1. The receiving report should be reconciled to the initial purchase order and the vendor’s invoice

b

efore recording or paying for inventory purchases. This procedure will verify that the inventory

3. No, they are not techniques for determining physical quantities. The terms refer to cost flow

9. Bibbins Company. Since the merchandise was shipped FOB shipping point, title passed to

10. Manufacturer’s. The manufacturer retains title until the goods are sold. Thus, any unsold

CHAPTER 6

INVENTORIES

DISCUSSION QUESTIONS

6-1

p

CHAPTER 6 Inventories

PE 6–1A

PE 6–1B

a. First-in, first-out (FIFO)

PE 6–2A

a. Cost of merchandise sold (May 28):

PE 6–2B

a. Cost of merchandise sold (July 24):

PRACTICE EXERCISES

Gross Profit

February

Ending Inventory

February 28

June June 30

Gross Profit Ending Inventory

$60 ($110 – $50) $130 ($60 + $70)

6-2

CHAPTER 6 Inventories

PE 6–3A

a. Cost of merchandise sold (June 26):

PE 6–3B

a. Cost of merchandise sold (March 27):

PE 6–4A

a. Weighted average unit cost: $71.25

Inventory total cost after purchase on July 15:

PE 6–4B

a. Weighted average unit cost: $9.50

Inventory total cost after purchase on October 22:

PE 6–5A

a. First-in, first-out (FIFO) method: $3,726 = 23 units × $162

PE 6–5B

a. First-in, first-out (FIFO) method: $20,094 = (40 units × $357) + (17 units × $342)

PE 6–6A

Unit Unit

Inventory Cost Market Lower of

Commodity Quantity Price Price Cost Market C or M

PE 6–6B

Unit Unit

Inventory Cost Market Lower of

Commodity Quantity Price Price Cost Market C or M

JFW1 6,330 $10 $11 $ 63,300 $ 69,630 $ 63,300

Total

Total

6-4

CHAPTER 6 Inventories

PE 6–7A

Balance Sheet:

Merchandise inventory understated*…………………

PE 6–7B

Balance Sheet:

Merchandise inventory overstated*…………………

…

Current assets overstated……………………………

…

8,780

Overstatement (Understatement)

Amount of Misstatement

Amount of Misstatement

Overstatement (Understatement)

$ 8,780

$(4,450)

6-5

PE 6–8A

a.

Cost of merchandise sold

Inventories:

b.

Cost of merchandise sold

Average daily cost of

2014 2013

$1,452,500 $1,120,000

Inventory Turnover

Number of Days’ Sales

in Inventory 2014 2013

$1,452,500 $1,120,000

($1,452,500 ÷ $415,000) ($1,120,000 ÷ $350,000)

6-6

CHAPTER 6 Inventories

PE 6–8B

a.

Cost of merchandise sold

Inventories:

b.

Cost of merchandise sold

Average daily cost of

$4,001,500

$3,864,000

Inventory Turnover

Number of Days’ Sales

in Inventory 2014 2013

2014 2013

$3,864,000 $4,001,500

6-7

CHAPTER 6 Inventories

Ex. 6–1

Switching to a perpetual inventory system will strengthen Triple Creek Hardware’s

