1. Some users of accounting information include managers, employees, investors, creditors,

customers, and the government.

2. The role of accounting is to provide information for managers to use in operating the business.

In addition, accounting provides information to others to use in assessing the economic

p

erformance and condition of the business.

5. The land should be recorded at its cost of $167,500 to Reliable Repair Service. This is consistent

with the cost concept.

6. a. No. The offer of $2,000,000 and the increase in the assessed value should not be recognized

in the accounting records because land is recorded on the cost basis.

b. Cash would increase by $2,125,000, land would decrease by $900,000, and owner’s equity

would increase by $1,225,000.

7. An account receivable is a claim against a customer for goods or services sold. An account

p

ayable is an amount owed to a creditor for goods or services purchased. Therefore, an account

receivable in the records of the seller is an account payable in the records of the purchaser.

8. (b) The business realized net income of $91,000 ($679,000 – $588,000).

CHAPTER 1

INTRODUCTION TO ACCOUNTING AND BUSINESS

DISCUSSION QUESTIONS

CHAPTER 1 Introduction to Accounting and Business

PE 1-1A

$597,000. Under the cost concept, the land should be recorded at the cost to Boulder

Repair Service.

PE 1-1B

$369,500. Under the cost concept, the land should be recorded at the cost to

Clementine Repair Service.

PE 1-2B

a. A = L + OE

$382,000 = $94,000 + OE

OE = $288,000

b. A = L + OE

–$63,000 = +$35,000 + OE

OE = –$98,000

OE on December 31, 20Y9 = $288,000 – $98,000

= $190,000

PE 1-3A

(2) Asset (Accounts Receivable) increases by $22,400;

Owner’s Equity (Delivery Service Fees) increases by $22,400.

(3) Liability (Accounts Payable) decreases by $4,100;

PRACTICE EXERCISES

CHAPTER 1 Introduction to Accounting and Business

PE 1-3B

(2) Owner’s Equity (Advertising Expense, increases) decreases by $6,750;

Asset (Cash) decreases by $6,750.

(5) Asset (Cash) increases by $11,410;

Asset (Accounts Receivable) decreases by $11,410.

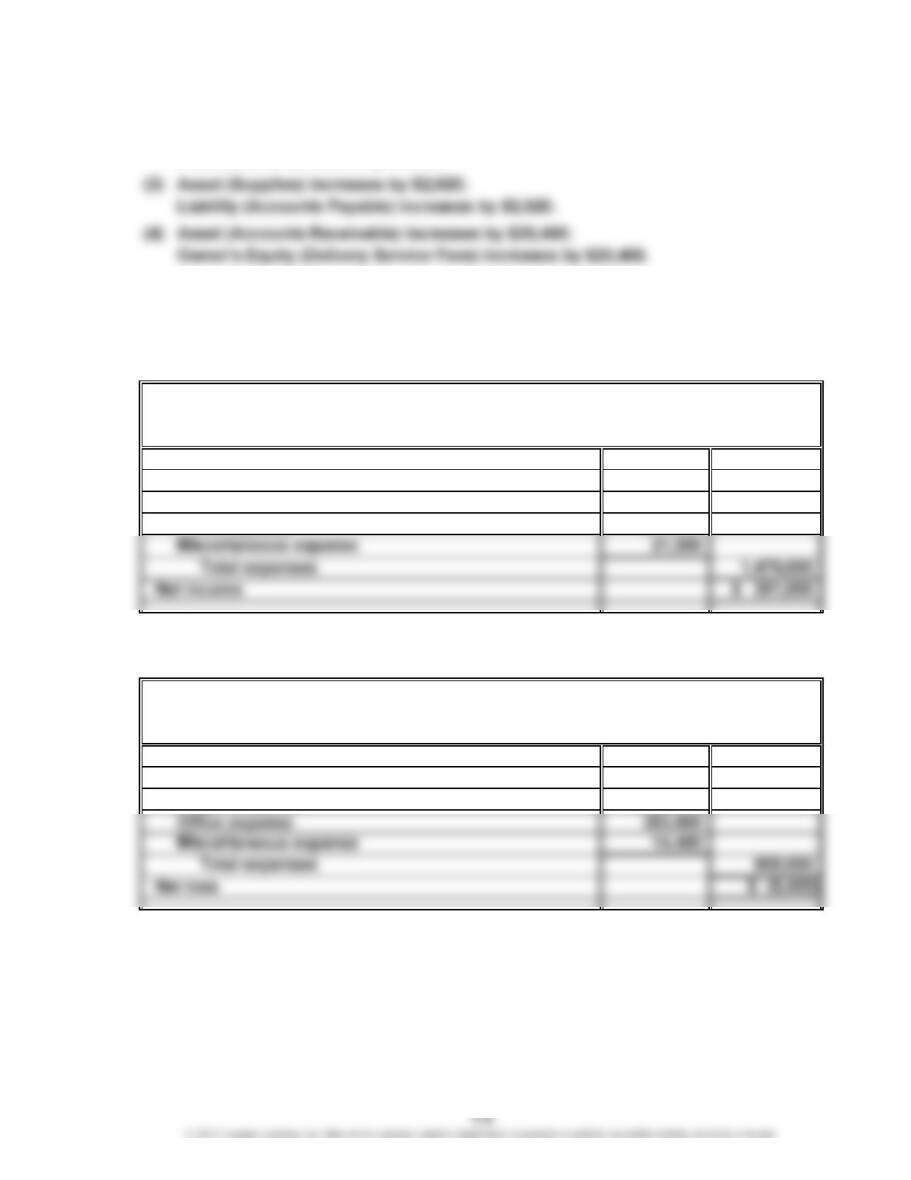

PE 1-4A

Fees earned $1,870,000

Expenses:

Wages expense $1,115,000

Office expense 343,000

PE 1-4B

Fees earned $899,600

Expenses:

Wages expense $539,800

Income Statement

For the Year Ended August 31, 20Y4

Up-in-the-Air Travel Service

Income Statement

For the Year Ended April 30, 20Y7

Zenith Travel Service

CHAPTER 1 Introduction to Accounting and Business

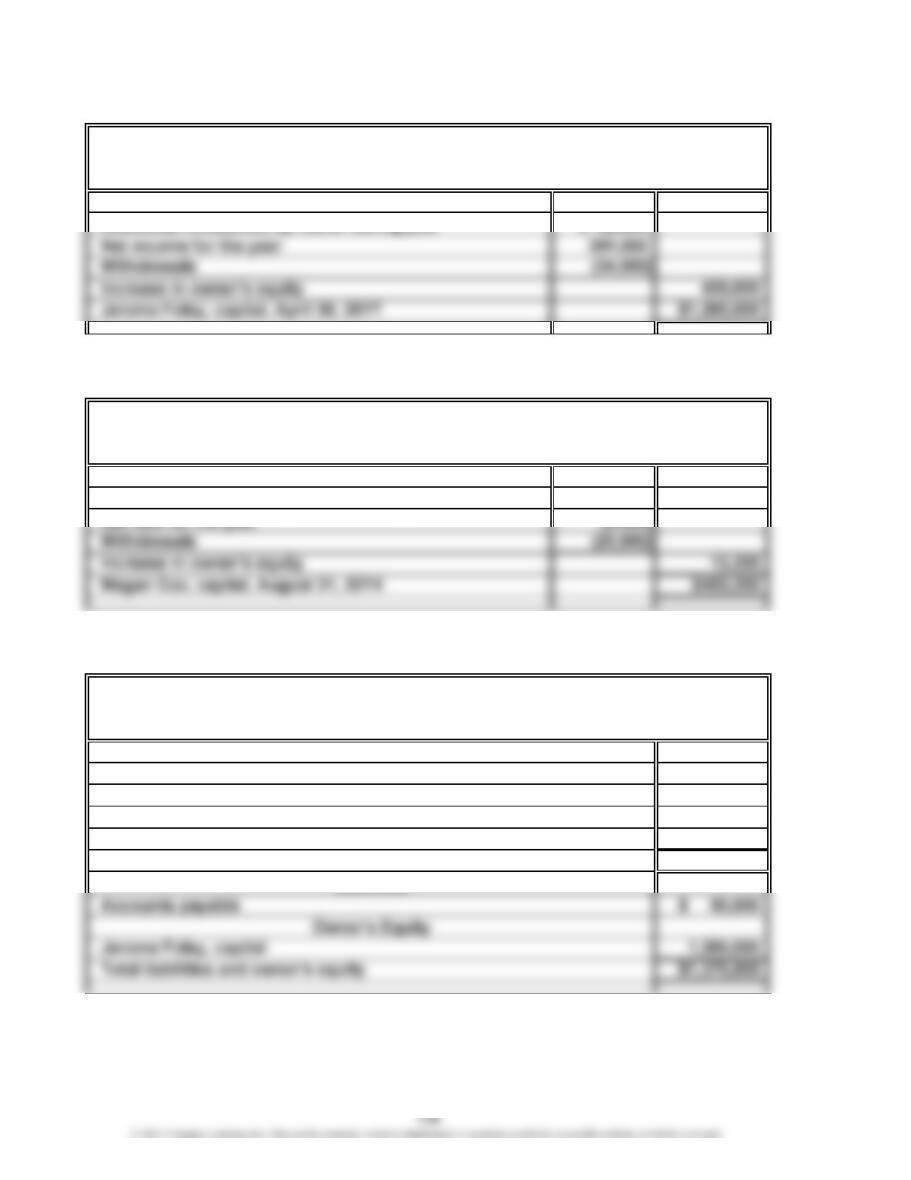

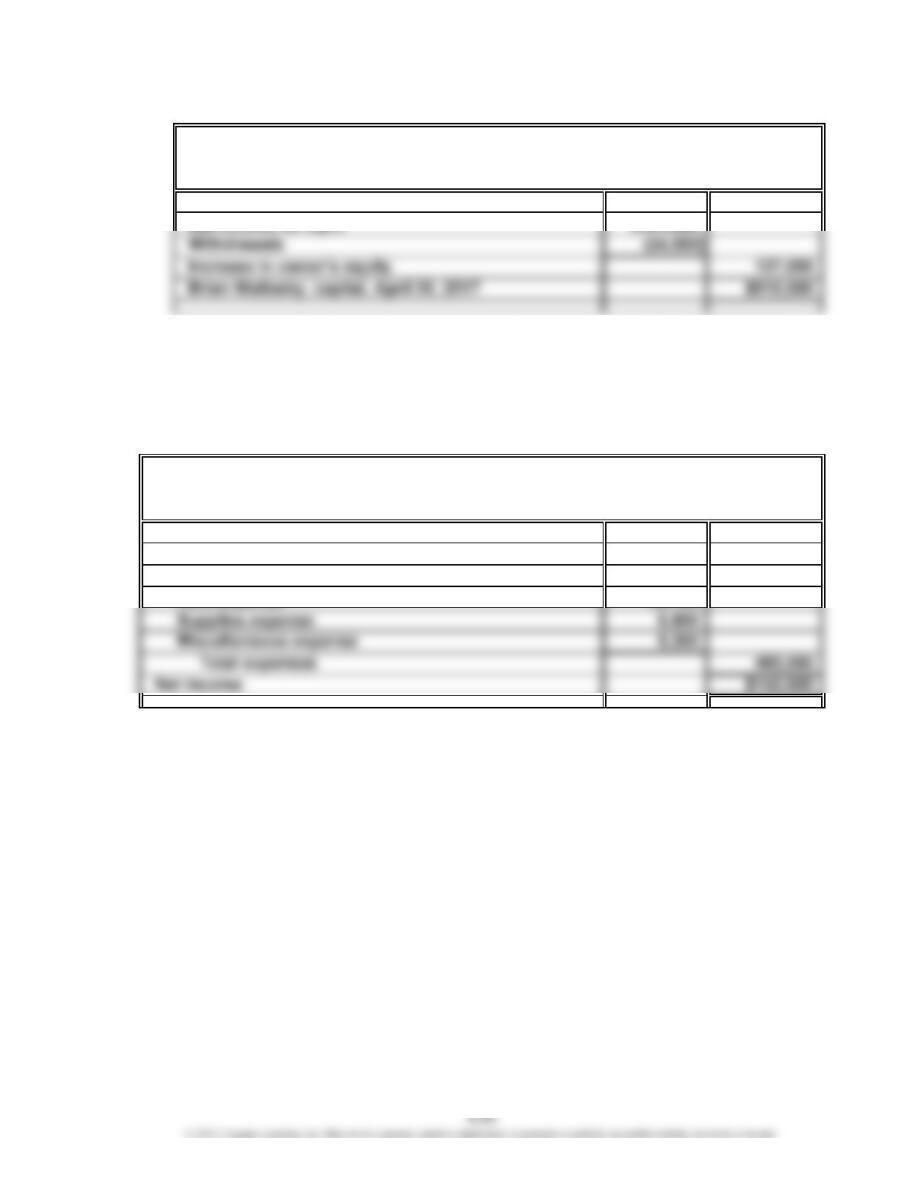

PE 1-5A

Jerome Foley, capital, May 1, 20Y6 $ 876,000

PE 1-5B

Megan Cox, capital, September 1, 20Y3 $456,000

Additional investment by owner during year $ 43,200

PE 1-6A

Cash $ 170,000

Accounts receivable 417,000

Supplies 16,000

Land 772,000

Total assets $1,375,000

Assets

Up-in-the-Air Travel Service

Balance Sheet

April 30, 20Y7

Zenith Travel Service

Statement of Owner’s Equity

For the Year Ended August 31, 20Y4

Up-in-the-Air Travel Service

Statement of Owner’s Equity

For the Year Ended April 30, 20Y7

PE 1-6B

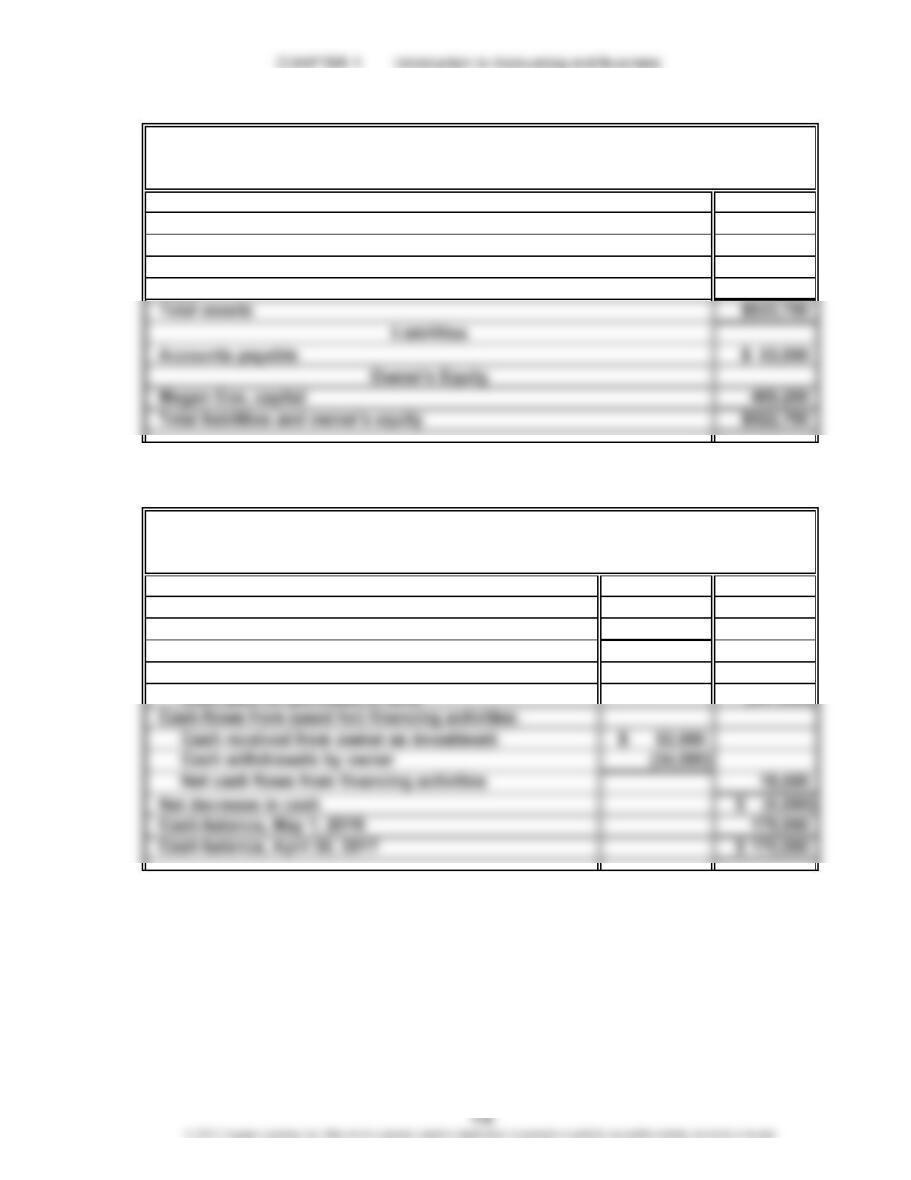

Cash $ 54,500

