Problem 1-4B (LO 1-3)

(Suggested order of calculation)

On the statement of stockholders’ equity,

$7,000 + $5,000 − (d) = $8,000

(d) = $4,000

Problem 1-5B (LO 1-3)

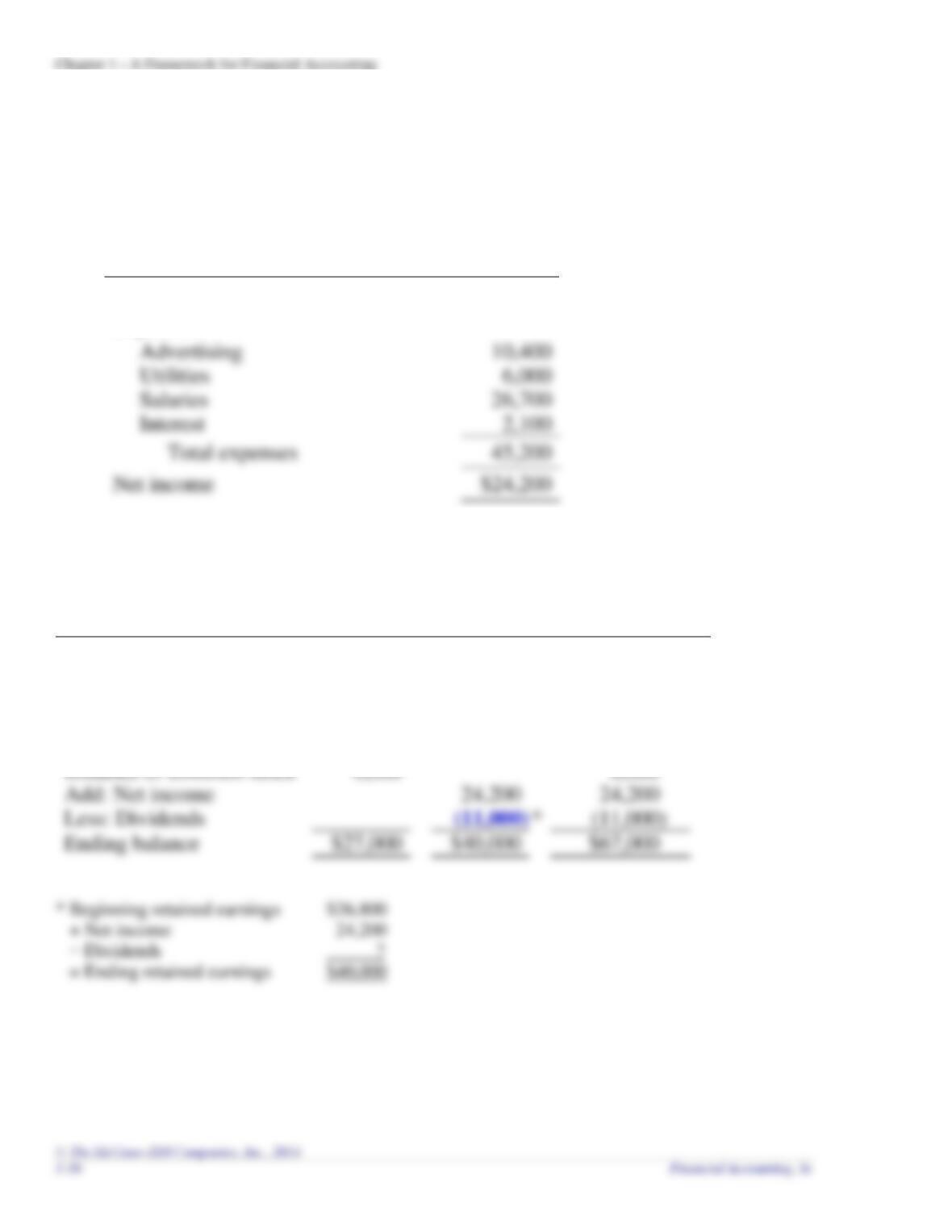

Tar Heel Corporation

Income Statement

For the year ended December 31, 2018

Service revenues

$69,400

Expenses:

