CHAPTER 1 Introduction to Accounting and Business

Prob. 1-5B (Continued)

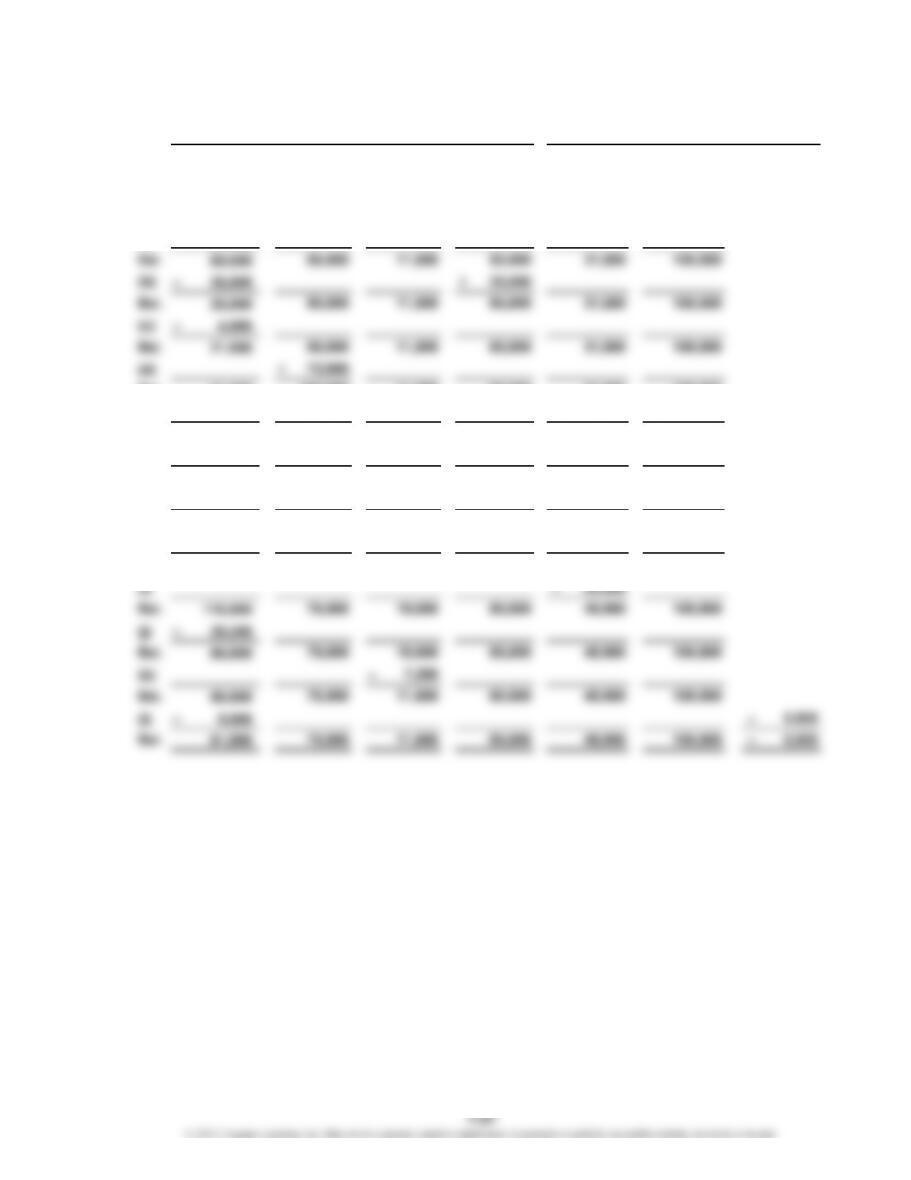

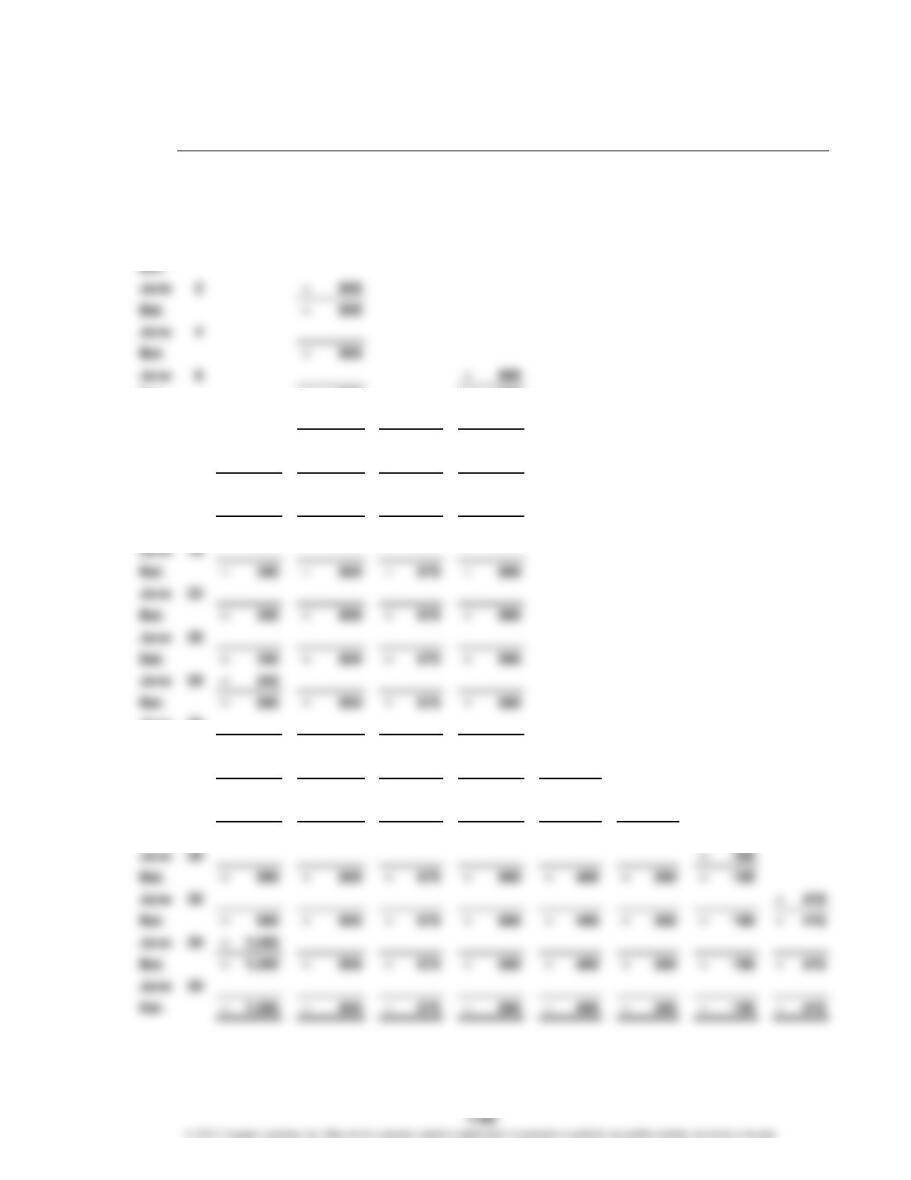

2. = +

+++=+ –

Bal. 39,000 80,000 11,000 50,000 31,500 148,500

(a) + 21,000 + 21,000

Bal. 21,000 152,000 11,000 85,000 31,500 169,500

(e)

–

20,000 – 20,000

Bal. 1,000 152,000 11,000 85,000 11,500 169,500

(f) + 8,000 +8,000

Bal. 1,000 152,000 19,000 85,000 19,500 169,500

(g) + 38,000

Bal. 39,000 152,000 19,000 85,000 19,500 169,500

(h) + 77,000 – 77,000

Bal. 116,000 75,000 19,000 85,000 19,500 169,500

–

–

Owner’s Equity

Accts.

PayableCash

Assets

Accts.

Rec.

Liabilities

Supplies Land

Beverly

Zahn,

Capital

Beverly

Zahn,

Drawing

–

–

CHAPTER 1 Introduction to Accounting and Business

Prob. 1-5B (Continued)