Accounts receivable 90,600

Supplies 5,600

Land 372,000

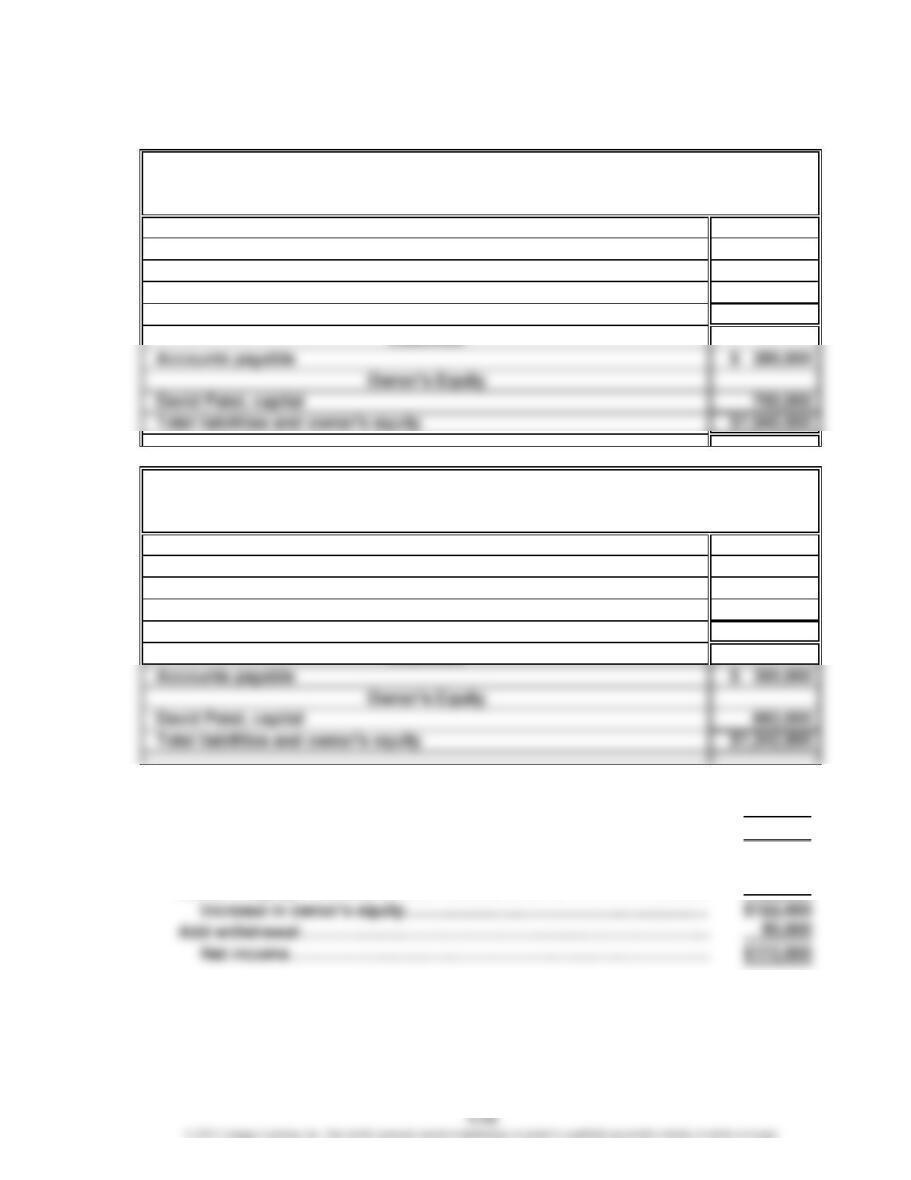

PE 1-7A

Cash flows from (used for) operating activities:

Cash received from customers $ 1,803,000

Cash paid for operating expenses (1,479,000)

Net cash flows from operating activities $ 324,000

Cash flows from (used for) investing activities:

For the Year Ended April 30, 20Y7

Zenith Travel Service

Balance Sheet

August 31, 20Y4

Assets

Up-in-the-Air Travel Service

Statement of Cash Flows

CHAPTER 1 Introduction to Accounting and Business

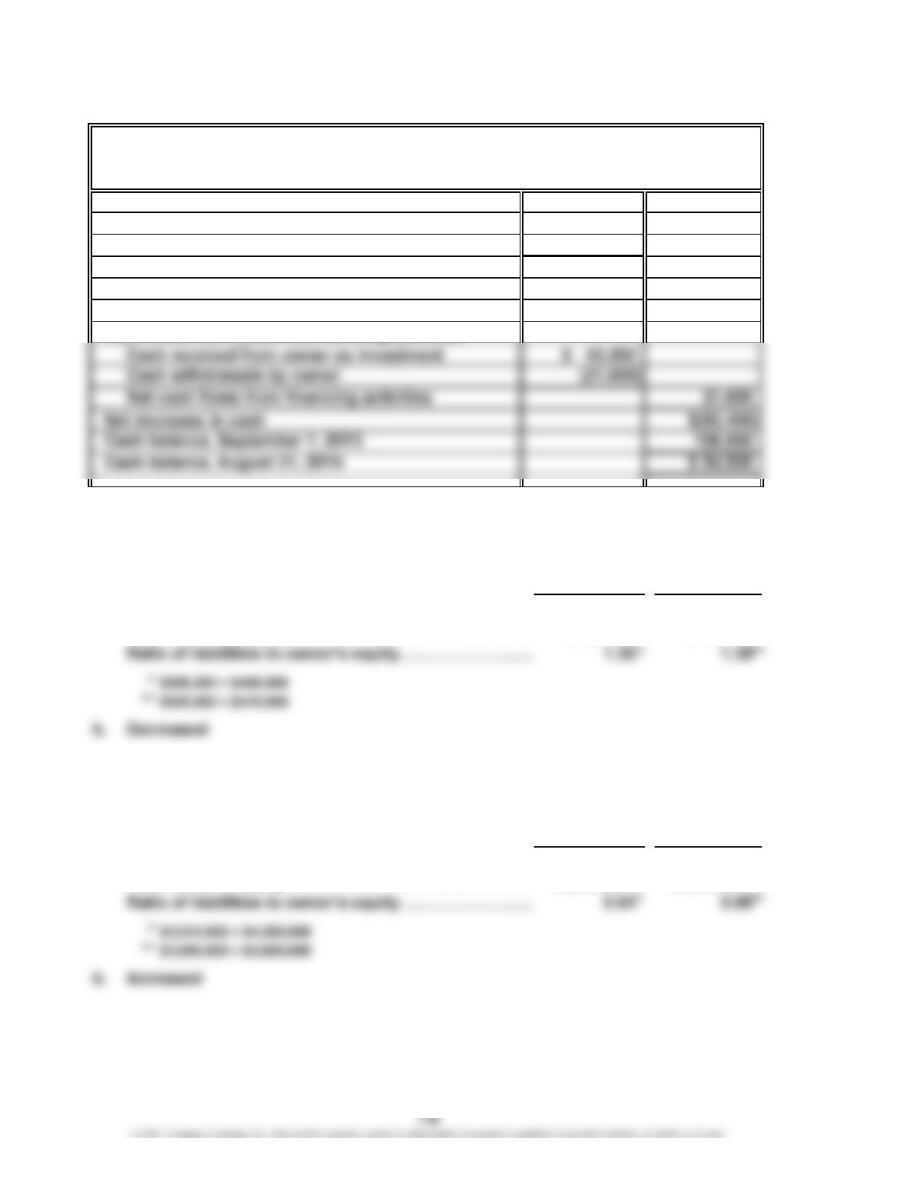

PE 1-7B

Cash flows from (used for) operating activities:

Cash received from customers

Cash paid for operating expenses

Net cash flows used for operating activities

Cash flows from (used for) investing activities:

Cash paid for purchase of land

PE 1-8A

a. Dec. 31, Dec. 31,

20Y6 20Y5

Total liabilities……………………………………………… $598,000 $569,900

Total owner’s equity………………………………………

…

$460,000 $410,000

PE 1-8B

a. Dec. 31, Dec. 31,

20Y6 20Y5

Total liabilities……………………………………………… $4,042,000 $3,096,000

Total owner’s equity………………………………………

…

$4,300,000 $3,600,000

Zenith Travel Service

Statement of Cash Flows

For the Year Ended August 31, 20Y4

$(14,000)

(60,000)

$ 881,000

(895,000)

CHAPTER 1 Introduction to Accounting and Business

Ex. 1-1

a. 1. manufacturing 6. service 11. service

2. manufacturing 7. service 12. service

Ex. 1-2

As in many ethics issues, there is no one right answer. Oftentimes, disclosing

only what is legally required may not be enough. In this case, it would be best

for the company’s chief executive officer to disclose both reports to the county

representatives. In doing so, the chief executive officer could point out any flaws

or deficiencies in the fired researcher’s report.