Net income

Tar Heel Corporation

Statement of Stockholders’ Equity

For the year ended December 31, 2018

Common

Stock

Retained

Earnings

Total

Stockholders’

Equity

Beginning balance

$21,000

$26,800

$47,800

Issuance of common stock

Add: Net income

Less: Dividends

Ending balance

$27,000

Chapter 1 – A Framework for Financial Accounting

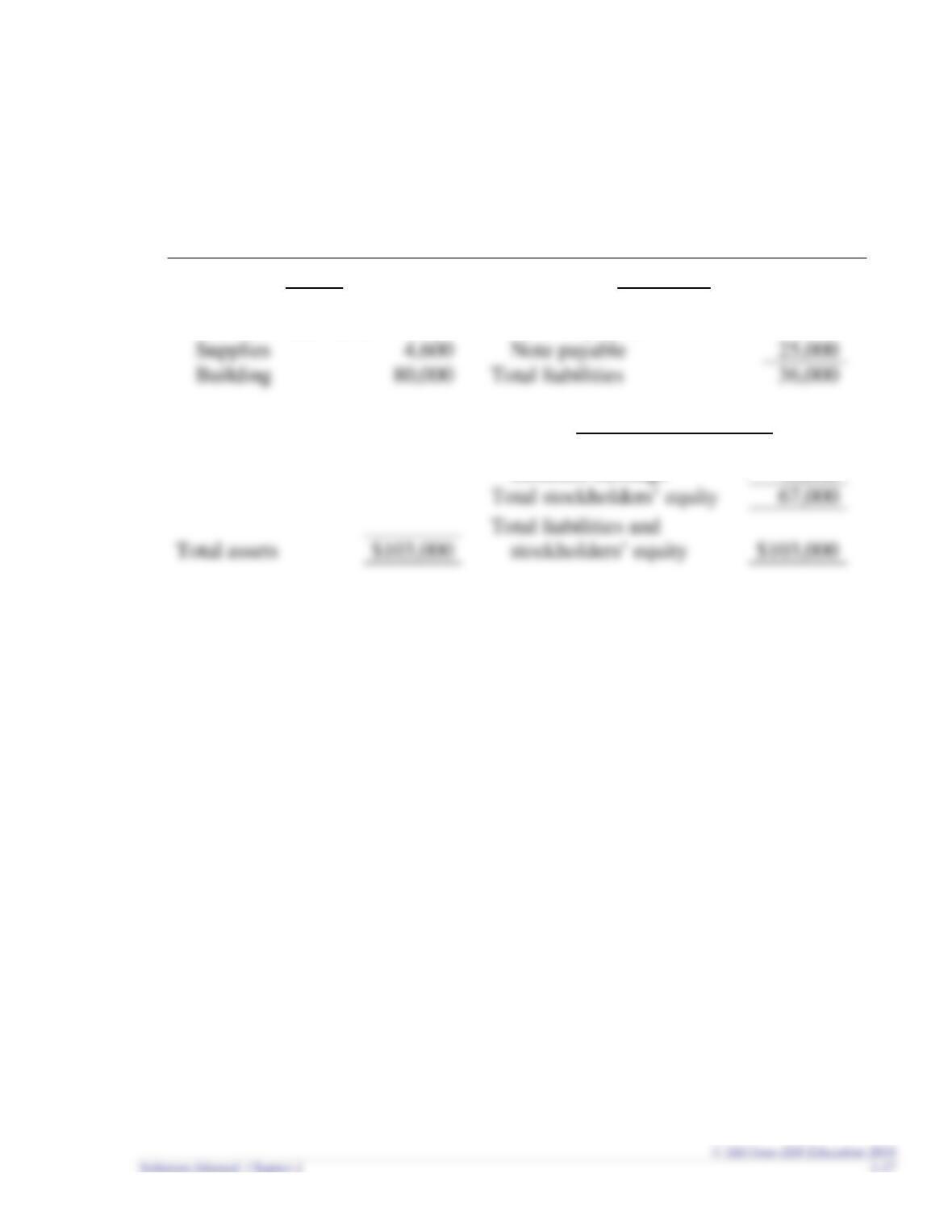

Problem 1-5B (concluded)

Tar Heel Corporation

Balance Sheet

December 31, 2018

Assets

Liabilities

Cash

$ 5,200

Accounts payable

$ 7,700

Accounts receivable

13,200

Salaries payable

3,300

Supplies

Note payable

Building

Total liabilities

Stockholders’ Equity

Common stock

27,000

Retained earnings

40,000

67,000

$103,000

Total assets

Problem 1-6B (LO 1-7)

Assumption violated

1.