internal controls over inventory, since the store managers will be able to keep

Ex. 6–2

EXERCISES

6-8

CHAPTER 6 Inventories

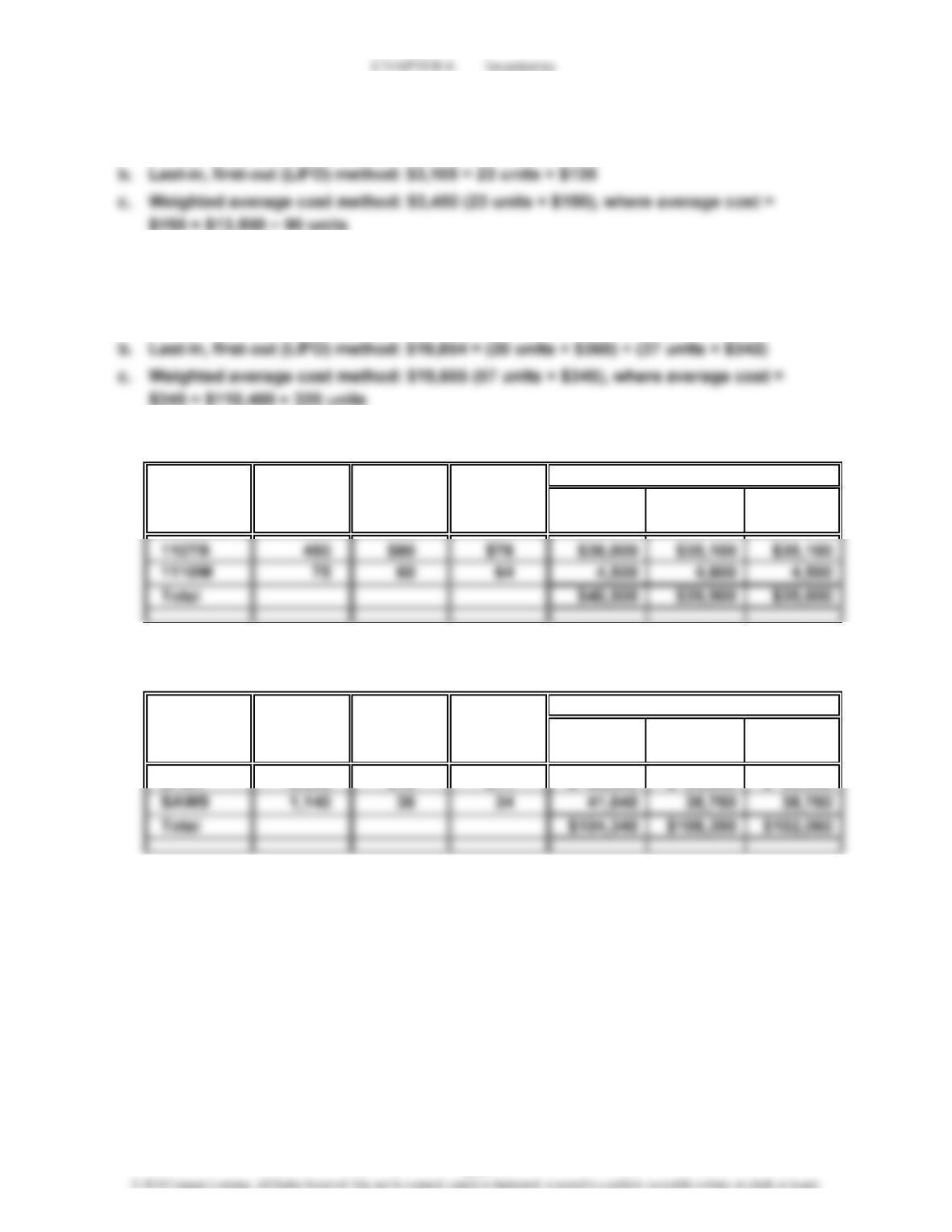

Ex. 6–3

a.

