CHAPTER 1

SOLUTIONS TO EXERCISES—SET B

EXERCISE 1-1B

(a) Factory utilities …………………………………………………………….. $ 18,600

Depreciation on factory equipment ………………………………… 14,445

Indirect factory labor …………………………………………………….. 48,900

Indirect materials ………………………………………………………….. 80,800

EXERCISE 1-2B

(a) Delivery service (product) costs:

Indirect materials ……………………………………………………

$ 8,775

Depreciation on delivery equipment ………………………..

11,200

Dispatcher’s salary …………………………..…………………….

7,000

Gas and oil for delivery trucks…………………………………

2,200

Delivery equipment repairs ……………………………………..

300

Total ………………………………………………………………

EXERCISE 1-2B (Continued)

(b) Period costs:

Property taxes on office building …………………………….

$ 3,625

CEO’s salary ………………………………………………………….

22,000

EXERCISE 1-3B

(a) Work-in-process, 1/1 …………………………. $ 17,500

Direct materials used ………………………… $135,000

Direct labor ………………………………………. 110,000

Manufacturing overhead

(b) Finished goods, 1/1 …………………………... $ 60,500

Cost of goods manufactured …………….. 352,500

EXERCISE 1-4B

Total raw materials available for use:

Direct materials used ……………………………………………….. $190,000

Add: Raw materials inventory (12/31) ……………………….. 17,500

Total raw materials available for use …………………………. $207,500

Advertising ……………………………………………………………

Office supplies……………………………………………………….

Office utilities ………………………………………………………..

Repairs on office equipment …………………………………..

745

Total ……………………………………………………………..

EXERCISE 1-4B (Continued)

Total cost of work in process:

Cost of goods manufactured ……………………………………….. $550,000

Total manufacturing costs:

Total cost of work in process ………………………………………. $617,000

Direct labor:

Total manufacturing costs …………………………………………… $409,500

Less: Total overhead …………………………………………………. 119,000

EXERCISE 1-5B

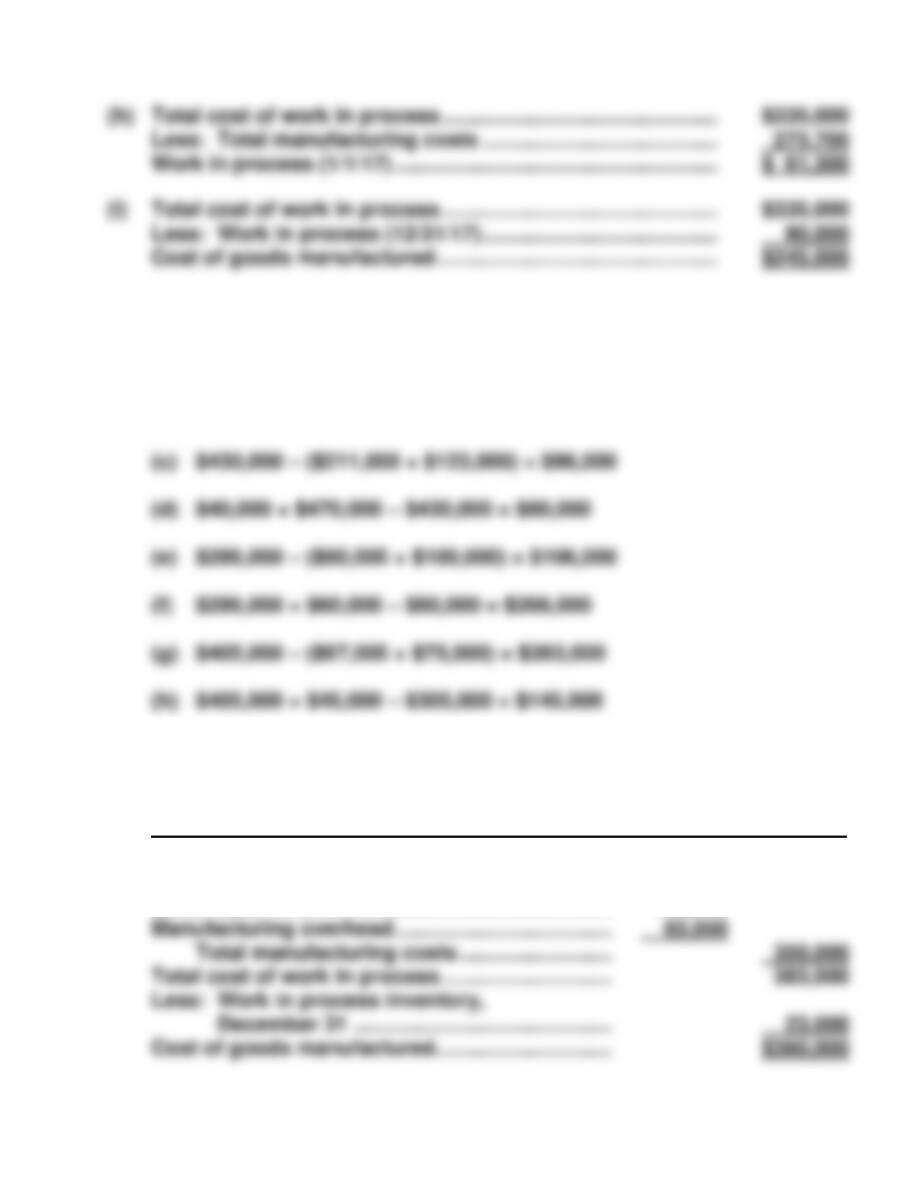

A + $63,200 + $46,500 = $175,650 $256,030 – $11,000 = F

A = $65,950 F = $245,030

EXERCISE 1-5B (Continued)

Additional explanation to EXERCISE 1-5B solution:

Case A

(a) Total manufacturing costs …………………………………………… $175,650

Less: Manufacturing overhead …………………………………….. 46,500

Direct labor ……………………………………………………….. 63,200

Direct materials used …………………………………………………… $ 65,950

Case B

(d) Direct materials used …………………………………………………… $ 72,330

Direct labor …………………………..…………………………………….. 86,500

Manufacturing overhead ……………………………………………… 81,600

Total manufacturing costs …………………………………………… $240,430

Case C

(g) Total manufacturing costs …………………………..………………. $273,700

Less: Manufacturing overhead ……………………………………. 102,000

Direct materials used ………………………………………… 137,060

Direct labor …………………………..…………………………………….. $ 34,640

EXERCISE 1-5B (Continued)

EXERCISE 1-6B

(a) (a) $127,000 + $140,000 + $83,000 = $350,000

(b) $350,000 + $33,000 – $360,000 = $23,000

(b) HEINTZ COMPANY

Cost of Goods Manufactured Schedule

For the Year Ended December 31, 2017

Work in process, January 1 ………………………….. $ 33,000

Direct materials …………………………………………… $127,000

Direct labor …………………………………………………. 140,000

EXERCISE 1-7B

(a) TART CORPORATION

Cost of Goods Manufactured Schedule

For the Month Ended June 30, 2017

Work in process, June 1 ……………………….. $ 4,800

Direct materials used ……………………………. $25,000

Direct labor …………………………..……………… 30,000

Manufacturing overhead

Indirect labor ………………………………… $4,000

Factory manager’s salary ………………. 4,500

(b) TART CORPORATION

Income Statement (Partial)