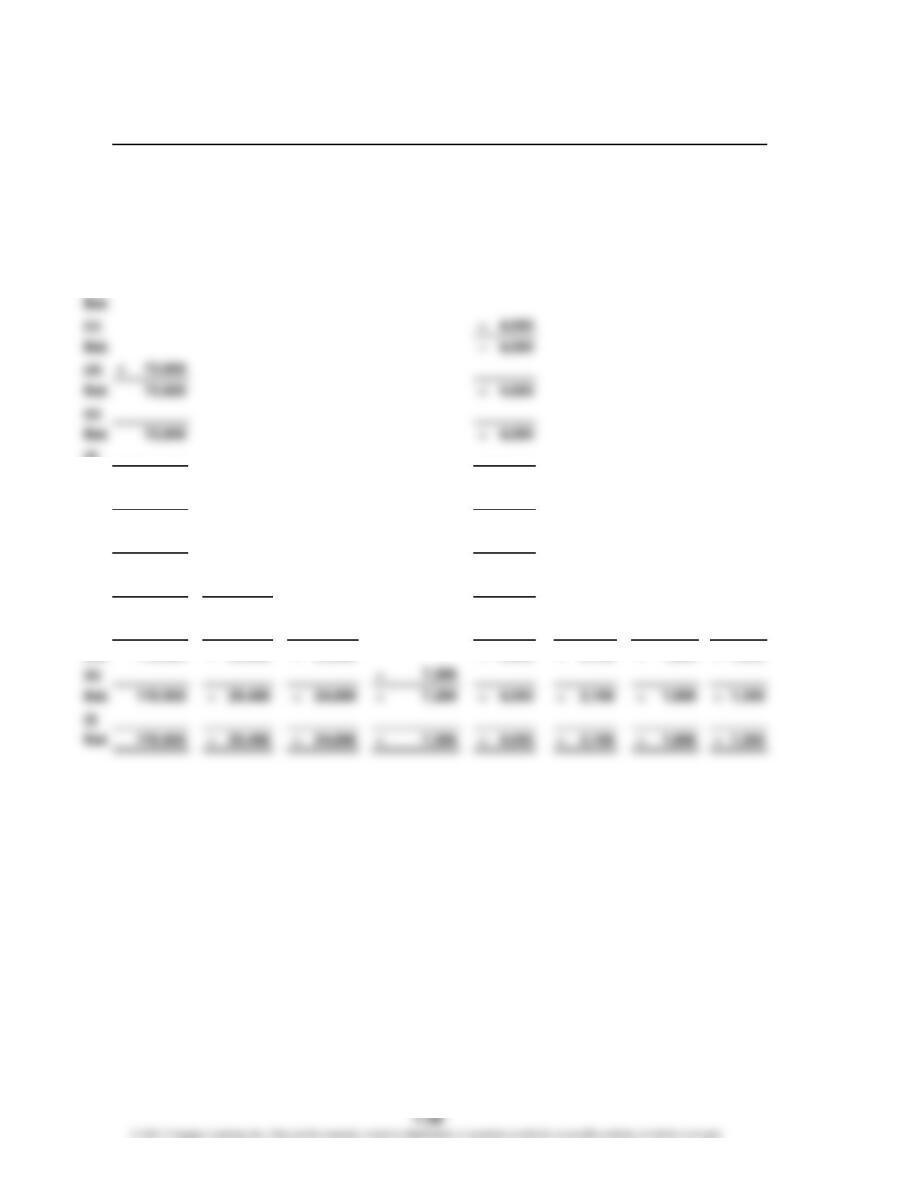

+–––

Supplies

Exp. ––– –

Bal.

(a)

Bal.

(b)

(f)

Bal. 72,000 –4,000

(g) + 38,000

Bal. 110,000 –4,000

(h)

Bal. 110,000 –4,000

(i) – 29,450

Bal. 110,000 –29,450 –4,000

(j) – 24,000 –2,100 –1,800 –1,300

Owner’s Equity (Continued)

Utilities

Exp.

Dry

Cleaning

Revenue

Dry

Cleaning

Exp.

Wages

Exp.

Rent

Exp.

Truck

Exp.

Misc.

Exp.

CHAPTER 1 Introduction to Accounting and Business

Prob. 1-5B (Continued)

