16

PROBLEMS

P1–1

1. UTAH TRAVEL SERVICE

Income Statement

For the Year Ended April 30, 20Y6

Fees earned …………………………………………………………… $ 1,594,200

Operating expenses:

Wages expense …………………………………………………. $890,200

2. UTAH TRAVEL SERVICE

Retained Earnings Statement

For the Year Ended April 30, 20Y6

Retained earnings, May 1, 20Y5………………………………. $ 300,000

Net income for the year ………………………………………….. $250,000

Less dividends ………………………………………………………. 75,000

Increase in retained earnings …………………………………. 175,000

Retained earnings, April 30, 20Y6 …………………………... $ 475,000

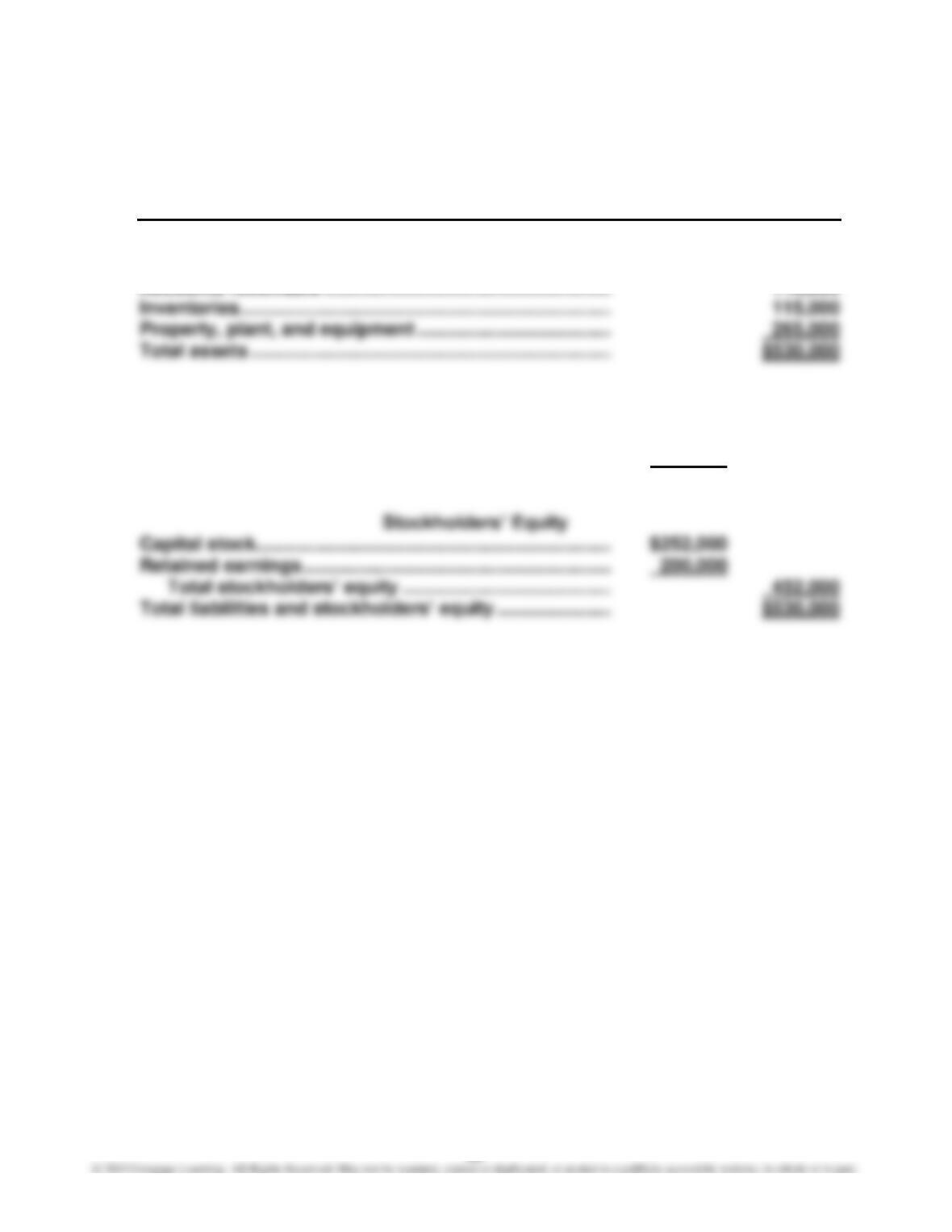

3. UTAH TRAVEL SERVICE

Balance Sheet

April 30, 20Y6

Assets

Cash ……………………………………………………………………… $ 428,300

Accounts receivable ………………………………………………. 188,100

P1–2

1. Realty businesses, such as Paradise Realty, are service businesses that aid

their clients in buying or selling real estate.