For the Month Ended June 30, 2017

Net sales ………………………………………………………. $85,100

Cost of goods sold

Finished goods inventory, June 1 ……………. $ 5,000

EXERCISE 1-8B

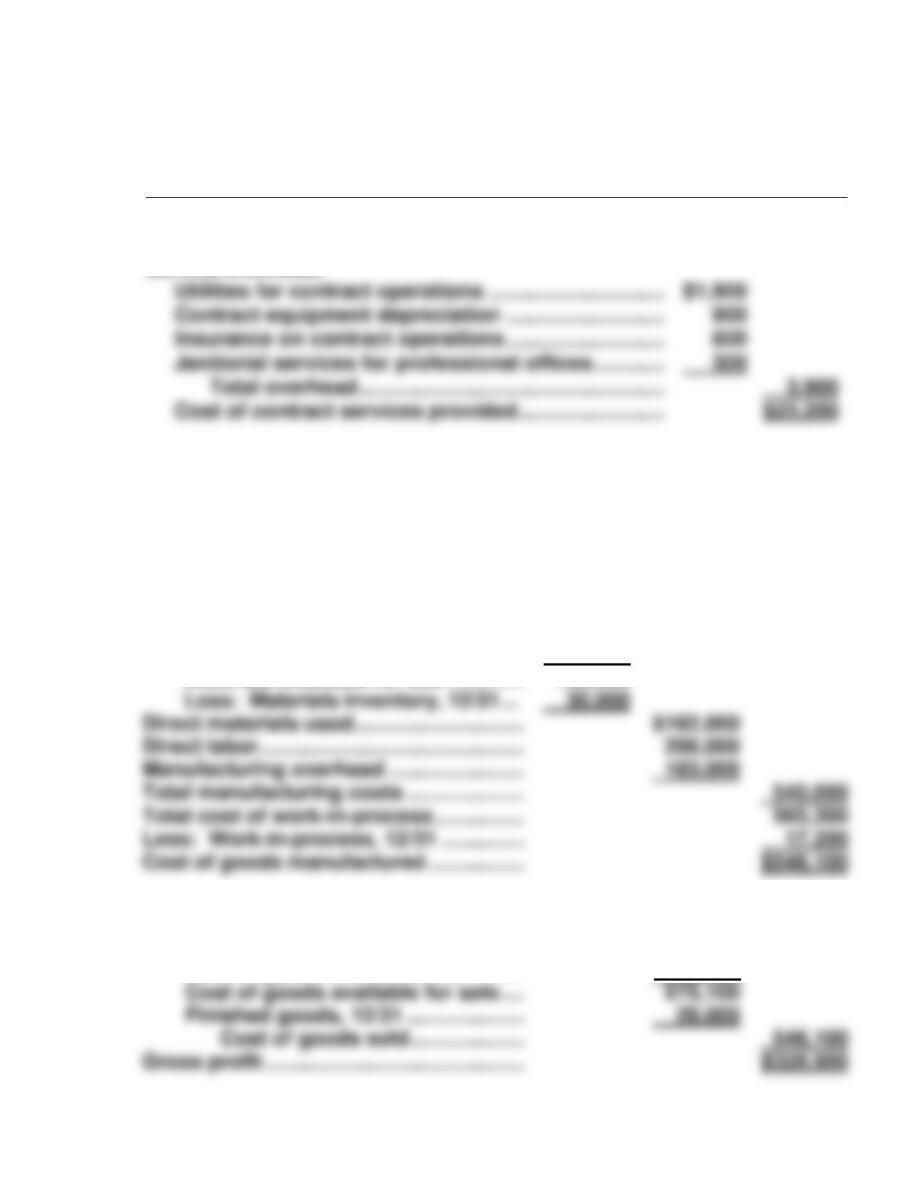

(a) PARE, ASH, AND TOCY

Schedule of Cost of Contract Services Provided

For the Month Ended August 31, 2017

Supplies used (direct materials) …………………………….

$ 3,700

Salaries of professionals (direct labor) …………………..

15,600

Service overhead:

(b) The costs not included in the cost of contract services provided would all

be classified as period costs. As such, they would be reported on the

income statement under administrative expenses.

EXERCISE 1-9B

(a) Work-in-process, 1/1 ………………………… $ 20,300

Direct materials

Materials inventory, 1/1 ……………… $ 22,000

Materials purchased ………………….. 170,000

Materials available for use …………. 192,000

(b) Sales revenue………………………………….. $875,000

Cost of goods sold

Finished goods, 1/1 …………………… $ 27,000

Cost of goods manufactured …….. 548,100

Utilities for contract operations …………………………

Contract equipment depreciation ………………………

Insurance on contract operations ………………………

Janitorial services for professional offices …………

Total overhead …………………………………………….

EXERCISE 1-9B (Continued)

