1

Cost Accounting: Information for Decision

Making

Solutions to Review Questions

1-1.

Among the goals of an organization, a central one is to create and increase value. Cost

1-2.

Financial accounting is designed to provide information about the firm to external users.

External users include investors, creditors, government authorities, regulators,

1-3.

1-4.

The value chain is the set of activities that transforms raw resources into the goods and

1-5.

1-6.

Value-added activities are activities that customers perceive as adding utility to the

1-7.

Answers will vary, but should include some of the following:

Title

Major Responsibilities and Major Duties

Chief financial officer (CFO) ………

• Oversees public issues of stock and debt

• Manages entire finance and accounting function

1-8.

Solutions to Critical Analysis and Discussion Questions

1-9.

We would not agree. The role of accountants is to help manage the organization. Part of

1-10.

The calculation of cost depends on the decision being made. Therefore, the first

1-11.

Costs that you could ask to be reimbursed might include the fuel, a share of the

maintenance costs, “wear and tear,” or depreciation, and insurance. To avoid

1-12.

Although it is not the “job” of accounting to determine strategy, accounting provides

1-13.

Executive performance evaluation systems are designed for a specific company’s

1-14.

Although not-for-profit organizations are not seeking to make a profit, they must remain

1-15.

Airlines are characterized by the need to own a substantial amount of capacity costs.

Managers at airlines require very sophisticated load management information that

1-16.

The cost accounting issues for Nabisco are the same as for Carmen’s Cookies in the

1-17.

In decision-making, managers or supervisors may wish to take actions that they believe

will increase the firm’s value that are difficult to justify given available information. Often,

1-18.

This is a tricky question. The problem is that if each firm tries to minimize its own cost,

1-19.

The purpose of bonuses is to provide incentives to managers to “work harder” when the

1-20.

The cost accountant provides information to decision makers in the firm. He or she

1-21.

Studying cost accounting will most likely increase Carmen’s chances of success with

her store. As illustrated in the chapter, she has a better idea of the costs of her business

1-22.

There are two types of costs the airline or hotel incur with such upgrades. One type of

cost results from the incremental resources that are a part of the upgraded service

Solutions to Exercises

1-23. (10 Min.) Value Chain and Classification of Costs: Apple, Inc.

Cost

Stage in the Value Chain

Programmer costs for a new operating system.

4. Research & Development

Costs to ship computers to customers.

6. Distribution

Call center costs for support calls.

3. Customer Service

designs.

5. Design

Costs to purchase advertising in university stores.

1. Marketing

1-24. (5 Min.) Supply Chain and Supply Chain Costs: Coastal Cabinets.

It is important that costs are minimized in the supply chain. Because it is cheaper for

1-25. (10 Min.) Accounting Systems: McDonald’s.

Decision Maker

System

a. Investor* ……………………………..

Financial (F)

b. Marketing manager ………………

Cost (C)

c. Competitor* …………………………

Financial (F)

d. Labor organization* ………………

Financial (F)

e. Advertising manager …………….

Cost (C)

system, but they would be unlikely to be given access to this information.

1-26. (10 Min.) Accounting Systems: Ford Motor Company.

Answers will vary, but examples include the following.

Manager

Example Decision

a. Plant manager …………………….

How to layout the plant.

b. Purchasing manager ……………

Which supplier to use.

c. Quality supervisor ………………..

Where to focus quality improvement efforts.

d. Personnel manager ……………..

Where to recruit workers

e. Maintenance supervisor ………

Whether to repair or replace a machine

1-27. (10 min.) Cost Data for Managerial Purposes: Delta Airlines.

a. Differential costs are costs that would change, which are the labor costs in this

situation. Other costs would presumably not be affected by the change in labor.

1-28. (20 Min.) Cost Data for Managerial Purposes: Betty’s Fashions.

Considering the following costs as differential shows that closing the City Division will

lower profits for the chain.

Betty’s Fashions, City Division

Divisional Income Statement

Differential Revenues and Costs

For the Year Ending January 31

Sales revenue ……………………………………….

$ 8,600,000

Differentiala

Costs

Advertising …………………………………………

350,000

Differentialb

Cost of goods sold ………………………………

4,300,000

Differentiala

Divisional administrative salaries …………..

580,000

Differentiala

Rent ………………………………………………….

Share of corporate administration ………….

Not differential

Total costs ………………………………………..

Net differential gain before income tax ………

1-29. (20 Min.) Cost Data for Managerial Purposes: State University Business

School.

Considering the following costs as differential shows that dropping the BBA degree will

lower profits for the school.

State University Business School

Degree Income Statement

Differential Revenues and Costs

For the Academic Year Ending June 30

Revenue ……………………………………………….