Ex. 1-3

a. 1. K 5. B 9. X

2. G 6. B 10. B

Ex. 1-4

Dunkin’s stockholders’ equity: $3,457 – $4,170 = ($713)

Starbucks’ stockholders’ equity: $24,156 – $22,981 = $1,175

EXERCISES

CHAPTER 1 Introduction to Accounting and Business

Ex. 1-6

a. $4,474,000 ($633,000 + $3,841,000)

b. $387,500 ($6,124,500 – $5,737,000)

c. $1,232,900 ($1,981,800 – $748,900)

Ex. 1-7

Ex. 1-8

a. (1) asset

b. (2) liability

c. (1) asset

d. (3) owner’s equity (revenue)

e. (1) asset

f. (3) owner’s equity (expense)

g. (1) asset

Ex. 1-9

Ex. 1-10

a. (1) Total assets increased $183,000 ($298,000 – $115,000).

(2) No change in liabilities.

(3) Owner’s equity increased $183,000.

b. (1) Total assets decreased $80,000.

(2) Total liabilities decreased $80,000.

CHAPTER 1 Introduction to Accounting and Business

Ex. 1-11

1. (b) decrease

2. (a) increase

Ex. 1-12

1. c 6. c

2. a 7. d

3. e 8. a

Ex. 1-13

a. (1) Provided catering services for cash, $71,800.

(2) Purchase of land for cash, $15,000.

(3) Payment of cash for expenses, $47,500.

(4) Purchase of supplies on account, $1,100.

(5) Withdrawal of cash by owner, $5,000.

Ex. 1-14

No. It would be incorrect to say that the business had incurred a net loss of

$8,000. The excess of the withdrawals over the net income for the period is a

decrease in the amount of owner’s equity in the business.

CHAPTER 1 Introduction to Accounting and Business

Ex. 1-15

Owner’s equity at end of year ($928,000 – $352,000)…………………………

…

$576,000

Deduct owner’s equity at beginning of year ($605,000 – $237,000)………

…

368,000

Net income (increase in owner’s equity)……………………………………

…

$208,000

Increase in owner’s equity (as determined for Dakota)……………………… $208,000

Deduct additional investment……………………………………………………

…

66,000

Net income (increase in owner’s equity)……………………………………

…

$142,000

…

…

…

Ex. 1-16

Balance sheet items: 1, 2, 3, 4, 6, 8, 10

Ex. 1-17

Income statement items: 5, 7, 9

Iowa

Dakota

Jersey

Carolina

…

…

CHAPTER 1 Introduction to Accounting and Business

Ex. 1-18

a.

Brian Walinsky, capital, April 1, 20Y7 $373,000

b. The statement of owner’s equity is prepared before the April 30, 20Y7, balance

sheet because Brian Walinsky, Capital as of April 30, 20Y7, is needed for the

balance sheet.

Ex. 1-19

Fees earned $627,600

Expenses:

Wages expense $440,800

Income Statement

For the Month Ended August 31, 20Y2

Pegasus Product Company

Statement of Owner’s Equity

For the Month Ended April 30, 20Y7

Hermes Services

CHAPTER 1 Introduction to Accounting and Business

Ex. 1-20

In each case, solve for a single unknown, using the following equation:

Owner’s Equity (beginning) + Investments – Withdrawals + Revenues – Expenses

= Owner’s Equity (ending)

Freeman

Owner’s equity at end of year ($1,260,000 – $330,000)……………

…

$930,000

Heyward

Owner’s equity at end of year ($675,000 – $220,000)………………

…

$455,000

Owner’s equity at beginning of year ($490,000 – $260,000)………

…

230,000

Increase in owner’s equity………………………………………………

…

$225,000

…

…

Jones

Owner’s equity at end of year ($100,000 – $80,000)…………………

…

$ 20,000

Owner’s equity at beginning of year ($115,000 – $81,000)…………

…

34,000

Decrease in owner’s equity……………………………………………… $(14,000)

…

…

Ramirez

Owner’s equity at end of year ($270,000 – $136,000)………………

…

$134,000

Add decrease due to net loss ($115,000 – $128,000)………………

…

(13,000)

Add withdrawals………………………………………………….………

…

39,000

Beginning owner’s equity plus additional investment ……………

…

$186,000

Deduct additional investment…………………………………………… 55,000

…

…

…

…

CHAPTER 1 Introduction to Accounting and Business

Ex. 1-21

a.