(c) Current assets

Inventories

Finished goods ……………………………………….. $29,000

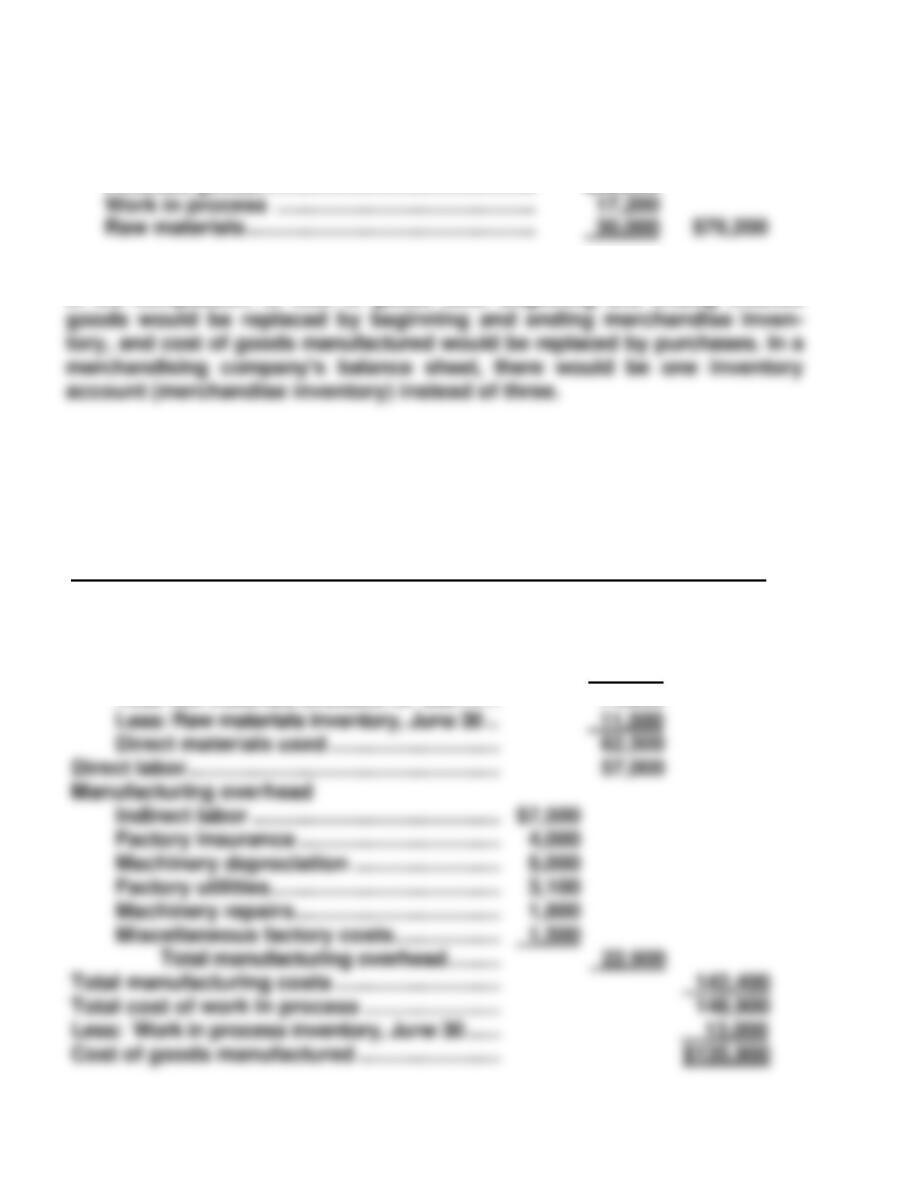

(d) In a merchandising company’s income statement, the only difference would be

in the computation of cost of goods sold. Beginning and ending finished

EXERCISE 1-10B

(a) MARKUS MANUFACTURING

Cost of Goods Manufactured Schedule

For the Month Ended June 30, 2017

Work in process inventory, June 1 …………… $ 6,500

Direct materials

Raw materials inventory, June 1 ……….. $10,000

Raw materials purchases …………………. 64,000

Total raw materials available for use ……. 74,000

EXERCISE 1-10B (Continued)