2. a. Wages expense, $29,850 ($69,300 – $14,400 – $12,000 – $8,100 – $4,950)

b. Net income, $80,000 ($149,300 – $69,300)

c. Net income for November, $80,000

d. Dividends, $36,000

18

P1–3

1. TARGET CORPORATION

Income Statement

For the Year Ended January 28, 20Y2

(in millions)

Sales …………………………………………………………………….. $68,466

Other credit card revenue ……………………………………… 1,399

Total revenue ……………………………………………………. $69,865

2. TARGET CORPORATION

Retained Earnings Statement

For the Year Ended January 28, 20Y2

(in millions)

Retained earnings, January 29, 20Y1 ………………………. $ 12,698

Add net income ……………………………………………………… $2,929

19

P1–3, Concluded

3. TARGET CORPORATION

Balance Sheet

January 28, 20Y2

(in millions)

Assets

Cash ……………………………………………………………………… $ 794

Receivables …………………………………………………………… 5,927

Liabilities

Accounts payable ………………………………………………….. $ 6,857

Debt and other borrowings……………………………….. 17,483

Other liabilities ………………………………………………………. 6,469

Total liabilities …………………………………………………… $30,809

20

P1–4

GOOGLE INC.

Statement of Cash Flows

For the Year Ended December 31, 20Y1

(in millions)

Net cash flows from operating activities …………………………... $ 14,565

Cash flows from investing activities:

Cash purchases for property, plant, and equipment, etc. $(67,787)

Receipts from sale of investments (net) ………………………. 48,746

Net cash flows used for investing activities …………………. (19,041)

21

P1–5

1. CASSANDRA CORPORATION

Income Statement

For the Year Ended December 31, Year 1

Revenue:

Sales …………………………..……………………………………. $800,000

2. CASSANDRA CORPORATION

Retained Earnings Statement

For the Year Ended December 31, Year 1

Retained earnings, January 1, Year 1 ……………………… $ 0

Net income ……………………………………………………………. $230,000

22

P1–5, Continued

3. CASSANDRA CORPORATION

Balance Sheet

December 31, Year 1

Assets

Cash ……………………………………………………………………. $ 40,000

Accounts receivable ………………………………………………. 110,000

Liabilities

Accounts payable …………………………………………………. $ 20,000

Income taxes payable ……………………………………………. 8,000

Note payable (due in 2019) ……………………………………… 50,000

Total liabilities …………………………………………………… $ 78,000

P1–5, Concluded

4. CASSANDRA CORPORATION

Statement of Cash Flows

For the Year Ended December 31, Year 1

Cash flows from operating activities:

Cash receipts from operating activities ……………… $ 690,000

Cash payments for operating activities ………………. (657,000)

Net cash flows from operating activities …………………. $ 33,000

Net cash flows from financing activities …………………. 272,000

Net increase in cash during Year 1 …………………………. $ 40,000

Cash as of January 1, Year 1 ………………………………….. 0

Cash as of December 31, Year 1 ……………………………… $ 40,000

Note to Instructors: The determination of cash receipts and payments from

operating activities is not discussed in Chapter 1 and is beyond the student

level of understanding or comprehension at this point in the text. This topic

24

FINANCIAL ANALYSIS

FA1–1

1. $6,644

2. $3,784

The markup percentage is computed as follows:

Cost of Sales + (Markup % × Cost of Sales) = Sales

$3,784 + (Markup % × $3,784) = $6,644

Markup % =

=

$3,784

$3,784 –– $6,644

=

$3,784

$2,860

= 75.6% (Rounded)

FA1–2

1. 68.7% ($366 ÷ $533) (Rounded)

2. 45.6% (Rounded)

The markup percentage is computed as follows:

3. 8.3% ($44 ÷ $533) (Rounded)