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

Apr. 1 120 39 4,680

Ex. 6–4

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

Apr. 1 120 39 4,680

6 90 39 3,510 30 39 1,170

Date

Portable DVD Players

Purchases Cost of Merchandise Sold Inventory

Date

Portable DVD Players

Purchases Cost of Merchandise Sold Inventory

6-9

CHAPTER 6 Inventories

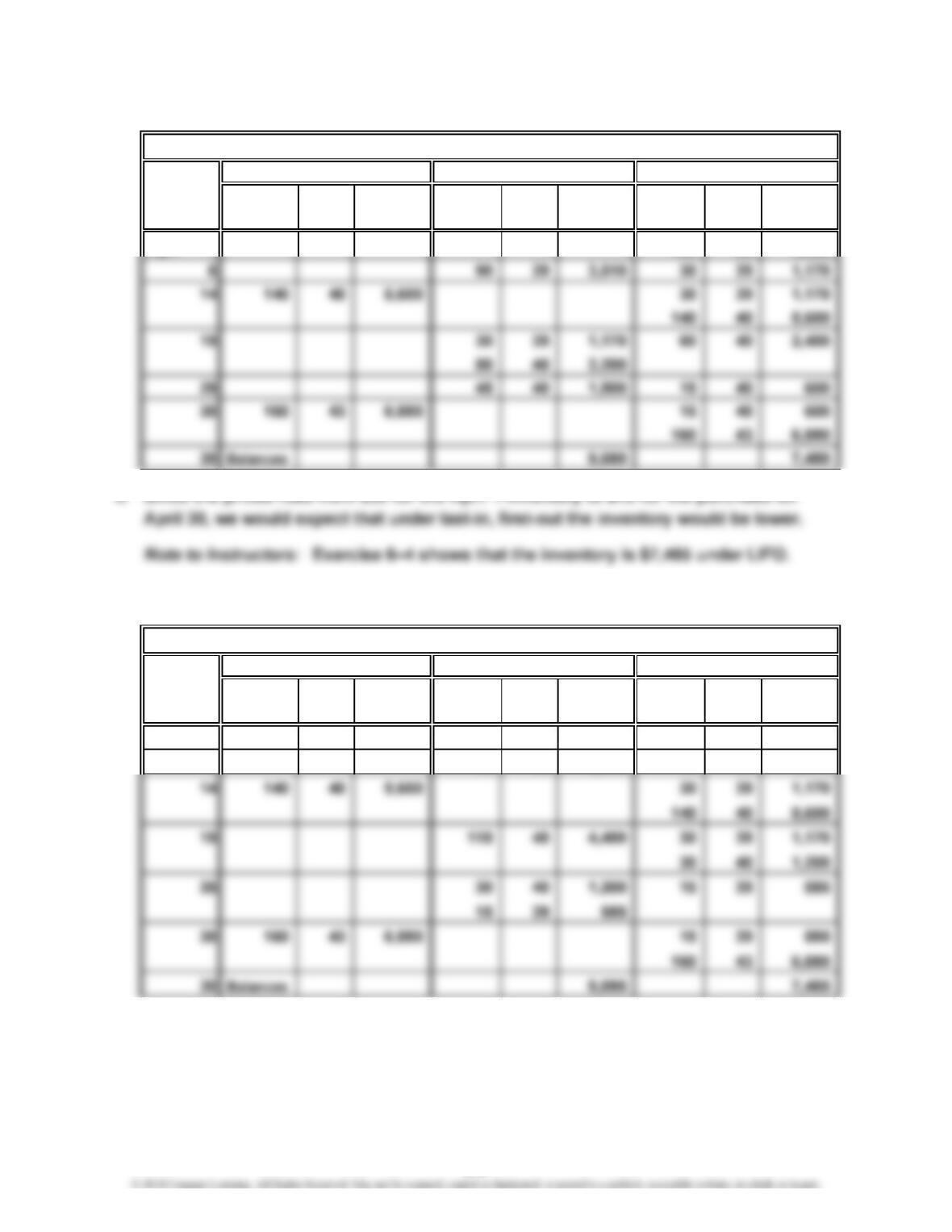

Ex. 6–5

a.

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

Aug. 1 775 44 34,100

10 360 45 16,200 775 44 34,100

b. Since the prices rose from $44 for the August 1 inventory to $48 for the purchase on