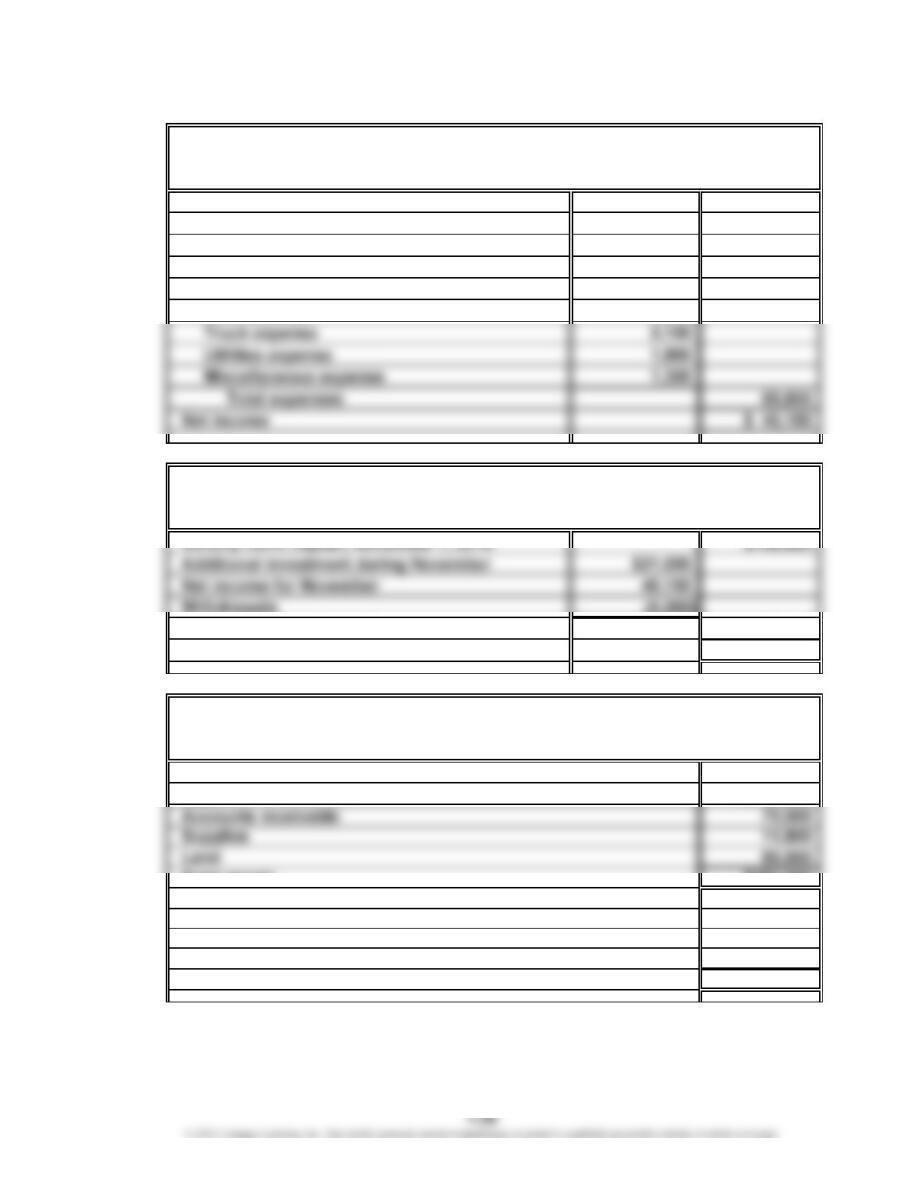

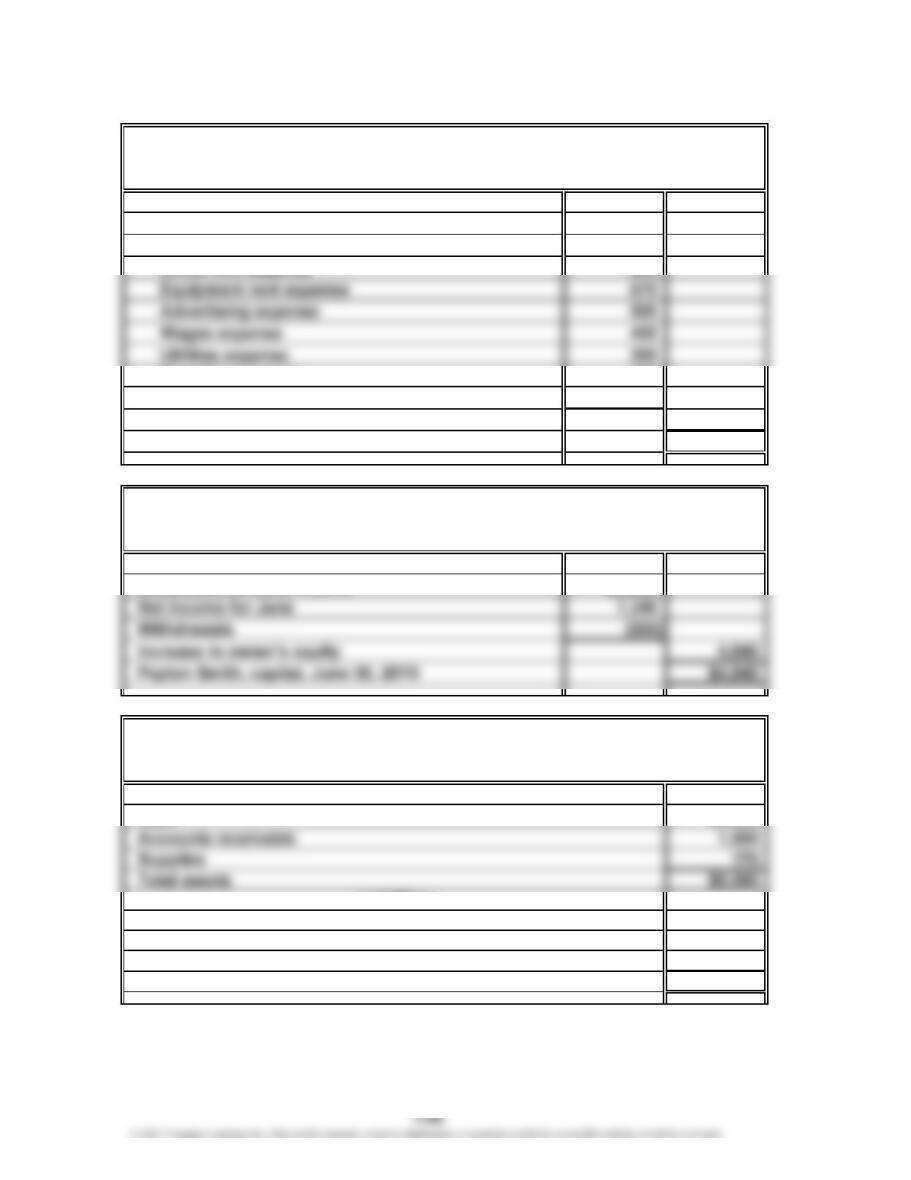

3.

Dry cleaning revenue $110,000

Expenses:

Dry cleaning expense $29,450

Wages expense 24,000

Supplies expense 7,200

Rent expense 4,000

Withdrawals (5,000)

Increase in owner’s equity 56,150

Beverly Zahn, capital, November 30, 20Y6 $204,650

Cash $ 81,800

Total assets $253,600

Accounts payable $ 48,950

Beverly Zahn, capital 204,650

Total liabilities and owner’s equity $253,600

Assets

Liabilities

Owner’s Equit

y

Bev’s Dry Cleaners

Income Statement

For the Month Ended November 30, 20Y6

Bev’s Dry Cleaners

Statement of Owner’s Equity

For the Month Ended November 30, 20Y6

Bev’s Dry Cleaners

Balance Sheet

November 30, 20Y6

CHAPTER 1 Introduction to Accounting and Business

Prob. 1-5B (Concluded)

4. (Optional)

Cash flows from (used for) operating activities:

Cash received from customers* $115,000

Cash paid for expenses and to creditors** (53,200)

Net cash flows from operating activities $ 61,800

Cash flows from (used for) investing activities:

Cash paid for purchase of land (35,000)

*$38,000 + $77,000; these amounts are taken from the Cash column of the spreadsheet

in Part 2.

** $4,000 + $20,000 + $29,200; these amounts are taken from the Cash column of the

spreadsheet in Part 2.

Bev’s Dry Cleaners

Statement of Cash Flows

For the Month Ended Novemer 30, 20Y6

CHAPTER 1 Introduction to Accounting and Business

Prob. 1-6B

a. Wages expense, $203,200 ($288,000 – $48,000 – $17,600 – $14,400 – $4,800)

b. Net income, $112,000 ($400,000 – $288,000)

f. Withdrawals, $64,000; from statement of cash flows

g. Increase in owner’s equity, $208,000 ($160,000 + $112,000 – $64,000)

h. LuAnn Martin, capital, May 31, 20Y3, $208,000

i. Land, $120,000; from statement of cash flows

l. Total liabilities and owner’s equity, $256,000 ($48,000 + $208,000)

m. Cash received from customers, $400,000; this is the same as fees earned

since there are no accounts receivable.

n. Net cash flows from operating activities, $147,200 ($400,000 – $252,800)