(b) MARKUS MANUFACTURING

(Partial) Balance Sheet

June 30, 2017

Current assets

Inventories

Finished goods ………………………………….. $ 6,000

EXERCISE 1-11B

(a) Raw Materials account: (5,200 – 4,650) X $8 = $4,400

Work in Process account: (4,550 X 10%) X $8 = $3,640

(b) To: Chief Accountant

From: Student

Subject: Statement Presentation of Accounts

Two accounts will appear in the income statement. Cost of Goods Sold

will be deducted from net sales in determining gross profit. Selling ex–

penses will be shown under operating expenses and will be deducted

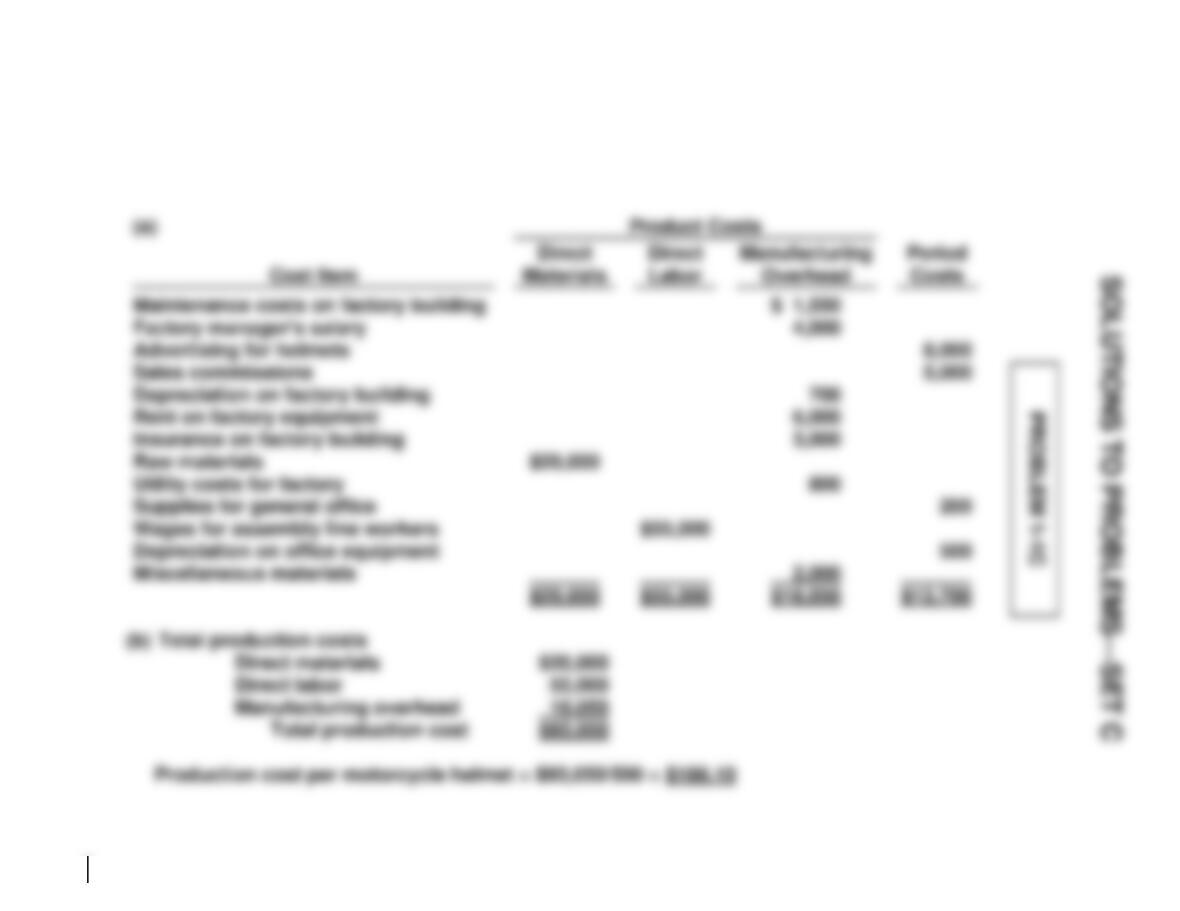

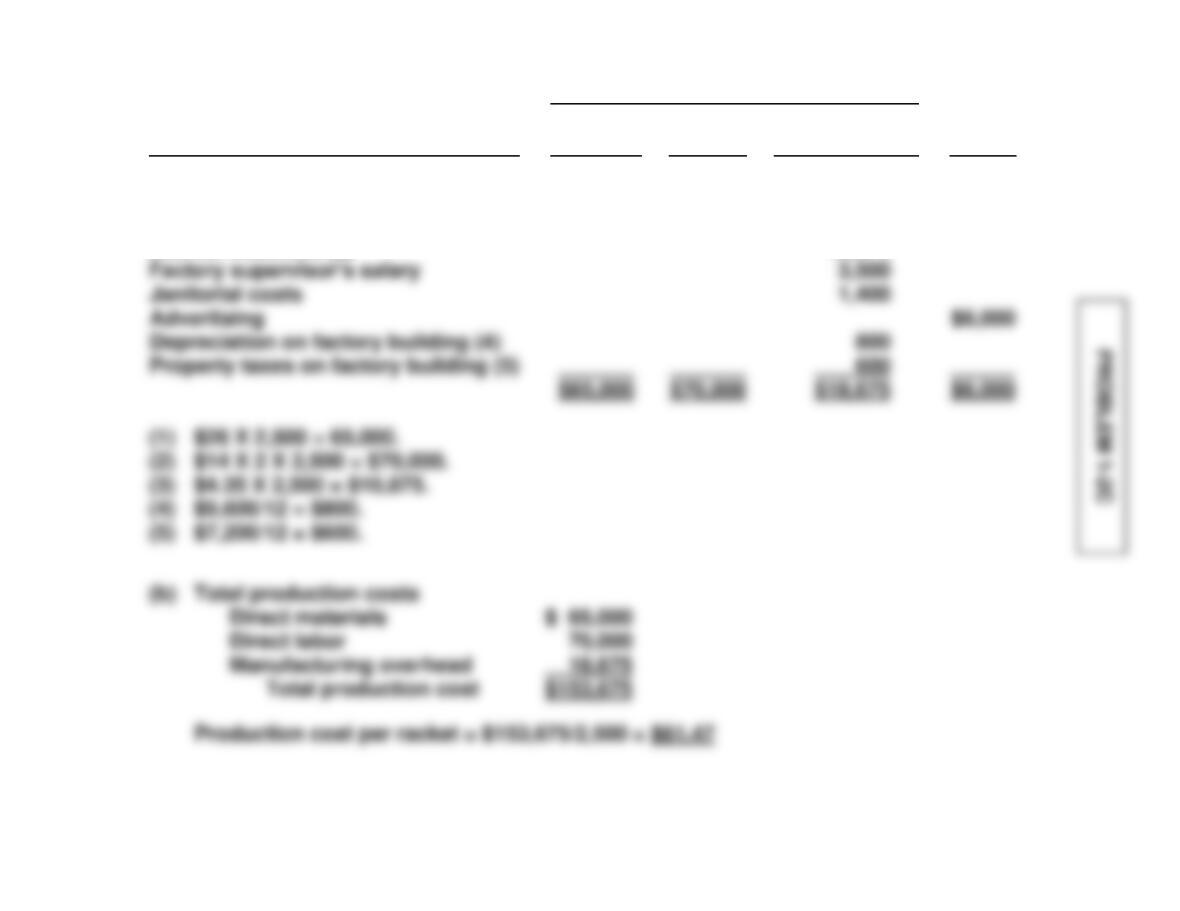

(a)

Product Costs

Cost Item

Direct

Materials

Direct

Labor

Manufacturing

Overhead

Period

Costs

Raw materials (1)

Wages for workers (2)

Rent on equipment

Indirect materials (3)

$65,000

$70,000

$ 1,500

10,875

Property taxes on factory building (5)

(4) $9,600/12 = $800.

(5) $7,200/12 = $600.

Production cost per racket = $153,675/2,500 = $61.47

PROBLEM 1-3C

(a) Case A

A = $6,025 + $3,000 + $6,000 = $15,025

$15,025 + $1,000 – B = $14,600

B = $15,025 + $1,000 – $14,600 = $1,425

Case B

G + $3,800 + $5,000 = $16,000

G = $16,000 – $3,800 – $5,000 = $7,200

$16,000 + H – $2,000 = $20,000

H = $20,000 + $2,000 – $16,000 = $6,000

PROBLEM 1-3C (Continued)