Ex. 6–6

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

Aug. 1 775 44 34,100

14 175 44 7,700

240 45 10,800 120 45 5,400

20 600 48 28,800 120 45 5,400

Date

Prepaid Cell Phones

Purchases Cost of Merchandise Sold Inventory

Date

Prepaid Cell Phones

Purchases Cost of Merchandise Sold Inventory

6-10

CHAPTER 6 Inventories

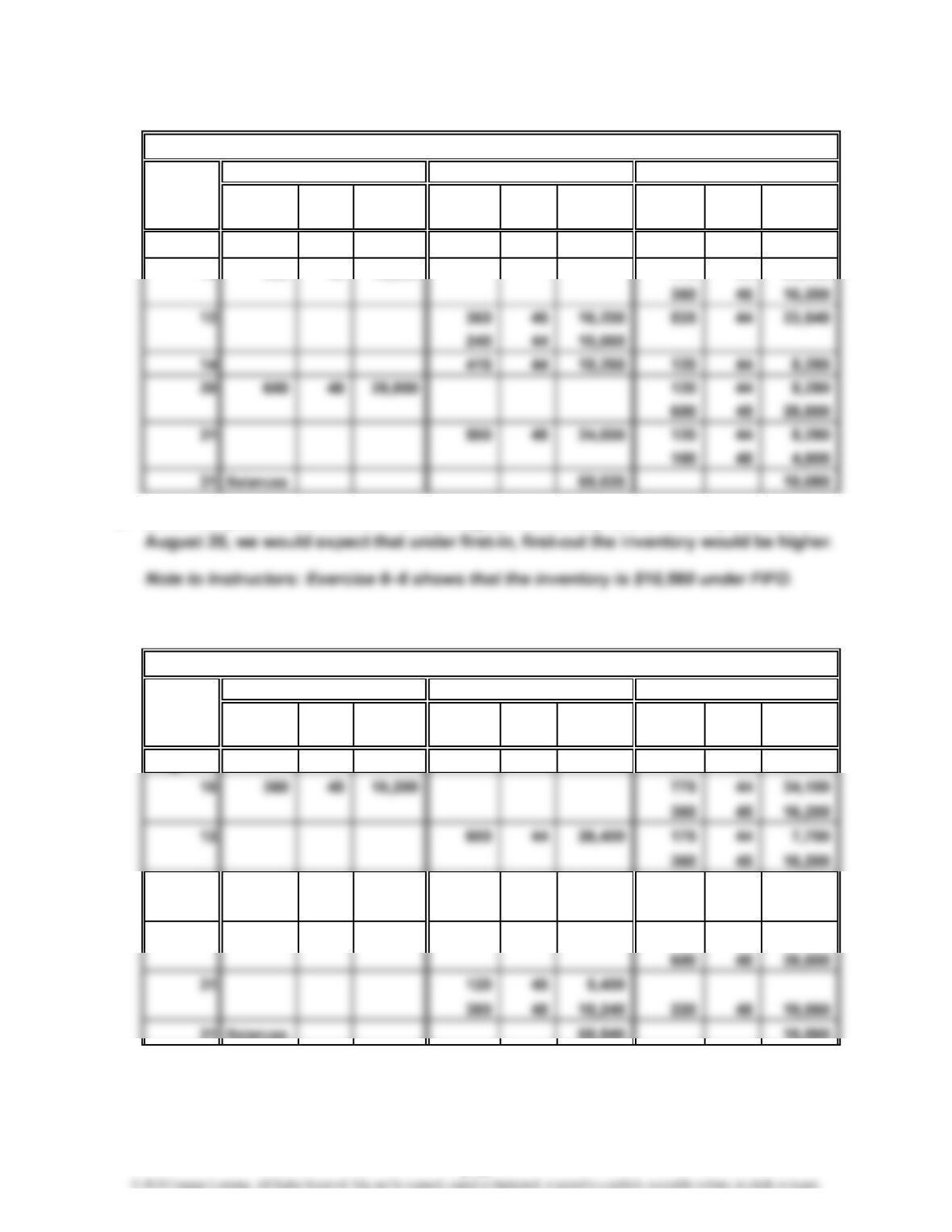

Ex. 6–7

a. $22,880 ($440 × 52 units)