Cash $ 290,000

Accounts receivable 720,000

Supplies 30,000

Total assets $1,040,000

Cash $ 340,000

Accounts receivable 870,000

Supplies 32,000

Total assets $1,242,000

b. Owner’s equity, March 31……………………………………………………

…

$882,000

Owner’s equity, February 29…………………….…………………………… 760,000

Net income…………………………………………………………………

…

$122,000

c. Owner’s equity, March 31……………………………………………………

…

$882,000

Owner’s equity, February 29…………………….…………………………… 760,000

…

Assets

Assets

March 31, 20Y0

Rockwell Interiors

Balance Sheet

February 29, 20Y0

Rockwell Interiors

Balance Sheet

CHAPTER 1 Introduction to Accounting and Business

Ex. 1-22

a. Balance sheet: 1, 2, 3, 4, 6, 7, 8, 9, 10, 11, 13

Income statement: 5, 12, 14, 15

Ex. 1-23

1. (a) operating activity

2. (a) operating activity

Ex. 1-24

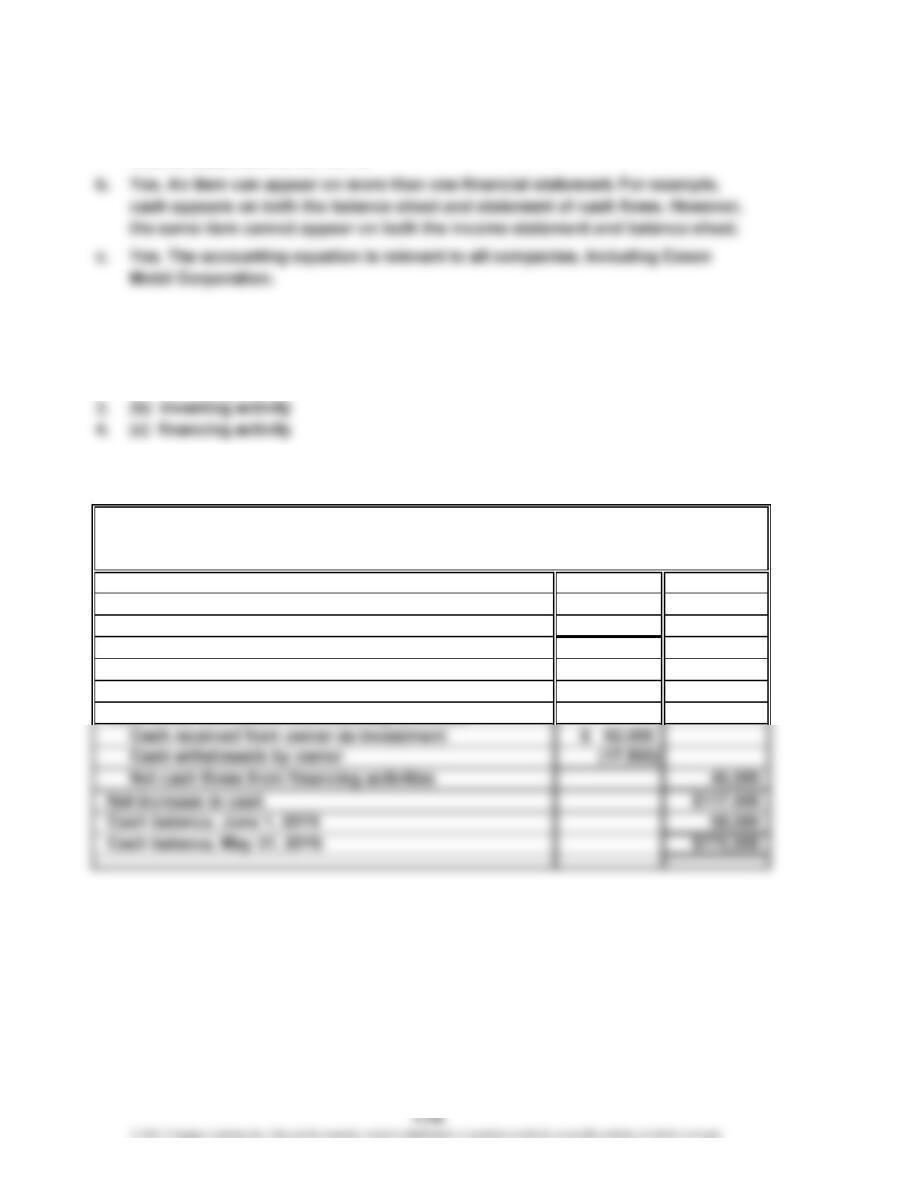

Cash flows from (used for) operating activities:

Cash received from customers

Cash paid for operating expenses

Net cash flows from operating activities

Cash flows from (used for) investing activities:

Cash paid for purchase of land

Ethos Consulting Group

Statement of Cash Flows

For the Year Ended May 31, 20Y6

$162,500

(475,000)

$ 637,500

(90,000)

CHAPTER 1 Introduction to Accounting and Business

Ex. 1-25

1. All financial statements should contain the name of the business in their

heading. The statement of owner’s equity is incorrectly headed as “Omar

Farah” rather than We-Sell Realty. The heading of the balance sheet needs

the name of the business.

2. The income statement and statement of owner’s equity cover a period of time

and should be labeled “For the Month Ended August 31, 20Y9.”

5. In the income statement, the miscellaneous expense amount should be listed

as the last expense.

6. In the income statement, the total expenses are incorrectly subtracted from

the sales commissions, resulting in an incorrect net income amount. The

correct net income should be $24,150. This also affects the statement of

owner’s equity and the amount of Omar Farah, Capital, that appears on

the balance sheet.

