PROBLEM 1-6

Total consideration for Sylvester:

Cash ………………………………………………………………………………. $580,000

Less fair value of net assets acquired:

Notes receivable ……………………………………………………………… $ 24,000

Payroll and benefit-related liabilities—Current ……………………… (12,500)

Debt maturing in one year …………………………………………………. (10,000)

Long-term debt ………………………………………………………………… (248,000)

Payroll and benefit-related liabilities—Long-Term ………………… (156,000)

Value of net identifiable assets acquired ………………………… 507,500

Patents …………………………………………………………………………… 20,000

Trade Names ………………………………………………………………….. 15,000

Goodwill …………………………………………………………………………. 72,500

Accounts Payable ………………………………………………………. 45,000

Payroll and Benefit-Related Liabilities—Current ……………… 12,500

1–19 Ch. 1—Problems

PROBLEM 1-7

(1) Total consideration for Sambo:

Cash …………………………………………………………………………. $225,000

Stock issued (15,000 shares × $20) ………………………………. 300,000

Contingent liability ($50,000 × 60%) ……………………………… 30,000

Total consideration ………………………………………………… $555,000

Accounts payable ……………………………………………………….. (63,000)

Taxes payable ……………………………………………………………. (15,000)

Interest payable ………………………………………………………….. (3,000)

Bonds payable …………………………………………………………… (220,000)

Value of net identifiable assets acquired …………………… 487,000

Vehicles …………………………………………………………………….. 25,000

Franchise ………………………………………………………………….. 70,000

Goodwill ……………………………………………………………………. 68,000

Accounts Payable ………………………………………………….. 63,000

Taxes Payable ………………………………………………………. 15,000

Problem 1-7, Concluded

(2) Revised estimate of contingent payment ($50,000 × 90%) …… $45,000

Original estimate ($50,000 × 60%) ……………………………………. 30,000

PROBLEM 1-8

Total consideration for Heinrich:

Cash ………………………………………………………………………………. $150,000

Less fair value of net assets acquired:

Accounts receivable …………………………………………………………. $ 90,000

Inventory ………………………………………………………………………… 30,000

Other current assets …………………………………………………………. 8,000

Equipment ………………………………………………………………………. 80,000

Vehicles………………………………………………………………………….. 50,000

PROBLEM 1-9

(1) Reported Income for 2015

Combined Income Statement

For the Period Ending December 31, 2015

Sales revenue ………………………………………………………………… $620,000

Cost of goods sold ………………………………………………………….. 223,000

Gross profit ……………………………………………………………………. $397,000

Selling expense ……………………………………………………………… $140,000

Administrative expenses ………………………………………………….. 172,500

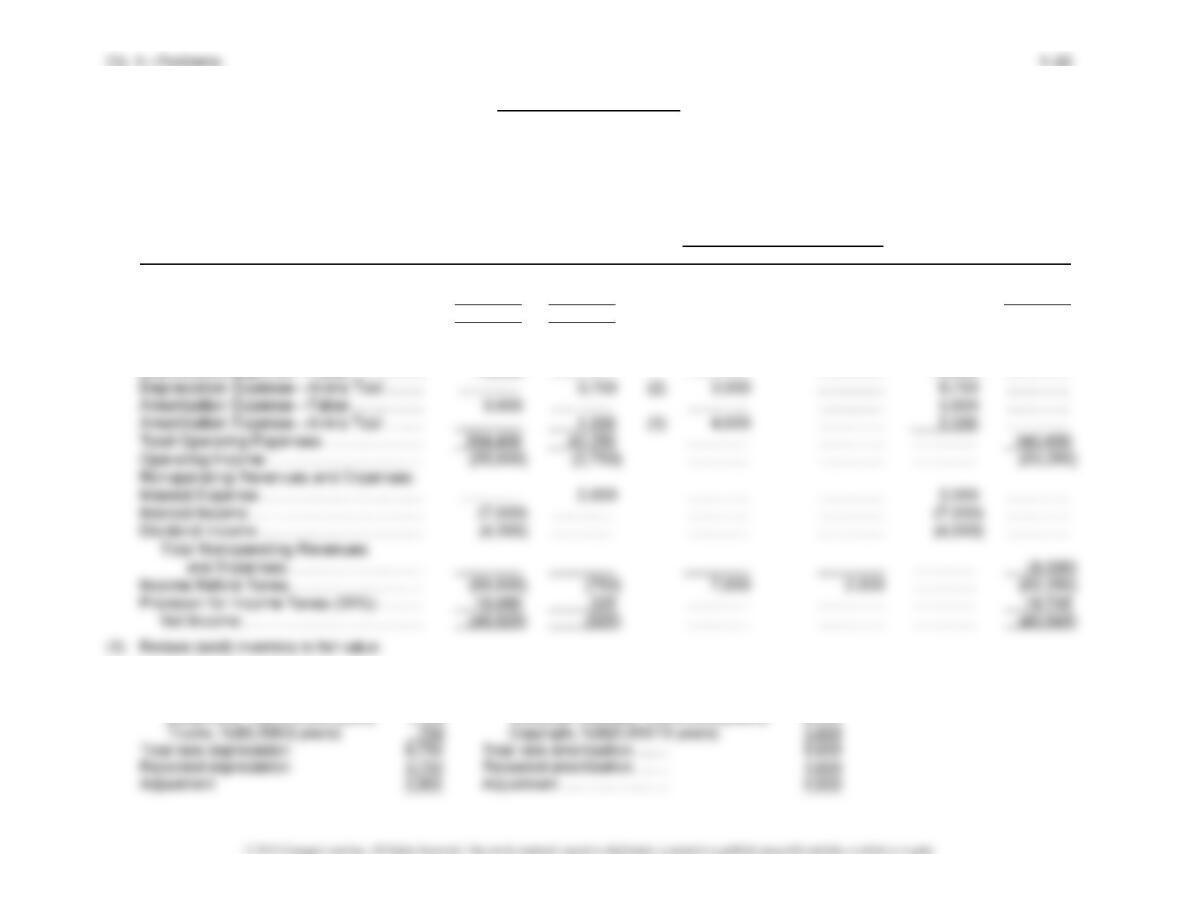

Problem 1-9, Continued

Name of Acquiring Company: Faber Enterprises

Name of Acquired Company: Ann’s Tool Company

Income Statement

For the Year Ending December 31, 2015

(Tax rate expressed as 0.3 for 30%)

Faber 6 Mo. Ann’s Adjustments Combined

Income Statement Accounts Enterprises Tool Co. Debit Credit Income Statement

Sales Revenue …………………………………. (550,000) (70,000) ………….. …………… ………….. (620,000)

Cost of Goods Sold …………………………… 200,000 25,000 ………….. (1) 2,000 ………….. 223,000

Gross Profit ………………………………………. (350,000) (45,000) ………….. …………… ………….. (397,000)

Selling Expenses ………………………………. 125,000 15,000 ………….. …………… 140,000 …………..

Administrative Expenses ……………………. 150,000 22,500 ………….. …………… 172,500 …………..

Depreciation Expense—Faber …………….. 13,800 ………….. ………….. …………… 13,800 …………..

(2) New depreciation: (3) New amortization:

Building, 1/2($125,000/25 years) 2,500 Patent, (1/2($18,000/6 years) 1,500

Equipment, ½($56,000/8 years) 3,500 Computer software, ½($10,000/2years) 2,500

1–23 Ch. 1—Problems

Problem 1-9, Concluded

(2) Pro forma disclosure for 2015 as if acquisition occurred at the start of the year:

Sales revenue ($550,000 + $140,000) ………………………………………………. $ 690,000

Net income…………………………………………………………………………………….. $ 39,270

Calculation of net income:

Reported net incomes before tax ($66,600 + $1,500) …………………….. $ 68,100

*($2,500 + $3,500 + $750 + $1,500 + $2,500 + $1,000) = $11,750 × 2 = $23,500

PROBLEM 1-10

Part A1

Total consideration for Iris:

Common stock (10,000 shares × $27) ………………………………… $270,000

Less fair value of net assets acquired:

Accounts receivable …………………………………………………………. $ 15,000

Inventory ………………………………………………………………………… 40,000

Prepaid expenses ……………………………………………………………. 12,000

Investments …………………………………………………………………….. 33,000

Land ………………………………………………………………………………. 40,000

Problem 1-10, Continued

Journal Entry:

Accounts Receivable ………………………………………………………… 15,000

Inventory ………………………………………………………………………… 40,000

Prepaid Expenses ……………………………………………………………. 12,000

Investments …………………………………………………………………….. 33,000

Land ………………………………………………………………………………. 40,000

Building ………………………………………………………………………….. 85,000

1–25 Ch. 1—Problems

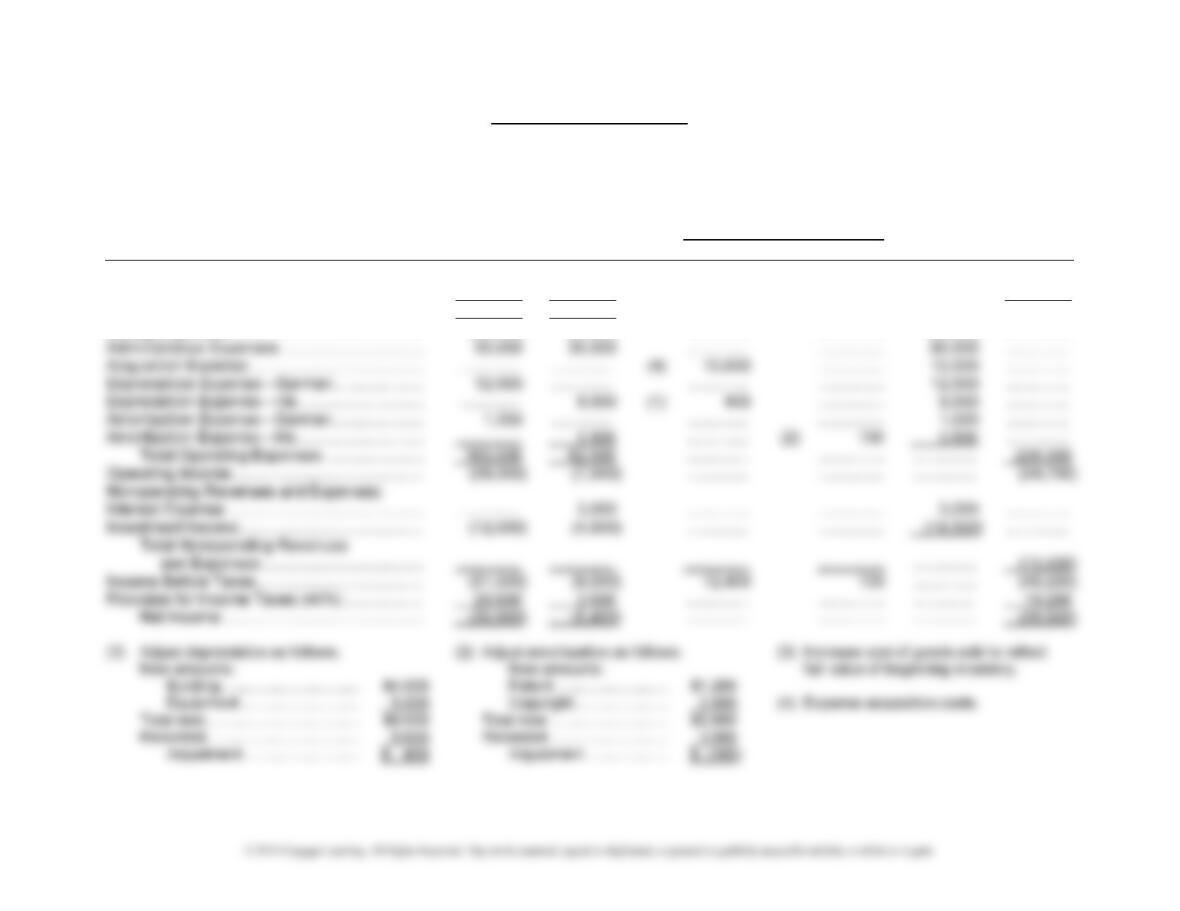

Problem 1-10, Concluded

Worksheet for

Pro Forma Income Statement

For the Year Ending December 31, 2016

(Tax rate expressed as 0.4 for 40%)