$ 6,000,000

Differentiala

Costs

Advertising – BBA program ……………………

225,000

Differentialb

Differentiala

Degree operating costs ………………………..

390,000

Differentiala

Building maintenance …………………………..

555,000

Differentiala

Differentiala

Not differential

Total costs ………………………………………..

$ 5,505,000

1-30. (20 Min.) Cost Data for Managerial Purposes: State University Business

School.

a. The following differential analysis shows that the combined contribution of the BBA

program will be positive.

State University Business School

Degree Income Statement

Differential Revenues and Costs, BBA Programs

For the Academic Year Ending June 30

Revenue ……………………………………………….

$ 6,000,000 x 2

$12,000,000

Costs

Advertising – BBA program ……………………

225,000 + (225,000 x 3)

900,000

Faculty salaries …………………………..………

3,060,000 x 2

6,120,000

Classroom costs ………………………………….

Classroom rental …………………………..……..

1-31. (20 Min.) Cost Data for Managerial Purposes––Budgeting

1-32. Trends in Cost Accounting

Answers will vary.

a. Activity-based costing might be used in the Design component to help designers

identify designs that will lead to less costly production requirements.

b. Benchmarking might be used in Purchasing to ensure the firm is not paying too

much for inputs.

1-33. Trends in Cost Accounting

Title

Responsibility

5 CFO

Signs off on financial statements.

3 Treasurer

Determines where to invest cash balances.

1 Internal auditor

Ensures procurement rules are followed.

2 Cost accountant

Evaluates costs of products.

1-34. (15 Min.) Ethics and Channel Stuffing: Continental Condiments.

a. As a management accountant, Maria has a responsibility to perform her professional

duties with competence in accordance with relevant laws and regulations. Channel

stuffing borders on illegal activity, especially if it is done to defraud investors by

confront the next higher level of management that she believes is not involved in the

marketing scheme. This could be the Controller or the CFO. If the matter remains

1-35. (15 Min.) Ethics and Cost Analysis: State University Business School.

a. As a management accountant, Jon has a responsibility to perform his professional

duties with competence in accordance with relevant laws and regulations. Choosing

Solutions to Problems

1-36. (15 Min.) Responsibility for Ethical Action: Giant Engineering.

a. As a management accountant Dewi has a responsibility to perform her professional

duties with competence in accordance with relevant laws and regulations. Clearly,

b. The first possible course of action is to discuss the situation with the controller. This

is an appropriate approach to the problem. Always take a problem to your immediate

1-37. (20 Min.) Cost Data for Managerial Purposes: Imperial Devices.

This problem demonstrates the ambiguity of cost-based contracting and, indeed, the

measurement of “cost.” This problem can stimulate a lively discussion in class.

Recommended prices may range from the $324 suggested by the state government to

the $522 charged by Imperial Devices. The key is to negotiate the cost-based price prior

to the signing of the contract. Considerations that affect the base costs are reflected in

the following options:

Options:

A. Only the differential production costs could be considered as the cost basis.

B. The total cost per device for normal production of 60,000 devices could be

used as the cost basis.

C. The total cost per device for production of 66,000 devices, excluding

marketing costs, could be used as the cost basis.

D. The total cost per device for production of 66,000 devices, including

marketing costs, could be used as the cost basis.

Costs

Unit Cost Options

(One Unit = One Device)

A

B

C

D

Materials (variable) ………………………………………

$75.00

$75.00

$75.00

$75.00

$75.00

Supplies (variable) ……………………………………….

Indirect costs (fixed) …………………………………….

Administrative (fixed) ……………………………………

Per device cost basis …………………………………..

a $45.00 = $2,700,000 ÷ 60,000 units.

We believe the most justifiable options exclude marketing costs and reflect the potential

1-38. (20 Min.) Cost Data for Managerial Purposes: Marco and Jenna.

b. If Jenna was not going to take the trip, then some of the “wear and tear” costs, for

1-39. (20 Min.) Cost Data for Managerial Purposes: T-Comm.

This problem demonstrates the ambiguity in measuring “costs.”

South Division’s controller included the “per unit” fixed costs, which were calculated for

allocation purposes under normal production volume, when he or she calculated the per

unit cost of the additional production. The controller charged North Division on that

basis, ignoring the differential costs as a basis for interdivision sales.

Possible options available are as follows:

Costs

Unit Cost Options:

A

B

C

Direct materials (variable) …………………………….

$ 200 a

$ 200

$ 200

$ 200

Direct Labor (variable) …………………………………

96 b

96

96

96

Other variable costs …………………………………….

64 c

64

64

64

Fixed costs ………………………………………………..