7. In the statement of owner’s equity, the additional investment should be added

first to Omar Farah, capital, as of August 1, 20Y9. The net income should be

presented next, followed by the amount of withdrawals, which is subtracted

from the net income to yield the increase in owner’s equity. The increase in

owner’s equity is added to Omar Farah, capital on August 1, 20Y9, to determine

CHAPTER 1 Introduction to Accounting and Business

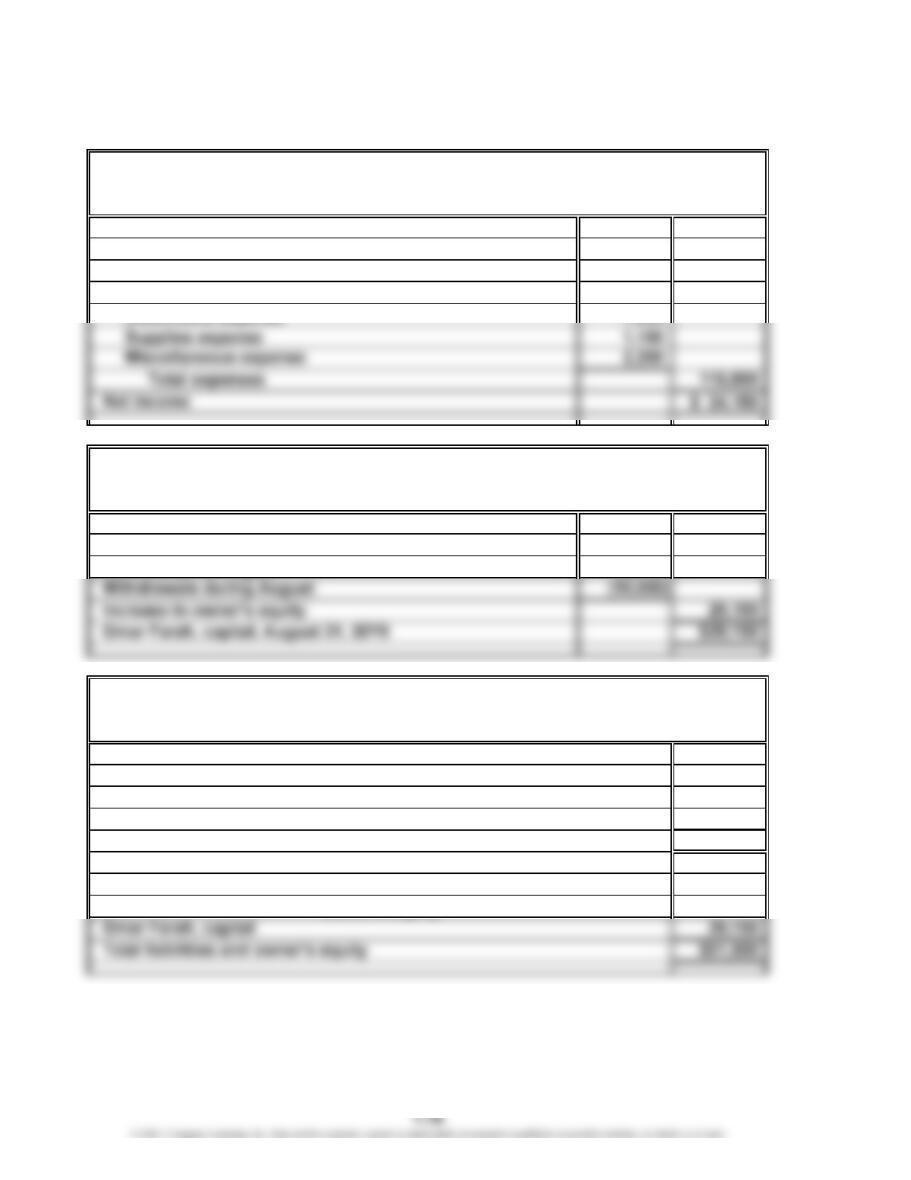

Ex. 1-25 (Concluded)

Corrected financial statements appear as follows:

Sales commissions $140,000

Expenses:

Office salaries expense $87,000

Rent expense 18,000

Omar Farah, capital, August 1, 20Y9 $0

Investment on August 1, 20Y9 $ 15,000

Net income for August 24,150

Cash $ 8,900

Accounts receivable 38,600

Supplies 4,000

Total assets $51,500

Accounts payable $22,350

Assets

Liabilities

Owner’s Equity

We-Sell Realty

Income Statement

For the Month Ended August 31, 20Y9

We-Sell Realty

Statement of Owner’s Equity

For the Month Ended August 31, 20Y9

We-Sell Realty

Balance Sheet

August 31, 20Y9

CHAPTER 1 Introduction to Accounting and Business

Ex. 1-26

a. Year 2: $43,075 ($44,529 – $1,454)

Year 1: $38,633 ($42,966 – $4,333)

Ex. 1-27

a. Year 2: $5,873 ($35,291 – $29,418)

Year 1: $6,434 ($34,408 – $27,974)

b. Year 2: 5.01 ($29,418 ÷ $5,873)

Year 1: 4.35 ($27,974 ÷ $6,434)

c. The risk for creditors has increased from 4.35 in Year 1 to 5.01 in Year 2.

CHAPTER 1 Introduction to Accounting and Business

Prob. 1-1A

1. Assets = +

+ +=+ – + ––– – –

(a) + 55,000 + 55,000

(b) + 3,300 + 3,300

Bal. 55,000 3,300 3,300 55,000

(c) + 18,300 + 18,300

Bal. 73,300 3,300 3,300 55,000 18,300

Bal. 62,710 30,800 3,300 1,010 55,000 49,100 – 8,300

(g) – 3,180 – 1,380 – 1,800

Bal. 59,530 30,800 3,300 1,010 55,000 49,100 – 8,300 – 1,380 – 1,800

(h) – 7,300 – 7,300

Bal. 52,230 30,800 3,300 1,010 55,000 49,100 – 8,300 – 7,300 – 1,380 – 1,800

(i) – 2,050 – 2,050

Bal. 52,230 30,800 1,250 1,010 55,000 49,100 – 8,300 – 7,300 – 2,050 – 1,380 – 1,800

(j) – 13,800 – 13,800

Bal. 38,430 30,800 1,250 1,010 55,000 – 13,800 49,100 – 8,300 – 7,300 – 2,050 – 1,380 – 1,800

2. Owner’s equity is the right of owners to the assets of the business. These rights are increased by owner’s investments and revenues

and decreased by owner’s withdrawals and expenses.

Misc.

Exp.

Rent

ExpenseCash

Pamela

Schatz,

Drawing

Supplies

Expense

PROBLEMS

Owner’s Equity

Accts.

Rec. Supplies

Accts.

Payable

Liabilities

Pamela

Schatz,

Capital

Fees

Earned

Salaries

Expense

Auto

Exp.

