–5 (MAN)

a. The High Times manager will use managerial accounting information to accumulate the

costs associated with different menu items. The costs, direct and indirect, will help in

determining the pricing strategy.

b. The plant manager is going to use cost information on scrap and rework to identify the

amount of waste occurring in the plant. This measure of waste is fairly common in

c. The cost of ending inventory must be determined as financial statements are prepared.

The division controller will likely require inventory valuation at the close of every month

in order to have a good understanding of the month-by-month earnings of the division.

The division controller will provide the ending inventory information by using managerial

accounting information in determining the cost of products. To determine the

appropriate cost, the product cost is multiplied by the units left in inventory.

d. The Maintenance Department manager needs to be able to plan the resources used by

his department. The planning process involves identifying the required resources to

CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

TIF 15–6 (FIN MAN); TIF 1–6 (MAN)

a. Obie’s bill has a number of points that should be considered. Some of the points, with

the appropriate argument, are identified below.

● The trip back to the shop resulted in an $80 labor charge. Obie should argue that the

whole hour should not be billed. The hour is the result of stocking out of a circuit

● The overtime premium should not have been charged to Obie. What if Obie was the

first appointment in the morning? If he was, there would be no overtime premium. It’s

only if the decision for overtime was caused by or required by Obie.

Thus, the labor portion of the bill should only be $70 + $60 + $60 = $190.

There are other parts of the bill that should not be in dispute.

● The materials storage and handling charge is a normal charge of maintaining a parts

inventory for the benefit of clients that need parts.

costs.

● The additional charge for the first hour is also reasonable. The first hour charge

covers the costs of transit, which are directly attributable to making a home visit.

Obie requires a home visit, so Obie should be responsible for the costs of making the

visit. If Obie brought the computer to the shop, this cost would not be incurred.

CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

TIF 15–6 (FIN MAN); TIF 1–6 (MAN) (Concluded)

b.

Cost

Direct Materials

Direct Labor

Overhead

Circuit board ………………………………………

X

Storage and handling ………………………….

X

Straight-time labor ………………………………

X

Fringe benefits* …………………………………..

X

Overhead ……………………………………………

X

Vehicle depreciation and fuel ………………

X

Overtime premium ………………………………

X

CHAPTER 15 (FIN MAN); CHAPTER 1 (MAN) Introduction to Managerial Accounting

CERTIFIED MANAGEMENT ACCOUNTANT (CMA®)

EXAMINATION QUESTIONS (ADAPTED)

1. b. Sales commissions on cars would be part of the selling expense for the car

2. c. Plunkett’s product costs are $656,100 and the period costs are $493,000, as follows:

Product

Costs

Direct materials

$ 56,000

Direct labor

179,100

Overhead

421,000

Total

$656,100

Period

Costs

Selling expenses

Administrative expenses

229,400

Fire loss

27,700

Total

$493,000

3. c. Prime costs of $150,000 are the combination of direct material costs of $100,000 and

direct labor costs of $50,000. Conversion costs of $130,000 are the combination of

direct labor costs of $50,000 and overhead costs of $80,000.

4. c. Factory overhead includes those items that cannot be directly traced to any one