4. Rate of Return on Assets = $61 ÷ $858 = 7.1%

FA1–2, Concluded

5. Hershey’s markup percentage of 75.6% is significantly higher than Tootsie

Roll’s markup percentage of 45.6%. As a result, Hershey earns 9.9 cents per

FA1–3

1. Note to Instructors: The purpose of this requirement is to get students think-

ing about businesses and their profitability. This is done by focusing on real-

2. Pfizer:

Rate of Return on Total Assets = $12,762 ÷ [($195,014 + $188,002) ÷ 2]

= $12,762 ÷ $191,508 = 6.7%

3. Microsoft has the highest rate of return on total assets of 19.4%. This is due

to the widespread acceptance and use of its products. However, in recent

years Microsoft has been challenged by Google and others. Ford has the next

FA1–4

1. Note to Instructors: The purpose of this requirement is to get students think-

ing about businesses and their profitability. This is done by focusing on real-

2. ExxonMobil:

Rate of Return on Total Assets = $73,504 ÷ [($302,510 + $331,052) ÷ 2]

= $73,504 ÷ $316,781 = 23.2%

Coca-Cola:

Rate of Return on Total Assets = $11,856 ÷ [($72,921 + $79,974) ÷ 2]

= $11,856 ÷ $76,448 = 15.5%

3. ExxonMobil has the highest rate of return on total assets of 23.2%. This is due

to the high demand for petroleum based products. At the same time, Exxon–

Mobil’s operations have the most risks. These risks include such factors as

FA1–5

1. Rate of Return on Total Assets = $5,325 ÷ [($43,705 + $46,630) ÷ 2]

= $5,325 ÷ $45,168 = 11.8%

2. Target’s rate of return on total assets of 11.8% is lower than Walmart’s rate of

return of 14.3%. Target’s recent strategy of adding more upscale merchandise

27

CASES

Case 1–1

Management’s actions are ethical. Management has a responsibility to the com-

pany’s stockholders to remain competitive and profitable. Similarly, many com-

Case 1–2

1. Acceptable professional conduct requires that Loretta Smith supply City

National Bank with all the relevant financial statements necessary for the

2. a. Owners are generally willing to provide bankers with information about

the operating and financial condition of the business, such as the follow-

ing:

Operating Information:

• description of business operations

• results of past operations

28

Case 1–2, Concluded

the business or future plans to expand operations into areas that are not

currently served by a competitor.

Case 1–3

1. In a commodity business like poultry production, the dominant business em-

phasis is a low-cost emphasis. This is because customers cannot differenti-

ate between chickens produced by different companies. The implication of a

2. A major business risk includes the selling of contaminated chickens and the

possibility that competitors will develop lower-cost methods of breeding and

raising chickens. Also, a major cost of raising chickens is the cost of feed.

3. The company could try to differentiate its products by emphasizing that it

raises its chickens with only “natural” feeds without the use of artificial in-

gredients such as steroids, etc. The company could then sell its products as

the “healthy choice” products and probably use a premium-price strategy.

29

Case 1–4

The difference in the two bank balances, $175,000 ($215,000 – $40,000), may not

be pure profit from an accounting perspective. To determine the accounting profit

for the 8-month period, the revenues for the period would need to be matched

with the related expenses. The revenues minus the expenses would indicate

whether the business generated net income (profit) or a net loss for the period.

Case 1–5

Note to Instructors: The purpose of this activity is to show students that the

accounting equation has real world impact. By illustrating how the accounting

equation applies to well-known companies, the importance of accounting and the

concepts discussed in this chapter are emphasized to students.

30

Case 1–6

As can be seen from the balance sheet data in the case, Enron was financed

largely by debt as compared to equity. Specifically, Enron’s stockholders’ equity

represented only 17.5% ($11,470 ÷ $65,503) of Enron’s total assets. The remainder

of Enron’s total assets, 82.5%, was financed by debt. When a company is fi-

nanced largely by debt, it is said to be highly leveraged.

After the allegations of misstatements became public, Enron’s stock rapidly de-

clined and the company filed for bankruptcy. Subsequently, numerous lawsuits

were filed against the company and its management. In addition, the Securities

and Exchange Commission, the Justice Department, and Congress launched in-

vestigations into Enron. As a result, several of Enron’s top executives were crim-

inally prosecuted and were sentenced to prison.