Ex. 6–8

Cost of Merchandise Sold

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

Jan. 1 1,000 150.00 150,000

Ex. 6–9

Cost of Merchandise Sold

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

Jan. 1 8,000 40.00 320,000

Date

Inventory

Inventory

Date

Purchases

Purchases

6-11

CHAPTER 6 Inventories

Ex. 6–10

Cost of Merchandise Sold

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

Jan. 1 8,000 40.00 320,000

Ex. 6–11

Inventory

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

Jan. 1 8,000 40.00 320,000

Apr. 19 5,000 40.00 200,000 3,000 40.00 120,000

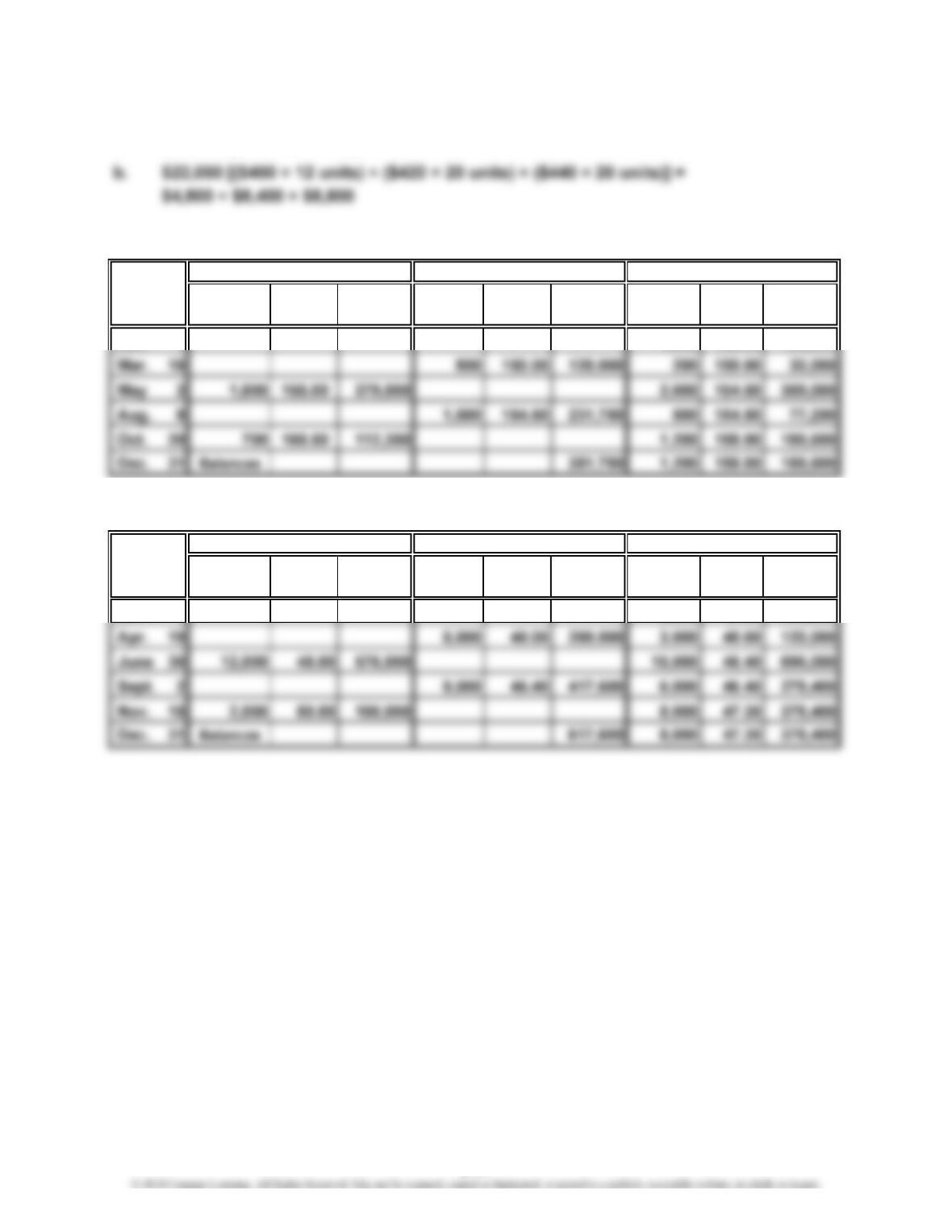

Ex. 6–12

Cost of merchandise available for sale:

units @ $1,440…………………………………

…

…

…

…

…

Date

InventoryPurchases

Date

Cost of Merchandise SoldPurchases

$ 25,920

18

6-12

CHAPTER 6 Inventories

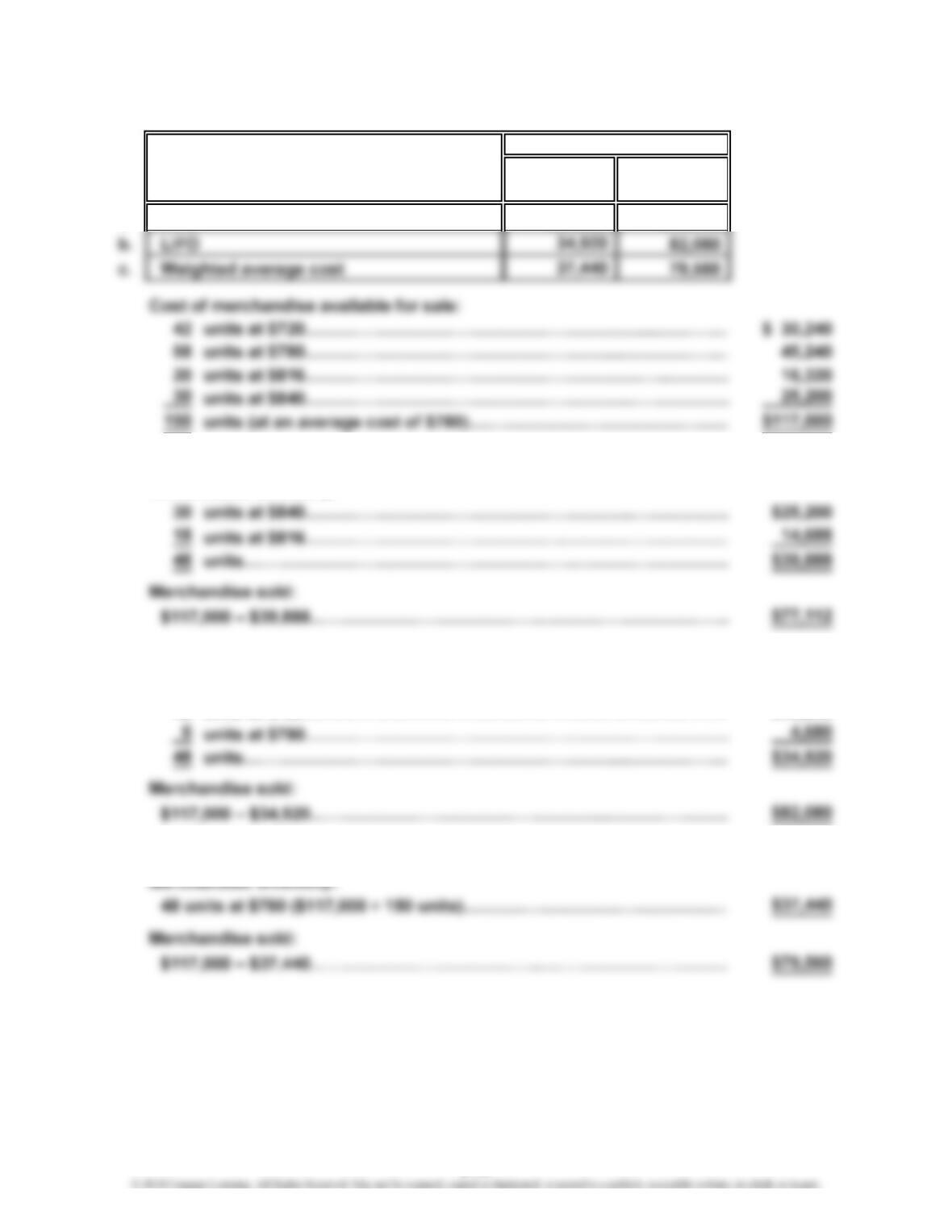

Ex. 6–13

Merchandise Merchandise

Inventory Method Inventory Sold

a. FIFO $39,888 $77,112

a. First-in, first-out:

Merchandise inventory:

…

b. Last-in, first-out:

Merchandise inventory:

42 units at $720…………………………………………………………………

…

$30,240

c. Weighted average cost:

Cost

6-13

…

…

CHAPTER 6 Inventories

Ex. 6–14

a. 1. FIFO inventory > (greater than) LIFO inventory

b. In periods of rising prices, the income shown on the company’s tax return

Ex. 6–15

Unit Unit

Inventory Cost Market Lower of

Quantity Price Price Cost Market C or M

77 $40 $39 $ 3,080 $ 3,003 $ 3,003

Ex. 6–16

The merchandise inventory would appear in the Current Assets section, as

follows:

Commodity

C300

Total

6-14

CHAPTER 6 Inventories

Ex. 6–17

a.

Merchandise inventory*………………………………………

…

$13,850 understated

Current assets…………………………………………………

…

$13,850 understated

Ex. 6–18

a.

Merchandise inventory*………………………………………

…

$21,600 overstated

…

b.

Cost of merchandise sold……………………………………

…

$21,600 understated

…

d. The December 31, 2015, balance sheet would be correct, since the 2014

Balance Sheet

Balance Sheet

Income Statement

6-15

…

…

CHAPTER 6 Inventories

Ex. 6–19

When an error is discovered affecting the prior period, it should be corrected. In

this case, the merchandise inventory account should be debited and the retained

Ex. 6–20

6-16

CHAPTER 6 Inventories

Ex. 6–21

c. If Winn-Dixie matched Kroger’s days’ sales in inventory, then its hypothetical

ending inventory would be determined as follows,

Thus, the additional cash flow that would have been generated is the difference

between the actual average inventory and the hypothetical average inventory,

as follows:

Actual average inventory……………………………………

…

$661.5 million

12.9

=

($4,966 + $4,935) ÷ 2

Inventory Turnover = Cost of Goods Sold

Average Inventory

Number of Days’ Sales in Inventory

Kroger: $63,927 =

a.