CHAPTER 1 Introduction to Accounting and Business

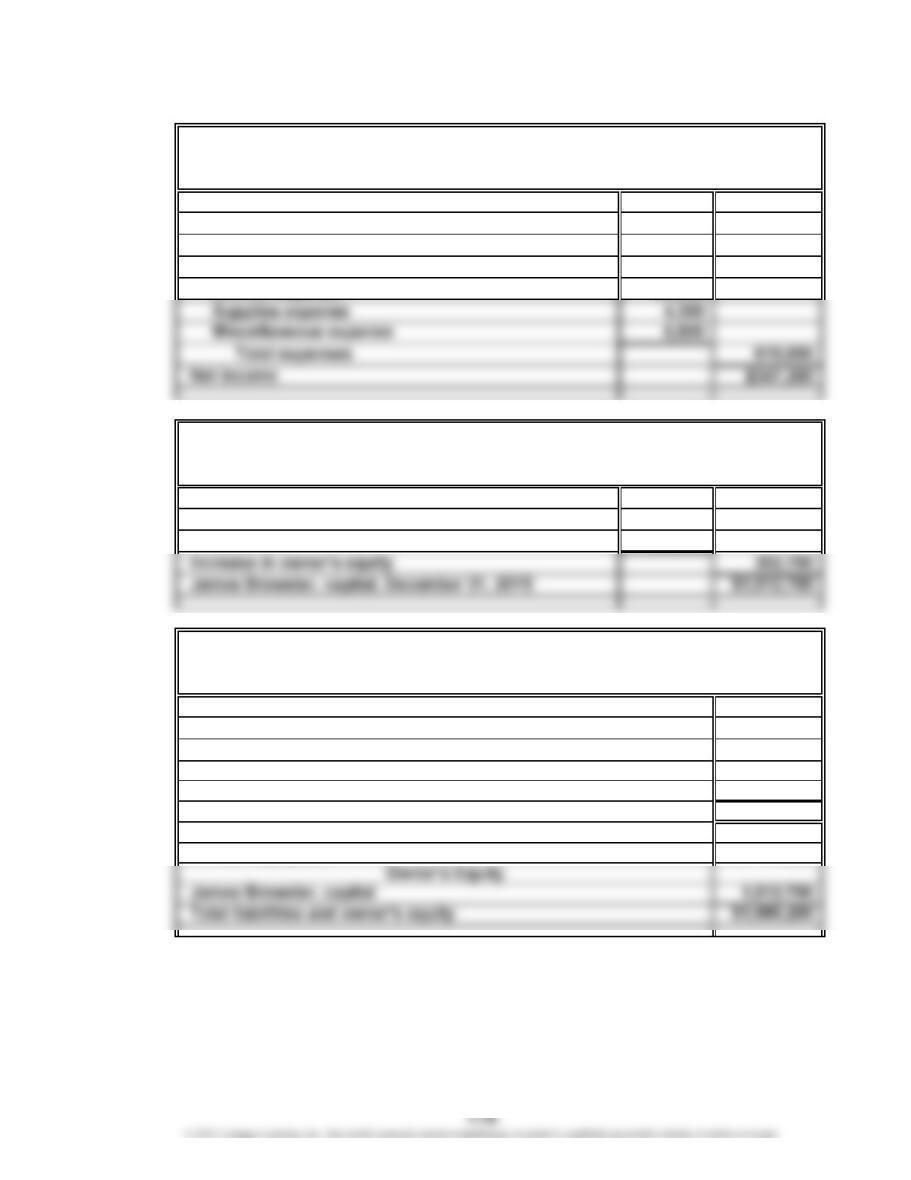

Prob. 1-2A

1.

Fees earned $967,000

Expenses:

Wages expense $540,400

Rent expense 38,100

2.

James Brewster, capital, January 1, 20Y5 $ 710,000

Net income for the year $347,200

Withdrawals (44,500)

3.

Cash $ 201,900

Accounts receivable 302,000

Supplies 5,800

Land 576,500

Total assets $1,086,200

Accounts payable $ 73,500

4. James Brewster, Capital of $1,012,700

For the Year Ended December 31, 20Y5

Excalibur Travel Agency

Excalibur Travel Agency

Income Statement

For the Year Ended December 31, 20Y5

Excalibur Travel Agency

Statement of Owner’s Equity

Assets

Liabilities

Balance Sheet

December 31, 20Y5

CHAPTER 1 Introduction to Accounting and Business

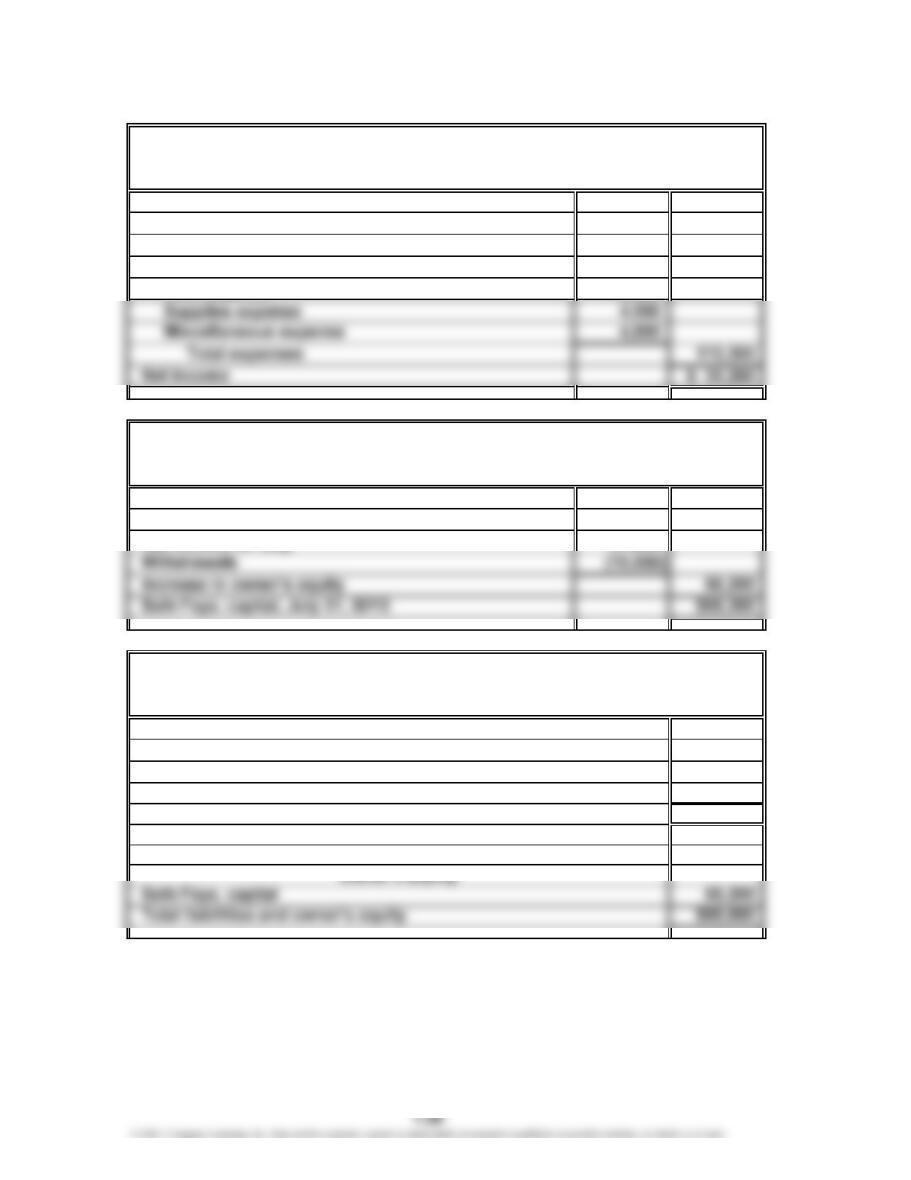

Prob. 1-3A

1.

Fees earned $144,500

Expenses:

Salaries expense $55,000

Rent expense 33,000

Auto expense 16,000

2.

Seth Feye, capital, July 1, 20Y2 $0

Investment on July 1, 20Y2 $ 50,000

3.

Cash $32,600

Accounts receivable 34,500

Supplies 2,500

Total assets $69,600

Accounts payable $ 3,400

Liabilities

For the Month Ended July 31, 20Y2

Reliance Financial Services

Balance Sheet

July 31, 20Y2

Assets

Reliance Financial Services

Income Statement

For the Month Ended July 31, 20Y2

Reliance Financial Services

Statement of Owner’s Equity