840

d

e

Per unit cost ……………………………………………….

Cost plus 15% ……………………………………………

If fixed costs are not differential and South has no alternative uses of the excess

1-40. (20 Min.) Cost Data for Managerial Purposes: Campus Package Delivery.

a.

b. The decision to expand and offer the express service results in differential profits of

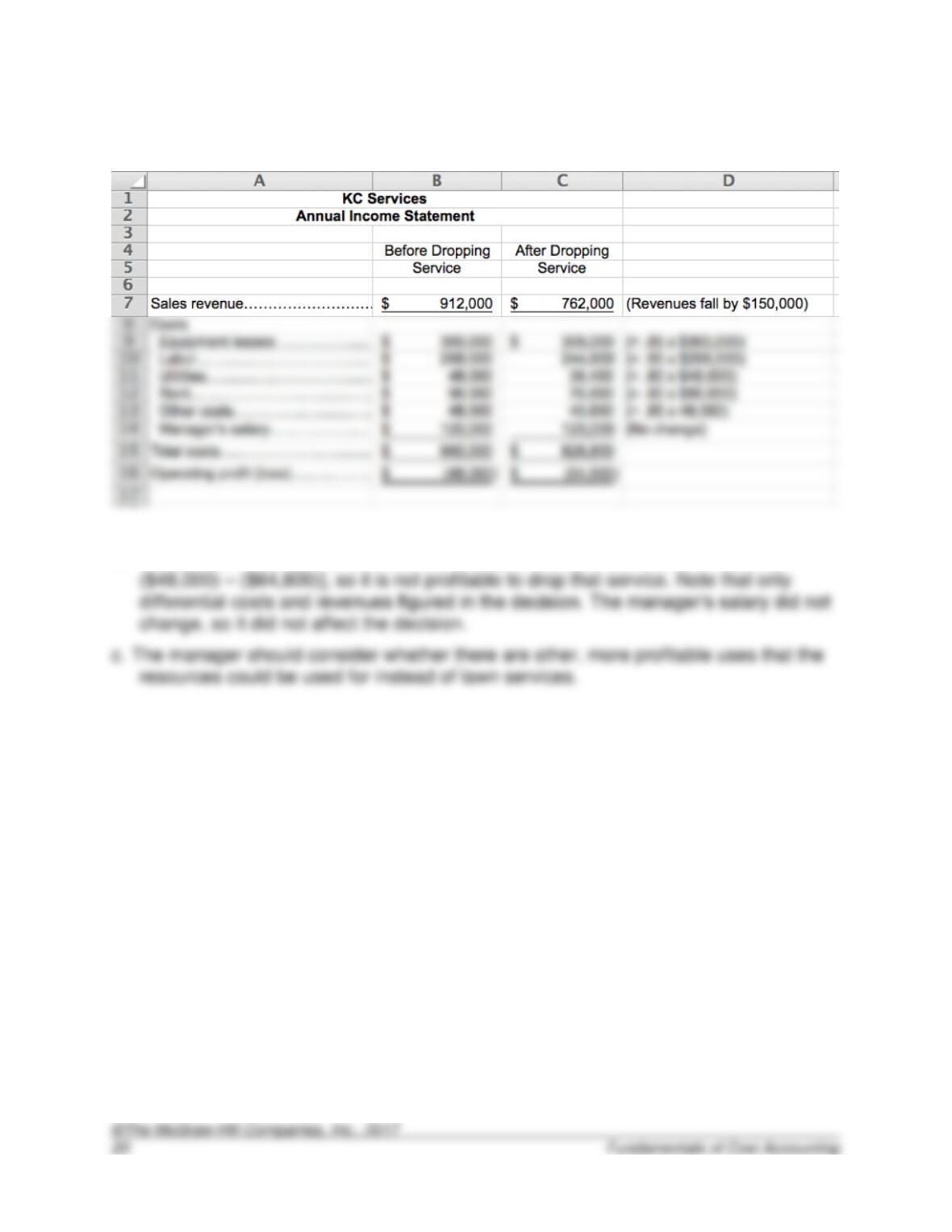

1-41. (20 Min.) Cost Data for Managerial Purposes: KC Services.

a.

b. The decision to drop the lawn service results in a differential loss of $16,800 [=

1-42. (20 Min.) Cost Data for Managerial Purposes: B-You

a. The following differential costs would be incurred:

b. Since acceptance of the contract would result in a decrease of operating profits by

1-43. (20 Min.) Cost Data for Managerial Purposes: Tom’s Tax Services.

a. The following differential costs would be incurred:

b. Since the addition of the customer would result in an increase of operating profits by

1-44. (20 Min.) Cost Data for Managerial Purposes––Budgeting

a.