CHAPTER 1 Introduction to Accounting and Business

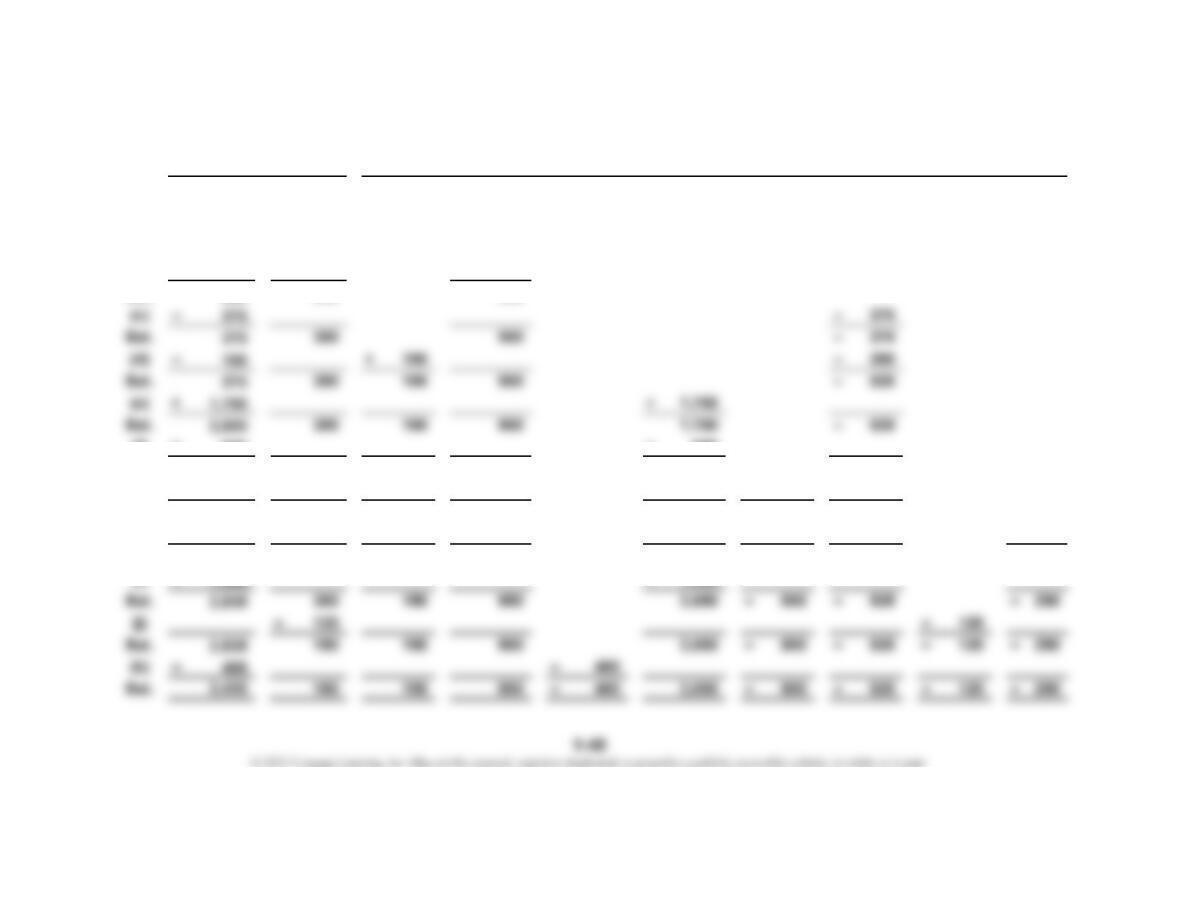

1. = +

++=+–+

June 1 + 4,000 + 4,000

June 2 + 3,500 + 3,500

Bal. 7,500 4,000 3,500

Bal. 6,200 350 350 4,000 3,500

June 8 – 675

Bal. 5,525 350 350 4,000 3,500

Bal. 5,375 350 250 4,000 3,800

June 22 + 1,000 + 1,000

Bal. 5,375 1,000 350 250 4,000 4,800

June 25 + 500 + 500

Bal. 5,875 1,000 350 250 4,000 5,300

June 29 – 240

Bal. 5,635 1,000 350 250 4,000 5,300

June 30 + 900 + 900

Bal. 6,535 1,000 350 250 4,000 6,200

June 30 – 400

Bal. 6,135 1,000 350 250 4,000 6,200

CONTINUING PROBLEM

Peyton

Smith,

Drawing

Owner’s Equity

Accts.

PayableCash

Assets

Accts.

Rec.

Liabilities

Supplies

Peyton

Smith,

Capital

Fees

Earned

CHAPTER 1 Introduction to Accounting and Business

Continuing Problem (Continued)

– – –– ––––

June 1

June 2

Bal. – 800 – 500

June 8 – 675

Bal. – 800 – 675 – 500

June 12 – 350

Bal. – 350 – 800 – 675 – 500

June 13

Bal. – 350 – 800 – 675 – 500

June 30

Bal. – 590 – 800 – 675 – 500

June 30 – 400

Bal. – 590 – 800 – 675 – 500 – 400

June 30 – 300

Bal. – 590 – 800 – 675 – 500 – 400 – 300

Misc.

Exp.

Owner’s Equity (Continued)

Supplies

Exp.

Wages

Exp.

Music

Exp.

Office

Rent

Exp.

Equip.

Rent

Exp.

Adver-

tising

Exp.

Utilities

Exp.