Cost of Goods Sold ÷ 365

Average Inventory

Number of Days’ Sales in Inventory = Average Inventory

Cost of Goods Sold ÷ 365

6-17

CHAPTER 6 Inventories

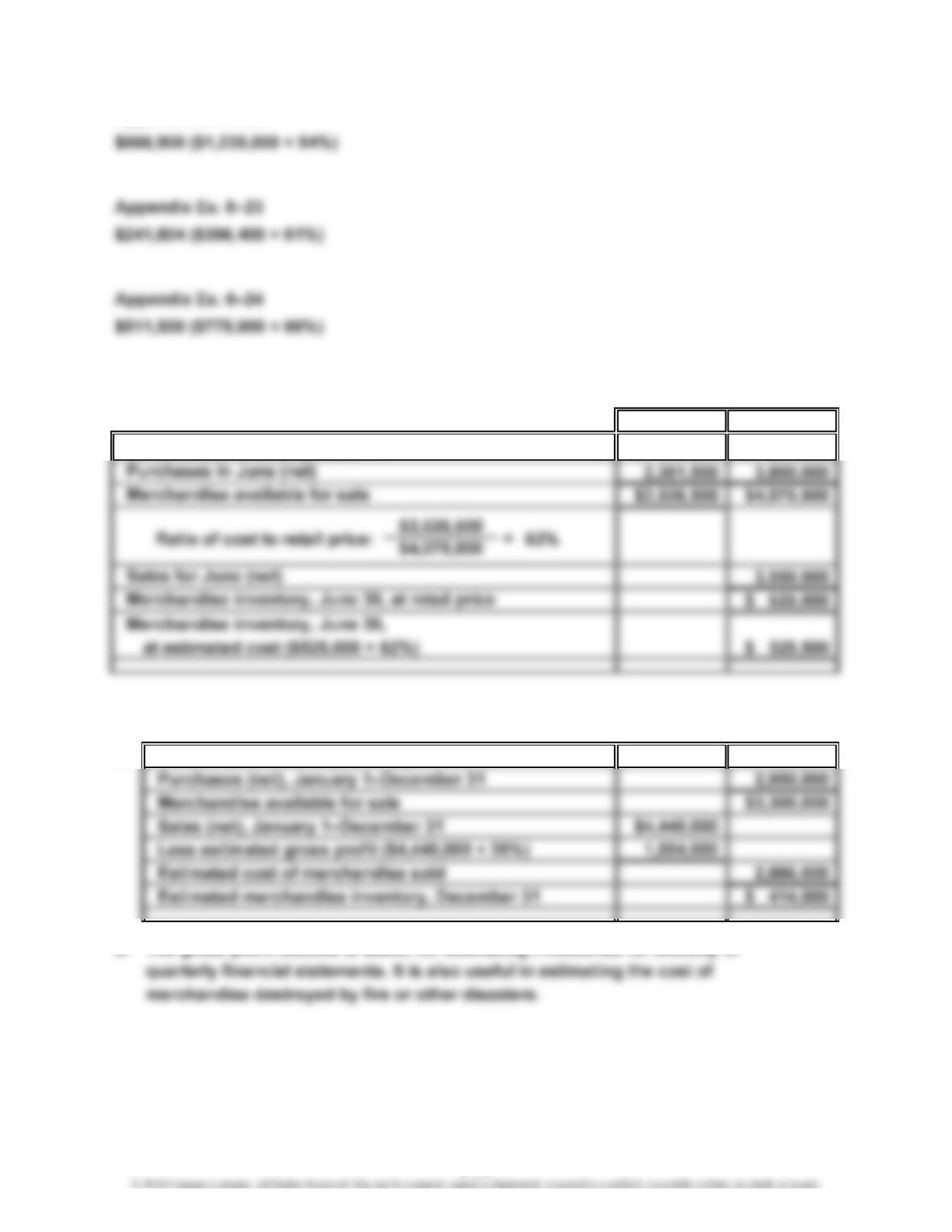

Appendix Ex. 6–22

Appendix Ex. 6–25

Cost Retail

Merchandise inventory, June 1 $ 165,000 $ 275,000

Appendix Ex. 6–26

a. Merchandise inventory, January 1 $ 350,000

b. The gross profit method is useful for estimating inventories for monthly or

6-18

CHAPTER 6 Inventories

Appendix Ex. 6–27