b. The three items that we would investigate would be (a) utilities; (b) chocolate; and,

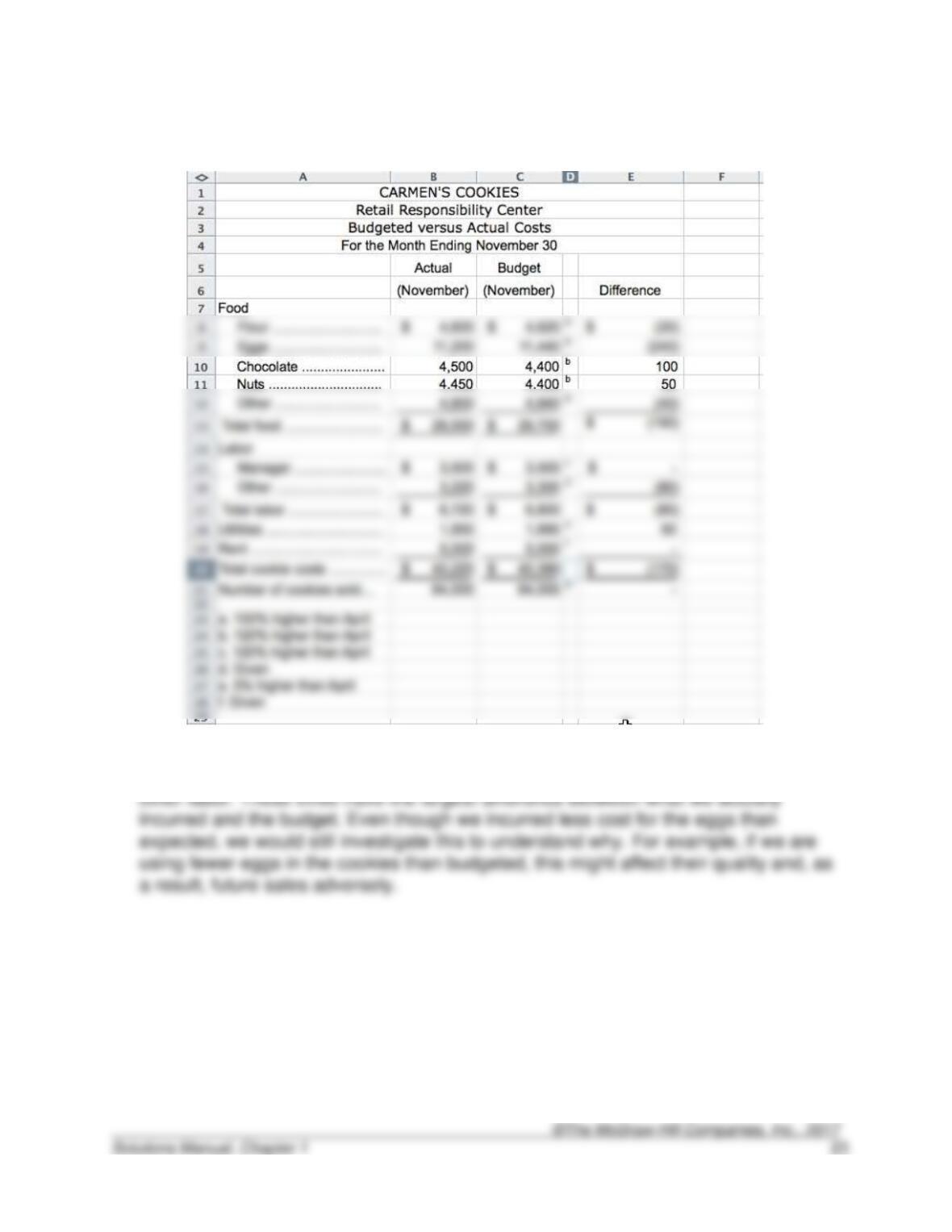

1-45. (20 Min.) Cost Data for Managerial Purposes––Budgeting

a.

b. The three items that we would investigate would be (a) eggs; (b) chocolate; and, (c)

1-46. (20 Min.) Cost Data for Managerial Purposes––Finding Unknowns:Quince

Products.

Solutions to Integrative Cases

1-47. (20 Min.) Identifying Unethical Action – Appendix

a. We recommend that Accountant B be retained to help Quince Products with their

1-48. (20 Min.) Cost Data for Managerial Purposes––Finding Unknowns

1-49. (20 Min.) Identifying Unethical Actions (Appendix)

1-50. (20 Min.) Responsibility for Unethical Action

b. People in this situation should contact a personal attorney (not the company

attorney) for advice. The next step would normally be to contact the most trustworthy