(b) CASE A

Cost of Goods Manufactured Schedule

Work in process, beginning ………………………….. $ 1,000

Direct materials ……………………………………………. $6,025

Direct labor ………………………………………………….. 3,000

(c) CASE A

Income Statement

Sales revenue ………………………………………………. $22,500

Less: Sales discounts ………………………………….. 1,770

Net sales ……………………………………………………… $20,730

Cost of goods sold

Finished goods inventory, beginning ……… $ 3,700

CASE A

(Partial) Balance Sheet

Current assets

Cash ……………………………………………………… $ 4,200

Receivables (net) …………………………………… 11,000

Inventories

PROBLEM 1-4C

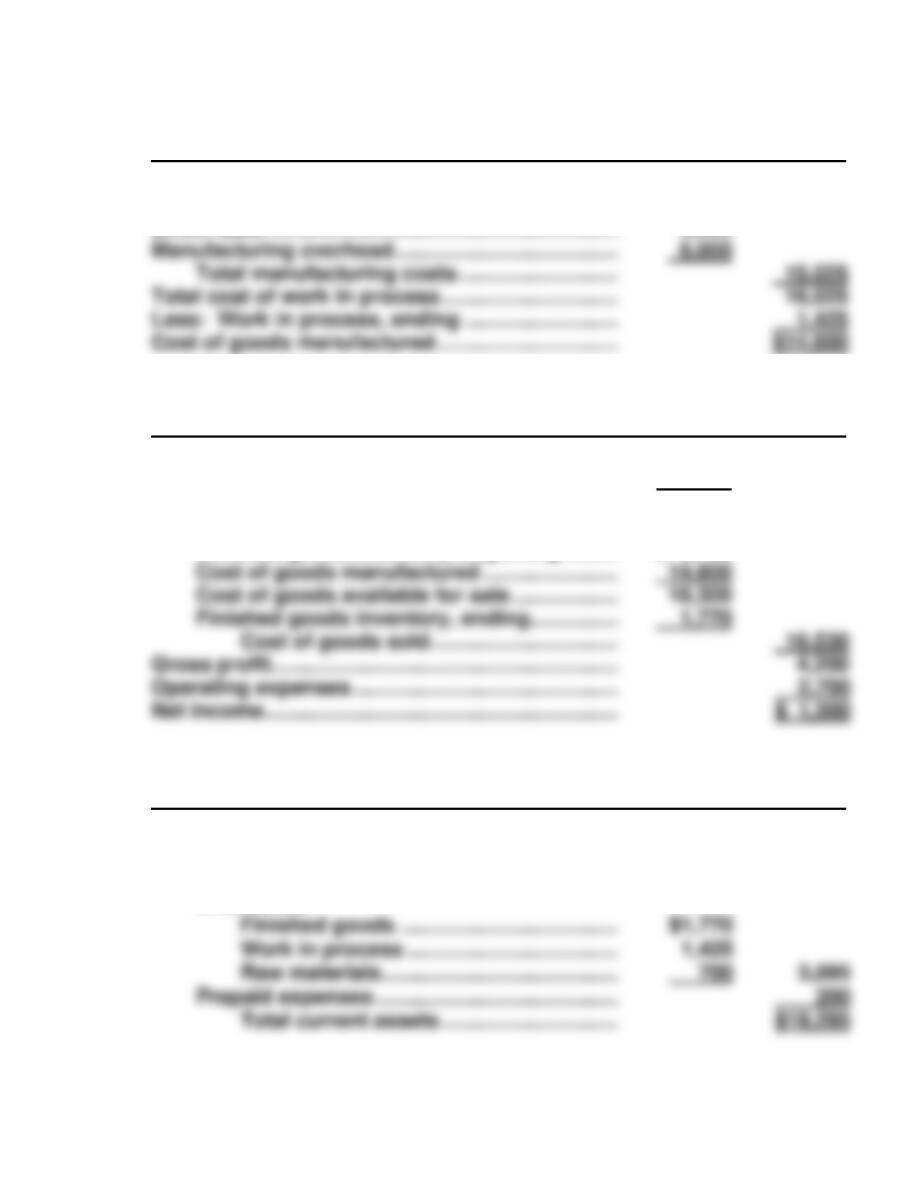

(a) FALCON MANUFACTURING COMPANY

Cost of Goods Manufactured Schedule

For the Year Ended December 31, 2017

Work in process inventory,

January 1 …………………………... $ 9,650

Direct materials

Raw materials inventory,

January 1 ……………………. $ 48,500

Manufacturing overhead

Plant manager’s salary ……. 42,000

Indirect labor ………………….. 18,100

Factory utilities ……………….. 12,900

Factory machinery

PROBLEM 1-4C (Continued)