Garman Iris Adjustments Pro Forma Combined

Income Statement Accounts International Company Debit Credit Income Statement

Sales Revenue ………………………………………… (350,000) (125,000) ………….. …………… ………….. (475,000)

Cost of Goods Sold ………………………………….. 147,000 55,000 (3) 2,000 …………… ………….. 204,000

Gross Profit ………………………………………. (203,000) (70,000) ………….. …………… ………….. (271,000)

Selling Expenses ……………………………………… 100,000 20,000 ………….. …………… 120,000 …………..

PROBLEM 1-11

Current Assets ……………………………………………………………………… 100,000

Assets Under Operating Leases (fair) ………………………………………. 580,000

Net Investment in Direct Financing Leases* ……………………………… 710,605

Leased Equipment Under Capital Lease (fair) …………………………… 60,000

PROBLEM 1-12

Current Assets ……………………………………………………………………… 150,000

Equipment ($150,000 increase) ………………………………………………. 350,000

Land and Buildings ……………………………………………………………….. 250,000

Deferred Tax Asset ……………………………………………………………….. 54,000

Goodwill* ……………………………………………………………………………… 91,000

Bonds Payable ………………………………………………………………… 200,000

Deferred Tax Liability ………………………………………………………. 45,000

Common Stock ($10 par) ………………………………………………….. 100,000

Ch. 1—Problems 1–28

PROBLEM 1-13

(1) Total consideration for Weber:

Common stock (20,000 shares × $60 + $20,000 contingency) $1,220,000

Less fair value of net assets acquired:

Cash …………………………………………………………………………. $ 30,000

Accounts receivable ……………………………………………………. 60,000

Investment in marketable securities ………………………………. 150,000

Land …………………………………………………………………………. 450,000

Buildings ……………………………………………………………………. 450,000

Dr. = Cr. Check Totals 1,740,000 1,740,000

(2) Entry to record contingent consideration:

Paid-in capital, contingent consideration ……………………………. 20,000

1–29 Ch. 1—Problems

APPENDIX PROBLEM

PROBLEM 1A-1

(1) Bonds:

Present value of interest payments for 5 years at 8%,

$27,000 × 3.9927 ………………………………………………………………………. $107,803

Present value of principal due in 5 years at 8%,

(2) Cash and Receivables …………………………………………………….. 150,000

Inventory ……………………………………………………………………….. 200,000

Land ……………………………………………………………………………… 100,000

Ch. 1—Cases 1–30

CASES

CASE 1-1

Part A

Confirmation:

Building:

Payment ………………………………………………………………………………. $80,000

Case 1-1, Continued

Part B

(1) Discounted cash flows:

Salvage/

Period Operating Capital (Capital Expenditures) Total

1 150,000 150,000

2 165,000 165,000

3 181,500 181,500

4 199,650 199,650

5 219,615 (100,000) 119,615

6 219,615 219,615

(2) Fair value comparison:

(3) Entry to record acquisition:

Cash Equivalents ……………………………………………………………. 80,000

Inventory ……………………………………………………………………….. 150,000

Accounts Receivable ………………………………………………………. 180,000

Case 1-1, Concluded

Part C

Impairment test:

Implied fair value of Frontier …………………………………………………………. $1,200,000

Book value, including goodwill ……………………………………………………… 1,300,000

Book value exceeds implied fair value; goodwill is impaired.

Impairment adjustment:

Implied fair value of Frontier …………………………………………………………. $1,200,000

CASE 1-2

1. The acquisition would be qualified as horizontal.

2. The total price paid and its assignment are as follows:

Cash (79.2 million shares × $30) ……………………………. $2,376,000,000

Stock issued (59 million shares × $32.25) ……………….. 1,902,750,000

Total consideration ………………………………………………. $4,278,750,000

3. Journal Entry:

Cash and Cash Equivalents ………………………………………….. 105,000,000

Receivables ………………………………………………………………… 141,000,000

Capitalized Film Costs ………………………………………………….. 269,000,000