CHAPTER 1 Introduction to Accounting and Business

Continuing Problem (Concluded)

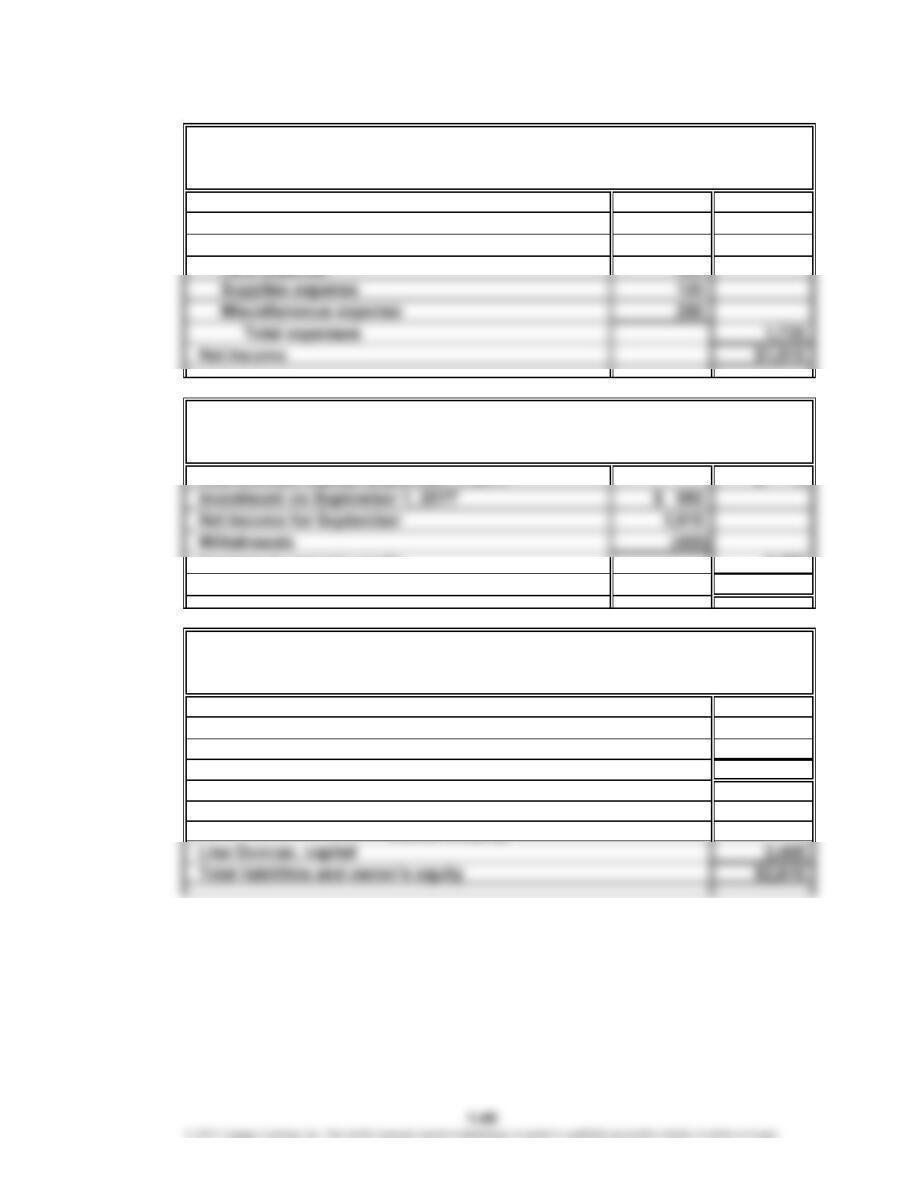

2.

Fees earned: $6,200

Expenses:

Music expense $1,590

Supplies expense 180

Miscellaneous expense 415

Total expenses 4,860

Net income $1,340

3.

Peyton Smith, capital, June 1, 20Y9 $0

4.

Accounts payable $ 250

Peyton Smith, capital 4,840

Total liabilities and owner’s equity $5,090

Assets

Liabilities

Owner’s Equity

PS Music

Income Statement

For the Month Ended June 30, 20Y9

PS Music

Statement of Owner’s Equity

For the Month Ended June 30, 20Y9

PS Music

Balance Sheet

June 30, 20Y9

CHAPTER 1 Introduction to Accounting and Business

CP 1-1

1. The car repair is a personal expense and is Marco’s personal responsibility. By

2. The partnership’s net income will be reduced by the $2,000 Marco has taken.

This will reduce the amount of net income available to Marco’s partners.