Merchandise available for sale………………………………………………………… $6,125,000

6-19

CHAPTER 6 Inventories

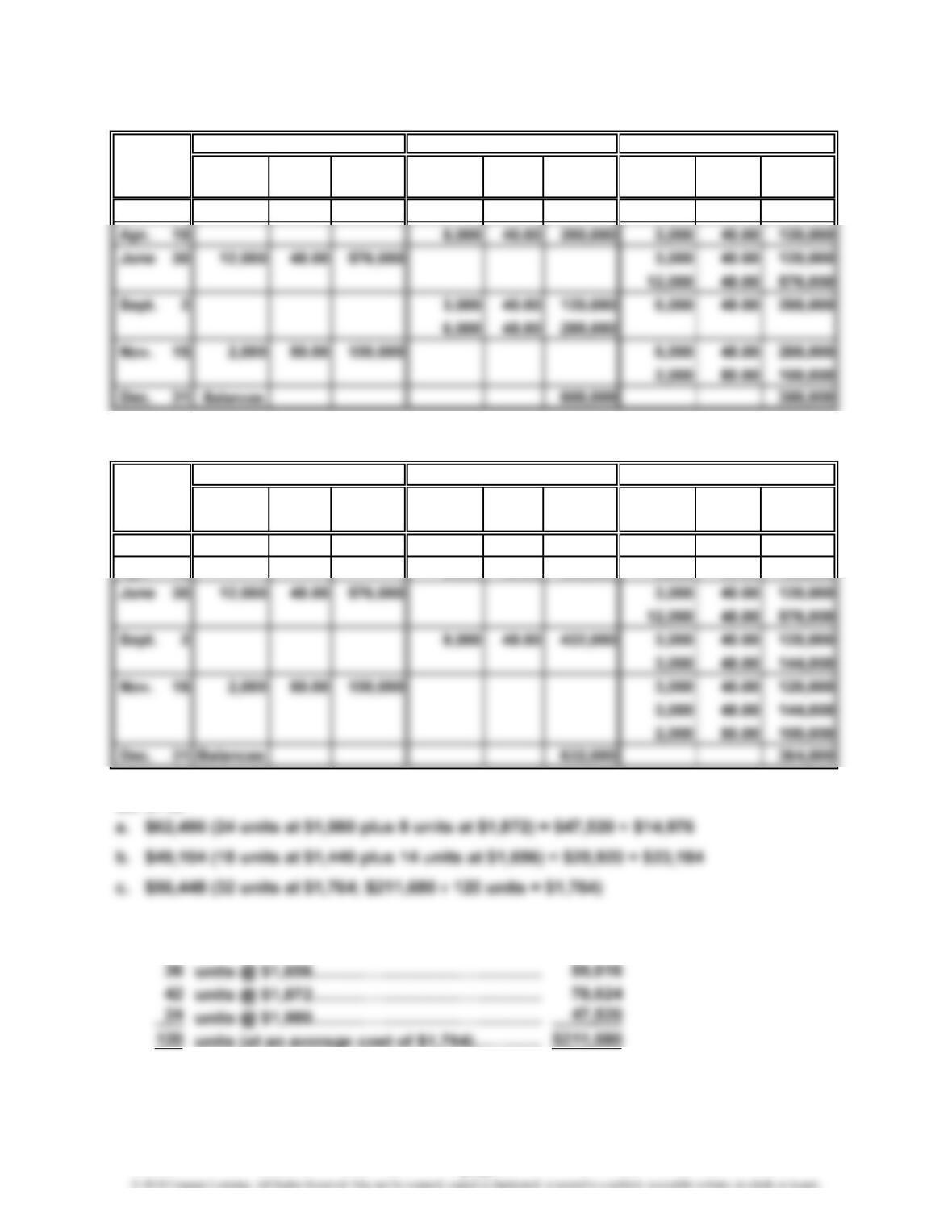

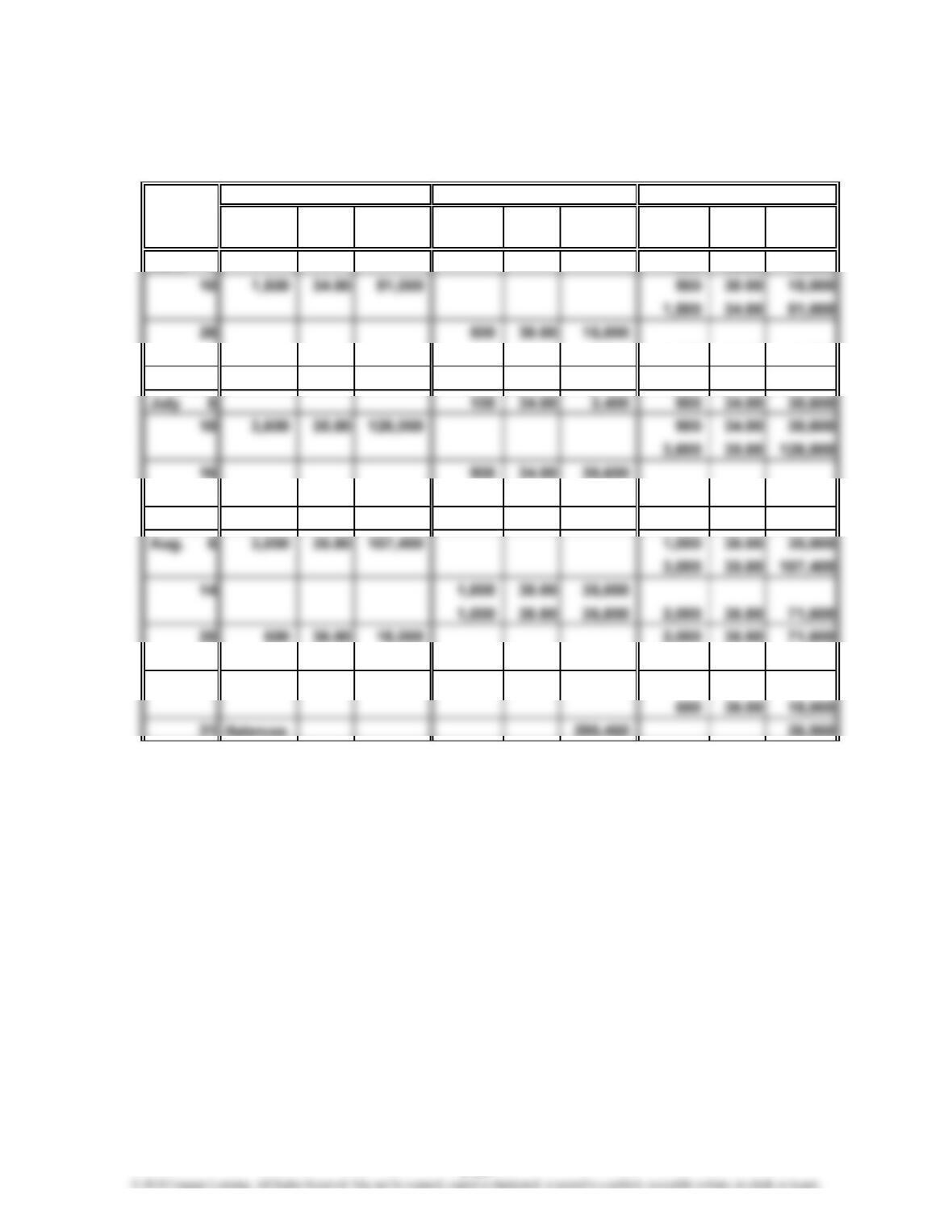

Prob. 6–1A

1.

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

June 1 500 30.00 15,000

250 34.00 8,500 1,250 34.00 42,500

30 250 34.00 8,500 1,000 34.00 34,000

900 35.00 31,500 2,700 35.00 94,500

28 1,700 35.00 59,500 1,000 35.00 35,000

500 36.00 18,000

30 1,750 35.80 62,650 250 35.80 8,950

PROBLEMS

2014

Date

Purchases Cost of Merchandise Sold Inventory

6-20