(b) FALCON MANUFACTURING COMPANY

(Partial) Income Statement

For the Year Ended December 31, 2017

Sales revenues

Sales revenue …………………………………….. $477,000

Less: Sales discounts ………………………… 2,500

Net sales …………………………………………….. $474,500

(c) FALCON MANUFACTURING COMPANY

(Partial) Balance Sheet

December 31, 2017

Assets

Current assets

Cash …………………………………………………… $ 33,500

Accounts receivable ………………………….... 27,000

Inventories

PROBLEM 1-5C

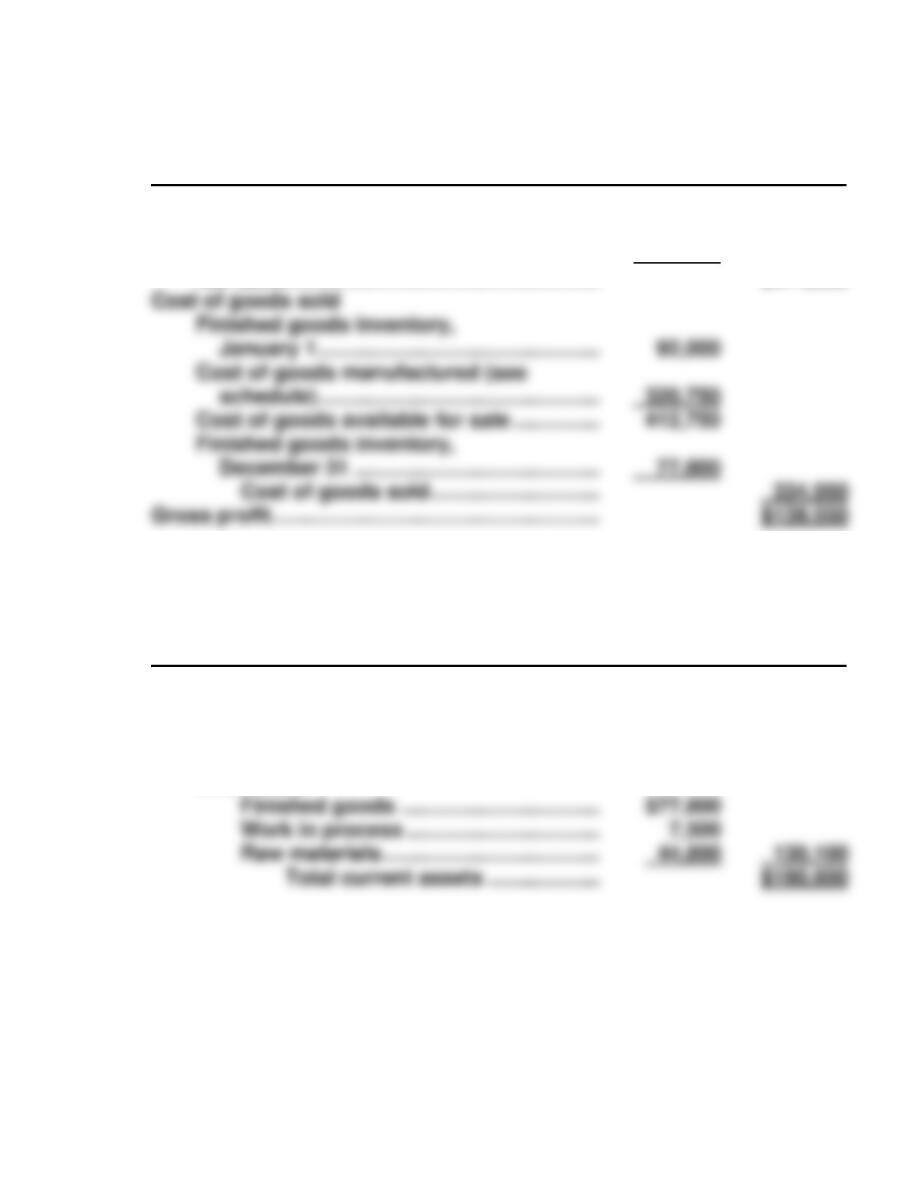

(a) FATHOM COMPANY

Cost of Goods Manufactured Schedule

For the Month Ended August 31, 2017

Work in process, August 1 ……………… $ 18,975

Direct materials

Raw materials inventory,

August 1 ……………………………… $ 19,500

Manufacturing overhead

Factory facility rent …………………. $ 60,000

Depreciation on factory

equipment …………………………... 35,000

Indirect labor ………………………….. 15,000

PROBLEM 1-5C (Continued)

(b) FATHOM COMPANY

Income Statement

For the Month Ended August 31, 2017

Sales (revenue) …………………………………………… $675,000

Cost of goods sold

Finished goods inventory, August 1 ……… $ 40,000

Cost of goods manufactured ………………… 475,375