Periodicity

2.

Monetary unit

4.

Economic entity

Problem 1-7B (LO 1-7)

1.

h.

2.

g.

3.

f.

4.

a.

6.

e.

7.

i.

8.

b.

9.

c.

Chapter 1 – A Framework for Financial Accounting

ADDITIONAL PERSPECTIVES

Additional Perspective 1-1

Requirement 1

The three primary forms of business organizations include sole proprietorship, partnership, and

corporation. The major advantage of a corporation is limited liability. Stockholders of a corporation

Requirement 2

Typical financing activities include issuing common stock, borrowing, and repayment of borrowing.

Typical investing activities include the purchase of long-term assets such as land, buildings,

Requirement 3

Assets – cash, accounts receivable, supplies, and equipment.

Requirement 4

Income statement – revenues less expenses equal net income during an interval of time.

Chapter 1 – A Framework for Financial Accounting

Additional Perspective 1-2

Requirement 1

Total assets = $1,696,908 ($ in thousands)

Requirement 2

Requirement 3

Net sales = $3,282,867 ($ in thousands)

Requirement 4

Inflows

Outflows

Investing activities

Sale of available-for-sale

Capital expenditures for

Requirement 5

The company’s auditor is Ernst & Young LLP. The auditor states, “In our opinion, the

financial statements referred to above present fairly, in all material respects, the