CP 1-2

1. Acceptable professional conduct requires that Colleen Fernandez supply First

Federal Bank with all the relevant financial statements necessary for the bank

to make an informed decision. Therefore, Colleen should provide the complete

2. a. Owners are generally willing to provide bankers with information about the

operating and financial condition of the business, such as the following:

● Operating Information:

● Description of business operations

● Results of past operations

● Preliminary results of current operations

● Plans for future operations

● Financial Condition:

● List of assets and liabilities (balance sheet)

● Estimated current values of assets

CASES & PROJECTS

CHAPTER 1 Introduction to Accounting and Business

CP 1-2 (Concluded)

●Personal Financial Information. Owners may have little choice here

because banks often require owners of small businesses to pledge their

personal assets as security for a business loan. Personal financial

b. Bankers typically want as much information as possible about the ability

of the business and the owner to repay the loan with interest. Examples of

such information are described above.

c. Both bankers and business owners share the common interest of the

CP 1-3

A sample solution based on Nike Inc.’s Form 10-K for the fiscal year ended May 31,

2018, is as follows:

1. Nike, Inc.

2. Beaverton, Oregon

3. Mark G. Parker

4. Manufacturing

report or 10-K, we listed it as part of the answer.

CHAPTER 1 Introduction to Accounting and Business

CP 1-4

Example Memo

To: My Teacher

From: Ima Student

Date: January 1, 20XX

Re: Causes of Accounting Fraud

Business and accounting fraud typically result from either a failure of individual

character or a culture of greed within an organization. Managers and accountants

CP 1-5

The difference in the two bank balances, $55,000 ($80,000 – $25,000), may not be

pure profit from an accounting perspective. To determine the accounting profit for

to be paid for wages or other operating expenses, additional investments that Dr.

Cousins may have made in the business during the period, or withdrawals during

the period that Dr. Cousins might have taken for personal reasons unrelated to the

business.

Some businesses that have few, if any, receivables or payables may use a “cash”

basis of accounting. The cash basis of accounting ignores receivables and payables

CHAPTER 1 Introduction to Accounting and Business

CP 1-6

1.

=+

+ =+ – + ––––

(a) + 950 + 950

(b) – 300 + 300

Bal. 650 300 950

(f) + 600 + 600

Bal. 2,625 300 150 950 2,350 – 525

(g) – 800 – 800

Bal. 1,825 300 150 950 2,350 – 800 – 525

(h) – 290 – 290

Bal. 1,535 300 150 950 2,350 – 800 – 525 – 290

Owner’s Equity

Supplies

Accts.

Payable

Liabilities

Misc.

Exp.Cash

Lisa

Duncan,

Drawing

Supplies

Expense

Assets

Lisa

Duncan,

Capital

Fees

Earned

Rent

Expense

Salaries

Expense

CHAPTER 1 Introduction to Accounting and Business

CP 1-6 (Continued)

2.

Fees earned: $3,650

Expenses:

Salaries expense $800

3.

Increase in owner’s equity 2,465

Lisa Duncan, capital, September 30, 20Y7 $2,465

4.

Cash $2,435

Supplies 180

Total assets $2,615

Accounts payable $ 150

For the Month Ended September 30, 20Y7

Serve-N-Volley

Serve-N-Volley

Income Statement

For the Month Ended September 30, 20Y7

Serve-N-Volley

Statement of Owner’s Equity

Assets

Liabilities

Owner’s Equit

y

Balance Sheet

September 30, 20Y7

CHAPTER 1 Introduction to Accounting and Business

CP 1-6 (Concluded)

5. a. Serve-N-Volley would provide Lisa with $715 more income per month than

working as a waitress. This amount is computed as follows:

b. Other factors that Lisa should consider before discussing a long-term

arrangement with the Phoenix Tennis Club include the following:

Lisa should consider whether the results of operations for September are

indicative of what to expect each month. For example, Lisa should consider

whether club members will continue to request lessons or use the ball

machine during the fall months when interest in tennis may slacken. Lisa

should evaluate whether the additional income of $715 per month from

Serve-N-Volley is worth the risk being taken and the effort being expended.

Lisa should also consider how much her investment in Serve-N-Volley

could have earned if invested elsewhere. For example, if the initial

investment of $950 had been invested to earn a rate of return of 6%

per year, it would have earned $4.75 in September, or $57 for the year.

CP 1-7

Note to Instructors: The purpose of this activity is to familiarize students with the

certification requirements and their online availability. You might use this as an

opportunity to discuss the advantages and disadvantages of careers in public

accounting (CPA), management accounting (CMA), and internal auditing (CIA).

The following websites provide students with useful information (such as starting

salaries) on careers in accounting:

CP 1-8

First Second Third

Year Year Year

Net cash flows from (used for)

operating activities negative positive positive

Net cash flows from (used for)

Start-up companies normally experience negative net cash flows from operating

activities; however, Amazon.com was able to generate positive net cash flows

from operations by its second year. Start-up companies normally have negative