Chapter 1 – A Framework for Financial Accounting

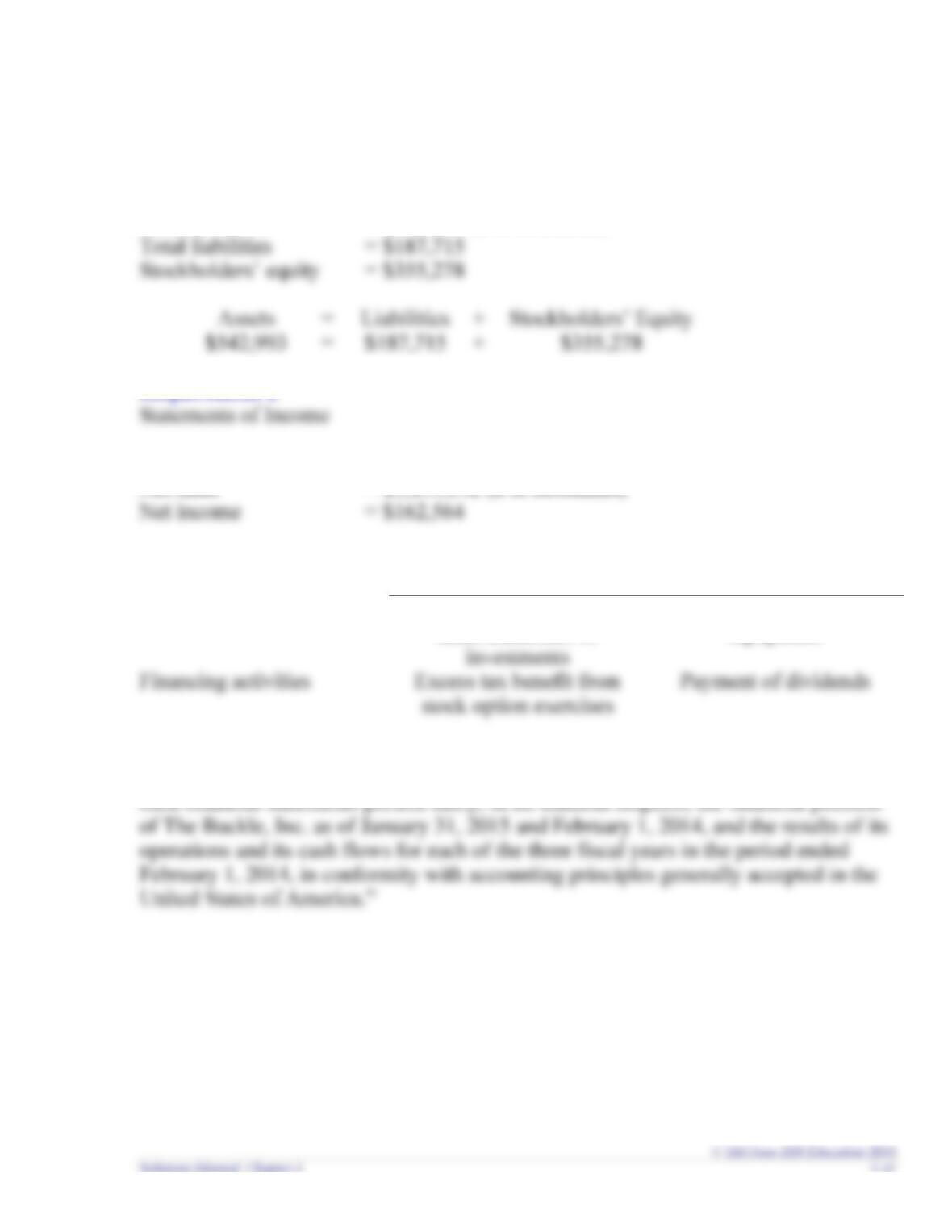

Additional Perspective 1-3

Requirement 1

Total assets = $542,993 ($ in thousands)

Requirement 2

Requirement 3

Net sales = $1,153,142 ($ in thousands)

Requirement 4

Inflows

Outflows

Investing activities

Proceeds from

sales/maturities of

Purchases of property and

equipment

Requirement 5

The company’s auditor is Deloitte & Touche LLP. The auditor states, “In our opinion,

Chapter 1 – A Framework for Financial Accounting

Additional Perspective 1-4

Requirement 1

The total assets of American Eagle are higher than the total assets of Buckle.

Requirement 2

The total liabilities of American Eagle are higher than the total liabilities of Buckle. A

higher amount of liabilities does not necessarily mean a higher chance of bankruptcy.

Requirement 3

Requirement 4

The net income of Buckle is higher than the net income of American Eagle. When one

Requirement 5

Net income provides a measure of a company’s ability to generate profit for its

Chapter 1 – A Framework for Financial Accounting

Additional Perspective 1-5

It is the responsibility of auditors to act independently of a company when providing a

professional opinion as to the conformity of the company’s financial statements with

GAAP. An auditor’s ethics might be challenged because of the need to retain the

Chapter 1 – A Framework for Financial Accounting

Additional Perspective 1-6

Requirement 1

The mission of the U.S. Securities and Exchange Commission is to protect investors,

maintain fair, orderly, and efficient markets, and facilitate capital formation.

The Securities Act of 1933 has two basic objectives:

by companies with publicly traded securities.

Chapter 1 – A Framework for Financial Accounting

Additional Perspective 1-6 (continued)

Requirement 2

The four main financial statements discussed by the SEC are: (1) balance sheets;

(2) income statements; (3) cash flow statements; and (4) statements of shareholders’

equity.

A balance sheet provides detailed information about a company’s assets, liabilities and

shareholders’ equity.

Chapter 1 – A Framework for Financial Accounting

Additional Perspective 1-6 (concluded)

Requirement 3

The mission of the FASB is to establish and improve standards of financial accounting

and reporting for the guidance and education of the public, including issuers, auditors,

Requirement 4

Chapter 1 – A Framework for Financial Accounting

Additional Perspective 1-7

The functions of financial accounting are to measure business activities of a company

and to communicate information about those activities to investors and creditors and

other outside users for decision-making purposes.

The four financial statements include:

1. Income statement, which shows revenues and expenses during the reporting period.